Home » Posts tagged 'Estimating'

Tag Archives: Estimating

Next Level of Tariffs Will Be Unknowns

Assessing the impact of this next level tariffs on the cost of construction has now become a nearly impossible task. Tariffs are on PARTS use in manufacture of goods. Who (architect? engineer?) will identify what parts are included in which products used in the building?

For example, look at something simple like light fixtures. The shell, the ballast, the reflector, the shade, the lamps or the wiring could be made in China. Who identifies where parts are made? Who now estimates the share of tariff increase on those parts to determine tariff impact on cost of manufacturing the entire light fixture?

Expand that issue to a pump assembly with valves and pressure gauges. Who identifies which parts in the pump assembly come from what country? How does an estimator determine the cost of manufacturing the pumps, valves and gauges and determine what fraction of total cost has a tariff?

This will inevitably lead to inflation, but it will be hidden inflation, hard to determine if a manufacturer’s price increase for a product is substantiated. This is not like the tariff on mill steel, a 25% tariff on mill steel which represents 25% of final structural steel bid, which represents 10% of the building cost.

At the conceptual or schematic design phase of construction, all the products are not even identified. And the project start date might be two years out. It can’t possibly be determined with certainty what factor should be carried to cover cost increases due to tariffs.

Inflation factors and contingency factors will need to increase to cover unknown costs. This increases the share of the budget that is unidentified, always a contentious issues with owners. Frankly with the margins general contractors or construction managers get for services on a large construction project, these unknown factors, if understated in cost factors, could wipe out the total fee or profit for the job.

This is not a good position to be in, but I don’t yet see how it would be any different.

Notre Dame Cathedral Repairs

I’ve read a few news articles that proclaimed charitable donations to Notre Dame may not be enough to cover the cost to rebuild the damaged cathedral roof. One article on Bloomberg news stated, “The cost might well run as high as 8 billion euros”.

I think it’s time some news sources engage with a professional architect, engineer and cost estimator before writing these articles. 8 billion Euros is enough to spend an astronomical amount to repair the damage!

One World Trade Center is the most expensive building built in the U.S. It cost $4 billion. It measures 3.5 million square feet (SqFt).

Some sources are saying the Notre Dame cathedral roof repair may cost more than $8 billion. The Notre Dame roof, as closely as I can determine from online data of the building, measures about 50,000 SqFt.

Just think about that.

I’m stretching my thought process to come up with a rough estimate that would cost as high as $250 million. Frankly, my rough estimate is quite a bit lower than that, and that would still be far more costly per SqFt than the most expensive building in the U.S.

I haven’t yet seen an architect / engineer estimate of the total area of the roof. I traded some emails with an architect who thought total area was 25,000 SqFt. I searched online and come up with potential area of roof at 50,000 SqFt. Here I’m using 50,000 SqFt.

I have not seen any other realistic cost estimates. But, the most expensive roof covering and roof structure I’ve ever estimated was less than $100/SqFt (in 2019 dollars).

My order of magnitude estimate (OME) (very general), for a unique, complex structure and premium roof covering could be $500/SqFt. Portions of this roof need to be quite ornate and also the estimate must include a ceiling structure. For a historical and rare roof plus inside work let’s double that estimate to $1000/SqFt. That’s 10x the cost of the most expensive roof I’ve ever estimated / built.

$1 billion would provide for $20,000/SqFt.

$8 billion would provide for $160,000/SqFt!

Even if my OME is 10x too low and I make a 10x adjustment, cost would then be $10,000/SqFt for a total cost = $500 million. That’s 100x more expensive than the most costly roof I’ve ever estimated. Frankly, I can’t come up with any conceivable scenario where it could cost that much.

footnote: 8 billion Euros is currently about $9 billion US dollars

Apr 2025 – News articles that I’ve seen state that the repair cost $700-$800 million.

Reliability of Predicted Construction Forecast Data

10-2-18

It’s not uncommon that clients ask for a forecast of construction spending for the next three years. It is less common that forecasters explain the reliability of the data in a forecast.

To predict the reliability of the data in a forecast, several assumptions must be stated.

Cash flow curves are generated to predict the spending pattern. These are assumed to be reliable. The cash flows are generated from monthly data releases for New Construction Starts. The Starts data is assumed reliable. However, major sector data is revised in the following month and again in the same month the following year. These revisions are incorporated when released, but nonresidential building markets revisions are not posted at the same frequency. That data becomes available in the 4th quarter report of the following year. It is updated at that time. The analytical methods are assumed to be reliable.

The primary driver of the spending forecast is New Construction Starts. Care must be taken to use Starts properly. Starts are sometimes misinterpreted in common industry forecasting articles. Starts dollar values represent a survey of about 50% to 70% of industry activity and that varies by market type, therefore Starts dollar values cannot ever be used directly to indicate the volume of spending. Also, Starts do not directly indicate changes in spending per month or per year. Projected starts data cannot be used to directly forecast expected construction volume. Only by including an expected duration for all Starts and producing a forecast Cash Flow from Starts data can the expected pattern of future backlog and spending be developed.

For short duration residential spending, single-family residential and renovations work, approximately 75% of the spending occurs in the current year and 20% in the following year.

For long duration residential spending, typical of multifamily residential, approximately 50%-55% of the spending occurs in the current year, 35%-40% in the next year and only 5%-10% occurs two years out.

For nonresidential buildings spending long duration jobs can sometimes have a 5 to 6-year schedule. On average most years have at least some projects start that will be under construction for 4 years. For an entire year’s worth of starts, approximately 20% of the spending occurs in the year started, 50% in the next year, 25% in the third year and only 5% in the fourth year or later year. This also means that nonresidential spending growth in 2019 is still being affected by starts from 2016.

Non-building Infrastructure spending has many of the longest duration jobs. Some job starts in the last two years have 6 to 8-year duration. Many years have at least some projects start that will be under construction for 5 years. For the entire year of starts, approximately 15% of the spending occurs in the year started, 40% in the next year, 33% in the third year and 12% in the fourth year or later year. This also means that non-building Infrastructure spending growth in 2019 is still being affected by jobs that started in 2015.

- 75%-80% of all Nonresidential Buildings spending within the year will be generated from projects in starting backlog.

- 80%-85% of all Non-Building Infrastructure spending within the year will be generated from projects in starting backlog.

- 70% of All Residential spending within the year is generated from new starts, but this is weighted because 85% of all residential work is short duration single family and renovation work.

