Home » Posts tagged 'outlook'

Tag Archives: outlook

Construction Briefs – As We Begin 2025

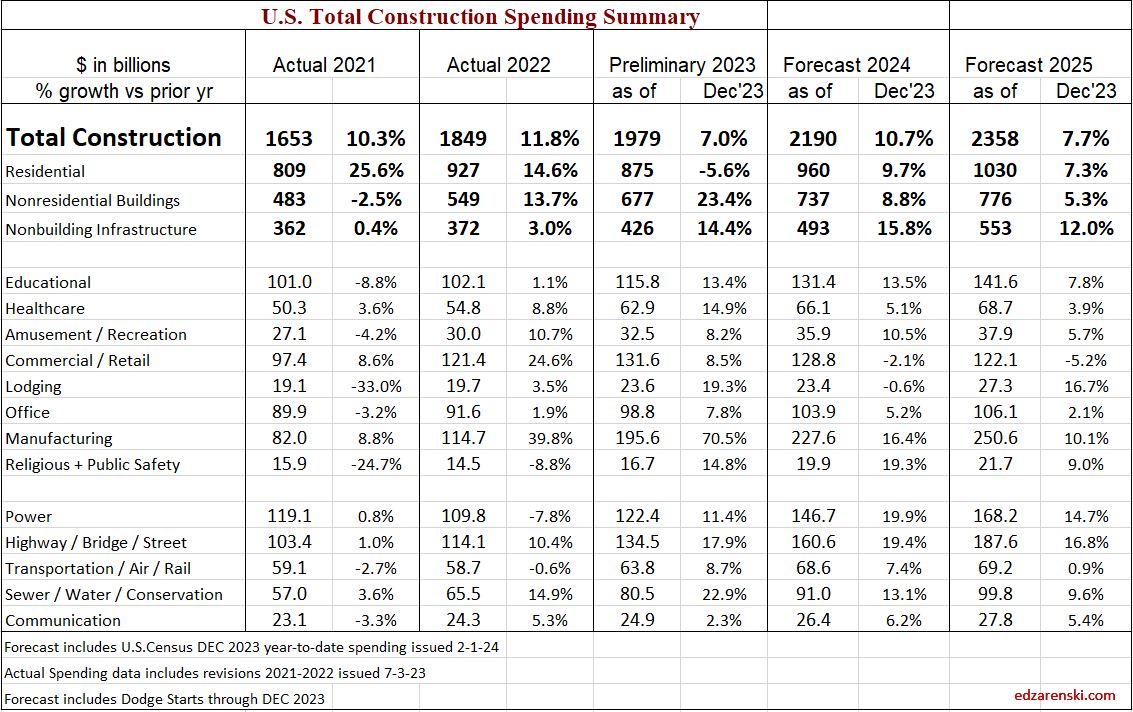

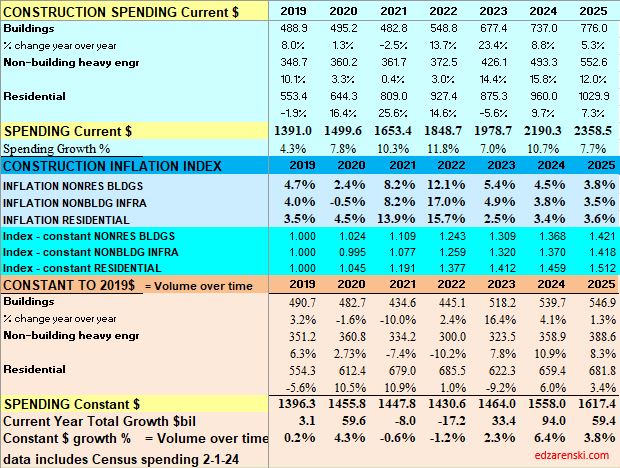

We are close enough, now in mid-January, to see where the numbers will end up for 2024. Construction spending as of Nov is up 6.5% year-to-date vs same 11 months in 2023. We are up 6.0% ytd vs the average of 2023. My forecast predicts we end 2024 up 6.2%, but growth is only 3.4% in 2025.

In February of 2024, with the Dec 2023 data in hand, my forecast for 2024 spending was $2,190 billion, only 1.8% higher than my current (Nov’24 data) forecast of $2,150 billion. Most of that early higher estimate was due to what I carried for my residential forecast, which I have since lowered by 3.6% from the initial forecast at the beginning of 2024. You can see in this monthly summary table that the Nonresidential Bldgs and Non-building forecasts have varied very little and the Total forecast has not varied up or down by more than 0.4% over the last 4 months.

edit 2-3-25 updated table to include Dec data. See the line comparing actual to the SEP data forecast.

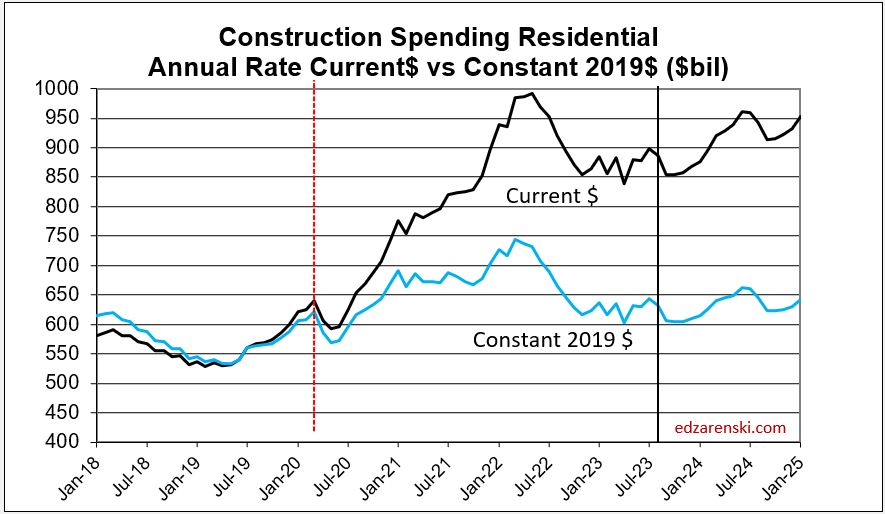

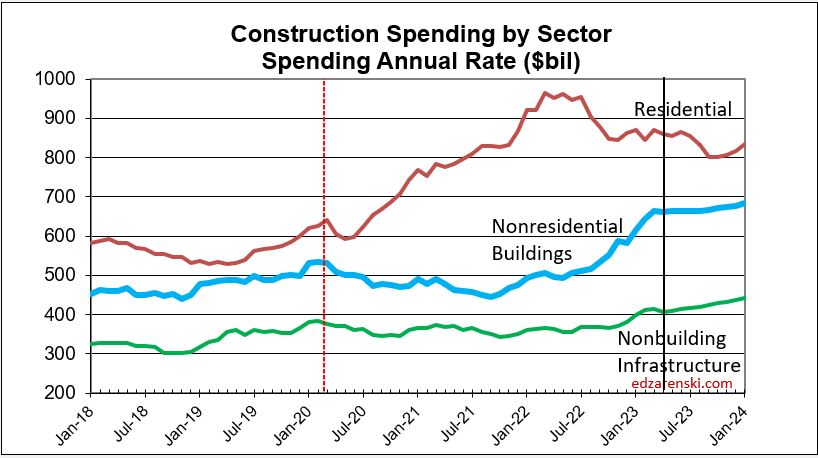

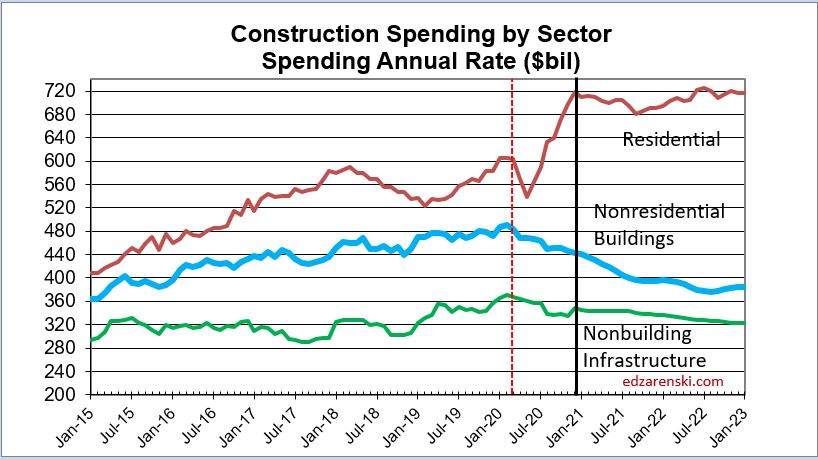

Single family construction spending reached a post-2006 high in Q4’21 thru Apr’22 ($480bil). From Apr’22 to the lowpoint in May ’23 ($360bil) spending dropped 25%. By year-end 2023 it had recovered almost 3/4ths of that drop. It fell again in mid-2024 to $410bil, but has since recovered to the year-end’23 level ($450bil). That drop is reflected in the difference between the current forecast and the earlier forecast.

NAHB – Cost of Constructing a Home 2024 excellent summary www.nahb.org/-/media/AB4E…

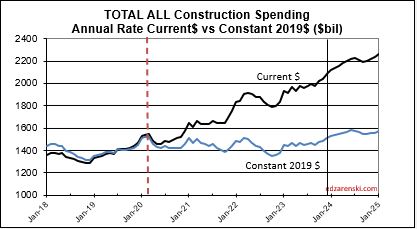

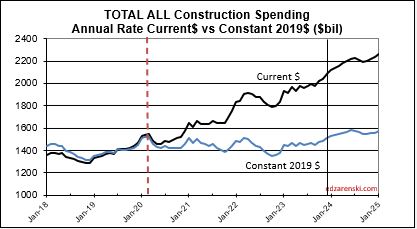

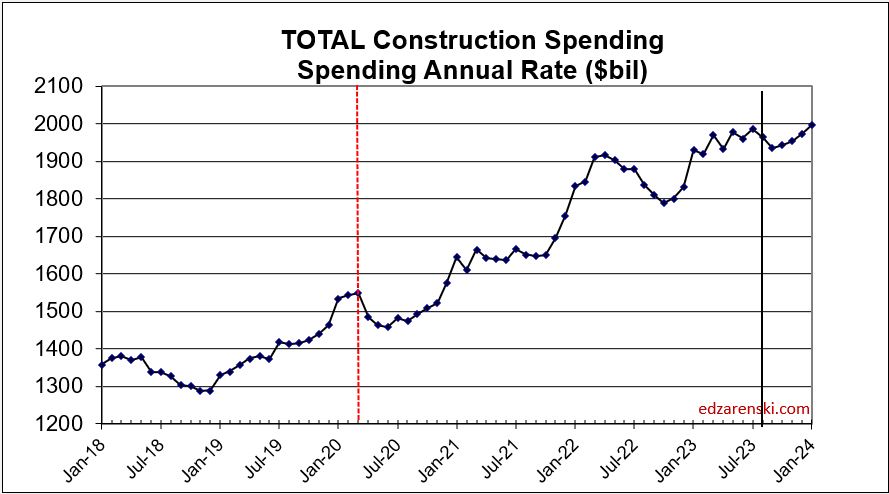

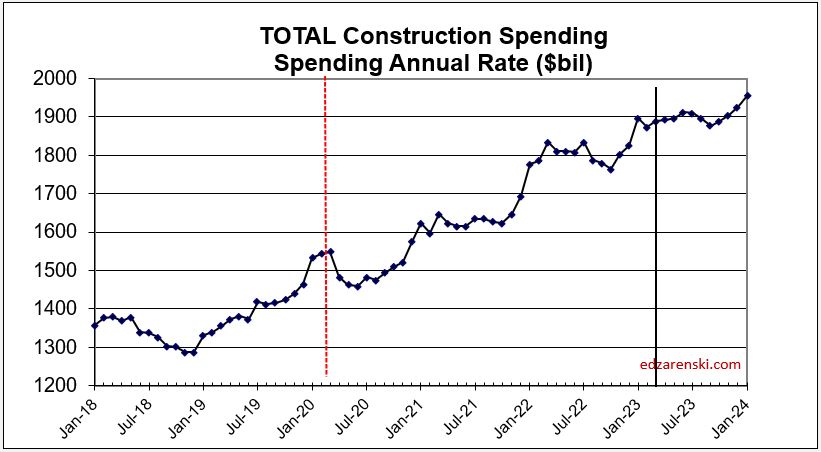

Construction spending in 2024 will hit near $2.15trillion, another new high, up 54% since 2019.

