Home » Posts tagged 'markets'

Tag Archives: markets

Construction Spending June 2018

8-1-18

U. S. Census posted Construction Spending for June at a seasonally adjusted annual rate (SAAR) of $1,317 billion, down 1.1% from an upwardly revised May. Year-to-date, June spending is up 5.1% from 2017.

May was revised UP 1.7% from the 1st release posted 7-2-18. April was revised UP 0.8%.

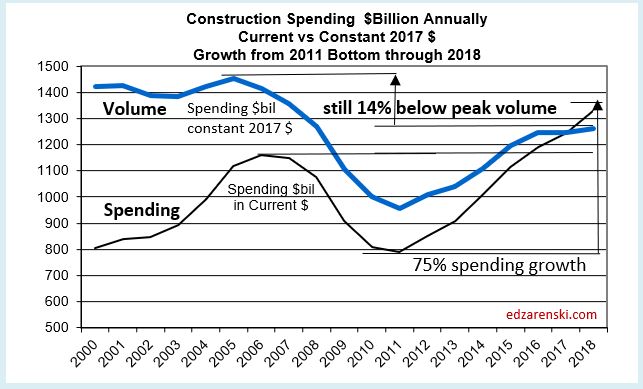

Construction Spending for the 1st half 2018, in Current $, averages $1,307 billion. This is an all-time high, well above the pre-recession high spending of $1,205 billion posted in the 1st quarter of 2006. Spending has been above the 2006 high since the 4th quarter 2016. Spending total is expected to average $1,330 billion for 2018.

Constant $ shows volume reached peak during the 2nd half 2005 and 1st half 2006, with 2005 posting the peak year. 2018 constant $ inflation adjusted spending is still 14% below the 2005-2006 peak.

Total spending year to date through June is $620 billion. Historically, only 47% of annual spending occurs in the 1st 6 months. Jan, Feb and Mar are the weakest months of the year, while Jul, Aug and Sep are the strongest spending months. Therefore, this indicates a 2018 total annual spending of $1,328 billion. This agrees very close to my total 2018 spending forecast.

The headline from the St Louis Fed > Total construction spending fell 1.1% in June, the largest monthly drop in more than a year. Just remember, spending subsequently gets revised 3x and final vs 1st release has been revised UP 79 times in the last 84 months.

Top performing construction spending markets 2018 year-to-date through June are Transportation +14.3%, Public Safety +12.1%, Lodging +10.7%, Water Supply +9.7%, Sewage and Waste Disposal +9.2%, Residential +8.1% and Office 6.8%.

The only markets down year-to-date are Religious -9.1%, Manufacturing -8.7% and Power -0.4%. Religious building as a percent of total is so small (1/4 of 1%) it has negligible effect on total annual performance. However, Manufacturing and Power make up about 15% of total construction.

Residential, Office, Commercial/Retail, Lodging, Highway and Environmental Public Works (Sewage, Water, Conservation) are all ahead of expectations for the 1st half of 2018.

June construction spending data shows an unusual $9 billion (SAAR) monthly decline (-9.3%) in Educational spending. This is several billion greater than the largest decline reported during the recession, so this looks like an anomaly in the data. There has never been a monthly decline like this in the Educational market since I’ve been tracking data, back to 2001. It is double the largest non-recession decline. I expect it will be revised up substantially at some point in the future.

Transportation is another market that appears to be unusually low for June. Because the monthly variance is not wildly out of balance it passes in obscurity. But here’s what we should see. Transportation (terminals and rail) new starts in 2016 increased 34% and then in 2017 increased 120%. Most of those projects will be completed in 3 years or less, but a number of the huge projects (no less than 15 projects ranging from $1 billion to $4 billion each) have a duration of 4 to 8 years. Even with long duration cash flow spreading out the spending for all those big projects, my analysis still predicts Transportation spending up 30% in 2018. Year-to-date through June, Transportation spending is up only 14%. I’ve forecast it should be up 18%. That’s a total shortfall of about $1 billion (SAAR ~$12 billion), or about 7%/month, for 3 months. April, May and June spending are all below expectations. I expect future revisions will increase current values. Also, we will see a big jump in year-to-date over the next three months since we are currently at an SAAR above $50 billion (and increasing) and Jul-Aug-Sep were the three lowest months in 2017, below $43 billion. Also, 2017 values were revised up 4%/month after the close of the year.

Manufacturing spending as of June is reported down 8.7% year-to-date from 2017. That decline will slowly turn positive in the second half of the year to finish up 2%. Spending is currently at an SAAR above $65 billion and expected to increase through December. In 2017, spending started the year above $70 billion but decreased to $60 billion by year end. Increasing values in the 2nd half 2018 compared to decreasing values in 2017 will continually increase the year-to-date performance in the 2nd half of 2018.

Power, similar to manufacturing, posted the highest spending for 2017 early in the year, then declined. In 2018, the 1st half posted the lowest spending, so the year-to-date is currently low. Increased spending in the 2nd half 2018, compared to the lowest values of the year in 2017, will boost year-to-date spending every month through year end. Although year-to-date spending through June is down 0.4%, the total for the year could finish up 9%.

Manufacturing and Power highlight one of the biggest shortfalls of judging expected performance based on year-to-date change. It is important to look at the trend line expected in the current year versus the trend line in the previous year. If they diverge, then year-to-date change will not give a clear indication of expected performance in the current year.

Total spending has increased from an average of $1,254 billion in Q4’17 to $1,292 billion in Q1’18 to $1,321 billion in Q2’18, growth of 3.0% and 2.25% the last two quarters. I’m expecting the rate of monthly spending will be above $1,360 billion by year end. The total spending forecast for 2018 is $1,330 billion.

Residential single family spending is up 9% YTD. Multifamily is down ~1%. Total residential spending is forecast to reach $566 billion in 2018, growth of 6.4% over 2017.

