Nonres Bldgs Construction Spending Midyear 2017 Forecast

7-24-17

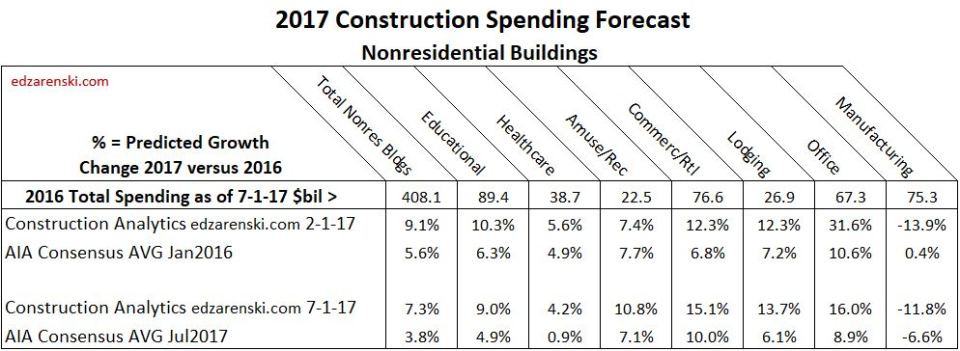

The AIA recently published the Nonresidential Buildings Consensus Forecast Midyear 2017 report. The consensus of seven firms projects spending growth for nonresidential buildings at 3.8% for 2017 and 3.6% for 2018. The largest growth in the AIA forecast for any building type for both years is 10% for 2017 Retail & Other Commercial. The highest reported total annual prediction from any firm is 4.4% for 2017 and 5.5% for 2018. AIA Midyear Consensus Report July 2017

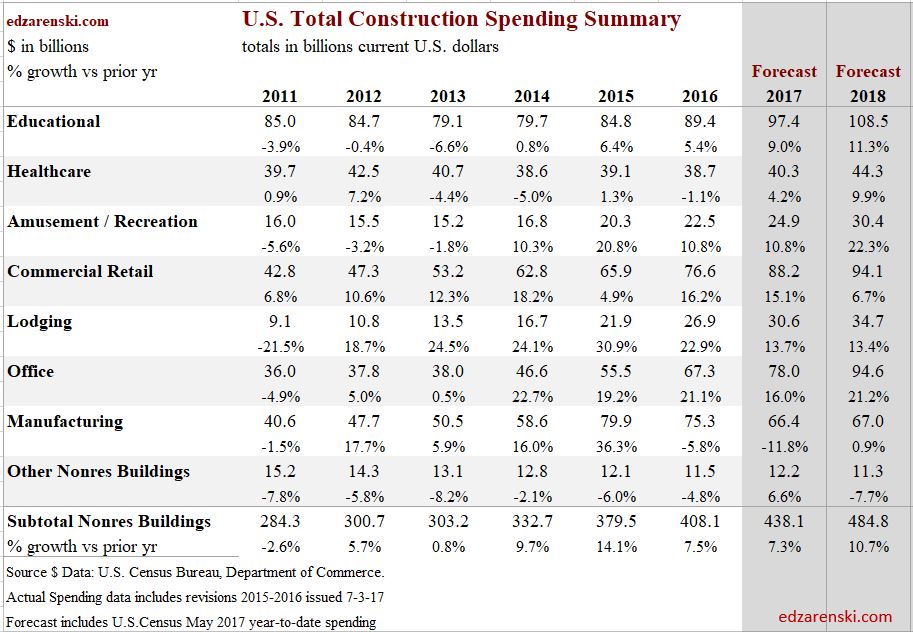

Construction Analytics forecast for nonresidential buildings construction spending growth is +7.3% for 2017 and +10.7% for 2018. Growth in 2016 was 7.5%.

Year-to-date (YTD) spending for the 1st 5 months of 2017 is up +5.2%, led by Office and commercial, both near 15%. Estimate-to-complete (ETC) for the final 7 months is forecast at +8.1%. Total spending for Nonresidential Buildings in 2017 is forecast to increase 7.3% = $438 billion.