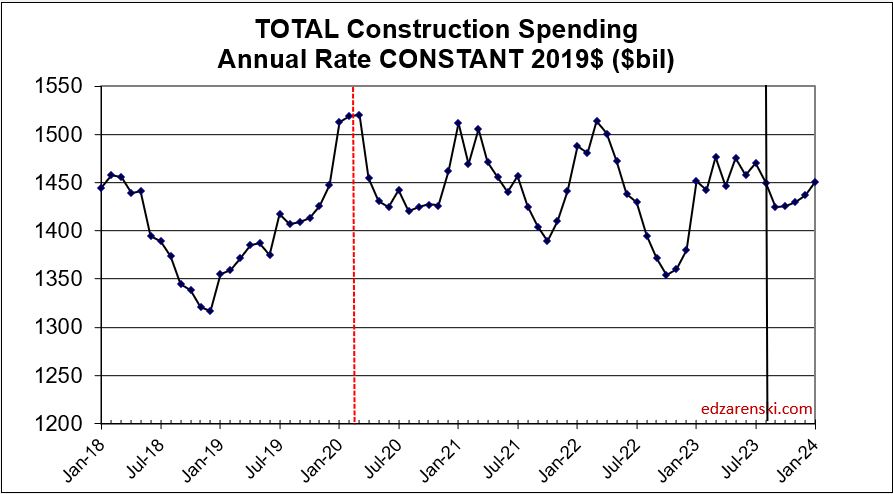

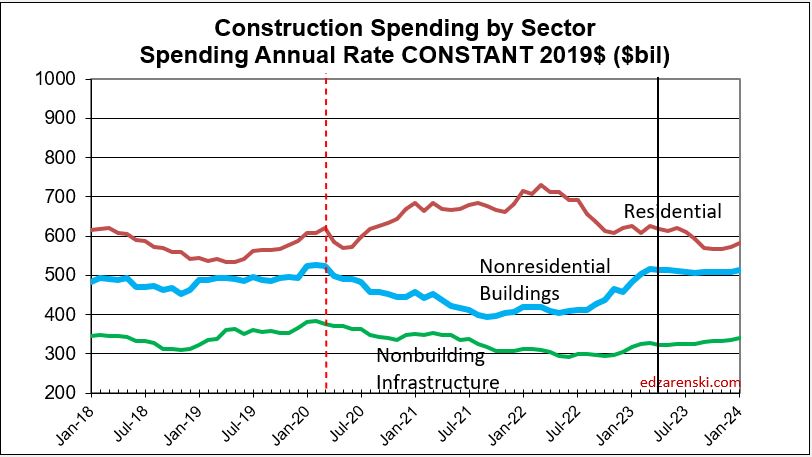

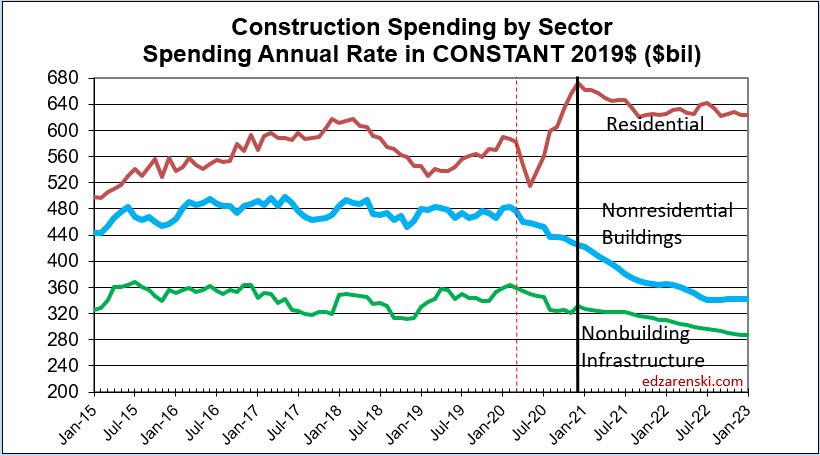

Caution: the following table, showing Constant$ analysis, now shows Constant$ with base year at 2024. Since Q1-2020 I have used the base year at 2019. This update changes the Constant$ amount, but not the Constant$ percent growth. Slight changes in prior years inflation resulted in some minor changes in Constant$ growth.

The last time construction spending declined was 2011. But construction spending includes inflation, which adds nothing to the volume of work put-in-place. Construction volume, (spending minus inflation) will finish the year up only 10% since 2019.

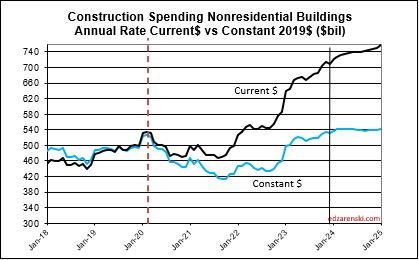

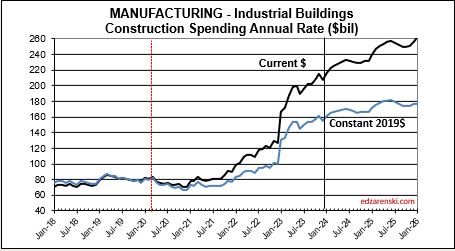

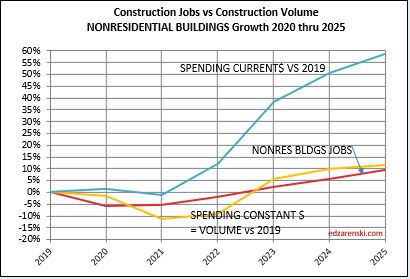

My construction spending forecast for 2025 Nonres Bldgs is down 0.7%. But it’s driven by projects ending in Manufacturing (and Warehouse). In the last 3 yrs, there were $230bil Mnfg starts, most in 2022, $130bil above normal, now some are ending. Without Mnfg, nonres bldgs 2025 spending would be up 4.5%. So while outward appearance may be that nonres spending is declining, in large part it is due to mega spending on Manufacturing buildings (and Warehouse) tapering down upon completion, creating very large annual declines, but normal. See The Manufacturing Spending Taper

Last year at this time, many of the Nonres Bldgs and Non-bldg line items showed Nov-Dec spending was already several points higher than the 2023 average. This was an indication leading into 2024 that those markets were on track to start the year already up. This year,most markets show a decline from the 1st half of the year into the 2nd half. Two notable declines are Warehouse and Office w/o Data Centers. Both start 2025 down 5%+ from the average in 2024.

I didn’t realize how much impact there was with the inclusion of (increasing) Data Centers in the (decreasing) Office construction spending values. I’ve now separated Data Centers from Office and Warehouse from Commercial/Retail. Office spending was pretty strong near it’s highs until 2h’22. Early in ’24 it had fallen to 8%-12% below ’22. Office spending is now 15%-18% below 2022. On the other hand, Data Center spending as of Nov is up 30% from the same months in 2023, and is up more than 60% above the average of 2023 and 120% above 2022. It will continue to increase into 2025.

In 2014-2015, Data Centers was less than 5% of total Office+DC construction spending. Today it is approaching 30%. Next year it will approach 40%. In 2015, Warehouse was 25% of total Commercial spending. By 2022 it had climbed to 54%. In 2025, it will fall back to 45%. Warehouse spending is now decreasing after climbing 100%+ since 2019.

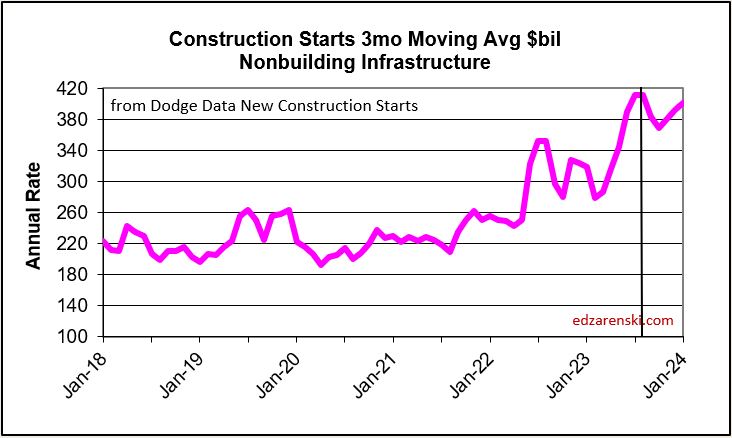

Dodge reports as of Nov construction starts for 2024 up 5% YTD. Residential starts up 7%. Nonresidential Buildings starts up 4%. Non-building starts up 5%.

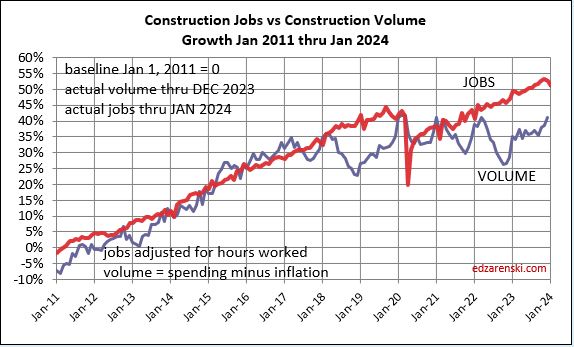

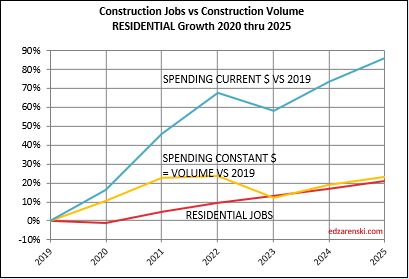

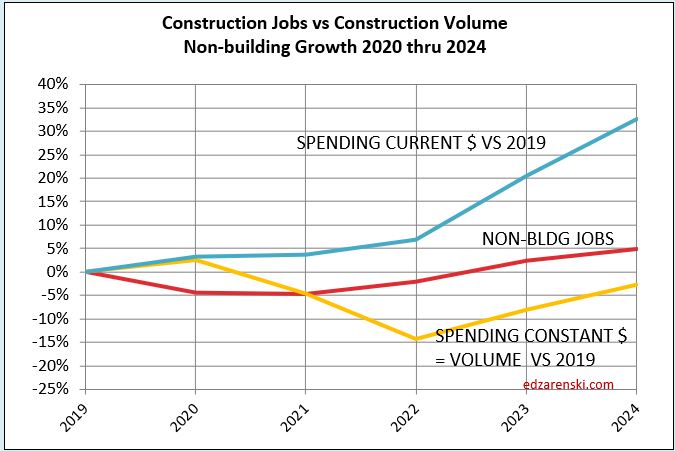

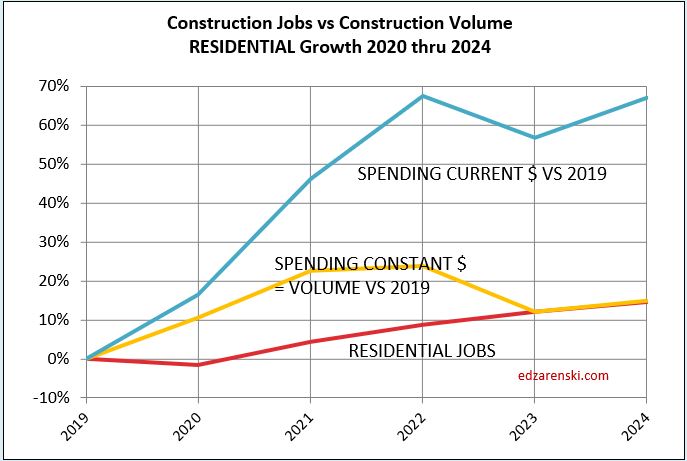

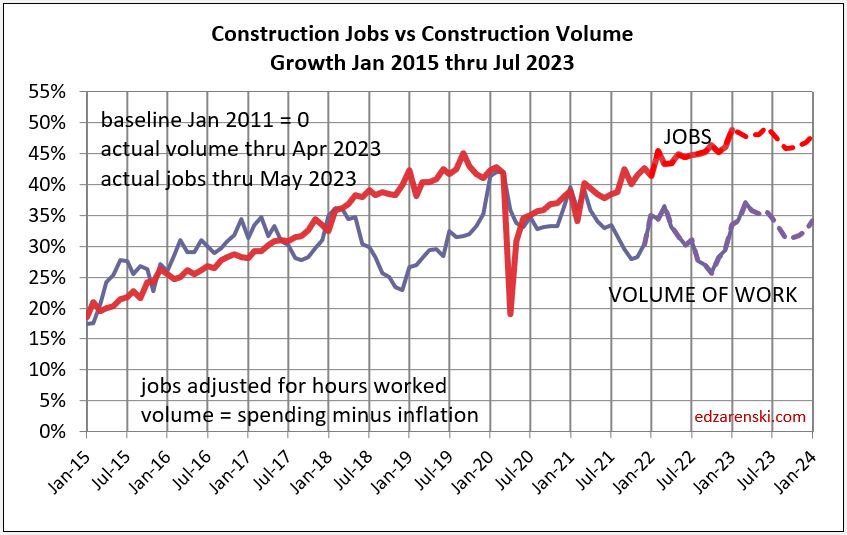

Construction Jobs do not get compared to construction spending. Spending includes inflation, which adds nothing to business volume. Compare jobs growth to Volume growth.

Construction Jobs counts here are the average for the year. That accounts for months during the year, other than Dec/Dec, with higher (or lower) percentage of yr/yr growth. For instance, total jobs Dec24 vs Dec23 increased only by 196k jobs or 2.4%. If you based annual growth on Dec/Dec, it would indicate 2024 increased by 2.4%. However, during the year, jobs growth in Mar-Apr-May were all greater than +3% compared to same month prior year. In fact, every other month during the year had a higher yr/yr growth rate than Dec/Dec. Yearly average of all 12 months shows total jobs annual average up 226K or 2.8%.

Dec/Dec shows a snapshot in time of one month compared to same month last year, without taking into account what might have happened in any of the other 11 months. YR24avg/YR23avg shows the change in the number of jobs over the whole year and accounts for all activity in the year.

Jobs 2024 AVG thru DEC. Rsdn+61k +1.9%. Nonres Bldgs+134k+3.7%. Nonbldg +29k+2.6%

Construction Volume AVG thru NOV Residential +2.9% Nonres Bldgs +3.3% Nonbldg +4.3%.

From 2012-2019, we added a yearly average 245,000 jobs/yr. In 2024 we added 226,000 jobs, but from 2021-2024, we added an average of 247,000 jobs/yr. We add the most jobs in Feb and Mar. We add the least jobs in Apr and Jun. We add more jobs, by far, in the 1st qtr. than any other qtr.