Nonresidential Buildings spending YTD totals $207 billion, up only 1.9% from 2017. It is being held down by Manufacturing which is currently down 8.7% from 2017. Also, the anomaly in Educational spending, explained above, contributes to the current low performance. 2018 forecast is $445 billion, 6.2% growth over 2017, with best growth in Lodging 13%, Office 11% and Amusement/Recreation 9%.

Non-building Infrastructure will post the best year of growth since 2014 to reach a new all-time high at $319 billion. Transportation, by far, will show the best growth, nearly 30% above 2017.

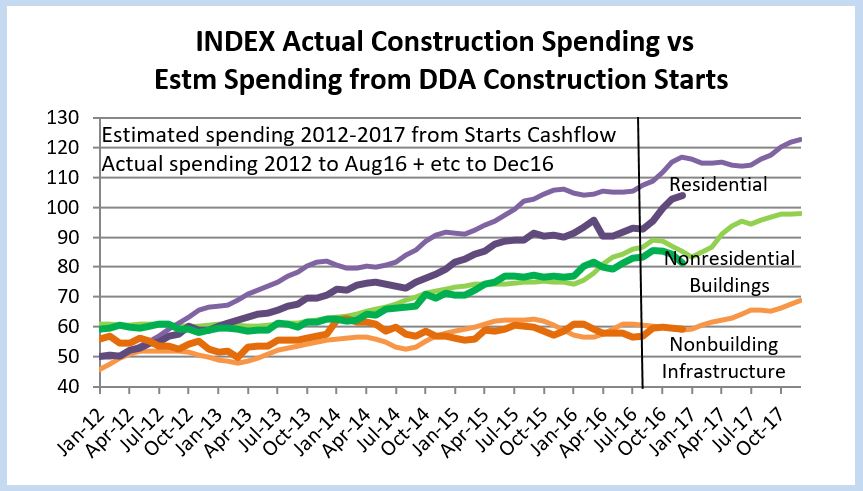

June Construction Starts Reach New Highs 7-25-18

In Which Category is That Construction Cost?

Seldom do two sources present information the same way!

In the construction industry, a disconnect exists in the reporting of construction starts data and actual spending data. Problems may arise when data is used to perform comparisons or forecasts between starts and spending. New starts and backlog may be listed in one category and spending for the same markets may be listed in another.

Almost universally, reporting of actual construction spending data follows the U.S. Census Put-in-Place Spending format. I adjust all other construction starts input/forecasting data that I use to conform to these Census Construction Spending Put-in-Place definitions. Here are some pitfalls to be aware of:

The U.S. Census Construction Put-in-Place (Construction Spending) Release follows these definitions.

Residential spending $ includes about 35% renovations and improvements that has no units associated with the dollars, so that portion of $ should not be included in a comparison to housing starts.

In census spending, MF dormitories is in educational and all types of MF healthcare related homes are in healthcare.

Demolition is not included in renovations/improvements. Partial repair of flood damaged homes is NOT included in residential improvements. Full replacement of flood damaged homes is included as improvements, not new single family. Here is the US Census definition of flood repairs

Offices includes pubic buildings such as city halls and courthouses. Includes data centers and bank buildings. Excludes medical office buildings, offices at manufacturing sites and offices at educational or healthcare facilities. Excludes Public Safety.

Commercial includes all retail buildings, warehouses, parking lots and garages. Excludes parking at educational/healthcare facilities.

Census DOES separate the costs for buildings that are mixed use retail/office/residential.

Educational, along with K-12, includes administrative offices, health centers, parking, residence halls, classrooms, educational research labs, food service and sports/recreation facilities at schools or colleges and universities and all associated infrastructure and maintenance facilities at the educational site. Also includes public libraries, science centers and museums.

Healthcare includes similar support and infrastructure to educational. Also includes medical office buildings, non-manufacturing and non-educational research labs.

Amusement and Recreation includes performing arts centers, civic centers, convention centers, sports and recreation facilities not located at schools or colleges.

Transportation includes air freight and passenger air terminals, runways, bus and railroad passenger terminals, light rail and subway facilities, railroad track, railway structures and bridges, docks and marine terminals and maintenance facilities and infrastructure associated with each.

Some sources of design or new construction starts data carry terminal buildings as commercial buildings, institutional buildings or other public nonresidential buildings. Census caries the building cost of all terminals grouped in with the non-building infrastructure costs of Transportation. Some sources carry public buildings such as city halls and courthouses as Public Safety but Census carries cost data for public buildings such as city halls and courthouses in Offices. Some sources classify laboratories as commercial and warehouses as industrial/manufacturing but Census includes warehouses in Commercial and Labs, depending on use, can be either Educational, Healthcare or Manufacturing.

Dodge Data New Construction Starts

Dodge includes monthly New Construction Starts for Terminals and Courthouses in Other Institutional Buildings, a Nonresidential Buildings category. The Census actual spending report includes Terminals in Transportation and Courthouses in Offices.

Although all of these still remain in Non-building Infrastructure, Dodge includes Rail, Mass Transit, Airport Runway and Pipelines in Other Public Works. Although not often mentioned by Dodge, it is assumed Communications is also included in Other Public Works. Census includes all mass transit in Transportation, Communications is listed separately and pipelines are included in Power.

Dodge does not identify Renovations in their residential starts data. Census reports SF and MF spending and Total Residential spending with the difference between Total and SF+MF being Renovations. Multifamily spending accounts for less than 15% of all residential actual spending. Dodge MF starts account for 30% of all residential starts dollars. Furthermore, Dodge totals for MF starts $ for the last 7 years exceed the actual total of MF spending for the year by 30% to 50%. Dodge MF data represents more than just MF starts. Which may mean it includes renovations starts. It might also include student housing.

Constructconnect (CC) Construction Starts Forecast

New starts for Transportation Terminals is in a line by the same name but subtotaled in Commercial (Nonresidential Buildings) starts. Census includes Terminals in Transportation.