If spending were to slow to 3.8% growth for 2017, since YTD growth is already 5.2%, the rate of growth in the final 7 months would need to fall to only 2.4%. However, the predicted cash flow from construction starts shows very strong spending growth in the 2nd half 2017 and into 2018. Nonresidential Buildings construction starts for the last 12 months posted the highest average since 2007-2008. This is helping boost spending.

Outside of recession years, nonresidential buildings construction spending for the year dropped below 4% annual growth only twice in 24 years, since data has been tracked. In fact, right now spending needs to grow at 4.5% just to stay ahead of construction inflation. So any forecast of spending growth below 4.5% actually might suggest that construction is not expanding, but is contracting. All indications are that there are no recessionary effects right now and economic activity does not suggest we are headed for a non-recession low spending for nonresidential building construction. I don’t expect spending to drop to 4% growth for the next three years.

The pattern of nonresidential buildings construction starts for the last 30 months is indicating spending increases in the 2nd half of 2017 and is setting up 2018 for the highest ever starting backlog and record spending. Even if starts crash to zero growth for the remainder of the year, 2017 spending would drop by less than 1% and we still begin 2018 with record backlog.

New Office construction starts for the last 12 months are the best ever recorded, on track to reach a total 50% growth over two years. Retail/Commercial starts have averaged year-over-year (YOY) growth of greater than 10%/year for the last three years. Educational starts averaged YOY growth of 8%/year for the last two years. These three markets comprise 60% of all nonresidential buildings. Healthcare starts have quietly increased to a record high over the last 12 months. Every market except manufacturing will finish 2017 with new starts totals near or at post recession highs. Manufacturing reached record high starts in 2014 and record spending in 2015. All construction starts $ data in this report references Dodge Data & Analytics starts data.

Construction spending for Commercial/Retail, Lodging and Office construction all remain very strong with 2017 total growth near 15%. Educational (+9%) and healthcare (+4%) both show sizable gains after years of little to no growth.

92% of all construction spending in 2017 is already in backlog projects.

A scenario that would have Office spending drop down to 8.9% annual growth from the track it is on today (+15.4% YTD) would require a highly improbable and unprecedented non-recessionary decline in spending in the remaining months of 2017. To grasp the enormity of the decline needed, it would take canceling 8% of all ongoing office projects or new starts for the remainder of the year would need to drop by 50%.

Educational will show an increase in YTD gains in the 3rd quarter because increasing spending in 2017 will be measured against the lowest quarter (3rdqtr) in 2016. Healthcare may not show sizable YTD gains until 4th quarter, for which 2016 reached lowest spending of the year and 2017 will reach highest.

Total nonresidential buildings spending growth accelerates to 10+% in 2018, led by institutional and office spending.

Nearly all nonresidential buildings construction starts in 2016 are still contributing to spending. Since originally posted they have been revised up by 16%. Since most spending from new starts (approximately 50%) occurs in the year following the start, early spending projections based on original posted starts $ may understate 2017 spending.

Nonresidential construction is comprised of two very different sectors, nonresidential buildings and non-building infrastructure. Infrastructure spending is quite erratic, while nonresidential buildings spending, with only slight variation, has been climbing at a strong steady pace for more than 4 years. Some analysts track nonresidential total spending, but these two sectors perform so differently it is important to break them apart to track trends. Buildings spending is up 2% from Q2’16 and up 5% YOY. In the 2nd half 2017 YOY spending is expected to reach 8% over the same months from 2016. Worthy of note is that non-building infrastructure spending, even though down slightly, just experienced two years of record highs. It will hold down the overall nonresidential total performance, but still finish 2017 near record highs.