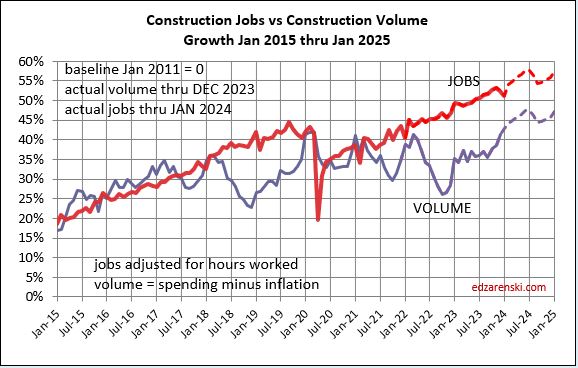

Don’t be surprised if 2025 construction jobs growth slows a bit. Jobs are slightly ahead of volume growth. Since 2019, both Jobs and Volume increased 10%. But that includes 2020, when volume increased 4% but jobs fell by 250k, or 3%. Over the period of 4 years 2021 thru 2024, Jobs increased 13%. Volume of work increased only 6%.

The unemployment rate in construction goes UP in the 1st qtr every year, by 2% to 3% (data since 2011). Now, your 1st thought may be, if unemployment is increasing, that is probably because jobs are falling. Well, construction has ADDED jobs in the 1st qtr. every year since 2011 (excluding 2020), by an avg of nearly 30% of all jobs added annually. More recently, since 2020, we’ve added almost 40% of total annual jobs in Q1. Construction unemployment is not going up in winter months because we lose jobs in winter. So how can the unemployment rate still go up? There’s only one number left in the equation. It goes up because the entire workforce increases by greater than the number of jobs added.

For an example of how this employment timing information can be useful see Employing Correlation – Using construction industry employment data as a proxy for flatbed demand

Harvard Joint Center for Housing Studies posted that In Texas, California, New Jersey, and the District of Columbia, immigrants make up more than half of construction trade workers.

Nov PPI for Construction Mtrls little changed from Oct Inputs YTD to Nonres +0.6%, to Rsdn +1.7%, to Hiway +0.6% Concrete products up 6%, Steel products down 7%-8%, Lumber/Plywood down 2%, Copper up 6%, Diesel down 14%. Final Demand YTD (all in) Nonres Bldgs all up 0.5% or less. Trades up 1%-2%.

We can’t always tell what affect changes in the cost of construction materials will have on the final outcome of annual construction inflation. PPI materials index does not account for productivity or margins and varies on stage of input. A good example of stage of input is PPI for Steel Mill Products. That does not include delivery from mill to fabricator, detailing, fabrication, shop painting, delivery to jobsite, shakeout, lifting, installation and finally overhead and profit, in all about 75% of the cost of structural steel installed.

Construction Analytics Nonres Building Cost Index is a weighted average of eight final cost indices.

NAHB estimates that $184 billion worth of goods were used in the construction of both new multifamily and single-family housing in 2023 and that $13 billon of those goods were imported. eyeonhousing.org/2024/12/impo…

Steel Statistics Cost Increase Effect on Construction? written 2016 US is world’s largest steel importer at 30MMT/yr. 50% from our top suppliers, Canada, Brazil, South Korea and Mexico. China supplies less than 2%. The U.S. annually imports about $2bil from Mexico.

One quarter of all annual Brussel Sprouts consumption occurs around the Christmas holiday.

Construction Analytics Outlook 2024

Construction Analytics Economic Outlook 2024 includes Construction Data – DEC 2023 Data 2-7-24

2-22-24 At the bottom of this article is a downloadable PDF of the complete 2024 Outlook

Here is a summary of construction spending through December 2023, Inflation through 4th qtr. or Nov where available, and resulting constant dollar volume. 2023 spending will be revised three times in 2024, Mar1, Apr1 and Jul1, and then again on Jul1 2025. Historically, almost all revisions are up.

Construction spending preliminary total for 2023 is up 7.0%. But nearly 80% of that total is inflation. Except for Nonresidential Bldgs, spending increased 23%, so inflation is only 25% of that. Even deducting inflation still leaves 75% of spending as volume growth Most of that growth is in Manufacturing buildings.

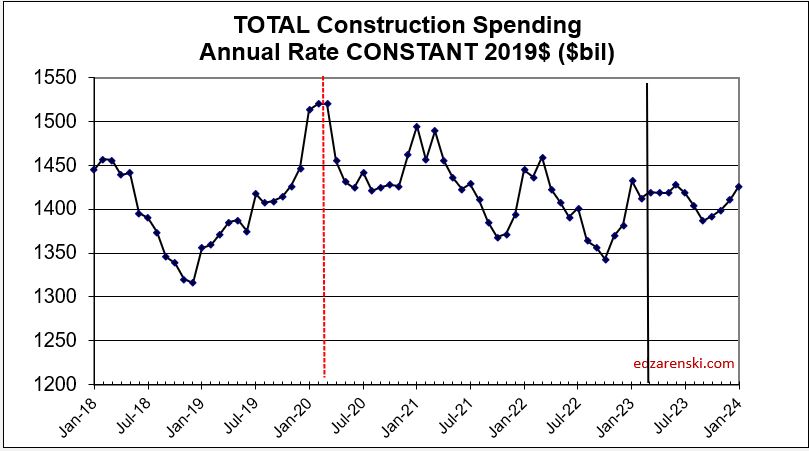

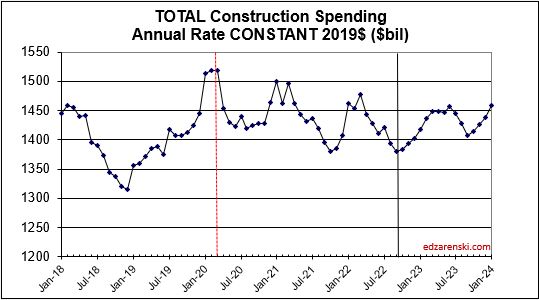

Spending is up a total of 42% since 2019; up 8% in 2020, 10% in 2021, 12% in 2022 and now 7% in 2023. But volume after adjusting for inflation is up only 5% total. You can see the Constant$ line, with one lower dip in 2022, has ranged between Constant$1400bil. to $1500bil. since mid-2019.

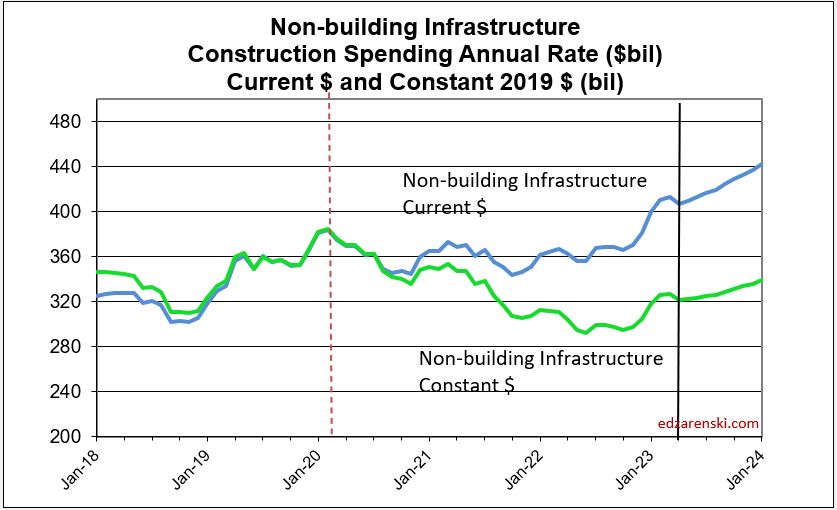

Construction spending total forecast for 2024 is up 10.7%. Nonresidential Buildings is forecast up 8.8%, Non-building Infrastructure up 15.8% and Residential up 9.7%. Lower inflation in 2024 means more of that spending is counting towards real volume growth. I’m expecting only 4% to 5% inflation for 2024, so real volume growth could reach 6% for the first time since 2015. From 2012-2016, volume growth averaged 6%/yr. For the last four years, 2020-2023, 42% spending growth vs 37% inflation growth netted only 5% total real volume growth. Since 2017, volume growth averaged less than 1%/yr. Non-building Infrastructure volume could increase 10%+ in 2024.

New Construction Starts

Dodge Construction Network (DNC) monthly news article of construction starts by sector provides the data from which the following is summarized.

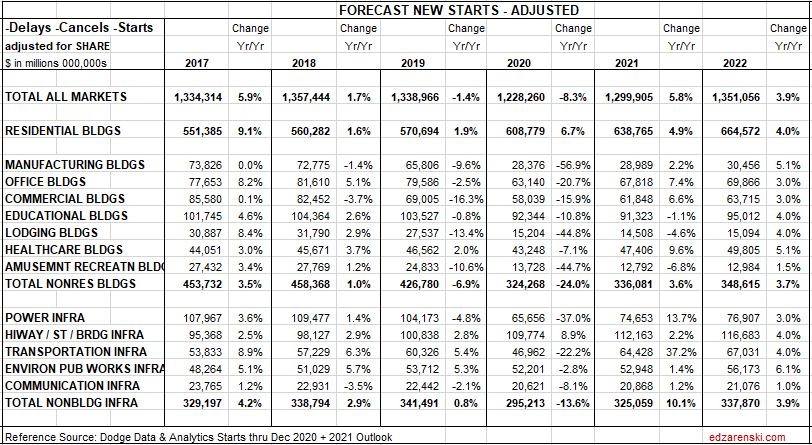

Total construction starts for 2023 ended down 4%, but Nonresidential Buildings starts finished down 7% and Non-building Infrastructure starts were UP 16%. Residential starts decreased 12% in 2023.

Total construction starts for 2024 are forecast up 7%. Nonresidential Buildings starts are forecast up 5% and Non-building Infrastructure starts up 8%. Residential starts are forecast up 10% in 2024.

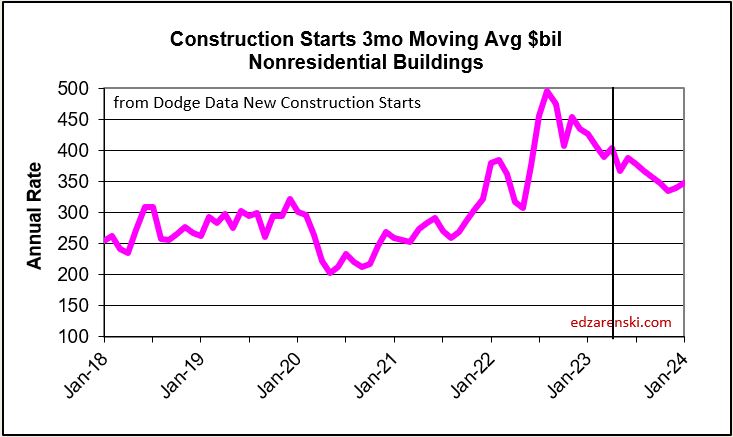

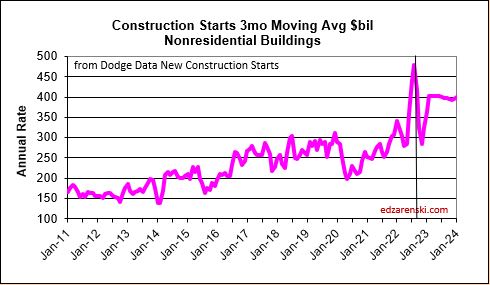

In recent years, Nonres Bldgs new starts averaged $300 billion/year. In the 2nd half of 2022, starts averaged near $500 billion/year. For the 1st half 2023 starts dropped to a rate of $390bil./yr., which is still well above the recent average. Then, for 2nd half 2023, starts came back up to average $430 billion/year, the 2nd highest half year average. A 50% increase in new nonresidential building starts in 2022 has a positive impact on the rate of construction spending in 2023 and 2024. It will continue to add lesser impact into 2025. Projects starting in 2nd half of 2023 could have midpoint of construction, point of peak spending, in 2024 or into 2nd half of 2025, some real long duration starts even later. So, the major spending impact from starts is sometimes one or two years later.

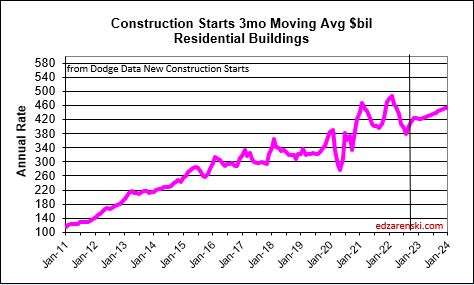

Residential construction (Dodge) starts posted the five highest months ever, all in the 1st 6 months of 2022. In the second half of 2022, residential starts fell 15%. In Q1 2023, residential starts dropped another 12% below 2nd half 2022, the lowest average since Q1-Q2 2020. Finally in July and August, starts regained some strength coming in 33% higher than the lows in Q1. Residential starts finish 2023 down 12% vs 2022. Forecast is up about 10% in 2024.

Nonresidential Buildings, in 2022 posted the largest ever one-year increase in construction starts, up 50%. Some of these starts will be adding to peak spending well into 2025. Nonres Bldgs starts in the 2nd half 2022, averaged 67% higher than any other 6mo period in history. Starts fell 20% in the 1st half 2023 but still posted the 2nd highest 6mo average ever. After two years of outstanding growth, Nonres Bldgs starts close 2023 down 7%. Although 2023 is down 7%, that’s still by far the 2nd best year ever. The forecast for 2024 is +5%.

Manufacturing starts, the market with the largest movement, gained 120% from 2020 to 2023. Manufacturing projects can have a moderately long average duration because some of these are multi-billion$ projects and can have schedules that are 4 to 5 years.

Educational, Healthcare, Lodging and Public Buildings all had starts of 20% or more the last two years.