CC lists Courthouse starts subtotaled in Institutional. Census carries Courthouses in Office (Commercial).

CC lists Military as a line item subtotaled in Institutional. This might include Office, Housing, Warehouse, etc., which would be carried by Census in Office, Residential, Commercial, etc., respectively.

CC lists Laboratories (Schools & Industrial) together and subtotals all labs in Commercial. Census separates labs by commercial, research and educational and carries spending in Manufacturing, Healthcare or Educational respectively which would subtotal spending in Manufacturing (industrial), or Institutional (Healthcare and Educational).

CC does not list rail or transportation separately, but does list Airport and Misc Civil (Power,etc.). This leads me to think rail is included in the line item with Misc Civil (Power, etc.). Also, CC does not list Communication, which I suspect is included in Misc Civil (Power, etc.) Already noted above is that Terminals is subtotaled in Commercial. Census carries rail, runway and terminals in Transportation and keeps Communication and Power separate from others.

CC provides an alternate table of new starts data that corresponds to a proprietary software, INSIGHT. This table of starts data reshuffles categories very far from anything that would resemble Census spending output.

The AIA publishes a twice annual Consensus Construction Forecast, comparing forecast of Nonresidential Buildings spending using inputs from seven or eight firms. Every firm but one follows a similar organization. The difference is FMI includes both Transportation and Communications in Commercial Nonresidential Buildings. I’m not aware of another other firm that reports these two categories of spending as Nonresidential Buildings. Both are typically carried as Non-building Infrastructure. That these categories include costs for projects such as rail beds, rail right-of-way civil structures, loading platforms, airfield runways and support structures, communication transmission lines and cell towers supports the more standardized inclusion of these items in Infrastructure.

Similar discrepancies may exist when comparing starts or spending to indexes, such as the AIA Architectural Billings Index, which broadly classifies projects as commercial, institutional or residential. Some resources classify Amusement/Recreation as institutional and some as commercial. In particular, the shifting of costs between Nonresidential Buildings and Non-building Infrastructure creates a particularly meaningful disparity between spending forecasts.

As you can see, there are numerous instances where the data are often mixed up. From the point of view of the forecaster, initial input data cannot always be used directly to forecast or match spending output. Some manipulation of the data may be required to make input and output match.

As an example, I move the Dodge data starts for Terminals from nonresidential buildings to non-building infrastructure Transportation, so that really changes my totals from theirs for Nonresidential Buildings to Non-building Infrastructure. My spending output conforms with most all others, most of whom also follow the Census PIP definitions.

What does your source for data take into consideration? Know your data!

BTH – 20 Snips From Recent Articles

2-17-17 Behind The Headlines

- From the Jan 2011 bottom of the recession in construction to current, both net jobs (jobs x hours worked) and volume (spending after adjusted for inflation) have increased equally by 28%.

- Growth of only 100,00 to 140,000 new jobs in 2017 would be the slowest growth in 5 years and will look like a hiring slowdown. Some might attribute it to lack of available workers. In large part it may be due to a balancing of workforce to real volume growth.

- Staffing patterns (appear to) lag changes in work volume.

- These six Nonresidential Buildings markets, which make up 80% of all nonresidential buildings spending, posted the following growth in starts leading into 2017: Office +37%, Lodging +40%, Educational +11%, Healthcare +21%, Commercial Retail +11% and Amusement/Recreation +21%

- Nonresidential buildings 2017 starting backlog is 45% higher than at the start of 2014, the beginning of the current nonres bldgs growth cycle.

- Office construction starting backlog for 2017 (projects under contract as of Jan 1, 2017) is the highest in at least 8 years, more than double at the start of 2014 when the current growth cycle of office construction spending began.

- For 2017, the amount of construction spending (on manufacturing buildings) from starting backlog has dropped 25% from the level of 2016. Even an increase of 50% in new 2017 starts would not make up for that loss.

- More infrastructure projects started construction in the 1st 6mo of 2015 than any time in history. This will boost infrastructure spending through 2017.

- As measured in comparable constant dollars, No, we are not back to previous levels of spending. We will probably not return to previous highs before 2020.

- The entire construction industry best growth rate ever achieved (in 2016 constant$) absorbed $1 trillion in new spending over 5 years. Infrastructure has not absorbed $1 trillion newly added work in 25 years.

- long term best average rates of growth (indicate) we could increase infrastructure spending through new stimulus between $7 billion to $10 billion a year

- Construction spending, from 1st release to last revision of data, has been revised upward every month since August 2013. That would indicate the first reports of an “unexpected decline” almost always get revised up in following months.

- In the last 36 months, there were 16 Census construction spending releases that initially showed a decline vs the previous month. Five months showed a decline vs the previous year. After revisions every month was revised up from the original posted amount. There remained only 2 significant mo/mo declines. There were no remaining year/year declines.

- Current year YTD “not-yet-revised” values for new construction starts are always compared to the previous year YTD “revised values” which has the affect of making current year growth appear lower than it should. In the last 10 years the YTD revisions to previous year values have never been down.

- Residential starts in 2016 posted the best year since 2005-2006. Residential starts bottomed in 2009 and have now posted the 7th consecutive year of growth.

- Total construction spending in 2017 will reach $1,236 billion supported by a 4th consecutive year of strong growth in nonresidential buildings.

- Office construction reached a new all-time high in September 2016. Spending will be in the range of +20% to +30% year over year growth for 2017 with total coming in at $91 billion.

- It’s real damn hard to add $100 billion in new construction volume in a year. After adjusting for inflation, construction volume has never increased by $100 billion. It has increased by $75 billion 4 times and 3 more times by $50 billion.

- If you want to avoid misusing a cost index, understand what it measures.

- Selling Price, by definition whole building actual final cost, tracks the final cost of construction. Selling price indices should be used to (adjust costs for inflation so you can) compare costs over time.

