New Construction Starts May 2018 Near All-Time High

6-20-18

Dodge reported May new construction starts at a seasonally adjusted annual rate of $778,000 million, up 15% from April. Also, year-to-date starts total $294,000 million, 3% lower than the same 5 months of 2017.

However, 2018 numbers will not be revised until next year and 2017 numbers through May have already been revised up 13%, up about 18% in nonresidential and 6% in residential. So the potential that YTD numbers remain 3% below 2017 is very small. Revisions to previous year’s numbers have averaged more than +7% for the last 5 years with most of the upward revision in nonresidential.

Revisions to 2017 year-to-date have already resulted in a 4% increase in both 2018 and 2019 starting backlog.

Although Dodge, in its midyear report, is predicting 2017 starts at a total of $763,000 million, the current rate of revision seems to indicate 2017 starts could reach closer to $800,000 million. Forecast 2018 total starts will increase only slightly over 2017.

Keep in mind, unlike the Census spending data which captures 100% of all spending, the new starts data is a sampling of project starts, representing about 60% of total work volume. For this reason, the actual starts dollars cannot be used directly to represent spending. However, the change in predicted cash flow from starts can be used to predict the change in spending.

From Sept’17 through May’18 new construction starts reached the highest average since 2004 and are just below an all-time high. Residential starts posted the best 6 months average since 2006, up 8% from the prior 6 months. Both nonresidential buildings and non-building infrastructure are lower than recent highs. Both could finish the year with starts at a decline of 4% to 5% below 2017 totals, but they are both still near the best year of starts on record.

Starts totals near new highs is in current $. If 2004$ were represented in constant 2018$, the total would be 40% higher due to inflation. So, after adjusting for inflation, today we are still 40% below that 2004 high point.

- TOTAL All Construction Starting Backlog for 2018 reached an all-time high, increased 35% in the last three years, 14% in the last year.

- Nonresidential Buildings 2018 starting backlog is the highest ever, up 50% in four years, up 17% from 2017.

- Non-building Infrastructure 2018 starting backlog is the highest ever, up 45% in three years, up 16% from 2017.

- Residential work within the year comes mostly from new starts within the year, only 30% from starting backlog.

The erratic nature of new construction starts belies how smoothly those projects feed into backlog and monthly spending.

Backlog shows fairly constant growth for the last 5 or 6 years. Spending in any given month includes projects started and entered into backlog from 1 month ago to 3 or 4 years ago. In some non-building cases, projects are in backlog for 6 to 8 years, so project starts that appear as a high spike enter backlog and spending and produce a constant upward slope. Most spending within the year in nonresidential work comes from backlog. Most spending in residential work comes from new starts.

The cash flow model of all previous jobs underway already in backlog and all new starts shows the current predicted spending. Starting backlog for 2018 plus new starts in 2018 minus all spending in 2018 generates the forecast work remaining in backlog for the start of 2019.

The predicted spending plot will be added here after July 1 Census spending release.

Much more to come in next few days. edz

Construction Spending April 2018 – 6-1-18

6-1-18

Construction Spending for April is up 1.8% from March and up 6.6% Year-to-date (YTD) from 2017. Both Feb. and Mar. were revised up slightly.

YTD$ Jan-Apr 2018 vs 2017 > Residential +8.7%, Nonresidential Buildings +6.0%, Nonbuilding Infrastructure +3.7%. Public +7.6%, Private +6.3%.

https://www.census.gov/construction/c30/pdf/release.pdf

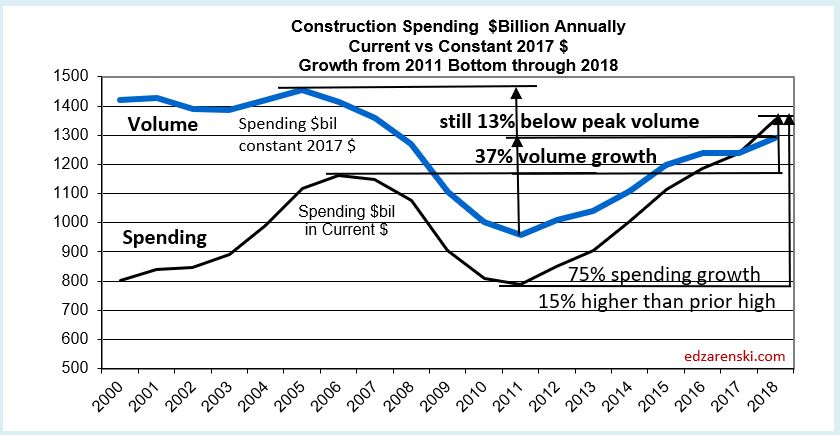

Spending in current $ has reached a new high of $1,310 billion surpassing the previous high spending from 2006. But after adjusting for inflation, constant $ shows volume is still 13% below the 2005 peak.

Census is reporting a 1.8% mo/mo gain from March. I am not seeing such a huge jump in April construction spending over March. My data shows very slight growth from Mar to Apr, possibly because my SAAR factor produces a much higher SAAR for March than the Census factor. The Census factor, which appears unusually low in March, lowers March (to a decline) and increases April growth.

Year-to-date indicators are often a better indicator of a growth trend than mo/mo comparisons. But, YTD can be deceiving. When both years being compared have similar slope to spending growth, YTD works well. But if one year has a declining slope and the other year an increasing slope, YTD values can vary widely from expected annual total yr/yr growth.

For example, Manufacturing shows YTD growth from 2017 is down 4.1% through April. Monthly spending in 2017 trended down most of the year starting at the highest, $74bil in Q1 2017, dipping as low as $61bil in Dec. For 2018, just the opposite trend is taking place. 2018 started in Jan at a rate of $65bil and is projected to finish the year at $72bil.

This means YTD comparisons for 2018 vs 2017 will start out at the lowest percent change for the year (-4.1%) and finish with 2018 values increasing and 2017 values decreasing. By the 4th quarter the mo$2018/mo$2017 could reach +20%. That diverging trend will continually move the average YTD up such that, for the first half of the year, YTD gives no clear indication of the expected annual performance.

Similar patterns, or at least partially similar patterns, can be found in Office, Educational, Power and Amusement/Recreation.

Overall, this indicates construction spending will experience an improving picture through the year. I’m predicting total YTD performance will increase every month into the 4th quarter. From April to September 2017, total monthly spending was declining. In 2018, for this same period, spending is predicted to increase every month. This will result in rapidly increasing YTD percents during this period. YTD will increase from 6.6% in April to 9% in the 3rd quarter. Even if spending were to realize no additional gains in 2018, the YTD% would still increase from now into the 4th quarter, because 2017 values declined.

The latest data comes in as expected, so does not appreciably change my outlook. I’m still forecasting 8% to 10% growth across all sectors and I expect 2018 will reach a total $1,350 billion in spending.

The outlook is particularly strong for Residential, Educational, Amusement, Office and Transportation. Transportation may exceeding 25% growth. Highway/Bridge and Healthcare growth will be limited.

MORE TO COME

Notes on March 2018 Construction Spending 5-2-18

Construction Economic Activity Notes 4-25-18

Construction Economics Brief Notes 3-10-18

2018 Construction Spending Forecast – Mar 2018