Non-building starts for the 6 month period Mar-Aug 2023 posted the best 6 months on record, up 30% from the average of 2022. The 2nd half 2022 was up 50% over 1st half 2022. For 2023, Highway/Bridge and Power have the strongest gains. Total Non-building Starts for 2023 are up 16% and they were up 25% in 2022. These starts will help elevate spending through 2025. Non-building starts for 2024 are forecast up 8%.

Power starts are up 25% the last two years. Highway starts and Environmental Public Works are both up 33% the last two years and up 50% the last three years.

Starts data captures a share of the total market or only a portion of all construction spending, on average about 60% of all construction. The easiest way to understand this is to compare total annual construction starts to total annual spending. National starts in recent years about $800 billion/year, while spending in this period ranges from $1,300 billion/year to $1,500 billion/year. From this simple comparison we can see starts captures a share of about 60% of the total market. The actual share for each market varies from as low as 35% to as high as 70%. Before using starts data to forecast spending, starts here were first adjusted for market share.

Starting Backlog

Starting backlog is the estimate to complete (in this analysis taken at Jan 1) for all projects currently under contract. The last time starting backlog decreased was 2011. If new construction starts in the year are greater than construction spending in the year, then for the following year starting backlog increases. It’s when new starts don’t replenish the amount of spending in the year that backlog declines.

80% of all nonresidential spending in any given year is from backlog and could be supported by projects that started last year or 2 to 4 years ago. Residential spending is far more dependent on new starts than backlog. Only about 30% of residential spending comes from backlog and 70% from new starts.

The table below, Forecast Starting Backlog, is model generated by Construction Analytics. Adjusted starts are spread over time to generate cash flow. A sum of spending each month/year, subtracted from start of year plus new starts provides Backlog.

Construction Backlog leading into 2024, in every sector, is at all-time high, in total up 46% from Jan 2020. For the years 2022 and 2023, backlog is up 11% and 12%. Reaching new highs in Backlog could mean contractors are comfortable adding some backlog, or it could mean not enough labor, subcontractors or suppliers to support advancing growth so quickly, so growth advances slower and more of the work is retained in backlog for longer, essentially dragging out the timeline, or it could be long term workload, 4yr.-6yr. long projects from new starts, such as Manufacturing, where a very large amount enters backlog and gets spent over 4-6yrs., so, although the monthly drawdowns reduce the amount remaining in backlog, it remains in backlog for a long time.

Residential backlog in 2024 is down 0.5%, but from such a previous high, essentially, starts are riding flat along the top. Starts are up 55% since Jan 2020.

Nonresidential Bldgs starting backlog for 2024 received a boost from all the starts in 2022 and 2023. Backlog is up 12% from 2023 and up 50% from Jan 2020.

Nonbuilding Infrastructure starting backlog is up 12% each of the last two years boosted by strong starts in 2022 and 2023. For 2024, backlog is up 40% from Jan 2020.

Manufacturing backlog increased nearly 300% from 2020-2024, from $117bil going into 2020 to $300bil beginning 2024. No other market has ever been close. Manufacturing was responsible for 60% of all the Nonres Bldgs spending growth in 2023. It was also responsible for 60% of the Backlog growth leading into 2024. Nonres Bldgs has a total 3.6 million jobs and has never increased by more than 150,000 jobs in one year. Manufacturing is 30% of all Nonres Bldgs spending, so assume 30% of Nonres Bldgs jobs. That’s 1.2million jobs supporting just Manufacturing projects. So Backlog of $300bil, at 5000 jobs per billion per year, would need 1,500,000 jobs for a year. With a 1,200,000 jobs share of the workforce, that backlog would provide support for 15 months. Of course, new starts add to support throughout the year, but the calculation of how long backlog would support that market segment is valuable.

Backlog at the beginning of the year or new starts within the year does not give an indication of what direction spending will take within the year. Backlog is increasing if new starts during the year is greater than spending during the year. An increase in backlog could immediately increase the level of monthly spending activity, or it could maintain a level rate of market activity, but spread over a longer duration. In this case, there is some of both in the forecast. It takes several years for all the starts in a year to be completed. Cash flow shows the spending over time.

Current Rate of Spending

The current seasonally adjusted annual rate (SAAR) of spending gives an indication of how spending will perform in the following year. As we begin 2024, the current rate of spending (SAAR) for Nonresidential Buildings in Q4’23 is $709bil., already 4.5% higher than the average for 2023 ($677bil). If spending stays at the current level and no additional growth occurs, Nonresidential Bldgs spending will finish 2024 up 4.5%. Spending would need to have more monthly declines than increases to finish the year up less than 4.5%. The current forecast shows a monthly SAAR rate of growth for Nonresidential Bldgs. averaging about 0.5%/mo in 2024, so we have a minimum, but we can expect 2024 total spending to rise considerably higher than the current rate.

Non-building Infrastructure current rate of spending is now 3.7% higher than the average for 2023, however the forecast is indicating steady growth of 1%/mo for all of 2024.

Residential current rate of spending is 2.4% above the 2023 average and is forecast to average an increase of just under 1%/mo for 2024.

2024 Construction Spending Forecast

Starts lead to spending, but that spending is spread out over time. Starts represent a contract award. Spending takes the amount of that contract award and spreads it out by a cash flow curve over the duration of the job. An average spending curve for the sum of nonresidential buildings is 20:50:30 over three years. Only about 20% of new starts gets spent in the year started. 50% gets spent in the next year and 30% in YR3/4. An average spending curve for Non-building Infrastructure is more like 15:30:30:20:5. The effect of new starts does not show up in spending immediately. For example: If 2024 posts an additional $100 billion in new starts for Infrastructure, only about $15 billion of that would get put-in-place in 2024. The cash flow schedule for that $100 bil of new starts would extend out over 3 to 5 years. Most of that $100 bil would get spent in 2025 and 2026.

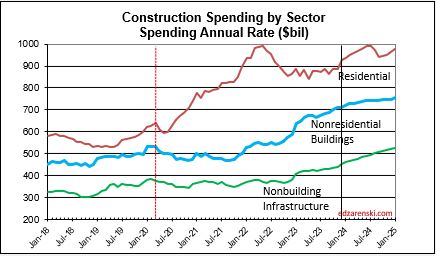

Total Construction Spending $2,190 billion +10.7% over 2023.

Nonresidential Buildings $737 billion +8.8% over 2023.

Non-building Infrastructure $493 billion +15.8% over 2023.

Residential Buildings $960 billion +9.7% over 2023.

This forecast does not include a recession.

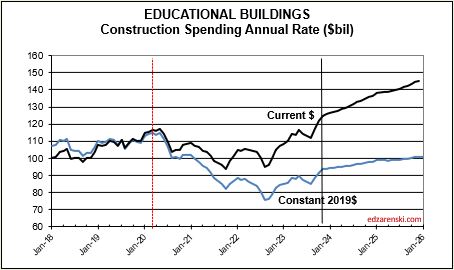

The largest increases to construction spending in 2023 are Manufacturing +$80bil, Highway +$20bil, Public Utilities (Sewage and Waste, Water Supply and Conservation-Rivers-Dams) +$15bil and Educational +$14bil.

Residential regains the top growth spot in 2024 with a forecast spending increase of +$68bil. Manufacturing is forecast to add +$32bil. Highway gains +$26bil, Power +$24bil and Educational gains +$15bil.

One big question is how did the forecast for Manufacturing increase so much since the beginning of 2023. Since January 2023, the starts forecast for 2023 increased by 35%. How much of that 35% is real growth in starts vs an increase in the capture rate of data gathering is yet to be determined, but has an impact of 2023-2024 spending. Also, starts for future years were increased by 50%. Starts (contract awards) drives up the spending forecast, since spending is a function of the future monthly cash flow (spending) of starts.

As we begin the year, Manufacturing SAAR current rate of spending is already 8% higher than the average for 2023. The current rate of spending is increasing at an average of near 2%/month for the next 6 months, then slows or dips slightly for the remainder of the year, indicating total spending for 2024 will finish well above the current rate of 8%. I’m forecasting 16% growth for the year.

Highway SAAR rate of spending begins the year 6.5% higher than the average for 2023, with the current rate increasing at an average of 1%/month for all of 2024, indicating total spending for 2024 will finish well above the current rate of 6.5%. Starts have increased +15%/yr the last three years. My forecast is for 19% growth in 2024 spending.

Power SAAR rate of spending begins the year 4% higher than the average for 2023, with the current rate increasing at an average over 1%/month for 2024, indicating total spending for 2024 will finish much higher. My forecast is for 20% growth in 2024.

Public Utilities SAAR rate of spending begins the year 6% higher than the average for 2023, with the current rate increasing at an average over 1%/month for 2024. Public Works averaged +15%/yr new starts the last three years. My forecast is for 13% spending growth in 2024.

Residential regains the top spot in 2024 with a forecast spending increase of $68bil. Residential SAAR rate of spending in Q4’23 was up 2.5% over 2023, but December was up 5%. So we begin the year 2.5% to 5% higher than the average for 2023. The rate of spending is forecast to increase 1%/month for 6 months, then fall 0.5%/mo for H2 2024. My forecast is for 10% growth in 2024.

Educational SAAR rate of spending begins 2024 7% higher than the average for 2023, and the current rate is increasing at an average of 0.7%/month for 2024. My forecast is for 13% growth.

Inflation

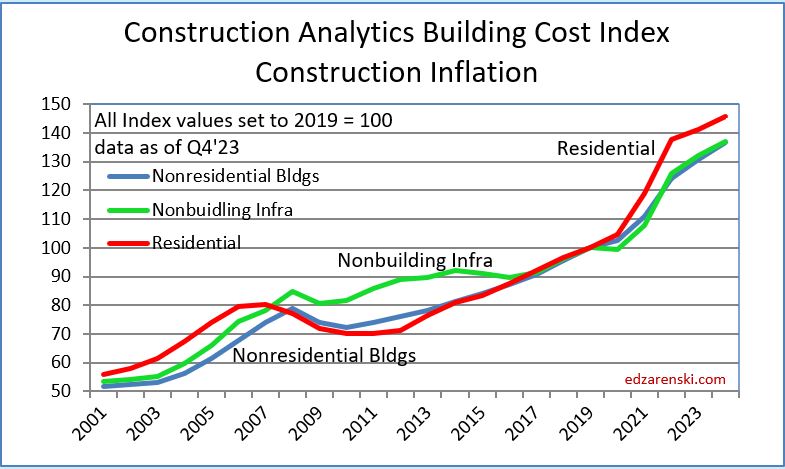

Construction Inflation differs from other common types of inflation, i.e., Consumer Price Index. It must be accounted for in order to make reasonable calculations for business volume and past or future costs.

30-year average inflation rate for residential and nonresidential buildings is 3.7%. Excluding deflation in recession years 2008-2010, for nonresidential buildings is 4.2% and for residential is 4.6%.

Deflation is not likely. Only twice in 50 years have we experienced construction cost deflation, the recession years of 2009 and 2010. That was at a time when business volume dropped 33% and jobs fell 30%. During two years of the pandemic recession, volume reached a low down 8% and jobs dropped a total 14%.But we gained back far more jobs than volume. That means it now takes more jobs to put-in-pace volume of work. That increases inflation.

The following Construction Inflation plot (for Nonresidential Buildings only) shows three elements: 1) a solid grey bar reflecting the max and min of the 10 indices I track in my weighted average inflation index, 2) a solid black line indicating the weighted average of those 10 indices, and 3) a dotted red line showing the Engineering News Record Building Cost Index (ENR BCI). Notice the ENR BCI is almost always the lowest, or one of the lowest, indices. ENR BCI, along with R S Means Index, unlike final cost indices, do not include margins or productivity changes and in the case of ENR BCI has very limited materials and labor inputs.

Final cost indices represent total actual cost to the owner and are generally higher than general indices. Producer Price Index (PPI) INPUTS to construction reflect costs at various stages of material production, generally do not represent final cost of materials to the jobsite and do not include labor, productivity or margins. Even with that, a PPI Inputs index +20% for a material could be only a +5% final cost. PPI Final Demand indices include all costs and do represent actual final cost. The solid black line (above) represents the Construction Analytics Building Cost Index for Nonresidential Bldgs and is a final cost index.

This short table shows the inflation rate for each year. Useful to compare to last year, but you would need to mathematically do the compounding to move over several years. The plot below shows the cumulative inflation index, or the cumulative compounded effect of inflation for any two points in time.

Typically, when work volume decreases, the bidding environment gets more competitive. We can always expect some margin decline when there are fewer nonresidential projects to bid on, which typically results in sharper pencils. However, when labor or materials shortages develop or productivity declines, that causes inflation to increase. We can also expect cost increases due to project time extensions or potential overtime to meet a fixed end-date.

Current$ Spending, Inflation, Constant$ Volume

Volume = spending minus inflation. Spending includes inflation. Inflation adds nothing to the volume.

Inflation adjusted volume is spending minus inflation, or to be more accurate, spending divided by (1+inflation). Inflation adds nothing to volume growth. The following table shows spending, inflation and volume (spending without inflation) for each year. Spending is current to the year stated. The values in the constant table are indexed to a constant value year, 2019. This shows business volume year to year, can be a lot different than spending would indicate. When inflation is positive, volume is always less than spending by the amount attributed to inflation.

Lower inflation in 2024 means more of that spending is counting towards real volume growth. Expecting only 4% to 5% inflation for 2024, real volume growth could reach 6% for the first time since 2015. From 2012-2016, volume growth averaged 6%/yr. For the last four years, 2020-2023, 42% spending growth vs 37% inflation growth netted only 5% total real volume growth. Since 2017, volume growth averaged less than 1%/yr. Non-building Infrastructure volume could increase 10%+ in 2024.