- 65% on long duration Multifamily Residential spending within the year will be generated from projects in starting backlog.

Multifamily residential has a longer duration and a much greater percentage of spending comes from backlog. But, due to the shorter duration of projects, about 75% of single family and residential renovation spending within the year is generated from new starts. Unlike nonresidential, backlog does not contribute nearly as much short-term residential spending within the year. For that reason, the reliability of SF and Reno residential work drops more quickly than all other types.

For any future forecast month, the most information is in hand the month before. For example, in the month of October the forecast for November includes a projected cash flow which is based 96%-98% on actual projects. Only the small amount from new projects that start in November is predicted. Assessing the amount of actual data versus the amount of predicted data gives an indication of how much weight can be placed on the forecast. Obviously, the balance of actual versus predicted data changes the further out in time we view the forecast.

From the current date, the forecast for the next month includes 95%-98% actual data. Only the cash flow curve and the predicted duration affects the reliability of the forecasts and even that is minor.

Twelve months from the current date, the forecast is more dependent on predicted starts and therefore the percentage of actual data drops. The Non-building Infrastructure forecast includes 85% actual data. The Nonresidential Buildings forecast includes 80% actual data. The Residential forecast includes 30%-40% actual data.

Two years out from the current date, the forecast is far more dependent on predicted starts. The Non-building Infrastructure forecast includes 45% actual data. The Nonresidential Buildings forecast includes 30% actual data. The actual data in a residential forecast drops to near zero with very little remaining in backlog and that only from multifamily.

Three years out from the current date, the forecast is near entirely dependent on predicted starts. The Non-building Infrastructure forecast includes about 15% actual data. The Nonresidential Buildings forecast is approaching zero. The residential forecast has already be reliant on predicted data for the past year.

To put this in perspective, let’s assume a Jan 1, 2019 forecast which includes all actual construction starts through Dec 2018. We’ll look at the forecast for 2020 and 2021. Also, we’ll base the volume of actual data on each sector’s actual data and its share of total construction spending. Non-building Infrastructure has the most actual data long term, but it is the smallest share of total construction. Residential has the least long-term data but is the largest share of total construction.

In my Jan. 1, 2019 forecast, the forecast for the year 2020, the period only 12 to 24 months out, actual data drops from 60% at the start of the year to 20% at the end. So, the 2020 forecast includes only an average of 40% actual data. In the forecast for the year 2021, the period from 24 to 36 months out, the actual data drops from 20% to 4% over the course of the year. Very little actual data is influencing the forecast.

Three years out from the current date the reliability of the forecast is dependent on the economic outlook of the developer and the predictive methodology of the analytic tools.

It’s good to know, when you are looking at a forecast that projects three years out past the current year, there is nearly no actual data in that forecast. It’s all predicted.

Inflation in Construction 2019. What Should You Carry?

1-28-20 See the latest post Construction Inflation 2020

8-26-19 go to this article for Added links to sources for international construction inflation rates

1-14-20 added new index table covering 2015-2023 at Index Table Link – see link to Tables below

This table updates 2018 and 2019 data and 2020-2023 forecast. Nonresidential inflation, after hitting 5% in both 2018 and 2019, is forecast for the next three years to fall from 4.4% to 3.8%, lower than the 4.5% avg for the last 4yrs. Forecast residential inflation for the next three years is level at 3.8%. It was only 3.6% for 2019 but averaged 5.5%/yr since 2013.

When construction is very actively growing, total construction costs typically increase more rapidly than the net cost of labor and materials. In active markets overhead and profit margins increase in response to increased demand. These costs are captured only in Selling Price, or final cost indices.

General construction cost indices and Input price indices that don’t track whole building final cost do not capture the full cost of inflation on construction projects.

To properly adjust the cost of construction over time you must use actual final cost indices, otherwise known as selling price indices.

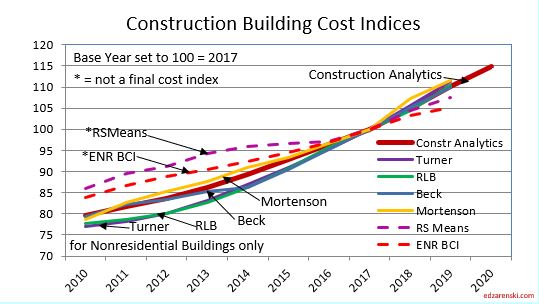

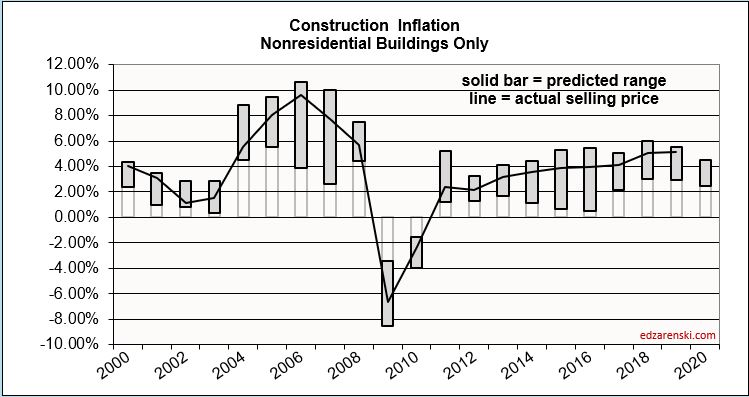

ENRBCI and RSMeans input indices are examples of commonly used indices that DO NOT represent whole building costs, yet are widely used to adjust project costs. An estimator can get into trouble adjusting project costs if not using appropriate indices. This plot of cost indices for nonresidential buildings shows how input indices did not drop during the 2008-2010 recession while all other final cost indices did drop.

CPI, the Consumer Price Index, tracks changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. The CPI is not related at all to construction and should not be used to adjust construction pricing. Historically, Construction Inflation is about double the CPI, but for the last 5 years construction inflation averages 3x the CPI.

Producer Price Index (PPI) Material Inputs (which exclude labor) to new construction increased +4% in 2018 after a downward trend from +5% in 2011 led to decreased cost of -3% in 2015, the only negative cost for inputs in the past 20 years. Input costs to nonresidential structures in 2017+2018 average +4.3%, the highest in seven years. Infrastructure and industrial inputs were the highest, near 5%. But material inputs accounts for only a portion of the final cost of constructed buildings.