Office Buildings Lead 2017 Construction Spending

New construction starts in 2016 for Office Buildings is setting up a very strong spending growth pattern for the next 2 years.

The five largest metropolitan areas comprise more than one third of total national new starts in commercial-multifamily construction. Total commercial-multifamily starts are up 7%. Commercial starts alone are up 11%. New starts for office projects increased more than 30% in 2016. The following percentages are growth in starts for new Office Buildings. Reference Dodge Data & Analytics New Commercial and Multifamily Construction Starts.

- New York City-Northern NJ-Long Island -2%, but from 2015 that was up 138%

- Los Angeles-Long Beach-Santa Ana +67%

- Chicago-Naperville-Jolliet +22%

- Washington DC-Arlington-Alexandria +87%

- Dallas-Fort Worth-Arlington +31%

Office construction starting backlog for 2017 (projects under contract as of Jan 1, 2017) is the highest in at least 8 years, more than double at the start of 2014 when the current growth cycle of office construction spending began. Also, the share of spending in 2017 from starting backlog is increasing.

Office spending since 2013 has increased every year by an average of more than 20%/year and is expected to continue or exceed that rate of growth in 2017.

Office construction spending reached a new all-time high in September 2016. Growth in office buildings will lead all 2017 commercial construction spending. Spending will be near +30% year over year growth for 2017 with total expected to come in at $91 billion.

Regardless what market fundamentals change for 2017, this work is already under contract and will be the driving force for 2017 nonresidential buildings spending.

See Also these related articles

Nonresidential Bldgs 2017 Forecasts Vary

Nonresidential Bldgs Construction Spending 2017

Behind The Headlines – Construction Backlog

Nonresidential Bldgs Construction Spending 2017

1-4-17

This is a first pass at 2017 spending. It will be update in February when December starts and spending become available.

2-1-17 updated to include December data

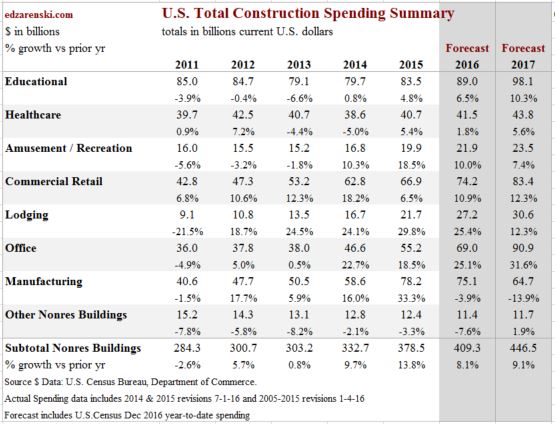

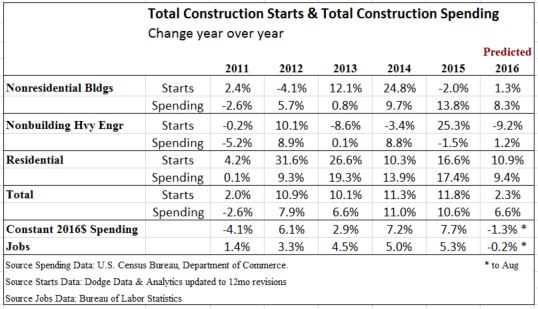

Nonresidential Buildings spending for 2016 totaled $409 billion, UP 8.1% from 2015. Spending posted increases of 9.7% in 2014 and 13.8% in 2015.

Nonresidential Buildings spending in 2017 will increase to $447 billion, 9.1% over 2016. The most recent 3-month average seasonally adjusted annual rate (SAAR) is $420 billion, only 5.5% below the peak in 2008. By midyear 2017 the SAAR will reach a new all-time high. Office, Commercial, Lodging and Educational markets are all expected to post strong results over 10% growth in 2017.

Office building new starts through August were up only 6% year-to-date but starts in September as tracked by Dodge Data & Analytics reached the highest in years. 2016 starts finished at +37% providing the highest amount of work in backlog going back at least 8 years. Lodging starts in 2016 finished up nearly 40%, Healthcare up 20% and Amusement/Recreation up 35%.

Manufacturing – spending will finish down this year, $75 billion vs $78 billion in 2015, but both years are more than 30% higher than the next closest years, 2014 and 2009. Rather than labeling 2016 a down year, 2015-2016 should be described as an extended period of extremely strong spending. 2017 spending will drop the most since pre-recession to $65 billion but will still remain well above 2014. In 2005-2006, manufacturing was less than 10% of total spending in the nonresidential buildings sector. In 2015 it reached 21%. Today it is 18%. Manufacturing in some reports is referred to as Industrial.

Office – spending dropped more than 40% from $65 billion/year in 2007-2008 to $37 billion from 2010 to 2013. Since then it has increased every year by an average of more than 20%/year and is expected to continue that level of growth in 2017. New starts for office projects increased more than 30% in 2016. Office construction 2017 starting backlog (projects under contract as of Jan 1, 2017) is the highest in at least 8 years, more than double at the start of 2014 when the current growth cycle of office construction spending began. More importantly, the ratio of spending from starting backlog is also increasing for 2017. This is setting up a very strong spending growth pattern for the next 2 years. Office construction reached a new all-time high in September 2016. Spending will be in the range of +20% to +30% year over year growth for 2017 with total coming in at $91 billion. Office was more than 16% of total sector spending in 2006 through 2008 before dropping to 13% in the recession. Now at over 17%, it has been growing steadily for the last few years. In 2017 it will be 19% of total sector spending. Offices includes data centers.

Commercial/Retail – this market dropped from $90 billion in 2007 to $40 billion in 2010. It has been growing steadily since reaching bottom in early 2011, but has only recovered to an annual total rate of $78 billion. New starts in 2016 increased moderately. For 2017 spending remains in a tight range between $82 and $84 billion, with total 2017 growth coming in at just over +12%.