Spending during the year is the value of business volume plus the inflation on that volume. When inflation is 12%, volume plus 12% = total spending. Revenue is generally measured by spending put-in-place during the year. Revenue does not measure volume growth. In 2022, Nonresidential buildings inflation was 12%, so business volume was 12% less than spending, or 12% less than revenue. Residential volume was 15% less then spending.

When referencing Constant $ growth, remember the dollars for all years are reported here as 2019$. If the baseline year is changed to this year (divide all indices by this year’s index), the resulting comparison would be all years reported as 2024$. The dollars would all be greater, but the percent change would be the same. In this table, nominal spending is divided by the inflation INDEX for the year. You can also deduct the percent inflation from any individual year of spending to find inflation adjusted $ for that year alone, however that method would not allow comparing the adjusted dollars to any other year. A baseline year is necessary to compare dollars from any year to any other year.

Reference Inflation Data Construction Inflation 2024

Through December 2023, Total Construction Spending is up 40% for the four years 2020-2023, but, during that same period inflation increased 35%. After adjusting for 35% inflation, constant $ volume is up only 5%. So, while the current $ spending plot shows a four-year total increase of 40% in spending, the actual change in business volume is up only 5% and has just in the last few months returned to the pre-pandemic peak in Feb-Mar 2020.

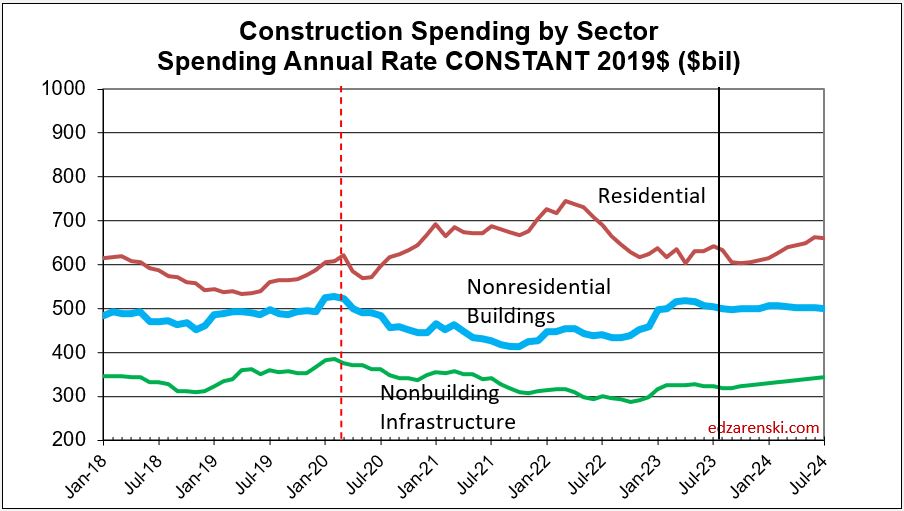

Jobs are supported by growth in construction volume, spending minus inflation. If volume is declining, there is no support to increase jobs. Although total volume for 2023 is up 2.3%, Residential volume is down 9%, Nonresidential Bldgs volume is up 16% and Non-building volume is up 8%. Inflation was so high in 2021 and 2022 that it ate away most of the spending gains in those years.

Jobs vs Volume

Construction Jobs increased 2.75% in 2023. We added 214,000 jobs (avg’23-avg’22). There are currently 8,056,000 construction jobs. The largest annual increase post 2010 is 321,000 jobs (+4.6%) in 2018. The average jobs growth post 2010 is 200,000 jobs per year.

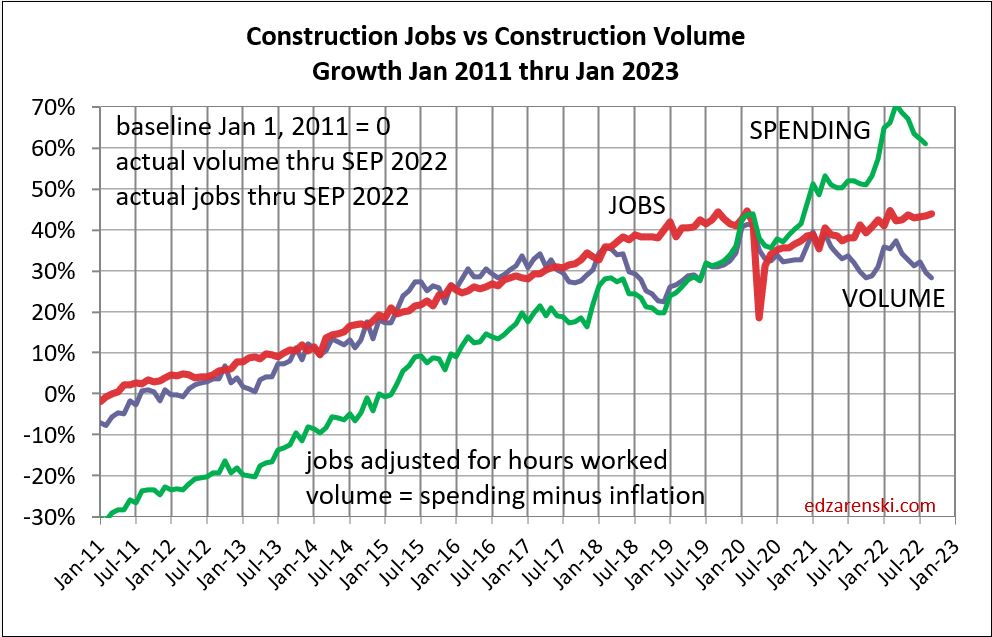

Since 2010, average jobs growth is 3%/yr. Average volume of work growth since 2010 is 2.3%/yr. This plot shows Jobs and Volume growth closely match from 2011 to 2018. With few exceptions for recession periods, this pattern can be seen throughout the historical data.

What’s remarkable about the growth is this, since 2016, spending has increased 63%, volume after inflation increased 6% and jobs increased 19%. In the last 7 years, 2017-2023, jobs increased 2.5%/yr. Volume of work increased only 0.8%/yr. Volume and jobs should be moving together.

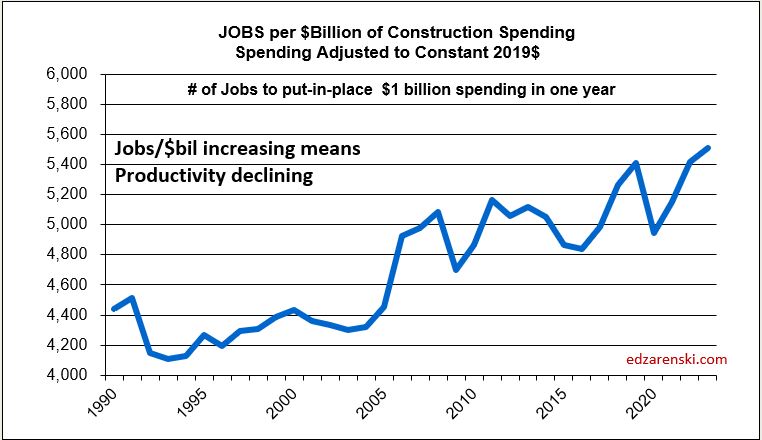

It takes about 5000 jobs to put-in-place $1 billion of volume in one year. It could easily vary from 4000 to 6000. So, an add of $100 billion+ in one year would need 500,000 new jobs. Jobs should track volume, not spending growth. Volume = spending minus inflation.

Normal construction jobs growth is about 250,000 jobs per year and maximum prior growth is about 400,000. From the table above, Nonresidential Bldgs and Non-building Infrastructure added $100bil of volume in 2023 and will add $60bil in 2024. The workload discussed above would theoretically require 500,000 new jobs in 2023 and 300,000 more in 2024. That’s an expansion of the industry workforce by 10% in two years, for just half the industry, in an industry that normally grows in total 3%/yr. This industry can’t grow that fast. This may have some impact if over-capacity growth results in a potential reduction or extension in future forecast. You can’t increase spending that fast if you can’t also expand the labor force and the suppliers to the industry that fast.

In the last 12 months, Dec’22 to Dec’23, Nonres Bldgs jobs are up 4%. Nonres Bldgs spending is up 23%, by far driven by Manufacturing, but after ~5.4% inflation, volume of nonres bldgs workload is up 16%. So, we have a 4% increase in jobs versus a 16% increase in volume.

The last year has shown a huge increase in the volume of nonres bldgs work, without an equal increase in jobs. Is this excess nonres bldgs jobs for the past three years now absorbing added workload, (a 4% increase in jobs but a 16% increase in volume), without collapsing the labor force or canceling the volume?

Non-building, over the next two years, could experience the same kind of growth spurt as Nonres Bldgs., a forecast increase in volume the next two years without an equal increase in jobs. Volume which was lower than jobs since 2021, is now increasing faster than jobs. Non-bldg volume is forecast up 6% to

8%/year the next 3 years. Jobs increase at an avg. 3.5%/year.

Residential volume has exceeded residential jobs all the way back to 2011. The recent decline in volume brings the two even, if the jobs hold the pace.

For as long as I can remember, the construction industry has been complaining of jobs shortages. And yet, as shown in the data mentioned above, jobs have increased multiples times greater than volume of work. With an exception for recession years, (2007-2010 and 2020), jobs increase at a rate of 2.5% to 3% per year. The greatest disparity between jobs and volume occurred in late 2022, when jobs growth had already resumed normal pace, but volume of work was still reeling from the effects of new construction starts that were canceled dating back to late 2020-early 2021. Recent volume growth at a much faster rate than jobs growth is now closing the gap.

When jobs increase without an equal increase in the volume of work, productivity declines. This recent increase in volume and the projected increase in volume in 2024, several points stronger than jobs, will offset some of the disparity which has been negative for a long time.

Reference Inflation Data Construction Inflation 2024

Reference Article The Next Forecast Challenge

Reference Article Midyear ’23 Jobs Outlook

Reference Article Reliability of Predicted Forecast

Reference Link to Web Dodge Construction News

Below is a downloadable 24 page PDF of the complete 2024 Outlook

Construction Data Briefs AUG Data 10-6-2023

Total Construction Spending in 2023 is forecast at $1,950 billion, an increase of 5.5% over 2022.

Nonresidential Buildings spending is leading Construction spending growth. With eight months in the year-to-date (ytd) for 2023, total all construction spending ytd is up 4.2%. Nonresidential buildings spending is up 22% ytd compared to Jan-Aug 2022, the fastest rate of nonres bldgs growth in over 30 years. Only 2006 & 2007 come close at 13% & 19% growth years. Commercial/Retail spending peaked in January 2023 and has dropped every month since. It will drop from a ytd of 8.5% down to a yearly total of 5%. Manufacturing is up 74% ytd and will hold on to finish the year up 66%.

Nonbuilding spending ytd is up 12%. The largest advances are in Highway, up 16% ytd, and Public Utilities. Sewage/Waste Water is up 24% ytd, Water Supply is up 15% ytd and Conservation/Rivers/Dams is up 26% ytd .

Residential Spending ytd compared to Jan-Aug 2022 is still down -8.7%. Residential spending peaked in Mar 2022 and had a recent bottom in Apr 2023. Since April, the annual rate of residential spending is up 5.6%, almost entirely due to an 8% increase in the largest segment, single family spending, 45% of all residential spending. Multifamily spending is is up 6%, but it’s only 15% of residential spending.

Spending Forecast

Total Construction Spending in 2023 is forecast at $1,950 billion, an increase of 5.5% over 2022.

Nonresidential Buildings spending is forecast at $662 billion, an increase of 20.6% over 2022.

Non-building Infrastructure spending is forecast at $421 billion, an increase of 12.9% over 2022.

Residential Buildings spending is forecast at $867 billion, a decline of -6.5% less than 2022.

This forecast does not include a recession.

Spending by Sector Current $ and Inflation Adjusted Constant $

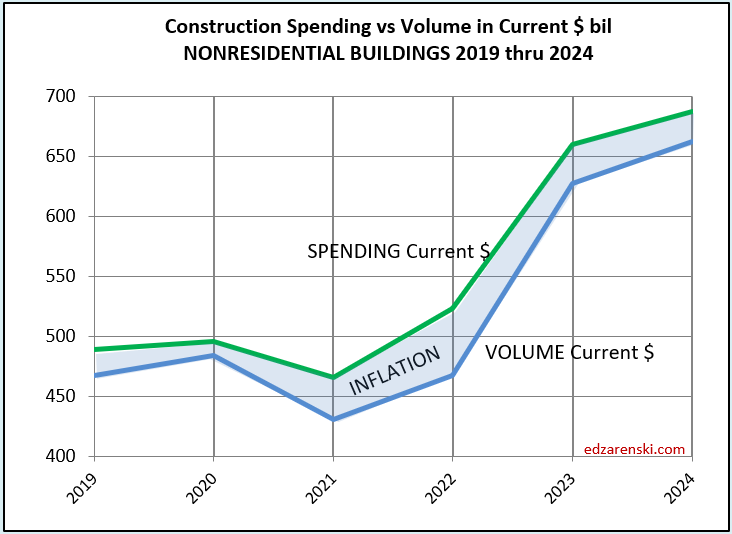

In 2023, it’s Nonresidential Buildings leading growth. In 2024, it will be Non-building Infrastructure leading spending growth. Both are expected to post spending growth greater than the inflation index, so there will be real volume growth. In 2020+2021, residential volume grew 10%/yr. For 2023, residential volume drops 10%. Nonresidential Bldgs will post a 13% increase in volume in 2023 and flatten out at that level through 2024. Non-building volume increases 6% to 7%/yr for the next few years.