Materials price input costs in 2019 slowed to an annual rate of less than 1%.

Labor input is currently experiencing cost increases. When there is a shortage of labor, contractors may pay a premium to keep their workers. Unemployment in construction is the lowest on record. The JOLTS ( Job Openings and Labor Turnover Survey) is at or near all-time highs. A tight labor market will keep labor costs climbing at the fastest rate in years.

Click Here for Link to a 20-year Table of 25 Indices

Inflation can have a dramatic impact on the accuracy of a construction budget. Usually budgets are prepared from known current costs. If a budget is being developed for a project whose midpoint of construction costs is two years in the future, you must carry an appropriate inflation factor to represent the expected cost of the building at that time.

The level of construction activity has a direct influence on labor and material demand and margins and therefore on construction inflation. Nonresidential Buildings and Non-building Infrastructure backlog are both at all-time highs. 75% to 80% of all nonresidential spending within the year comes from starting backlog.

Although nonresidential buildings new starts are up only 5% the last three years, spending from backlog in 2020 is up 20% in three years and reaches an all-time high.

Most spending for residential comes from new starts. Residential new starts in Q1-2018 reached a 12 year high. Spending from new starts in 2019 fell 6% but is up 6% for 2020. Spending from new starts in 2020 is back to the level posted in 2017 and 2018.

2020 starting backlog is up 5.5% across all sectors. However, while a few markets will outperform in 2020 (transportation, public works, office), predicted cash flow (spending) from backlog is up only 1% to 2%.

Although many contractors report shortages due to labor demand, labor growth may slow due to a forecast 2019-2020 construction volume decline. But, we might see a labor decline lag spending/volume decline.

Expect 2019 escalation in almost all cases to finish at or lower than 2018.

Residential construction inflation in 2019 was only 3.6%. However, the average inflation for six years from 2013 to 2018 was 5.5%. It peaked at 8% in 2013, but dropped to 4.3% in 2018 and only 3.6% in 2019. Residential construction volume in 2019 dropped 8%, the largest volume decline in 10 years. Typically, large declines in volume are accompanied by declines in inflation. Forecast residential inflation for the next three years is level at 3.8%.

Note 8-2-19: Residential inflation for the 1st half of 2019 has come in at only 3.5%.

A word about Hi-Rise Residential. Probably all of the core and shell and a large percent of interiors cost of a hi-rise residential building would remain the same whether the building was for residential or nonresidential use. This type of construction is totally dis-similar to low-rise residential, which in large part is stick-built single family homes. Therefore, use the residential cost index for single family but a more appropriate index to use for hi-rise residential construction is the nonresidential buildings cost index.

Nonresidential inflation, after hitting 5% in both 2018 and 2019, is forecast for the next three years to fall from 4.4% to 3.8%, lower than the 4.5% average for the last 4 years. Spending needs to grow at a minimum of 4.4%/yr. just to stay ahead of construction inflation, otherwise volume is declining. Spending slowed dramatically in 2019. However, new starts in 2018 and 2019 boosted backlog and 2020 spending will post the strongest gains in four years.

Material tariffs in 2018 and 2019 are already incorporated into inflation. Adjust for any new tariffs impact.

In another article on this blog, (see steel cost increase), I calculated the 25% tariff on steel would cost nonresidential buildings 1%. Some Infrastructure could be much more, i.e., bridges 4-5%. Residential impact would be small. A 25% increase in mill steel could add 0.65% to final cost of building just for the structure. It adds 1.0% for all steel in a building. If your building is not a steel structure, steel still potentially adds 0.35%.

Note 8-2-19: Nonresidential Buildings inflation for the 1st half of 2019 as tracked by most national selling price indices has come in at just over 5%.

Reliable nonresidential buildings selling price indexes have been over 4% since 2015. Some have averaged over 5% for the last four years. Construction Analytics forecast (line) for 2019 is currently 5.1%. This may move higher due to the impact of September 2019 tariffs which are not yet reflected in any indices.

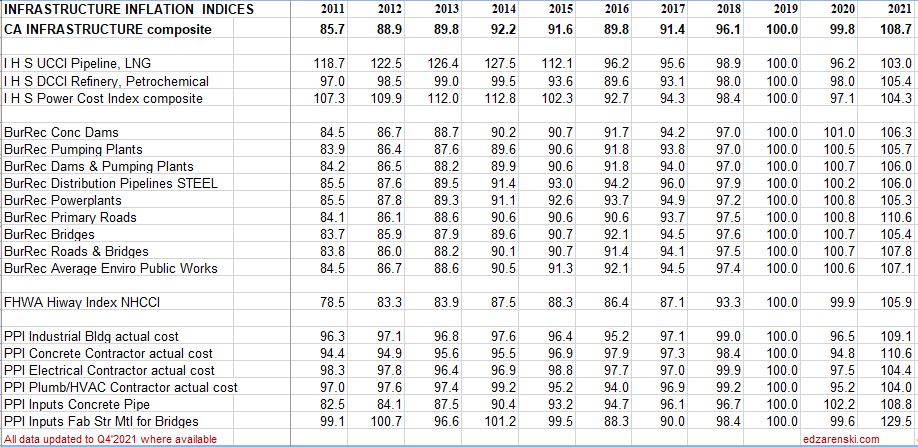

Non-building infrastructure indices are so unique to the type of work that individual specific infrastructure indices must be used to adjust cost of work. The FHWA highway index increased 17% from 2010 to 2014, stayed flat from 2015-2017, then increased 15% in 2018-2019. The IHS Pipeline and LNG indices increased 4% in 2019 but are still down 18% since 2014. Coal, gas, and wind power generation indices have gone up only 5% since 2014. Refineries and petrochemical facilities dropped 10% from 2014 to 2016 but regained all of that by 2019. BurRec inflation for pumping plants and pipelines has averaged 2.5%/yr since 2011 and 3%/yr the last 3 years.

Anticipate 3% to 4% inflation for 2019 with the potential to go higher in rapidly expanding Infrastructure markets, such as pipeline or highway.

This link refers to Infrastructure Indices.

Watch for unexpected impacts from tariffs. Steel tariff could potentially add 5% to bridges. Also impacted, power industry, pipeline, towers, transportation.

- Long term construction cost inflation is normally about double consumer price inflation (CPI).

- Since 1993 but taking out 2 worst years of recession (-8% to -10% total for 2009-2010), the 20-year average inflation is 4.2%.

