The data continues to get tighter with each new release. This forecast is updated Dec 5th to include US Census October spending released Dec. 1 and Dodge Data & Analytics construction starts October released Nov. 20.

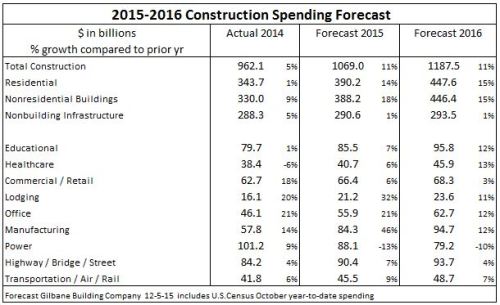

The six major nonresidential buildings markets reported here represent 90% of all nonresidential buildings and the three infrastructure markets represent 75% of all nonbuilding infrastructure. This gives a good picture of which markets contributed the most (least) to 2015 growth and which will offer the most (least) support to 2016 growth.

My forecast is construction spending for 2015 will total $1.069 trillion supported by an 18% increase in nonresidential buildings spending. For 2016 expect spending to total $1.187 trillion with increases of 15% in both residential and nonresidential buildings.

With the October spending results included, robust data allows predicting 2015 year-end results with great confidence. For the 2016 forecast, new starts booked through December 2015 will contribute 75% to nonresidential buildings spending, 55% to residential spending and 80% to spending on nonbuilding infrastructure.

This forecast may be revised slightly for the upcoming Winter Construction Economics report.