New Construction Starts

The rate of construction spending in 2023 will be influenced predominantly by a 50% increase in new nonresidential building starts in 2022. In recent years, new nonres bldgs starts averaged $300 billion/year. In the 2nd half of 2022, starts averaged near $500 billion/year. From Mar-Aug 2023 starts averaged $400 billion/year. Many of those projects will have peak spending in 2023 or 2024.

Residential construction (Dodge) starts posted the five highest months ever, all in the 1st 6 months of 2022. In the second half of 2022, residential starts fell 15%. In Q1 2023, residential starts dropped another 12% below 2nd half 2022. Finally in July and August, starts regained some strength coming in 33% higher than the lows in Q1. Residential starts are still down 17% year-to-date vs 2022.

Nonresidential Buildings, in 2022 posted the largest ever one-year increase in construction starts, up 50%. Nonres Bldgs starts in the 2nd half 2022, averaged 67% higher than any other 6mo period in history. Starts fell 20% in the 1st half 2023 but still posted the 2nd highest 6mo average ever. Nonres Bldgs starts are down 17% ytd.

Growth in Manufacturing construction starts for 2022 far surpasses growth in any other market, up over 150%.

Non-building starts for the 6 month period Mar-Aug 2023 posted the best 6 months on record, up 30% from the average of 2022. The 2nd half 2022 was up 50% over 1st half 2022. The 6 months Mar-Aug 2023 is up 18% from 2nd half 2022. For 2023, Highway/Bridge and Power have the strongest gains. Total Non-building Starts for 2023 are forecast up 25%. Non-bldg starts are up 22% ytd.

Current $ Spending, Inflation and Constant $ Volume

Inflation adjusted volume is spending minus inflation, or to be more accurate, spending divided by (1+inflation). Inflation adds nothing to volume growth. The following table shows spending, inflation and volume (spending without inflation) for each year. Spending is current to the year stated. The values in the constant table are indexed to a constant value year, 2019. This shows business volume year to year, can be a lot different than spending would indicate. When inflation is positive, volume is always less than spending by the amount attributed to inflation.

SEE Construction Inflation 2023

Spending during the year is the value of business volume plus the inflation on that volume. When inflation is 12%, volume plus 12% = total spending. Revenue is generally measured by spending put-in-place during the year. Therefore, Revenue does not measure volume growth. In 2022, Nonresidential buildings inflation was 12%, so business volume was 12% less than spending, or 12% less than revenue. Residential volume was 15% less then spending.

Through August 2023, Overall Construction Spending is up 28% in the 42 months since the onset of the pandemic, but, during that same period inflation increased 33%. After adjusting for 33% inflation, constant $ volume is down 5%. So, while the plot on the left shows three years of increases in spending, the actual change in business volume is still down and has not yet returned to the pre-pandemic peak in Feb-Mar 2020.

Does Volume of Work Support Jobs Growth?

or, Can jobs growth support volume of work?

Jobs should track volume, not spending growth. Volume = spending minus inflation. Volume is down, although now increasing, while jobs are up. Nonres Bldgs volume, in constant $, fell 25% from Feb 2020 to Sept 2021, and hit a second deeper low in mid-2022. Since then, the actual change in nonres bldgs volume has increased 18%. Yet nonres bldgs jobs increased only 3.5%. That still leaves volume nearly 10% lower than the pre-pandemic high. If the same production levels ($ put-in-place per worker) as 2019 were to be regained, theoretically, nonresidential volume would need to increase 10% with no increase in nonresidential jobs. For now, productivity is well below that of 2019, but it is improving because volume is increasing rapidly and jobs are increasing slowly.

Nonresidential Buildings spending in 2023 is forecast at $660 billion, an increase of 20.6%, or an increase of $113 billion in 2023. Non-building Infrastructure spending is forecast up 13% ($50bil) in 2023 and 10% ($40bil) in 2024.

Generally, it takes 5000 jobs to put-in-place $1 billion in one year. It could easily vary from 4000 to 6000. So an add of $100 billion+ in 2023 would need 500,000 new jobs. Adding $200 billion over two years would need 1,000,000 new jobs.

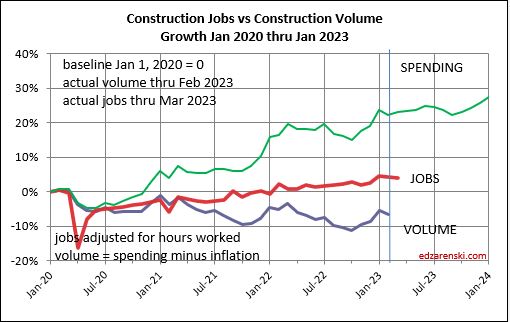

Construction Jobs vs Construction Volume

These plots updated to jobs report 10-6-23

Since Q1 2020, pre-pandemic high, spending increased 28%, but inflation was 33%, so real volume of work is down 5%. In that time jobs increased 5%. Jobs are way ahead of volume, but volume is backfilling in the void, especially in nonres bldgs.

This plot with baseline Jan 1, 2011 shows that jobs increase pretty consistently at about 3% to 4% per year. Except for the spike down in 2020, rate of growth (slope of the jobs line) is consistent for 13 years.

If we were to grow the labor force to meet the newly identified workload added from new starts, we would need to double the prior maximum rate of construction jobs growth. Normal construction jobs growth is about 250,000 jobs per year and maximum prior growth is about 400,000. The workload discussed above would require 500,000 new jobs/yr., back to back. That’s an expansion of the industry by 15%, in an industry that normally grows 3%/yr. This industry can’t grow that fast. (Which means we may all need to account for over-capacity growth as a potential reduction in future forecast. You can’t increase spending that fast if you can’t also expand the labor force and the suppliers to the industry that fast).

My first thoughts were, Jobs may not be able to increase fast enough to put-in-place the forecast spending. This impediment needs to be accounted for and could reduce overall construction spending forecast over the next two years. The most likely markets where a reduction might occur are Manufacturing, Highway and Public Utilities.

However this is what happened the past year. In the last 12 months, Aug’22 to Aug’23, Nonres Bldgs jobs are up 3.8%. Nonres Bldgs spending is up 21%, by far driven by Manufacturing, but after ~6% inflation, volume of nonres bldgs workload is up 15%. So, we have a 3.8% increase in jobs to accomodate a 15% increase in volume.

The last year has shown a huge increase in the volume of nonres bldgs work, without an equal increase in jobs. This shows the excess nonres bldgs jobs for the past three years is now absorbing new workload, (a 3.8% increase in jobs to accomodate a 15% increase in volume), without collapsing the labor force or canceling the volume. However, the ability to absorb work into the existing workforce cannot continue.

Non-building, over the next two years, could experience the same kind of growth spurt as Nonres Bldgs., a forecast increase in volume the next two years without an equal increase in jobs. Volume which was lower than jobs since 2021, is now increasing faster than jobs. Non-bldg volume is forecast up 6% to 8%/year the next 3 years. Jobs increase at an avg. 3.5%/year.

Residential volume has exceeded residential jobs all the way back to 2011. The recent decline in volume brings the two even, if the jobs hold the pace.

SEE more discussion on Volume and Jobs

here 2023 Construction Volume Growth

here 2023 Midyear Jobs Outlook

and here Infrastructure Construction Expansion – Not So Fast

See also Midyear Construction Forecast Update 8-12-23

Construction Data Briefs JUN 2023

Nonresidential Buildings spending is leading Construction spending growth. For the first four months of 2023, total construction spending year-to-date (ytd) is up 6.1%. Nonresidential buildings spending is up 30% ytd compared to the same four months 2022, the fastest rate of nonres bldgs growth in over 20 years. Nonbuilding spending ytd is up 11%. Residential spending peaked in March 2022. Since then the annual rate of residential spending has dropped 11%.

SPENDING FORECAST

Total Construction Spending in 2023 is now forecast to reach $1,915 billion, an increase of 6.4% over 2022.

Nonresidential Buildings spending in 2023 is now forecast at $660 billion, an increase of 26.2% over 2022.

Construction Spending through April is up 6.1% ytd. Spending is forecast to finish 2023 up 6.4%.

Total construction spending for 2023 is on track to increase +6.4%. Residential -8.1%, Nonres Bldgs +26.2%, Nonbldg +14.4%.

SPENDING BY SECTOR CURRENT $ AND INFLATION ADJUSTED CONSTANT $

In 2023, it’s Nonresidential Buildings leading growth. In 2024, it will be Nonbuilding Infrastructure leading spending growth. Both are expected to grow greater than the inflation index.

See also Construction Spending Outlook – Feb 2023

STARTS

The rate of construction spending in 2023 will be influenced predominantly by a 40% increase in new nonresidential building starts in 2022. In recent years, new nonres bldgs starts averaged $300 billion/year. In the 2nd half of 2022, starts averaged over $500 billion/year. Many of those projects will have peak spending in 2023. Some will occur in 2024.

Residential construction (Dodge) starts posted the five highest months ever all in the 1st 6 months of 2022. In the second half of 2022, residential starts fell 15%. In Jan and Feb 2023, starts dropped another 20% below 2nd half 2022. Starts are now down 25% in 12 months.

Nonresidential Bldgs starts in 2022 posted the largest ever one-year increase in new nonresidential buildings construction starts, up 40%. Starts were also up 15% in 2021. Nonres Bldgs new starts in the 2nd half 2022, averaged 67% higher than any other 6mo period in history.

Growth in Manufacturing construction starts for 2022 far surpasses growth in any other market, up over 150%. Office is up 33% (datacenters), Healthcare up 23%, Comm/Rtl up 30% (warehouses). Warehouse stats have slowed and will hold Comm/Rtl down the next two years. Nonresidential buildings starts in 2023 decline in most markets, but 2023 will still be the 2nd highest year for total Nonres Bldgs starts.

Non-building starts increased more than 100% in July 2022. The 2nd half 2022 was up 50% over 1st half 2022. For 2022, Highway is up 25%, Transportation up 45%, Power up 30% and Public Works up 15%. Starts for 2023 are forecast up 15%. For 2023, every market is forecast up double digits.

Current $ Spending, Inflation and Volume

SEE Construction Inflation 2023

Inflation adjusted volume is spending minus inflation, or to be more accurate, spending divided by (1+inflation). Inflation adds nothing to volume growth. The following table shows spending, inflation and volume (spending without inflation) for each year. All $ are current to the year stated. The values in this table are not indexed to a constant value year. This simply shows business volume in any given year is not as high as spending would indicate. When inflation is positive, volume is always less than spending by the amount attributed to inflation.

Spending during the year is the value of business volume plus the inflation on that volume. When inflation is 12%, volume plus 12% = total spending. Revenue is generally measured by spending put-in-place during the year. In 2022, Nonresidential buildings inflation was 11.9%, so business volume was 11.9% less than spending, or less than revenue. Residential volume was 15.5% less then spending.

SPENDING TOTAL CURRENT $

VOLUME CURRENT $ = SPENDING MINUS INFLATION

CONSTANT $ = VOLUME OVER TIME

Overall Construction Spending is up 25% in the 38 months since the onset of the pandemic, but, during that same period inflation increased 31%. After adjusting for 31% inflation, constant $ volume is down 4%. So, while the plot on the left shows three years of increases in spending, the actual change in business volume is still down and has not yet returned to the pre-pandemic peak in Feb-Mar 2020.

NONRESIDENTIAL SPENDING (CURRENT $) AND VOLUME (CONSTANT $)

Nonresidential Buildings spending in 2023 is forecast at $660 billion, an increase of 26.2%, or $137 billion.

In 2022 we realized the largest ever one-year increase in new nonresidential buildings construction starts, up 40%. Starts were also up 15% in 2021.

The AIA Consensus Construction Forecast, December 2022 predicts only a 5.8% increase in spending for nonresidential buildings in 2023. My beginning of year forecast for comparison was 15.8%. My current forecast is +26.2%. The current year-to-date spending through April is up 30%.

We began the year with record new starts indicating an increasing spending rate. The monthly rate of spending is up 12 of the last 14 months, has increased for 6 consecutive months and is up 20% in the last 6 months. The rate of spending is predicted to increase 10 out of 12 months in 2023, a total increase of 11% over the year. Barring any unforeseen negative occurrence, the trajectory in the rate of spending is increasing.

Year-to-date nonresidential buildings spending for Apr is up 30%. This is driven by Manufacturing, up 84% ytd, but also supported by Lodging up 40% ytd and Commercial/Retail up 23% ytd. Every nonresidential building market except Public Safety (up only 8%) is up greater than 10% ytd.

Nonresidential buildings spending fell 17% from March 2020 to Sept 2021, then increased 48% from Sept 2021 to Apr 2023. Currently, as of Apr 2023, spending is 24% higher than the pre-pandemic peak in Feb 2020. But nonresidential buildings inflation over that same 36 months increased 27%. Business volume in constant $ actually fell 25% from Feb 2020 to Sept 2021, and hit a secondary low in mid-2022. Since then, the actual change in business volume has increased 31%, but that still leaves volume nearly 2% lower than the pre-pandemic high.

Non-building Infrastructure spending for 2023-24 is forecast up 25%, up $50 billion/year for two years. Non-building Infrastructure will post the 1st year of sizable gains since 2019, forecast at $418bil, up 13.5% in 2023. In 2022, Highway and Public Utilities posted strong gains of 9.1% and 16.6%, but those gains were offset by a 8.7% decline in Power. For 2023, Highway and Transportation recorded the strongest starts in five years. All markets post spending gains in 2023, with Highway up 26%, Transportation up 6% and Public Utilities up 18%.