- Average long term (30 years) construction cost inflation is 3.5% even with any/all recession years included.

- In times of rapid construction spending growth, construction inflation averages about 8%.

- Nonresidential buildings inflation has average 3.7% since the recession bottom in 2011. It has averaged 4.2% for the last 4 years.

- Residential buildings inflation reached a post recession high of 8.0% in 2013 but dropped to 3.4% in 2015. It has averaged 5.8% for the last 5 years.

- Although inflation is affected by labor and material costs, a large part of the change in inflation is due to change in contractors/suppliers margins.

- When construction volume increases rapidly, margins increase rapidly.

- Construction inflation can be very different from one major sector to the other and can vary from one market to another. It can even vary considerably from one material to another.

The two links below point to comprehensive coverage of the topic inflation and are recommended reading.

Click Here for Link to a 20-year Table of 25 Indices

Click Here for Cost Inflation Commentary – text on Current Inflation

Construction Inflation >>> LINKS

- 10-24-16 Originally posted

- 2-11-22 added INFRASTRUCTURE index table Q4 2021

This post is preserved for the multitude of LINKS back to sources of cost indices and for the explanation of the difference between Input indices and Output or Final Cost Indices. For all latest indices plots and table see the latest yearly Inflation post.

2-20-25 SEE Construction Inflation 2025

2-1-23 SEE Construction Inflation 2023

2-11-22 SEE Construction Inflation 2022

11-10-21 See 2021 Construction Inflation

See the article Construction Inflation 2020

Construction Cost Indices come in many types: Final cost by specific building type; Final cost composite of buildings but still all within one major building sector; Final cost but across several major building sectors (ex., residential and nonresidential buildings); Input prices to subcontractors; Producer prices and Select market basket indices.