Lodging – this market recorded the largest drop of any, falling 75% from $36 billion in 2008 to $9 billion in 2011. However it recorded the strongest rebound of any market climbing 19% to 30% per year for the last 5 years. New starts in 2016 increased almost 40% setting up increased spending from starting backlog in 2017. In 2017, lodging will grow by 12% with a spending total of just over $30 billion. Lodging is still 2 years away from reaching previous highs. Lodging dropped to only 3% of total sector spending in 2011 but has rebounded to 7% in 2016.

Educational – previous highs of over $100 billion in both 2007 and 2008 are perhaps two years away. However, the rate of growth has been increasing slowly since 2014 from 1% to 4.8% to 6.5% annually. New starts have increased every year since 2012. Expect 2017 educational spending to increase by more than 10% to $98 billion. At peak, educational represented 30% of all nonresidential buildings spending. Now it’s only 22%.

Healthcare – this market has been very slow to recover, experiencing declines as recently as 2013 and 2014, hitting an 8 year low in 2014, when all other nonresidential building markets had already returned to growth. 2015 was a moderate growth year, up 5%, but 2016 increased less than 2%. Starts are indicating 5.6% growth to $44 billion for Healthcare spending in 2017. Healthcare has dropped from 14% to only 10% of all nonresidential buildings spending.

Amusement/Recreation – this market hit an 8 year low in 2013 but we’ve had 3 years of excellent growth of 10%/yr or more. 2017 is expected to increase 7.4% over 2016 to a total of $23 billion. This market is only 5%of nonresidential buildings spending.

Religious and Public Safety represent less than 3% of total nonresidential building spending. The religious bldg market has been declining since 2002 and is down 55%. Public Safety peaked in 2009 and has declined every year since, now down 40%.

Starts Point to Robust 2017 Spending

10-20-16

Starts Point to Robust 2017 Spending

Construction Starts for September were released 10-18-16 from Dodge Data and Analytics. Here’s some of the major points that can be developed from the data:

The six Nonresidential Buildings markets, Office (+30% YTD), Lodging (+50%), Educational (+10%), Healthcare (+20%), Commercial Retail (+15%) and Amusement/Recreation (+15%) make up 80% of all nonresidential buildings spending and account for combined growth of 16.5% in YTD new starts. Office and Lodging in 2016 will reach the 5th consecutive annual increase. Educational Markets, Commercial Retail and Amusement/Recreation will each record the 4th consecutive annual increase in total value of new starts. Spending combined for these six markets peaked in 2008 and dropped 37% to a bottom in 2012. For the last 3 years spending growth has ranged between 9%/yr and 12%/yr. For 2017, expect spending growth of 8%.

Manufacturing makes up 18% of nonresidential building market share. New starts 2016 YTD are down 54% from 2015. However, in 2014 and 2015 this market posted the fastest growth of any market in a decade and posted the two highest years on record for this market. It is currently settling back to a normal growth range. In 2014 starts increased 90%. In 2015 spending increased 33% to the highest ever recorded for manufacturing buildings. Spending will be down 2% to 3% in 2016 and down another 13% more in 2017, but 2017 will still be the 3rd highest year of spending on record.

Non-building Infrastructure starts will be down nearly 10% in 2016 but were up 25% in 2015. Power and Highway/Bridge/Street make up 2/3rds of non-building infrastructure spending. In 2015, Power starts increased 150% to an all-time high and Highway/Bridge/Street finished just shy of a 6-year high. It is not unexpected that starts in these markets will be down for 2016. The volume of monthly spending from projects started in 2014 and 2015 in this sector will contribute to spending for several years to come. Spending in 2017 will be the highest ever in this sector, up 7% from 2016.

Residential starts are having the best year since 2005-2006. Residential starts bottomed in 2009 and are now in the 7th consecutive year of growth. Although new starts will increase only about 7%-8% for 2016, that follows 4 years of growth averaging more than 20%/year. Spending peaked in 2005-2006 and dropped 60% to a low in 2009-2010. Spending has bounced 90% off the bottom in large part due to 17%/year average growth in 2013-2014-2015. Both starts and spending slowed in 2016 but still expect 7% to 8% spending growth in both 2016 and 2017.

Starts are recorded in full in the month a project starts but the total project budget gets spent over a long duration, so the effects on spending are spread over the next 2 to 3 years. Total starts are Up 10%/yr to 12%/yr for the last 4 years. The current forecast for 2016 is growth of only 3.5%, but that now leads us to a very important factor that must be considered when using starts data to predict future spending.

There is a major factor that keeps new starts in the current year from appearing as good as they should. Dodge Data continually revises starts. In every monthly release, the previous month is revised AND the last year’s year-to-date is revised. Dodge does incorporate other (usually minor) revisions at a later date, but the “12 month” revision to the previous year-to-date values captures a large part of all revisions.

So this September report includes revisions to the total 2015 YTD values through September 2015. None of the 2016 values yet include that equivalent “12 month” revision and won’t until next year. But the current year YTD not-yet-revised values are being compared to the previous year YTD revised values which has the affect of making current year growth appear lower than it should.

In the last 10 years the YTD revisions have never been down. Usually, most of the revisions occur to nonresidential buildings, about 5% to 6% per year, with only a 2% to 3% revision each to infrastructure and residential.

For total nonresidential buildings, so far year-to-date 2015 values through September have been revised UP by 9%. So while the 2016 year-to-date nonresidential buildings value this month is noted as down 2% compared to last year, much of the reason it is down is because 2015 values have had revisions applied that increase the 2015 base by 9%. We won’t get those equivalent “12 month” revisions applied to 2016 values until next year. When all the revisions are in, new starts for nonresidential buildings (typically revised up by 5% to 6%) in 2016 are on track to equal or exceed 2015 and perhaps record the third consecutive year of over $220 billion. We are within easy striking distance of the all-time high for nonresidential buildings starts reached in 2007!

