2-5-7

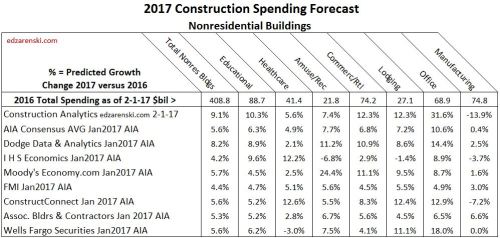

The following table includes my 2017 growth forecast for construction spending in nonresidential buildings compared to the recently published AIA Consensus Forecast which includes individual forecasts from seven economists.

The AIA Jan. 2017 Nonresidential Consensus Forecast can be found here

My 2017 Nonresidential Buildings Spending Forecast can be found here

Construction Analytics (edzarenski.com) forecast is based primarily on scheduled cash flow of construction starts in backlog. About 75% to 80% of all nonresidential buildings construction spending in 2017 will be generated by projects that are already underway. Only 20% to 25% of all spending in 2017 will come from new projects that start in 2017.

See my recent blog post on 2017 Starting Backlog here describes in part how I use backlog starts data to generate future spending forecast.

Nonresidential buildings 2017 starting backlog is 45% higher than at the start of 2014, the beginning of the current growth cycle. Spending in 2017 from that starting backlog has increased every year and it will be up 35% over 2014.

This comment I made two weeks ago in a post on Dodge Data 2016 Construction Starts helps explain in part the level of new starts in 2016 that established the pattern I see going into 2017:

“Nonresidential Building new starts in December remained consistent with October and November. Although well below the yearly highs reached in August and September, the final three months helped carry 2016 totals to an 8-year high. Nonresidential Buildings starts for the last six months averaged the highest since the 1st half of 2008.”

Nonresidential Buildings spending for 2016 totaled $409 billion, UP 8.1% from 2015.

Nonresidential Buildings spending in 2017 is forecast to increase to $447 billion, 9.1% over 2016.

The most recent 3-month average seasonally adjusted annual rate (SAAR) is already leading into 2017 starting at $420 billion only 5.5% below the peak in 2008. By midyear 2017 the SAAR will reach a new all-time high.

The widest variances between my forecast and the AIA panel forecasts are in Office, Manufacturing, Educational and Commercial. Here are explanations to support my forecast.

Office project starts at the end of the year increased more than 30% for 2016. Office construction 2017 starting backlog (projects under contract as of Jan 1, 2017) is the highest in at least 8 years, more than double at the start of 2014 when the current growth cycle of office spending began. More importantly, the share of spending from starting backlog is also increasing for 2017. This is setting up a very strong spending growth pattern for the next 2 years.

Manufacturing buildings new starts dropped 33% in 2015 and 38% in 2016. A disproportionately large portion of both 2015 & 2016 spending was generated from starts in 2014. In 2014, starts had jumped 80%+, but now almost all of that work is completed. For 2017, the amount of spending from starting backlog has dropped 25% from the level of 2016. Even an increase of 50% in new 2017 starts would not make up for that loss.

Educational buildings new starts increased 11% in 2016. But more important is that the total value of starting backlog has been increasing for several years. In 2015, the value of starting backlog increased only 5% over 2014. In 2016 it was 9% and in 2017 it is 13%. Even if new educational starts in 2017 decline by 10% to 20%, 2017 spending is being driven higher by the work already in backlog.

Commercial spending increased 11% in 2016. For 2017, spending from starting backlog will increase 10%, and starting backlog is at the highest level since pre-recession. In fact, spending from starting backlog will be 40% higher than 2014. Since starting backlog generates about 75% of spending within the year, most of the growth in 2017 is coming from very strong starting backlog.

Once again,”Simply referencing total backlog does not give a clear indication of spending within the next calendar year. The only way to know how much of total backlog that will get spent in the current year and following years is to prepare an estimated cash flow from start to finish for all the projects that have started in backlog.”

With few exceptions over the last three years, Construction Analytics, Dodge Data & Analytics and ConstructConnect have provided the most accurate forecasts. We’ll see in Feb. 1, 2018 how we all did when the total 2017 spending report gets released.