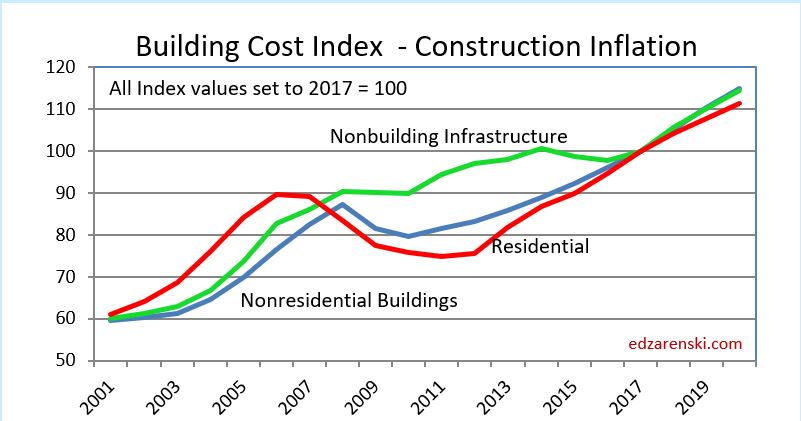

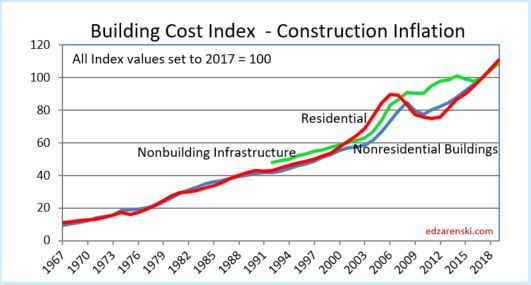

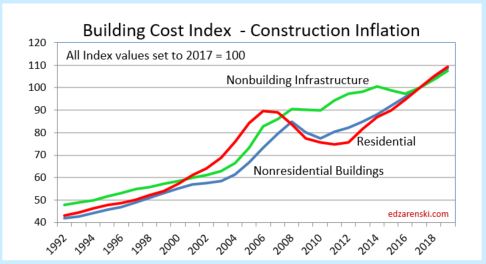

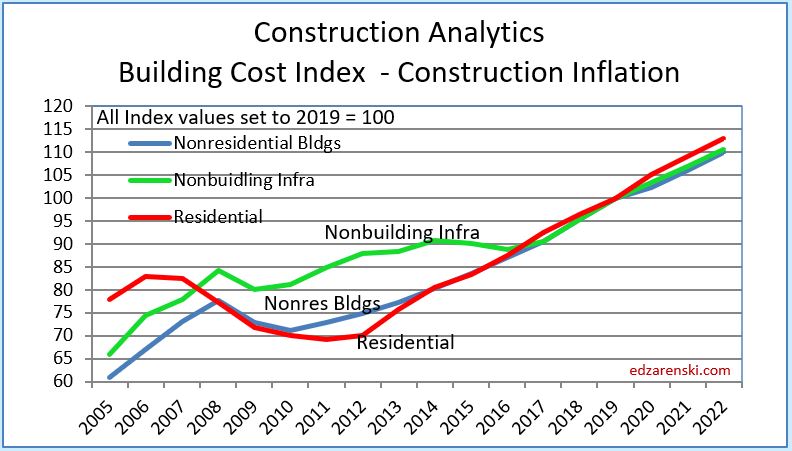

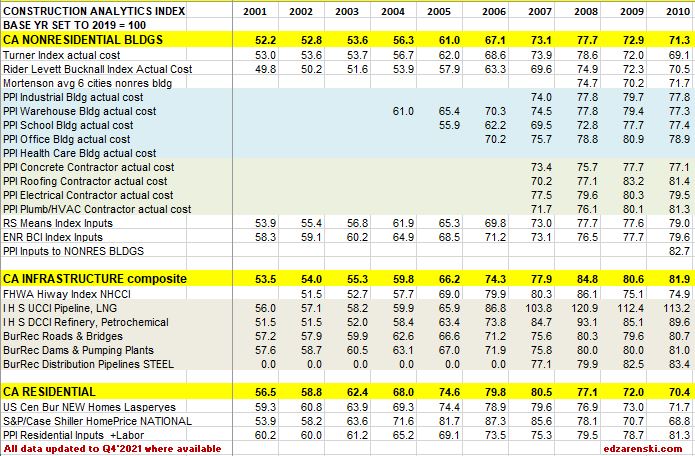

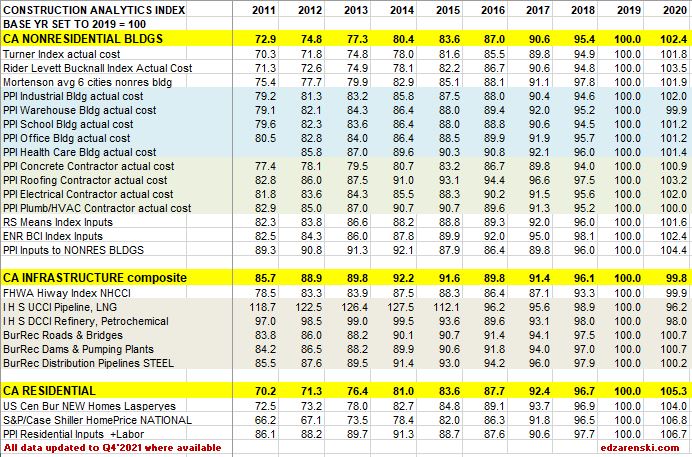

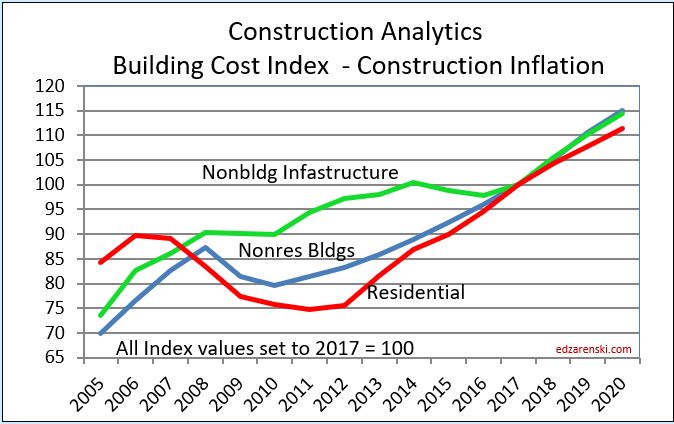

Residential, Nonresidential Buildings and Non-building Infrastructure Indices developed by Construction Analytics, (in highlighted BOLD CAPS in the tables below), are sector specific selling price (final cost) composite indices. These three indices represent whole building final cost and are plotted in Building Cost Index – Construction Inflation, see below, and also plotted in the attached Midyear report link. They represent average or weighted average of what is considered the most representative cost indicators in each major building sector. For Non-building Infrastructure, however, in most instances it is better to use a specific index to the type of work.

The following plots of Construction Analytics Building Cost Index are all the same data. Different time spans are presented for ease of use.

See the article Construction Inflation 2022

All actual index values have been recorded from the source and then converted to current year 2017 = 100. That puts all the indices on the same baseline and measures everything to a recent point in time, Midyear 2017.

All forward forecast values wherever not available are estimated and added by me.

Not all indices cover all years. For instance the PPI nonresidential buildings indices only go back to years 2004-2007, the years in which they were created. In most cases data is updated to include June 2019.

- June 2017 data had significant changes in both PPI data and I H S data.

- December 2017 data had dramatic changes in FHWA HiWay data.

SEE BELOW FOR TABLES

When construction is very actively growing, total construction costs typically increase more rapidly than the net cost of labor and materials. In active markets overhead and profit margins increase in response to increased demand. When construction activity is declining, construction cost increases slow or may even turn to negative, due to reductions in overhead and profit margins, even though labor and material costs may still be increasing.

Selling Price, by definition whole building actual final cost, tracks the final cost of construction, which includes, in addition to costs of labor and materials and sales/use taxes, general contractor and sub-contractor overhead and profit. Selling price indices should be used to adjust project costs over time.

quoted from that article,

R S Means Index and ENR Building Cost Index (BCI) are examples of input indices. They do not measure the output price of the final cost of buildings. They measure the input prices paid by subcontractors for a fixed market basket of labor and materials used in constructing the building. ENR does not differentiate residential from nonresidential, however the index includes a quantity of steel so leans much more towards nonresidential buildings. RS Means is specifically nonresidential buildings only. These indices do not represent final cost so won’t be as accurate as selling price indices. RSMeans Cost Index Page RS Means subscription service provides historical cost indices for about 200 US and 10 Canadian cities. RSMeans 1960-2018 CANADA Keep in mind, neither of these indices include markup for competitive conditions. FYI, the RS Means Building Construction Cost Manual is an excellent resource to compare cost of construction between any two of hundreds of cities using location indices.

Notice in this plot how index growth is much less for ENR and RSMeans than for all other selling price final cost indices.

8-10-19 note: this 2010-2020 plot has been revised to include 2018-2020 update.

Turner Actual Cost Index nonresidential buildings only, final cost of building

Rider Levett Bucknall Actual Cost Index published in the Quarterly Cost Reports found in RLB Publications for nonresidential buildings only, represents final cost of building, selling price. Report includes cost index for 12 US cities and cost $/SF for various building types in those cities. Boston, Chicago, Denver, Honolulu, Las Vegas, Los Angeles, New York, Phoenix, Portland, San Francisco, Seattle, Washington,DC. Also includes cost index for Calgary and Toronto. RLB also publishes cost information for select cities/countries around the world, accessed through RLB Publications.

Mortenson Cost Index is the estimated cost of a representative nonresidential building priced in seven major cities and average. Chicago, Milwaukee, Seattle, Phoenix, Denver, Portland and Minneapolis/St. Paul.

Beck Biannual Cost Report in 2017 and earlier cost reports developed indices for six major U.S. cities and Mexico, plus average. In the most recent Summer 2021 report, while Beck provides valuable information on cost ranges for 30 different types of projects, the former inflation index is absent. Beck has not published city index values since 2017. Read the report for the trend in building costs. See discussion for Atlanta, Austin, Charlotte, Dallas/Fort Worth, Denver, Tampa and Mexico

Bureau of Labor Statistics Producer Price Index only specific PPI building indices reflect final cost of building. PPI cost of materials is price at producer level. The PPIs that constitute Table 9 measure changes in net selling prices for materials and supplies typically sold to the construction sector. Specific Building PPI Indices are Final Demand or Selling Price indices.

PPI Materials and Supply Inputs to Construction Industries

PPI Nonresidential Building Construction Sector — Contractors

PPI Nonresidential Building Types

PPI Materials Inputs and Final Cost Graphic Plots and Tables in this blog updated 2-10-19

PPI BONS Other Nonresidential Structures includes water and sewer lines and structures; oil and gas pipelines; power and communication lines and structures; highway, street, and bridge construction; and airport runway, dam, dock, tunnel, and flood control construction.