For residential starts, if 2016 values get revised up next year by only 2%-3%, then 2016 will have grown by nearly 10% over 2015. Unless we experience a severe downward trend in new residential starts, which is NOT predicted, 2016 will post an all-time high for new residential starts.

(Year-to-date by market and month/month values by market are not published.)

See also this post on Construction Spending Sept 2016

Construction Spending 2016 – Midyear Nonresidential Markets

Construction Spending 2016 – Nonresidential Markets

9-8-16

Refer here to the Construction Spending 2016 Midyear Summary

Nonresidential Buildings

Nonresidential Buildings spending for July totaled a SAAR of $403 billion, down slightly from June but up 1.3% from the May dip. Spending YTD for nonresidential buildings through July is up 8.0% over 2015. The current 3-month average of $403 billion is up slightly from the 1st quarter but is still 9% below the peak in 2008.

How does actual spending YTD compare to my early 2016 forecast?

Nonresidential Bldgs predicted YTD $236.9b, actual YTD $228.1b (-$8.8bil, -3.7%).

Nonresidential Buildings spending for 2016 predicted in Dec 2015 $439.2b. Now with YTD data through July forecast spending for 2016 is $410.9b (-$28.3bil, -6.4%).

Total Nonresidential Buildings construction spending increased 9.7% in 2014 and 13.8% in 2015 and will grow 8.5% in 2016 and 6.3% in 2017.

Nonresidential Buildings Spending History

- 5 years 2004-2008 up 64%

- 3 years 2006-2008 up 45%

- 3 years 2009-2011 down 36%

- 2 years 2014-2015 up 25%

Manufacturing construction spending YTD is down 2.6% from 2015. However, that is because 2015 manufacturing construction spending reached all-time highs after record new starts in 2014, some of which will extend spending into 2017. 2016 is on track to reach the second highest year of spending on record, only slightly below 2015. Although new starts YTD in 2016 are down 75% from 2015, that will have most affect next year. A very large volume of starts in mid-2014 and early 2015 will generate spending extending into the 2nd half of 2016and early 2017. Total manufacturing construction spending for 2016 will finish 2% below 2015. Due to declining new starts in 2015 and 2016, spending in 2017 will drop more than 10%, and yet still be the 3rd highest year on record. Manufacturing construction represents 19% of total nonresidential buildings spending.

Office construction spending YTD is up 22% from 2015. Although new starts are currently down slightly from last year, starts are expected to grow 4% for 2016. Office starts have been strong since 2013. Vacancy rates peaked in 2010 and demand for office space has been increasing. A large component of office construction is data centers. Although we may see a few months of spending declines in late 2016, the large volumes of spending generated by several years of strong starts will keep total spending high. Office construction spending increased 23% in 2014 and 19% in 2015 and it will grow 23% in 2016 and 15% in 2017. Office construction represents 17% of total nonresidential buildings spending.

Commercial construction spending YTD is up 11% from 2015. Commercial new starts have been increasing slowly for the last 4 years. Spending will remain nearly flat for the next several months and is forecast to grow very slowly through mid-2017, then taper off slightly. Commercial construction had its biggest years in 2012-2013-2014 with growth of 11%, 12% and 18%. Total commercial construction spending for 2016 will finish 9% higher than 2015 and 2017 will grow 3% to 4%. Commercial construction represents 18% of total nonresidential buildings spending.

Lodging construction spending YTD is 29% higher than 2015. Lodging construction spending has exceeded the growth rate of all other markets. Starting in 2012 annual spending increased 19%, 25%, 24% and 30%. However, during that time lodging averaged only 5% of total nonresidential buildings spending. It now represents just under 7%. Total lodging construction spending forecast growth for 2016 is 25%. For 2017 expect spending growth of only 8%.

Educational construction spending YTD is up 4.8% from 2015. Educational buildings spending experienced the longest downturn of any market, declining for 5 consecutive years from 2009 through 2013. It has been slow to recover with 2015 showing the first real growth of only 4.8%. 2014 marked the beginning of the turn but registered growth of less than 1%. New starts posted 15% growth in 2014 and then slowed to only 4% growth in 2015. However, a large volume of those starts occurred in late 2014 and then again in early 2015. The timing of these starts generates a lot of spending in late 2016. I expect spending in the 2nd half 2016 to grow 5% over the 1st half. Total educational construction spending for 2016 will finish 8% higher than 2015 and 2017 will grow 9%. Educational construction spending is the largest component of nonresidential buildings representing 22% of total nonresidential buildings spending. Before the 5 years of declines it represented 30% of nonresidential buildings spending.

Healthcare construction spending YTD is up only 2.3% from 2015. Healthcare new starts since 2011 increased only in 2014. Spending may see some moderate declines in late 2016 before resuming slow growth in 2017. Changes and uncertainty in the healthcare climate are having a dampening effect on spending growth. Total healthcare construction spending for 2016 will finish only 2% higher than 2015 and 2017 will grow 3% to 4%. Healthcare construction represents 10% of total nonresidential buildings spending.

Amusement/Recreation construction spending YTD is up 10.1% from 2015. New starts were very strong in 2013 and 2014 and generated strong spending increases of 10% and 18% in 2014 and 2015. However, starts in 2015 declined slightly and 2016 starts to date have been flat. Spending through 2016 will remain strong but we will experience moderate declines in the 1st half of 2017. Total Amusement/Recreation construction spending for 2016 will finish 12% higher than 2015 but 2017 will grow only 2%. Amusement/Recreation construction represents 5% of total nonresidential buildings spending.

Non-building Infrastructure

Non-building Infrastructure spending for July fell to a SAAR of $289 billion, down slightly over for the last four months. YTD spending through July is up only 1.3% over 2015. Spending began to slow in April and May and is now at the 2016 low. The current 3-month average is down 4% from the 1st quarter. However, spending on non-building infrastructure reached an all-time high in the first half of 2014 and has remained near those highs through 2015 into the 1st quarter of 2016.

