Construction Jobs – Is July a Turning Point?

8-6-16

The July jobs report issued yesterday gives us labor data to compare to spending. Here’s a few tweets I put out yesterday.

From Sep to Mar spending increased by 4.5% but jobs/hours increased by only 3% = productivity gains. Now seems to be reversing.

Since March, construction spending is down 3.7%, construction jobs are down 0.3%. Beginning to see 2015 productivity gains reset.

Last 12mo Residential Construction Spend up 3%, rsdn jobs up 5%. Next few months room for spend to grow with little jobs growth = Balance

Construction Workforce portion identified as in force but unemployed at 16 year low. Yes, there is a labor shortage.

While the immediate comparison we read is often what happened this month versus last month, for comparison to construction spending it is perhaps better to look at recent longer trends.

- For the 6 month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of growth in 10 years. Then, after 3 months of losses, July shows a modest gain.

- During that same period Q4’15 spending was flat but by the end of Q1’16 spending had increased more than 4% in 6 months, or at an annual rate of 8% to 9%.

- Even though some upward revision is expected for June spending, total Q2’16 spending will still be down 2% to 3% from Q1.

- Q2’16 jobs declined all 3 months, keeping in mind this immediately follows the fastest rate of growth in 10 years. But it also tracks directly to three monthly declines in spending.

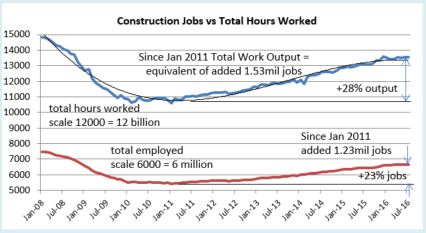

- Since Q1 2011 the constant $ value of construction spending after inflation increased by 30%. Jobs/hours worked output increased by 28%.

It is not so unusual to see jobs growth slowed in these last few months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

We got modest growth in July that I hope to see continue for the 2nd half 2016. I expect spending to experience strong growth in the 2nd half and jobs growth should follow closely, perhaps adding 125,000 to 150,000 more jobs. However, although I do expect both spending and jobs growth, jobs could be somewhat restrained by lack of available skilled workers.

June 2016 Year-To-Date Construction Spending

update 8-6-16 See this link to July Jobs Report

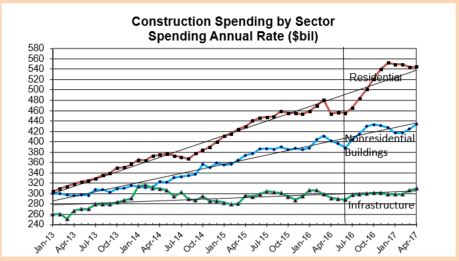

Construction spending for June reported by U.S. Census totaled $1.134 trillion, the lowest since $1.126 trillion in December 2015. Spending hit the lowest for 2016 after reaching a 9 1/2 year high of $1.176 trillion in March.

Spending for June is down 0.6% month/month from a revised May. May and April were both revised down. Construction spending year-to-date is now only +6.2% vs. the same six months 2015. It was above +8% year-to-date for the last three months.

Construction spending reached a 9 1/2 year high in March. The biggest declines in spending since March are Residential -5%, Healthcare -4%, Educational -6%, Highway & Street -6%, Sewage & Waste Disposal -12% and Manufacturing -8%. The only significant increases since March are Lodging +3.4%, Power +2.5% and Conservation +6%. Power is the only big $ volume sector.

The Census spending numbers for both May and June seem somewhat suspect as they fall well outside the statistical mean for expected percentage of total annual spending within those months. June reported residential spending is 6% below statistical mean for June, larger than any variance in 15 years, therefore it becomes suspect. Granted this is based on only six months of actual spending with six months still to go. However the residential variance is so significant, following that trend would reduce residential spending for the remainder of the year by $30 billion, or more than 10% of the final six months. This is an unlikely scenario, unless it were to signify the beginning of a steep downturn starting in March and continuing for the remainder of 2016. Construction starts dollar volume does not support that scenario. Therefore, I have not adjusted down my predicted spending for the remainder of the year based on the downtrend for April, May and June as-reported actual spending. Although it is an uncomfortable position to take, I expect to see some upward revisions in the coming months.

Spending is dependent on long duration cash flows from all previous construction starts. Construction Starts as reported by Dodge Data & Analytics provide a base to predict spending. Dodge reports starts in dollars. Starts gives a long term trend view of spending.

Previously I said we should expect a short duration downturn in spending occurring from January through March. The monthly unevenness in the dollar volume of new starts over the last two years indicated a slowdown in spending during the first quarter 2016. As it turns out, first quarter spending was much stronger than expected, averaging $1,175 billion which is a 9 1/2 year high. Spending has been declining since the March peak, averaging only $1,140 for Q2, down 3% from Q1, but still near a nine year high.

It will take several more months to see if spending rebounds and to see if that helps identify this April-May-June downturn as the dip I expected in Q1, but just had targeted it off by several months for when the dip would occur.

If May or June get revised up and/or the 2nd half rebounds to confirm the slight dip, spending will come right back to the long term trend.

Total first half spending is only 1% below what I predicted. If a 2nd half spending rebound materializes, we should still finish 2016 near $1.200 trillion in total spending, up 8% from 2015.

This article by Luke Kawa @LJKawa on BloombergMarkets @markets which quotes me also includes comments from Bespoke’s @GeorgePearkes on the disparity between the trend in spending and Census residential # of units under construction. The graphic comparison shows spending vs # units diverging for May-June, units advancing and spending declining. This is another clue this may get revised in future data.

Something Is Odd About the Latest U.S. Construction Data

7-6-17 The most recent release of Census Construction Spending data issued July 3, 2017, revises data back to January 2015. The May and June 2016 data discussed in the Aug. 2, 2016 article linked above were both revised up 3%. This upward revision to the data puts it right in line with growth expected back in August 2016, confirming our questioning the data as suspect at that time.