RS MEANS Key material cost updates quarterly

National Highway Construction Cost Index (NHCCI) final cost index, specific to highway and road work only.

The Bureau of Reclamation Construction Cost Trends comprehensive indexes for about 30 different types of infrastructure work including dams, pipelines, transmission lines, tunnels, roads and bridges. 1984 to present.

IHS Power Plant Cost Indices specific infrastructure only, final cost indices

- IHS UCCI tracks construction of onshore, offshore, pipeline and LNG projects

- IHS DCCI tracks construction of refining and petrochemical construction projects

- IHS PCCI tracks construction of coal, gas, wind and nuclear power generation plants

S&P/Case-Shiller National Home Price Index history final cost as-sold index but includes sale of both new and existing homes, so is an indicator of price movement but should not be used solely to adjust cost of new residential construction

US Census Constant Quality (Laspeyres) Price Index SF Houses Under Construction final cost index, this index adjusts to hold the build component quality and size of a new home constant from year to year to give a more accurate comparison of real residential construction cost inflation

TBDconsultants San Francisco Bay Area total bid index (final cost).

Other Indices not included here:

CoreLogic Home Price Index HPI for single-family detached or attached homes monthly 1976-2019. This is a new home and existing home sales price index.

Consumer Price Index (CPI) issued by U.S. Gov. Bureau of Labor Statistics. Monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. This index in not related at all to construction and should not be used to adjust construction pricing.

Jones Lang LaSalle Construction Outlook Report National Construction Cost Index is the Engineering News Record Building Cost Index (ENRBCI), a previously discussed inputs index. The report provides some useful commentary.

Sierra West Construction Cost Index is identified as a selling price index with input from 16-20 U.S. cities, however it states, “The Sierra West CCCI plays a major role in planning future construction projects throughout California.” This index may be a composite of several sectors. The link provided points to the description of the index, but not the index itself. No online source of the index could be found, but it is published in Engineering News Record magazine in the quarterly cost report update.

Leland Saylor Cost Index Clear definition of this index could not be found, however detailed input appears to represent buildings and does reference subcontractor pricing. But it could not be determined if this is a selling price index. A review of website info indicates almost all the work is performed in California, so this index may be regional to that area. Updated Index Page

DGS California Construction Cost Index CCCI The California Department of General Services CCCI is developed directly from ENR BCI. The index is the average of the ENR BCI for Los Angeles and San Francisco, so serves neither region accurately. Based on a narrow market basket of goods and limited labor used in construction of nonresidential buildings, and based in part on national average pricing, it is an incomplete inputs index, not a final cost index.

Vermeulens Construction Cost Index can be found here. It is described as a bid price index, which is a selling price index, for Institutional/Commercial/Industrial projects. That would be a nonresidential buildings sector index. No data table is available, but a plot of the VCCI is available on the website. Some interpolation would be required to capture precise annual values from the plot. The site provides good information.

CALTRANS Highway Cost Index Trade bids for various components of work and materials, published by California Dept of Transportation including earthwork, paving and structural concrete. Includes Highway Index back to 1972, quarterly from 2012.

Colorado DOT Construction Cost Index 2002-2019 Trade bids for various components of work published by Colorado Dept of Transportation including earthwork, paving and structural concrete.

Washington State DOT Construction Cost Index CCI for individual components or materials of highway/bridge projects 1990-2016

Minnesota DOT Highway Construction Cost Index for individual components of highway/bridge projects 1987-2016

Iowa DOT Highway Cost Index for individual components of highway/bridge projects 1986-2019

New Hampshire DOT Highway Cost Index 2009-2019 materials price graphs and comparison to Federal Highway Index.

New York Building Congress New York City Construction Costs compared to other US and International cities

U S Army Civil Works Construction Cost Index CWCCIS individual indices for 20 public works type projects from 1980 to 2050. Also includes State indices from 2004-2019

Eurostat Statistics – Construction Cost Indices 2005-2017 for European Countries

Comparative International Cities Costs – This is a comparative cost index comparing the cost to build in 40 world-wide cities If this International Cities Costs is a parity index, which involves correcting for difference in currency, then you must know the parity city in each country, which in the US I think is Chicago.

OECD International Purchasing Power Parity Index

Turner And Townsend International Construction Markets 2016-2017

Turner And Townsend International Construction Markets 2018

Rider Levitt Bucknall Caribbean Report 2018

US Historical Construction Cost Indices 1800s to 1957

Click Here for Link to Construction Cost Inflation – Commentary

2-12-18 – Index update includes revisions to historic Infrastructure data

1-26-21 The tables below, from 2011 to 2020 and from 2015 thru 2023, updates 2020 data and provides 2021-2023 forecast.

NOTE, these tables are based on 2019=100. Nonresidential inflation, after hitting 5% in both 2018 and 2019, and after holding above 4% for the six years 2014-2019, is forecast to increase only 2.5% in 2020, but then 3.8% in 2021 and hold near that level the next few years. Forecast residential inflation for the next three years is level at 3.8%. It was only 3.6% for 2019 but averaged 5.5%/yr since 2013 and returned to 5.1% in 2020.

11-10-21 Follow the link at the bottom to 2021 Inflation

The Tables below 2001 to 2010 and 2011-2020 are updated to Q4 2021 with any revisions to past years posted on source websites.

The Table below 2015 to 2023 is updated to Q4 2021

How to use an index: Indexes are used to adjust costs over time for the affects of inflation. To move cost from some point in time to some other point in time, divide Index for year you want to move to by Index for year you want to move cost from. Example : What is cost inflation for a building with a midpoint in 2022, for a similar nonresidential building whose midpoint of construction was 2016? Divide Index for 2022 by index for 2016 = 110.4/87.0 = 1.27. Cost of building with midpoint in 2016 x 1.27 = cost of same building with midpoint in 2022. Costs should be moved from/to midpoint of construction. Indices posted here are at middle of year and can be interpolated between to get any other point in time.

All forward forecast values, whenever not available, are estimated by Construction Analytics.

2-13-23 Construction Inflation 2023

Construction Cost Inflation – Commentary 2019

1-28-20 See the new post Construction Inflation 2020

8-10-19 updated plots and commentary

General construction cost indices and Input price indices that don’t track whole building final cost do not capture the full cost of escalation in construction projects. To properly adjust the cost of construction over time you must use actual final cost or selling price indices.