How does actual spending YTD compare to my early 2016 forecast?

Non-building Infrastr predicted YTD $156.2b, actual YTD $160.5b (+$4.3bil, +2.8%).

Non-building Infrastrusture spending for 2016 predicted in Dec 2015 $293.2b. As of July data forecast spending for 2016 is $297.3b (+$4.1bil, +1.4%).

Total Non-building Infrastructure construction spending increased 8.8% in 2014 but decreased 1.5% in 2015. It will grow only 1.2% in 2016 but then 9.6% in 2017.

Non-building Infrastructure Spending History

- 7 years 1995-2001 up 56%

- 4 years 2005-2008 up 60%

- 3 years 2009-2011 down 8%

- 3 years 2012-2014 up 19%

Power construction spending YTD is up 6.0% from 2015. Power new starts are erratic. Also some power projects are very long duration from start to finish. In 2012 starts totaled over $50 bil., in 2013 only $30 bil. and in 2014 less than $25 bil. In 2015 starts reached an all-time high of $56 bil. The power construction spending pattern for 2012-2015 was +30%, -4%, +18%, -16%. Many of the starts in 2012 supported 18% spending growth in 2014, yet not much of the record year of starts in 2015 supported spending in 2015. Although new starts in 2016 are forecast to drop by 30%, that’s still over $40 bil. and more than in 2013 or 2014. Part of the reason for a drop in spending in 2016 is the tailing off of projects that started in previous years combined with the fact that 2013 and 2014 were “lean” years. Cash flow of starts determines spending and it follows the erratic flow of starts. A very high volume of starts in early 2015 will generate spending extending out through 2019. I’m forecasting total power construction spending for 2016 will finish only 1.2% higher than 2015 and 2017 will increase 7%. Power construction represents 32% of total non-building infrastructure spending.

Highway/Bridge/Street construction spending YTD is up only 2.5% from 2015. Some highway and street projects are long duration from start to finish. Although new starts in 2015 increased by 11%, that was significantly unbalanced with two very high months of new starts in the 1st quarter and below average starts for almost the entire 2nd half of 2015 and the 1st half of 2016. The very high months have starts with much longer duration so do not add significantly to monthly spending, they spread the spending over a longer period of time. Spending has declined in 8 out of the last 12 months. I’m expecting declines in 6 out of the next 12 months. Yet the plus months will still carry both 2016 and 2017 to spending growth. I’m forecasting total highway/bridge/street construction spending for 2016 will finish 4.5% higher than 2015 and 2017 will increase 8%. Highway/Bridge/Street construction represents 32% of total non-building infrastructure spending.

Transportation/Air/Rail construction spending YTD is down 2.4% from 2015. YTD spending is 9% lower than what I had predicted in my early 2016 forecast. There is a disconnect between where Dodge reports transportation starts and how U S Census reports transportation spending, so it is difficult to directly relate the two. I’m forecasting total transportation construction spending for 2016 will finish 2.5% higher than 2015 and 2017 will increase 6%. Transportation construction represents 16% of total non-building infrastructure spending.

What Did He Say? Fact Checker – Track Record

MY TRACK RECORD

Indoor Masters National Track Championships

masters age group 45-50

Mile – 4:41.7 – 4th place

3000m – 9:25.3 – 3rd place

Oh, wait. That’s not what you are here to read. You want my track record on construction economic forecasts. How good are my forecasts? Do they prove to be accurate? How do they compare to the rest of the industry forecasts? OK. Let’s have a look.

- Bullets show what I forecast.

This is what actually occurred. Actual is in red if I got it wrong.

From Jan 2013

- The ABI, McGraw Hill Dodge new starts and the Dodge Momentum Index (DMI) are all indicating a dip in nonresidential spending potentially from February through May 2013.

- Architecture Billings Index (ABI) went UP from May 2012 to January 2013 with only December down slightly (see figure B). This is a very good leading indicator for new construction work starting in Q3-Q4 2013.

- I expect a dip in nonresidential buildings work between January and May 2013, at which point all indicators point to sustained growth through year end.

From February 2013 through June 2013 actual spending on nonresidential buildings dropped by 2%. Then from June through November spending increased by 6%.

From Jan 2013

- As spending continues to increase, contractors gain more ability to pass along costs and increase margins. However, contractors almost always are playing catch-up. In the most recent three-month period, contractors’ costs began to climb faster than whole building costs went up, due to both increasing material costs and declining productivity.

- Once growth in nonresidential picks up and both residential and nonresidential are active, we will begin to see apparent labor shortages and productivity losses.

For 2013 and 2014 construction spending increased 7% and 10%. During that 2 year period, total labor and materials inputs increased only 2% to 3%, but construction inflation measured 4.5%. Margins increases drove up the total inflation cost. Available (nonworking) workforce declined to about 400,000, near the lowest on record. Productivity declined by 2%.

From Jan 2013

- Construction Spending for 2013 will be pushed higher by huge growth in residential construction, a rate of spending growth that increased by 30% from Q1 to Q4 2012

Residential spending in 2013 grew at a rate of 1.5% per month, largest one year growth since 2004.

From Jan 2013

- The National Association of Home Builders consensus estimate for new residential units is growth of 23% in 2013 and 33% in 2014. 2012 grew by 28%.

- The NAHB projections are for an increase of 150,000 units in 2013 and 230,000 in 2014, 20% and 27% growth the next two years. There’s a possibility we could achieve that. But, especially in 2014, that would exceed the fastest growth rates, both volume and total jobs, achieved in the last 30 years.

- Mark Zandi, economist for Moody’s, in the same article is quoted as saying his more optimistic forecast has residential construction growing to 1.1mil in 2013 and 1.7mil new housing starts in 2014, growth of 46% and then 54%. I say NO WAY

- A more reasonable projection is new housing starts may reach 850K to 900K in 2013 and 1.0 to 1.05 million in 2014, new homes growth rates of 15% to 20% and total residential spending growth of 12% to 15%. That still has the workforce expanding rapidly, but at least at a not unheard of rate.