See this article from February comparing my starting forecast compared to the Jan 2017 AIA Consensus Nonresidential Bldgs 2017 Forecasts Vary

Construction Spending Midyear 2017 Summary

7-11-17

Construction Spending Summary for May Spending

Year-to-date % growth in construction spending for 1st five months and expected estimate-to-complete (ETC) % growth for remaining seven months 2017. Total % growth vs 2016 and 2017 total $.

Total All Construction

YTD = +6.1%, ETC = +7.0%, 2017vs/2016 = 6.7%, 2017 total = $1.266 trillion

Particular strength is evident in the long term trend for Nonresidential Buildings for which spending growth is increasing and continues into 2018. Recently, all of 2016 spending was revised, in total up by 2%. Current 2017 values are being compared to revised 2016 values. History shows revisions have been up 45 of last 48 months. In the future, 2017 spending will most likely be revised higher. Even without that, at 6.7% total growth expected, 2017 will come in stronger than 2016. All sectors show some improvement over 2016. For 2018, Nonresidential Buildings and Infrastructure both contribute to an 7.8% forecast spending increase.

Also See Construction Spending May 2017 – Behind The Headlines

Residential Buildings

YTD = +12.2%, ETC = +9.3%, 2017vs2016 = +10.5%, 2017 total = $523 billion

Residential spending YTD has been above 12% each of the 1st 5 months of 2017. It is expected to dip between May and October due to a low volume of work contributed from starts during the period Q4’15 to Q1’16. This results in a temporary dip in spending. We could see annual spending averaging only $515b to $525b from April through September. New starts in Q1’17 reached an 11 year high, so spending increases later in the year. Residential work will finish the year with 10% growth, the 5th consecutive year over 10%. Average growth the last 5 years is 14%. Spending slows to 5% growth in 2018 .

Nonresidential Buildings

YTD = +5.2%, ETC = +7.5%, 2017vs2016 = +7.4%, 2017 total = $438 billion

Nonresidential Buildings spending is expected to increase slightly from May through September due to an above average volume of work contributed from starts during the period Q1’15 to Q2’15. The only major nonresidential building in decline this year is manufacturing. That’s not unexpected since manufacturing spending reached an all-time high in 2015 and stayed close to that level in 2016. Commercial/Retail, Lodging and Office construction all remain very strong with growth near 15%. Educational (+9%) and healthcare (+6%) both show sizable gains after years of little to no growth. Growth accelerates to 10+% in 2018, led by institutional spending.

See Also Nonres Bldgs Construction Spending Midyear 2017 Forecast

Non-building Infrastructure

YTD = -3.0%, ETC = +1.4%, 2017vs/2016 = 0.0%, 2017 total = $304 billion

Non-building Infrastructure spending, always the most volatile sector, is expected to increase slightly in the 2nd half 2017. An above average volume of work in early 2015 contributed very long duration jobs that will still contribute spending in late 2017, adding to normal average duration spending. Environmental Public Works (Sewer, Water Supply and Dams & Rivers) is holding back infrastructure from gains in 2017. Declines in that group are offsetting gains in Power, Highway and Transportation. No future growth is included from infrastructure stimulus and yet 2018 is projected to increase by 7%.

Construction Spending May 2017 – Behind The Headlines

7-6-17 Construction Spending May 2017 – Behind The Headlines

See Also Construction Spending Summary 7-11-17

Headline – Construction Spending for May came in flat compared to April, up 4.5% vs May 2016.

In this latest May report, April spending was revised up by 1% and May 2016 was revised up by 3%. The average revision since Jan 2016 is 3%/month. May 2017 will be revised in each of the next two reports and again with the May report issued in July 2018.

Current unadjusted construction spending is always being compared to previous months revised spending and growth is almost always being understated. Spending has been revised UP 45 times in the last 4 years.

In 2016, the 1st report indicated monthly spending declined 8 times from the previous month. After revisions, spending declined only twice from the previous month. Most MSM articles declaring construction spending was a miss are revised away in following months.

Nonresidential Construction Spending Remains Stagnant in May.

