A few brief comments. More comments to follow

See also Construction Briefs Nov’22

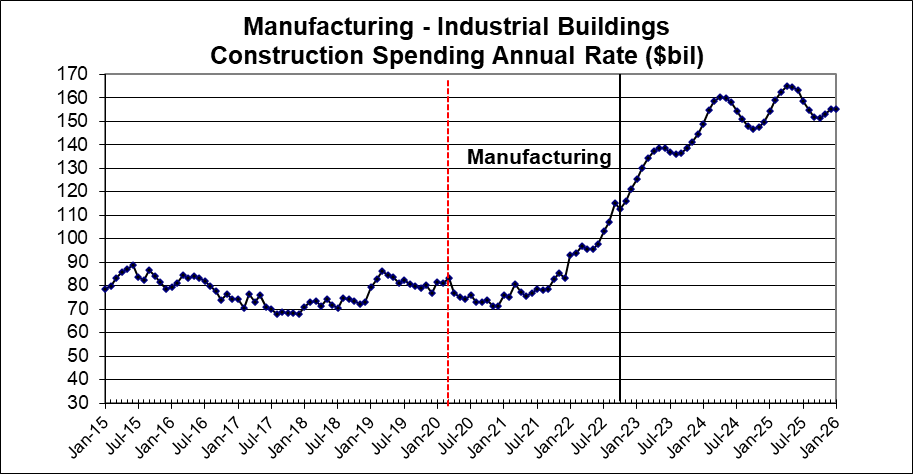

With only one month to go and eleven months in the year-to-date spending, we should see very little variance from the Forecast for 2022, which is expected to finish up 10.1% at $1,791 billion. Residential spending will finish up 13.4% even though it’s posted declines in six of the last eight months and is down 13% since March. Nonresidential Buildings spending, expected to finish up 10.9%, is being driven by Commercial Retail (up 20%, in this case Warehouses) and Manufacturing, which will finish the year up over 35%. Non-building Infrastructure finishes the year up only 1.9% due to a large drop off in Power spending. Highway and Public Utilities helped offset some of the Power decline.

Total construction spending for 2023 is forecast to increase +5.1%. Residential -2%, Nonres Bldgs +15%, Nonbldg +8%.

Some high $ items: Comm/Rtl +16%, Manufacturing +35%, Highway +11%, Transportation +16%, Pub Utilities +12%.

Residential starts in 2021 were up +21% to a lofty new high. But starts are forecast flat in 2022 and 2023. Spending grew 44% in the last 2yrs, but inflation was 30% of that 44%. With zero growth in starts forecast for 22-23, residential spending struggles to keep up with inflation. Residential spending will post a decrease of 2% in 2023. If inflation is 5%, that’s an 7% loss of business volume. Midyear there is potential for 6 consecutive down months.

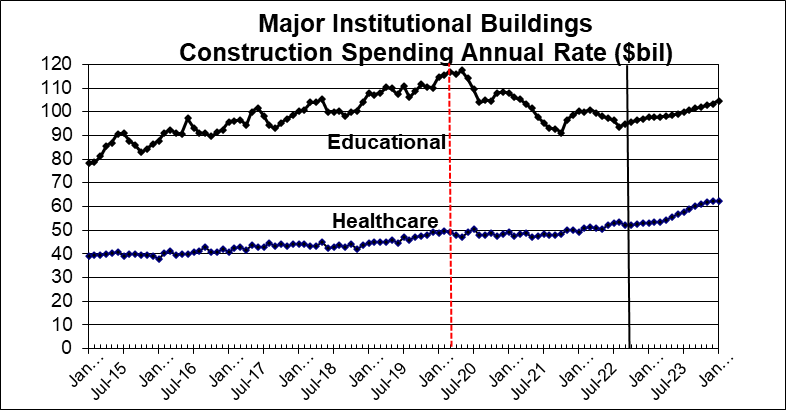

Nonres Bldgs new starts last 2yrs (2021-2022) are up 50%. Spending next 2yrs is forecast up 20%.

Nonresidential Bldgs starts in Sept dropped 23% from August and yet still that was the 3rd highest month ever. July and August were 2nd and 1st. October starts added another 9% over Sept., taking over the 3rd best spot. Even though November dropped 25% from Oct., Nov. starts are still higher than the 1st half 2022 average.

Construction starts for Nonresidential Bldgs posted each of the last 4 months thru October higher than any months ever before. The avg of last 4 months is 33% higher than the avg of the best previous 4 mo ever (even non-consecutive).

Growth in Manufacturing construction starts for 2022 far surpasses growth in any other market, up over 150% year-to-date. Spending for Manufacturing Bldgs is expected to increase more than 30% in 2023. This seems high after already increasing 35% in 2022, but when taking into consideration that the expected spending for 2023 is only 15% higher than where we stand already in Q4 2022, it seems much more reasonable.

Backlog as we begin 2023 is up 16% over 2022, all nonresidential.

Inability to expand staff fast enough to match spending growth may limit some spending to lower than forecast.

Nonbuilding Infrastructure starts for 2022-23 are forecast up 37%. Spending 2023-24 is forecast up 20%. Starts since July are up 50% over the 1st half 2022 average. Highway/Bridge/Street starts increased almost 25% in 2022 and are forecast to increase 20% in 2023. Highway spending is up 9% in 2022, then increases 11% in 2023. A bigger spending increase of 16% occurs in 2024. Transportation starts will drop more than 30% in 2023, but that comes after a 100% increase in 2022. Transportation spending will jump 16% in 2023. Public Utilities, Sewer-Water-Conservation, collectively will post 60% growth in starts for 2021-22-23. Spending for this group increases 45% for 2022-23-24.