Housing starts reached 925,000 in 2013 and 1,003,000 in 2014, well below the 30 year historical annual growth.

From Jan 2013

- Future escalation, in order to capture increasing margins, will be higher than normal labor/material cost growth. Lagging regions will take longer to experience high escalation.

- I’m advising a range of 4% to 6% for 2013, 5% to 7% for 2014 and 6% to 8% for 2015.

- Expect residential escalation near the upper end of the range.

Actual total construction cost inflation 2013 = 4.3%, 2014 = 4.7% 2015 = 2.9%. All inflation values were held to lower totals due to infrastructure work which did not have more than 2% inflation during that period and actually experienced deflation in 2015. Residential buildings inflation for 2013-14-15 was 8.9%, 7.1% and 4.1%.

Posted April 2014

- Construction Spending “residential buildings” expect $379 billion in 2014

- Construction Spending “nonresidential buildings” expect $325 billion in 2014

- Construction Spending “totals” expect $960 billion in 2014

Posted August 2014

- Construction Spending “residential buildings” expect $365 billion in 2014

- Construction Spending “nonresidential buildings” expect $314 billion in 2014

- Construction Spending “totals” expect $961 billion in 2014

2014 Residential spending = $354 billion

2014 Nonresidential spending = $320 billion

2014 Total Construction spending = $960 billion

These values prior to U.S. Census major correction to data.

Posted August 2014

- If you are pricing future construction jobs the way you always have, with 2-3 pct escalation, you are already in trouble!

- If you’re an owner with plans to construct a building in the future and you are inflating cost by only 2-3 pct, you’ve missed the boat.

Total construction inflation for 2013-14-15 was 4.3%, 4.7% and 2.9%. All years were reduced by a lack of inflation in infrastructure work. Inflation for nonresidential buildings was 3.5%, 4.2% and 4.8%. Residential buildings inflation was 8.9%, 7.1% and 4.1%.

Posted September 2014

- Real Construction Volume in 2014 (construction spending minus inflation) will grow less than 2 percent

Real construction volume in 2014 increased 4.9%. Commercial nonresidential construction started it’s current boom.

Posted Dec 2014

- Construction Spending “residential buildings” expect $405 billion in 2015

- Construction Spending “nonresidential buildings” expect $364 billion in 2015

- Construction Spending “totals” expect $1,040 billion in 2015

Posted Jan 2015

- Cash flow of new starts for nonresidential buildings indicates a 15% increase in the monthly rate of spending over the next 10 months.

- Both ABI and Starts cash flows indicate a mild slowdown in nonresidential buildings construction spending at the end of 2014 before a strong upturn in spending in 2015. Expect another drop in spending late in 2015

For the period Nov 2014 through Feb 2015, spending on nonresidential buildings stalled flat for 4 months. The monthly rate of spending increased 14% over the 10 months from Oct 2014 to September 2015. Since Sept 2015 spending has been flat.

Posted March 2015

- Even if new starts turn flat for rest of 2015, starts already recorded are indicating Nonresidential buildings construction spending for 2015 will reach 15%+ growth. My closest competitor is forecasting 12.5% growth. The average of all other industry forecasts is 8% growth.

Spending for nonresidential buildings actually hit +17% growth over 2014.

Posted July 2015

- Construction Spending “residential buildings” expect $388 billion in 2015

- Construction Spending “nonresidential buildings” expect $397 billion in 2015

- Construction Spending “totals” expect $1,067 billion in 2015

2015 Residential spending = $390 billion

2015 Nonresidential spending = $387 billion

2015 Total Construction spending = $1068 billion

These values prior to U.S. Census major correction to data.

Posted July 2015

- Nonresidential Buildings spending growth 2015 vs 2014.

- My forecast (Average all others) [closest competitor]

- Educational 7.1% (3.8%) [5.6%]

- Healthcare 6.0% (3.9%) [4.0%]

- Commercial/Retail 5.5% (11.8%) [8.4%]

- Lodging 24.0% (13.7%) [17.1%]

- Office 21.1% (13.5%) [19.2%]

- Manufacturing 49.6% (15.9%) [24.6%]

Educational 6.7%

Healthcare 4.6%

Commercial/Retail 8.4%

Lodging 30.8%

Office 21.9%

Manufacturing 47.3%

So there you have it. Several years of forecasts and how they turned out. You can get an idea of my track record. You be the judge. 🙂

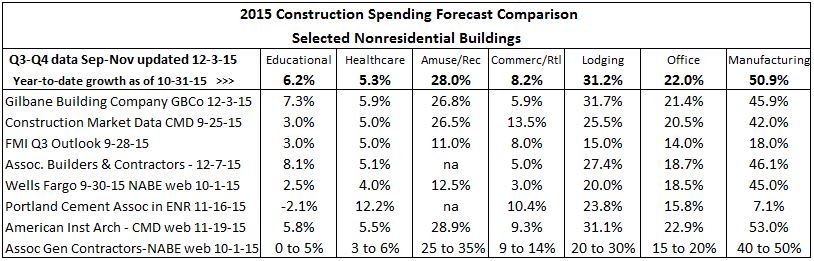

Forecasting Nonresidential Buildings Markets 2015 Results

Here are latest updates for 2015 predictions in nonresidential buildings markets. Eight firms have posted forecasts for spending growth in nonresidential construction markets.

Actual spending put-in-place for October year-to-date (YTD) is included in the YTD shown at the top of the table. Don’t expect most markets to change much in the last two months of data. Both Commercial/Retail and Manufacturing have been declining in recent months and are expected to continue to drop slightly.

Once the September YTD data is in, a strong forecast for the year can be made with only three months outstanding. It will be interesting to look back at this chart when the final numbers for 2015 become available in February 2016 to see how we did. Earlier posts and reports can be referenced to see forecasts from midyear.