Non-building Infrastructure spending is up 6% since Feb 2020. After adjusting for 27% inflation, constant business volume is down 16%.

RESIDENTIAL SPENDING SF-MF-RENO CURRENT $ AND CONSTANT $

Residential starts are forecast down or flat in 2022 and 2023. Spending grew 44% in the last 2yrs, but inflation was 30% of that 44%. With no growth in starts forecast for 22-23, spending will struggle to keep up with inflation. Residential spending is forecast to fall 8% in 2023. Most of the decline is single family. Single family is down 24% over 12 consecutive down months. Multifamily is up 24% over the same 12 months. But, it’s not an even swap. There’s 3x more spending in SF than in MF. Renovations gained 25% in 2022 but spending varies +/- 10% throughout the year. Midyear there is potential for 6 consecutive down months that could send residential spending down another 7% before year end.

DOES VOLUME OF WORK SUPPORT JOBS GROWTH? or, Can jobs growth support volume of work?

Jobs should track volume, not spending growth. Volume = spending minus inflation. Volume is down, although now increasing, while jobs are up. Nonres Bldgs volume, in constant $, fell 25% from Feb 2020 to Sept 2021, and hit a secondary low in mid-2022. Since then, the actual change in nonres bldgs volume has increased 18%. Yet nonres bldgs jobs increased only 3.5%. That still leaves volume nearly 10% lower than the pre-pandemic high. If the same production levels ($ put-in-place per worker) as 2019 were to be regained, theoretically, nonresidential volume would need to increase 10% with no increase in nonresidential jobs. For now, productivity is well below that of 2019.

Nonresidential Buildings spending in 2023 is forecast at $660 billion, an increase of 26.2%, or an increase of $137 billion in 2023. Non-building Infrastructure spending for 2023-24 is forecast up 25%, up $50 billion/year each year.

Normally, it takes 5000 jobs to put-in-place $1 billion in one year. So an add of $100 billion in 2024 would need 500,000 new jobs. 2023 would need 750,000 new jobs.

If we were to grow the labor force to meet the newly identified workload added from new starts, we would need to double the prior maximum rate of construction jobs growth. Normal growth is about 250,000 jobs per year and maximum prior growth is about 400,000. The workload discussed above would require 750,000 + 500,000 new jobs back to back. That’s an expansion of the industry by 15%, in an industry that normally grows 3%/yr. This industry can’t grow that fast. (Which means I need to account for over-capacity growth as a potential reduction in future forecast. You can’t increase spending that fast if you can’t expand the industry that fast).

My first thoughts were, Jobs may not be able to increase fast enough to put-in-place the forecast spending. This impediment needs to be accounted for and could reduce overall construction spending forecast over the next two years. The most likely markets where a reduction would occur are Manufacturing, Highway, Commercial/Retail and Office.

However this is what happened the past year. In the last 12 months, Mar’22 to Mar’23, nonres bldgs jobs are up 3.5%. Nonres Bldgs spending is up 21%, but after ~7% inflation, volume of nonres bldgs workload is up 14%. So, we have a 3.5% increase in jobs to accomodate a 14% increase in volume.

The last year has shown a huge increase in the volume of nonres bldgs work, without an equal increase in jobs. This shows the excess nonres bldgs jobs for the past three years is now absorbing new workload, (a 3.5% increase in jobs to accomodate a 14% increase in volume), without a cry of jobs shortages.

SEE more discussion on Volume and Jobs

here 2023 Construction Volume Growth

and here Infrastructure Construction Expansion – Not So Fast

Construction Data Briefs APR 2023

Construction is booming. Nonresidential buildings is leading growth. For the first two months of the year, total construction spending year-to-date (ytd) is up 5.9%, but nonresidential buildings spending is up 23% ytd, the fastest rate of nonres bldgs growth in over 20 years. Nonresidential buildings annual rate of spending has increased 19% in the last six months. Nonbuilding spending ytd is up 8%. Nonbuilding annual rate of spending increased 10% in the last four months. Residential spending peaked in March 2022. Since then the annual rate of residential spending has dropped 11%.

Total Construction Spending in 2023 is now forecast to reach $1,894 billion, an increase of 5.3% over 2022.

Nonresidential Buildings spending in 2023 is now forecast at $629 billion, an increase of 20.3% over 2022.

STARTS

The rate of construction spending in 2023 will be influenced predominantly by a 40% increase in new nonresidential building starts in 2022. In recent years, new nonres bldgs starts averaged $300 billion/year. In the 2nd half of 2022, starts averaged over $500 billion/year. Many of those projects will have peak spending in 2023. Some will occur in 2024.

Residential construction (Dodge) starts posted the five highest months ever all in the 1st 6 months of 2022. In the second half of 2022, residential starts fell 15%. In Jan and Feb 2023, starts dropped another 20% below 2nd half 2022. Starts are now down 25% in 12 months.

Nonresidential Bldgs starts in 2022 posted the largest ever one-year increase in new nonresidential buildings construction starts, up 40%. Starts were also up 15% in 2021. Nonres Bldgs new starts in the 2nd half 2022, averaged 67% higher than any other 6mo period in history.

Growth in Manufacturing construction starts for 2022 far surpasses growth in any other market, up over 150%. Office is up 36% (datacenters), Healthcare up 17%, Comm/Rtl up 23% (warehouses).

Non-building starts increased more than 100% in July 2022. The 2nd half 2022 was up 50% over 1st half 2022. Starts for 2023 are forecast up 15%. For 2022, Highway up 25%, Transportation up 45%, Power up 30% and Public Works up 15%.

SPENDING FORECAST

Construction Spending through February 2023 is up 5.9% ytd. Spending is forecast to finish 2023 up 5.3%.

While residential falls back nearly 7% in 2023, Nonresidential buildings is leading with a forecast of 20% spending growth.

Total construction spending for 2023 is on track to increase +5.3%. Residential -6.7%, Nonres Bldgs +20.3%, Nonbldg +13.5%.

SPENDING BY SECTOR CURRENT $ AND INFLATION ADJUSTED CONSTANT $

In 2023, it’s Nonresidential Buildings leading growth. In 2024, it will be Nonbuilding Infrastructure leading spending growth. Both are expected to grow greater than the inflation index.

See also Construction Spending Outlook – Feb 2023

Current $ Spending, Inflation and Volume SEE Construction Inflation 2023

Inflation adjusted volume is spending minus inflation, or to be more accurate, spending divided by (1+inflation). The following table shows spending, inflation and volume (spending without inflation) for each year. All $ are current to the year stated. This table shows that inflation adds nothing to volume growth. All values in this table are current to the year stated. The values in this table are not indexed to a constant value year. This is an attempt to show that business volume in any given year is not as high as spending would indicate. When inflation is positive, volume is always less than spending by the amount attributed to inflation.

Spending during the year is the value of business volume plus the inflation on that volume. When inflation is 12%, volume plus 12% = total spending. Revenue is generally measured by spending put-in-place during the year. In 2022, Nonresidential buildings business volume was 12.2% less than spending, or less than revenue. Residential volume was 15.7% less then spending.

SPENDING TOTAL CURRENT $ AND INFLATION ADJUSTED CONSTANT $

Overall Construction Spending is up 22% in the 36 months since the onset of the pandemic, but, during that same period inflation increased 31%. After adjusting for 31% inflation, constant $ volume is down 7%. So, while the plot on the left shows three years of increases in spending, the actual change in business volume is still down and has not yet returned to the pre-pandemic peak in Feb-Mar 2020.

NONRESIDENTIAL SPENDING (CURRENT $) AND VOLUME (CONSTANT $)

Nonresidential Buildings spending in 2023 is forecast at $629 billion, an increase of 20.3%, or $100 billion and add another $50 billion in 2024.

In 2022 we realized the largest ever one-year increase in new nonresidential buildings construction starts, up 40%. Starts were also up 15% in 2021.

The AIA Consensus Construction Forecast, December 2022 predicts only a 5.8% increase in spending for nonresidential buildings in 2023. My beginning of year forecast for comparison was 15.8%. My current forecast is +20.3%.

We began the year with record new starts indicating an increasing spending rate. The monthly rate of spending is up 12 of the last 14 months, has increased for 6 consecutive months and is up 20% in the last 6 months. The rate of spending is predicted to increase 10 out of 12 months in 2023, a total increase of 11% over the year. Barring any unforeseen negative occurrence, the trajectory in the rate of spending is increasing.

Year-to-date nonresidential buildings spending for Jan+Feb is up 23%. This is driven by Manufacturing, up 53% ytd, but also supported by Lodging up 38% ytd and Commercial/Retail up 23% ytd. Every nonresidential building market except Educational (up only 8%) is up greater than 10% ytd.

Nonresidential buildings spending fell 17% from March 2020 to Sept 2021, then increased 36% from Sept 2021 to Feb 2023. Currently, as of Feb 2023, spending is 14% higher than the pre-pandemic peak in Feb 2020. But nonresidential buildings inflation over that same 36 months increased 26%. Business volume in constant $ actually fell 25% from Feb 2020 to Sept 2021, and hit a secondary low in mid-2022. Since then, the actual change in business volume has increased 18%, but that still leaves volume nearly 10% lower than the pre-pandemic high.

Non-building Infrastructure spending for 2023-24 is forecast up 25%, up $50 billion/year for two years. Non-building Infrastructure will post the 1st year of sizable gains since 2019, forecast at $415bil, up 13.5% in 2023. In 2022, Highway and Public Utilities posted strong gains of 9.1% and 16.6%, but those gains were offset by a 8.7% decline in Power. For 2023, Highway and Transportation recorded the strongest starts in five years. All markets post spending gains in 2023, with Highway up 26%, Transportation up 9% and Public Utilities up 8%.

Non-building Infrastructure spending is up 4% in 36 months since Feb 2020. After adjusting for 26% inflation, constant business volume is down 17%.

RESIDENTIAL SPENDING SF-MF-RENO CURRENT $ AND CONSTANT $

Residential starts are forecast down or flat in 2022 and 2023. Spending grew 44% in the last 2yrs, but inflation was 30% of that 44%. With no growth in starts forecast for 22-23, spending will struggle to keep up with inflation. Residential spending is forecast to fall 7% in 2023. Most of the decline is single family. Single family is down a total of 23% over 10 consecutive months. Multifamily is up 22% over 13 consecutive months. Renovations gained 25% in 2022 but spending varies +/- 10% throughout the year. Midyear there is potential for 6 consecutive down months in residential spending.

DOES VOLUME OF WORK SUPPORT JOBS GROWTH? or, Can jobs growth support volume of work?

Jobs should track volume, not spending growth. Volume = spending minus inflation. Volume is down, although now increasing, while jobs are up. Nonres Bldgs volume, in constant $, fell 25% from Feb 2020 to Sept 2021, and hit a secondary low in mid-2022. Since then, the actual change in nonres bldgs volume has increased 18%. Yet nonres bldgs jobs increased only 3.5%. That still leaves volume nearly 10% lower than the pre-pandemic high. If the same production levels ($ put-in-place per worker) as 2019 were to be regained, theoretically, nonresidential volume would need to increase 10% with no increase in nonresidential jobs. For now, productivity is well below that of 2019.

Nonresidential Buildings spending in 2023 is forecast at $629 billion, an increase of 20.3%, or $100 billion and another $50 billion in 2024. Non-building Infrastructure spending for 2023-24 is forecast up 25%, up $50 billion/year each year.

This growth amounts to an increase of $150 billion in 2023 and $100 billion in 2024. It takes 5000 jobs to put-in-place $1 billion. So $100 billion in 2024 would need 500,000 new jobs. 2023 would need 750,000 new jobs.

If we were to grow the labor force to meet the newly identified workload added from new starts, we would need to double the prior maximum rate of construction jobs growth. Normal growth is about 250,000 jobs per year and maximum prior growth is about 400,000. The workload discussed above would require 750,000 + 500,000 new jobs back to back. That’s an expansion of the industry by 15%, in an industry that normally grows 3%/yr. This industry can’t grow that fast. (Which means I need to account for over-capacity growth as a potential reduction in future forecast. You can’t increase spending that fast if you can’t expand the industry that fast).

4-16-23 update- Everything forecast above is predicated on the normal cash flow of forecast new starts. As of yet, this forecast has not been reduced to reflect the inability of the industry to expand jobs fast enough to absorb the volume of spending generated from forecast starts. Whether new starts get canceled or delayed, spending needs to be reduced annually for at least the next two years simply because jobs cannot increase fast enough to put-in-place the forecast spending. This impediment needs to be accounted for and could reduce overall construction spending forecast by approximately $40-$60 billion in 2023 and $25-$40 billion in 2024. The most likely markets where a reduction would occur are Manufacturing, Highway, Commercial/Retail and Office.

SEE more discussion on Volume and Jobs

here 2023 Construction Volume Growth

and here Infrastructure Construction Expansion – Not So Fast

Construction Briefs Nov’22

Construction is Booming. Well, OK, construction is setting up to be booming in 2023-2024. New construction starts for Sept are down 19% from August and yet starts are still near the highest levels ever. Sept is 4th highest total starts ever, all four of the highest ever months of new starts are in 2022. July and Aug were the two highest months of new starts ever. Total growth in starts over 2021-2022 > Nonres Bldgs +50%, Nonbldg Infra +40%, Residential (all in ’21) +22%.

STARTS

Construction Spending will not be participating in a 2023 recession. Except, residential might. Residential starts in 2021 were up +21% to a really high new high. But starts are forecast flat in 2022 and 2023. Spending grew 44% in the last 2yrs, but inflation was 30% of that 44%. With zero growth in starts forecast for 22-23, spending struggles to keep up with inflation. Residential will post only an increase of 3% in 2023 spending, but midyear there is potential for 6 consecutive down months.

