Dodge Data & Analytics Outlook 2016 event held in Washington DC, October 30, 2015.

A brief summary of comments heard and information from my notes.

Art Gensler – Founder Gensler

How do you control 5000 people? Hire good people and get out of their way.

People value what they pay for and ignore what they get for free.

Beth Ann Bovino – U.S.Chief Economist, Global Economics & Research, Standard & Poor’s

Domestic economy is strong and strengthening.

Jobs are stronger – Quits rate is at a 7 year high.

Housing starts are up – Home prices are up.

Wages are struggling and we have a historical 38 year low labor participation rate.

Ted Hathaway – CEO Oldcastle BuildingEnvelope

We increased wages significantly to keep people from leaving.

The cost and disruption is huge if you lose a valuable member of a team.

Dan McQuade – President, Construction Services, AECOM

Three emerging trends

Global collaboration

Investing capital with clients and partners

Better collaboration with vendors & suppliers. Treat subs and vendors as partners.

Larry Kudlow – Economist and Senior Contributor CNBC

Our biggest problem – We do not have strong steady economic growth.

Corporate profits were high after recession but have declined last three quarters. Profits were likely responsible for the stock market rise.

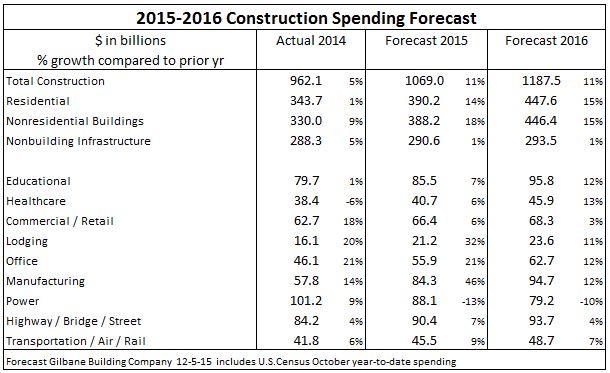

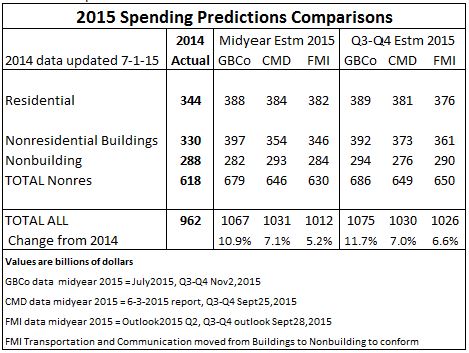

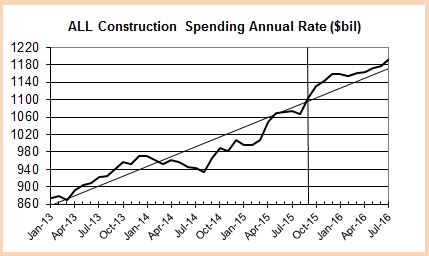

Bob Murray – Vice President, Economic Affairs, Dodge Data & Analytics

The DMI is reflecting the institutional dip has ended and now beginning to grow, although slowly.

New construction starts 2013 = 11%, 2014 = 9%, 2015 = 13%p

Actual $ put-in-place 2013 = 7%, 2014 = 5%, 2015 = 10%

New starts that declined in 2015 Warehouses, Stores, Public Bldgs, Manufacturing

New Starts that increased in 2015 Residential, Hotels, Highway, Electric-Gas-Power

Expectations for 2016

Total new construction starts up 6%.

Residential up 16%, single family will grow faster than multifamily.

Commercial up 11%, led by warehouses and stores

Institutional up 9%, led by educational

Manufacturing down 1%, but from very high 2014 and 2015

Power down 43% from extreme high starts in 2015

Construction cycles may be indicating we have years of growth left in the current cycle.