Click Here for Link to a 20year Table of 25 Indices

Inflation in construction acts differently than consumer inflation. When there is more work available, inflation increases. When work is scarce, inflation declines. A very large part of the inflation is margins, wholesale, retail and contractor. When nonresidential construction was booming from 2004 through 2008, nonresidential final price inflation averaged almost 8%/year. This was at a time when input costs were averaging between 5% and 6%/year. When residential construction boomed from 2003 to 2005, inflation in that sector was 10%/year. But from 2009 through 2012 we experienced deflation, the worst year being 2009. Residential construction experienced a total of 17% deflation from 2007 through 2011. From 2008 to 2010, nonresidential buildings experienced 10% deflation in two years.

The following plots are all the same data. Different time spans are presented for ease of use.

8-10-19 note: this 2005-2020 plot has been revised to include 2018-2020 update.

Nonresidential Buildings – Since 1993, the 25-year long-term annual construction inflation has averaged 3.5%, even when including the recessionary period 2007-2011. Long-term average inflation, without recessionary declines, is 4% for 20 non-recessionary years since 1993. During rapid growth period of 5 years from 2004-2008, inflation averaged 8% per year. Since 2011, nonresidential buildings inflation has averaged 3.8%, averaging 4.25%/yr. for the last 4 years with a high of 5.1% in 2018.

Residential, from 2007- 2011 experienced 5 consecutive years of deflation, down 20%. In the 4-year boom just prior to that, 2003-2006, inflation averaged 9% per year. Residential inflation snapped back to 8.0% in 2013. It slowed to 4.4% in 2018 but has averaged over 5% for the last three years.

Construction Spending growth posted two separate 4-year periods of 40%+ growth, up 41% in 2012-2015 and up 40% in 2013-2016, exceeding the growth during the closest similar four-year periods 2003-2006 (+37%) and 1996-1999 (+36%), which were the two fastest growth periods on record with the highest rates of inflation and productivity loss. Growth peaked at +11%/year in 2014 and 2015, exceeded only slightly by 2004-2005.

Spending growth slowed to 7.0% in 2016 and only 4.5% in 2017. In 2018, spending dropped to a gain of only 3.3%. It’s expected, after revisions that 2019 spending will finish at a gain of less than 2%.

Producer Price Index (PPI) Material Inputs (excluding labor) costs to new construction increased +4% in 2018 after a downward trend from +5% in 2011 led to decreased cost of -3% in 2015, the only negative cost for inputs in the past 20 years. Input costs to nonresidential structures in 2017+2018 average +4.2%, the highest in seven years. Infrastructure cost are up near 5% and single-family residential inputs are up 4%. But material inputs accounts for only a portion of the final cost of constructed buildings.

Labor input is currently experiencing cost increases. When there is a shortage of labor, contractors may pay a premium to keep their workers. All of that premium may not be picked up in wage reports. Also, some of the labor inflation is due to lost productivity due to less skilled workforce. Unemployment in construction is the lowest on record. There is some sign of jobs growth slowing down in Q2 and Q3 2019, and potentially getting slower.

Nationally tracked indices for residential, nonresidential buildings and non-building infrastructure vary to a large degree. When the need arises, it becomes necessary that contractors reference appropriate sector indices to adjust for whole building costs.

Click Here for Link to a Table of 25 Index Values

ENRBCI and RSMeans input indices are prefect examples of commonly used indices that DO NOT represent whole building costs, yet are widely used to adjust project costs. An estimator can get into trouble adjusting project costs if not using appropriate indices. The two input indices for nonresidential buildings did not decline during the 2008-2010 recession. All other final cost indices dropped 6% to 10%.

From 2010 to 2019, total final price inflation is 110/80 = 1.38 = +38%. Input cost indices total only 106/85 = 1.25 = +25%, missing a big portion of the cost growth over time.

CPI, the Consumer Price Index, tracks changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. This index in not related at all to construction and should never be used to adjust construction pricing. Historically, Construction Inflation is about double the CPI. However for the last 5 years it averages 3x the CPI.

Taking into account the current (Jan 2018 12 mo) CPI of 2% and the most recent 5 years ratio, along with accelerated cost increases in labor and material inputs and the high level of activity in markets, I would consider the following forecasts for 2018 inflation as minimums with potential to see higher rates than forecast.

Residential construction, from 2007- 2011, experienced five consecutive years of deflation, down 20%. In the 4-year boom just prior to that, 2003-2006, inflation averaged +9% per year. Residential construction inflation saw a slowdown to only +3.5% in 2015. However, the average inflation for five years from 2013 to 2017 is 6%. It peaked at 8% in 2013. It climbed back over 5% for 2016 and reached 5.8% in 2017. For 2018, residential final cost inflation indexes are up only 4.5%. Residential construction inflation for 2019 is now about 4% to 4.5%.

A word about Hi-Rise Residential. About 95% of the cost of a hi-rise residential building would remain the same whether the building was for residential or nonresidential use. This type of construction is totally dis-similar to low-rise residential, which in large part is stick-built single family homes. Therefore, a more appropriate index to use for hi-rise residential construction is the nonresidential buildings cost index.

Nonresidential Buildings inflation, during the rapid growth period of five years from 2004-2008, averaged 8% per year. Inflation averaged near 4% per year for the 4 years 2014-2017.

Several Nonresidential Buildings Final Cost Indices averaged over 5% per year for the last 2 years and over 4% per year for the last 5 years. Nonresidential buildings inflation totaled 22% in the last five years. Input indices that do not track whole building cost would indicate inflation for those four years at only 12%, much less than real final cost growth. For a $100 million project escalated over those four years, that’s a difference of $8 million, potentially underestimating cost.

Nonresidential buildings spending slowed from 2017 to 2019 but is now entering a phase in which it may reach the fastest rate of growth in three years, which historically leads to accelerated inflation. Construction inflation for nonresidential buildings for 2018 and 2019 was 5%/yr. For 2020 expect 4.25%, rather than the long term average of 3.5% to 4.0%.