See also Construction Year-End Spending Forecast Dec’22

SPENDING BY SECTOR CURRENT $ AND INFLATION ADJUSTED CONSTANT $

Nonresidential Buildings new starts last 2yrs (2021-2022) are up 50%. Spending next 2yrs (23-24) is forecast up 21%.

Nonbldg starts 2022-23 are forecast up 38%. Spending 2023-24 forecast up 20%.

In 2023, it’s Nonresidential Buildings leading growth. In 2024, it will be Nonbuilding Infrastructure leading spending growth. Both are expected to grow more than the inflation index, so there will be real volume growth to report.

Residential construction (Dodge) starts since Jan 2021 have posted 17 out of 21 months of the highest residential starts ever posted. The 5 highest months ever are all in 2022.

Nonresidential Bldgs starts in Sept dropped 23% from August and yet still that was the 3rd highest month ever. July and August were 2nd and 1st.

Construction starts for Nonresidential Bldgs posted each of the last 4 (consecutive) months thru October higher than any months ever before. The avg of last 4 (consecutive) months is 33% higher than the avg of the best previous 4 mo ever (even non-consecutive). Growth in Manufacturing construction starts for 2022 far surpasses growth in any other market, up over 150% year-to-date.

Construction Spending Sept total up 0.2% from Aug. Aug & Jul were revised up 1.1% & 1.3%. Total spending YTD thru Sept’22 is up 11.4% from Sept’21. MAJOR movers; Mnfg up 16% since Jun. Jul & Aug were revised up 7.4% & 8.4%. Highway is up 9% since June. Jul & Aug were revised up by 4.0% & 4.4%.

SPENDING FORECAST

Total construction spending for 2022 is on track to increase +11.1%. Residential +16.8%, Nonres Bldgs +9.5%, Nonbldg +0.5%.

Comm/Rtl +18% Mnfg +32% Power -8% Pub Utilities +14%.

Current and predicted Inflation SEE Construction Inflation at Year-End 2022

Inflation adjusted volume is spending minus inflation.

Total volume for 2022 falls 1%. Rsdn +3%, Nonres Bldgs -1%, Nonbldg -9%.

Total volume for 2023 is up 1%. Rsdn -3%, Nonres Bldgs +8%, Nonbldg +2%.

SPENDING TOTAL ALL $ CURRENT $ AND INFLATION ADJUSTED CONSTANT $

Overall Construction Spending is up 15% since the onset of the pandemic, but, after adjusting for 25% inflation, volume is down 10%. Residential jobs are near even on track with volume, but Nonres and Nonbldg have volume deficits of approx 20-25% vs jobs.

- Feb 2020 to Aug 2022

- Resdn spend +42%, vol +6.5%, jobs +7%

- Nonres Bldgs spend -8%, vol -24%, jobs -3%

- NonBldg spend -7.5%, vol -24%, jobs +1%

JOBS VS CONSTRUCTION VOLUME VS SPENDING (VOL = SPENDING MINUS INFLATION

Labor Shortage? Jobs should track volume, not spending growth. Vol = spending minus inflation. Volume is down while jobs are up. If the same production levels ($ put-in-place per worker) as 2019 were to be regained, theoretically, nonresidential volume would need to increase 20% with no increase in nonresidential jobs. I don’t expect that to occur, therefore, productivity will remain well below that of 2019.

LABOR PRODUCTIVITY

Over the next year or two, there could be several billion$ of construction spending to repair hurricane damaged homes in Florida. That spending will NOT be reported in Census spending reports. Renovations to repair natural disaster damage are not recorded in construction spending. Construction spending to replace homes entirely lost to damage IS reported in Census spending, but is reported as renovations/repair, not new SF or MF construction.

RESIDENTIAL SPENDING SF-MF-RENO CURRENT $ AND CONSTANT $

Construction Economics – An Eye on Forecasts

5-5-21

How can you tell if your preferred construction economic forecast is on track to finish the year as predicted?

For comparison, in the following link I’ve collected initial 2021 construction spending forecasts from nine different sources. Measuring Forecasting Methodology & Accuracy

As of 5-3-21, three months of actual data are in. The first step is to compare that current actual data to the predictions. The next step is to use a bit of math to answer the question, Can we get there from here?

Here’s examples:

First let’s look at Lodging. In the AIA initial 2021 Outlook, ABC forecast -13% and Moody’s forecast -52%. Current spending year to date through March is -25%. Are either of these forecasts achievable?

Lodging construction starts dropped 11% in 2019 and dropped another 50% in 2020. The seasonally adjusted annual rate (SAAR) of spending fell from $33bil in Q1 2020 to $24bil in Q1 2021, down 27%. The current rate of spending is coming in between 25%-30% below same month last year (yoy).

Now do the math.

Look at the ABC forecast for lodging. To finish the year down -13%, monthly spending needs to average -13% for all 12 months of 2021. 12 months x -13% = -157. But 3 months, down cumulatively 25%, are already known. 3 months x -25% = -75. What would need to occur for the last 9 months to reach a total 2021 spending down -13%?

12 x -13% = -157 minus 3 x -25% = -75, therefore -157 minus -75 = -82. In the remaining nine months, Lodging would need to fall a cumulative 82%, or 82/9 = an average of 9%/month.

Well, the current rate of spending is down 25% yoy and construction starts the previous two years are down 60%. Cash flows seem to indicate spending will not increase this year. There is little hope of seeing an increase in monthly spending in 2021. Since new starts are less than half of only two years ago, spending is unlikely to increase from a monthly rate down 25% to a monthly rate down only 9% for the next nine consecutive months. Therefore this forecast is unlikely to play out. The ABC forecast is too optimistic.

*********************************

Now let’s look at the Moody’s forecast for lodging. To finish the year down -52%, monthly spending needs to average -52% for all 12 months of 2021. 12 months x -52% = -624. But 3 months, down cumulatively 25%, are already known. 3 months x -25% = -75. What would need to occur for the last 9 months to reach a total 2021 spending down -52%?

12 x -52% = -624 minus 3 x -25% = -75, therefore -624 minus -75 = -549. In the remaining nine months, Lodging would need to fall a cumulative 549%, or 549/9 = an average of 61%/month.

Well, the current rate of spending is down 25% yoy and construction starts the previous two years are down 60%. Cash flows are indicating monthly spending will drop 3% to 4% per month this year. Spending would need to decline 61-25=36% in one month and stay at that rate for the remainder of the year, OR, spending would need to start falling at a rate of 12%/month and continue 12% lower every month for the remainder of the year. By December, spending would be down over 100%, so this is not even feasible. Therefore this forecast cannot play out. The Moody’s forecast is far too pesimistic.

*********************************

Second, let’s look at Manufacturing. In the AIA initial 2021 Outlook, ABC forecast +6.5% and Moody’s forecast -3.4%. Current spending year to date through March is -9%. Are either of these forecasts achievable?

Manufacturing construction starts dropped 10% in 2019 and dropped another 57% in 2020. The seasonally adjusted annual rate (SAAR) of spending fell from $78bil in Q1 2020 to $71bil in Q1 2021, down 10%. The current rate of spending is coming in between 7%-11% below same month last year (yoy).

*********************************

Look at the ABC forecast for manufacturing. To finish the year up +6.5%, monthly spending needs to average +6.5% for all 12 months of 2021. 12 months x +6.5% = +78. But 3 months, down cumulatively 9%, are already known. 3 months x -9% = -27. What would need to occur for the last 9 months to reach a total 2021 spending up+6.5%?

12 x +6.5% = +78 minus 3 x -9% = -27, therefore +78 minus -27 = +105. In the remaining nine months, Manufacturing would need to gain a cumulative 105%, or 105/9 = an average of +12%/month.

Well, the current rate of spending is down 9% yoy and construction starts the previous two years are down 67%. Cash flows seem to indicate spending will continue to drop at a rate of 2% to 3% per month this year. There is little hope of seeing an increase in monthly spending in 2021. Since new starts are down 67% from two years ago, spending is unlikely to increase from a monthly rate down 9% to a monthly rate up 12%, a swing of 21%, for the next nine consecutive months. Therefore this forecast is highly unlikely to play out. The ABC forecast is far to optimistic.

*********************************

Now let’s look at the Moody’s forecast for manufacturing. To finish the year down -3.4%, monthly spending needs to average -3.4% for all 12 months of 2021. 12 months x -3.4% = -41. But 3 months, down cumulatively 9%, are already known. 3 months x -9% = -27. What would need to occur for the last 9 months to reach a total 2021 spending down +3.4%?

12 x -3.4% = -41 minus 3 x -9% = -27, therefore -41 minus -27 = -14. In the remaining nine months, Manufacturing would need to fall a cumulative -14%, or -14/9 = an average of -1.5%/month.

Well, the current rate of spending is down 9% yoy and construction starts the previous two years are down 67%. Cash flows are indicating monthly spending will drop 2% to 3% per month, every month this year. Spending would need to begin falling at a rate of only -1.5%/month and continue -1.5% lower every month for the remainder of the year. A decline of 67% in starts over the previous two years solidifies a rate of decline beyond that at near 3%/month. This scenario would depend on cutting the rate of decline in half for the remainder of the year, but the lack of starts in previous years provides no help to achieve that goal. The Moody’s forecast is too optimistic.

*********************************

It’s in your best interest to know how to assess the plausibility of forecast components before you question an analysis that varies widely from your preferred forecast. It may be your preferred forecast that is way off.

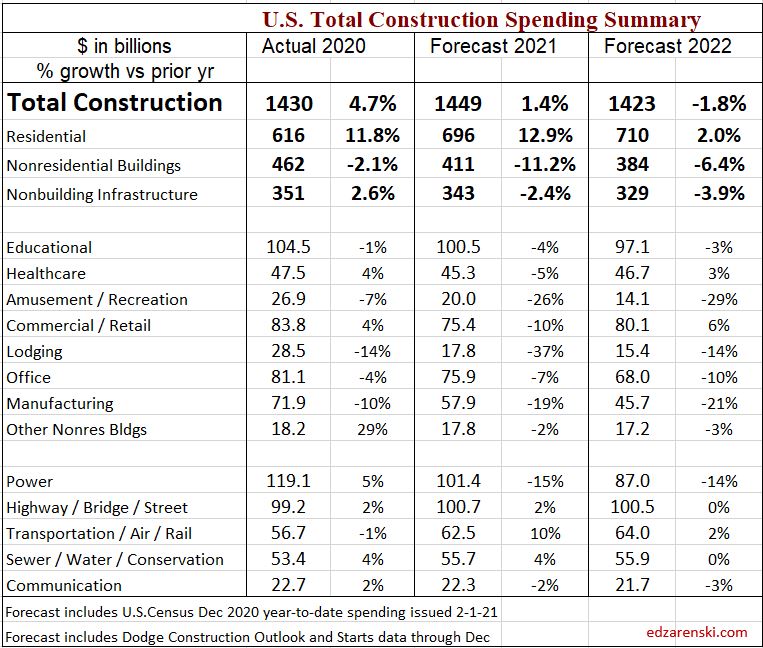

2021 Construction Economic Forecast – Summary

Initial Construction Outlook 2021, 2-5-21, based on data from:

- Actual Jobs data includes BLS Jobs to Jan 16th, issued 2-5-21

- Forecast includes US Census Dec 2020 year-to-date spending as of 2-1-21

- Forecast includes Dodge Outlook 2021 and Dec construction starts 1-19-21

SUMMARY – CONCLUSIONS

Construction Spending drives the headlines. Construction Volume drives jobs demand. Volume is spending minus inflation. Current outlook shows the most recent peak volume was 2017-2018. Total Volume is forecast to decline every year out to 2023, but Residential is rising, Nonresidential is falling.

When spending increases less than the rate of inflation, the real work volume is declining. Nonresidential buildings spending for 2020 is down -2%, but with 3% to 5% inflation, volume is down 5% to 7%. The extent of volume declines would impact the jobs situation.

STARTS – BACKLOG – SPENDING

By far the greatest impact of the pandemic on construction is the massive reduction in new nonresidential construction starts in 2020 that will reduce spending and jobs in that sector for at least the next two years. Residential continues to increase.

- 2020 new starts declined -8%. Res +7%, Nonres Bldgs -24%, Nonbuilding -14%.

- New starts for residential reached an all-time high in 2020. Expect up +5% in 2021.

Nonresidential construction starts in backlog at the beginning of the year provide for 75% to 80% of all spending in 2021. New starts in 2020 were down 24% for buildings and 14% for non-buildings, so backlog is down. It would be difficult to show any scenario that has these sectors up in 2021.

Construction has yet to experience the greatest downward pressure from the pandemic. After hitting a post-pandemic spending high in December, spending and jobs losses won’t hit bottom until 2022. Nonresidential declines outweigh Residential gains.

- Spending forecast for 2021 is up +1.4%, but nonresidential buildings is down -11%.

- Almost all gains in spending are due to large 12%/yr gain in residential.

The largest declines in 2021 spending are Lodging -37%, Amusement/Recreation -26%, Manufacturing -19% and Power -15%.

PROJECT COST ESCALATION – INFLATION

- Inflation for nonresidential buildings near 4% the next few years. Residential 5% to 6%.

VOLUME – JOBS

Construction Jobs annual average for 2020 is down 220,000 jobs. The current spending forecast is indicating that December 2020 was the highpoint for jobs. Residential jobs will be up in 2021, but Nonresidential Buildings jobs are down steep. Net jobs will be down 15 of next 18 months. Forecast 2021 net annual average jobs losses of -200,000. Nonresidential Buildings 2021 jobs losses will outweigh residential gains.