I’ve said this before many times, spending predictions are best tracked based on cash flows from all projects that have started. This is not simply tracking total backlog, nor is it tracking new construction starts. New starts (new backlog) represent only 20% to 25% of total spending within the year. Most spending comes from projects that started in previous years.

Big monthly changes in spending come from unusual fluctuations in starts. Very large projects ending (spending ending), compared to new projects starting, would cause a monthly drop in spending. The reverse would cause an increase. If a record volume month of construction projects that started two or three years ago are now reaching completion, and new starts today are experiencing normal growth not at record levels, then spending will most likely decline temporarily. Most monthly construction spending predictions are predetermined months ago.

Also, Nonresidential construction is comprised of two very different sectors, nonresidential buildings and non-building infrastructure. Infrastructure is quite erratic while buildings spending has been climbing at a steady strong rate for several years. Buildings spending is up 2% from Q2’16 and up 6% YOY. In the 2nd half 2017 YOY spending is expected to reach 8%.

Most infrastructure projects that started in 2015 and 2016 are still ongoing so do not effect much change in current monthly spending. It is projects from late 2014/early 2015 that are finishing that are resulting in the largest share of current spending drops. Worthy of note is that non-building infrastructure spending just experienced two years of record highs, so even though spending is down slightly we will still see 2017 finish near record highs.

Construction Companies Continue to Face Labor Shortage Challenges

Construction Spending for the last 24 months increased +13%, but after inflation actual volume during that period increased only +5.5%. Construction jobs output, (jobs x hours worked) for that same period increased +7.6%. Overall, jobs output is exceeding the growth in volume put-in-place. Most of this is being driven by imbalances in Nonresidential Buildings, for which jobs output grew by 7% in two years but volume growth measured only 2% after inflation.

Why is it that jobs output is growing faster than construction volume? Could it be that shortages are localized, not as widespread as thought? Or perhaps it’s that contractors can’t get skilled workers, so they are hiring more workers with less skill? Maybe contractors anticipate growth, so they are hiring more now to prepare for the future? Whatever the case, jobs are growing faster than construction volume and that is not what should be expected in a labor shortage.

Are contractor’s responses to survey questions about filling job positions based on an anticipated need to staff up to meet revenue growth? If so, that is a major miscalculation to determine staffing needs. This is not as far-fetched as you might think. I’ve talked with numerous contractors in the past who were doing this. As I tried to explain in several previous articles, growth in revenue (or construction spending) doesn’t address how much of the growth is due to inflation. Right now, in fact for the last 24 months, the largest portion of spending growth is inflation, not real volume growth.

If you are hiring to match your revenue growth, you are part of the reason jobs are growing faster than volume. INFLATION!

See also Construction Jobs Growing Faster Than Volume

Is there a Residential Construction Spending slowdown? If so, how significant?

YTD Residential Construction spending for the 1st 5 months 2017 is up 12.2% from 1st 5 months 2016. YTD has been above 12% since January.

Average spending for the last three months is up 4.0% from the average in Q4 2016. That’s a ~10% annual rate of growth. Starts cash flows are indicting flat spending for the next few months but then accelerated spending from late Q3 into the end of the year. Current projected spending for 2017 is $523 billion, +10.5% higher than 2016.

May vs April residential construction spending shows a 0.5% decline. However, April has been revised up once and May has not yet been revised. All months are revised twice after the first release of data. The average revision (to residential data) for the last 16 months is up 4%, the average revision for the last 28 months is up 7%. All revisions for the last 28 months were up. After revisions, there were only two monthly declines in the last 28 months, and both of those were slight.

If new starts collapse to show no gains for the remainder of the year, then based on starts already in backlog and reduced starts for the remainder of the year, spending would be reduced to $513 billion. That’s still 8.5% higher than 2016. Of course, this would be an extremely unlikely scenario. The last time residential construction starts declined for three or more consecutive months was 2010, and the last time there were no gains for six or more months was 2008.