Non-building infrastructure indices are so unique to the type of work that individual specific infrastructure indices must be used to adjust cost of work. The FHWA highway index increased 17% from 2010 to 2014, stayed flat from 2015-2017, then increased 6%+ in 2018. The Highway index for 2019 is up about 6%. The IHS Pipeline and LNG indices increased in 2018 but are still down 20% since 2014. Coal, gas, and wind power generation indices have gone up only 6% in seven years. Refineries and petrochemical facilities have dropped 5% in 4 years but 2018 regained the level of 2013. Input costs to infrastructure are down slightly from the post recession highs, but most have increased in the last year. Input cost to Highways are up 5.0% and to the Power sector are up 3.6% in 2018. Work in Transportation and Pipeline projects has increased dramatically in 2017 and 2018.

Infrastructure power indices registered 2.5% to 3.5% gains in 2017 and again in 2018. Highway indices increased 6.6% in 2018. Anticipate 4% inflation for Power sector and at least 5%-6% inflation for Highway in 2019 with the potential to go higher in rapidly expanding markets, such as pipeline or highway.

This plot for nonresidential buildings only shows bars representing the predicted range of inflation from various sources with the line showing the composite final cost inflation. Note that although 2015 and 2016 have a low end of predicted inflation of less than 1%, the actual inflation is following a pattern of growth above 4%. The low end of the predicted range is almost always established by input costs, while the upper end of the range and the actual cost are established by selling price indices.

8-10-19 note: this 2005-2020 plot has been revised to include 2018-2020 update.

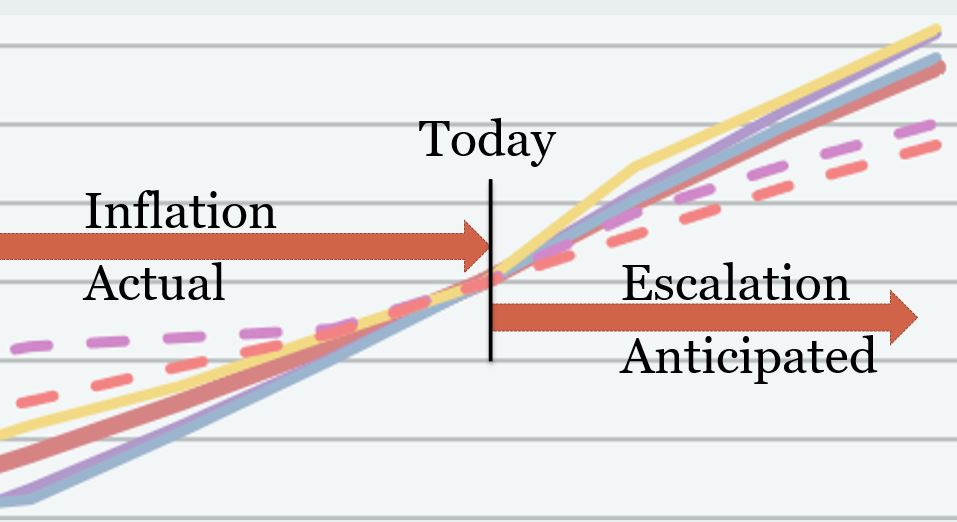

A word about terminology: Inflation vs Escalation. These two words, Inflation and Escalation, both refer to the change in cost over time. However escalation is the term most often used in a construction cost estimate to represent anticipated future change, while more often the record of past cost changes is referred to as inflation. Keep it simple in discussions. No need to argue over the terminology, although this graphic might represent how most owners and estimators reference these two terms.

In every estimate it is always important to carry the proper value for cost inflation. Whether adjusting the cost of a recently built project to predict what it might cost to build a similar project in the near future or adding an escalation factor to the summary of an estimate for a project with a midpoint 2 years out, or answering a client question, “What will it cost if I delay my project start by one year?”, whether you carry the proper value for escalation can make or break your estimate.

- Long term construction cost inflation is normally about double consumer price inflation (CPI).

- Since 1993 but taking out 2 worst years of recession (-8% to -10% total for 2009-2010), the 20-year average inflation is 4.2%.

- Average long term (30 years) construction cost inflation is 3.5% even with any/all recession years included.

- In times of rapid construction spending growth, construction inflation averages about 8%.

- Nonresidential buildings inflation has average 3.7% since the recession bottom in 2011. It averaged 4.6% for the 4 years 2016-2019.

- Residential buildings inflation reached a post recession high of 8.0% in 2013 but dropped to 3.5% in 2015. It averaged 4.6% for the 4 years 2016-2019, but is at the low point of 3.3% in 2019.

- Although inflation is affected by labor and material costs, a large part of the change in inflation is due to change in contractors/suppliers margins.

- When construction volume increases rapidly, margins increase rapidly.

- Construction inflation can be very different from one major sector to the other and can vary from one market to another. It can even vary considerably from one material to another.

Click Here for Link to a Table of 25 Index Values

Construction Inflation Cost Index

Note: The post you’ve reached here was originally written in Jan 2016. For the latest information follow this link to the newest data on Inflation. 8-15-19

ESCALATION / INFLATION INDICES

Thank You. edz

Jan. 31, 2016

Construction inflation for buildings in 2016-2017 is quite likely to advance stronger and more rapidly than some estimators and owners have planned.

Long term construction cost inflation is normally about double consumer price inflation. Construction inflation in rapid growth years is much higher than average long-term inflation. Since 1993, long-term annual construction inflation for buildings has been 3.5%/yr., even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8%/yr.

For the period 2013-2014-2015, nonresidential buildings cost indices averaged just over 4%/yr. and residential buildings cost indices average just over 6%/yr. I recommend those rates as a minimum for 2016-2017. Some locations may reach 6% to 8% inflation for nonresidential buildings but new work in other areas will remain soft holding down the overall average inflation. Budgeting should use a rate that considers how active work is in your area.

Infrastructure projects cost indices on average have declined 4% in the last three years. However, infrastructure indices are so unique that individual specific indices should be used to adjust cost of work. The FWHA highway index dropped 4% in 2013-2014 but increased 4% in 2015. The IHS power plant cost index gained 12% from 2011-2014 but then plummeted in 2015 to an eight year low. The PPI industrial structures index and the PPI other nonresidential structures index both have been relatively flat or declining for the last three years.

These infrastructure sector indices provide a good example for why a composite all-construction cost index should not be used to adjust costs of buildings. Both residential and infrastructure project indices often do not follow the same pattern as cost of nonresidential buildings.

Anticipate construction inflation of buildings during the next two years closer to the high end rapid growth rate rather than the long term average.