8-6-16

The July jobs report issued yesterday gives us labor data to compare to spending. Here’s a few tweets I put out yesterday.

From Sep to Mar spending increased by 4.5% but jobs/hours increased by only 3% = productivity gains. Now seems to be reversing.

Since March, construction spending is down 3.7%, construction jobs are down 0.3%. Beginning to see 2015 productivity gains reset.

Last 12mo Residential Construction Spend up 3%, rsdn jobs up 5%. Next few months room for spend to grow with little jobs growth = Balance

Construction Workforce portion identified as in force but unemployed at 16 year low. Yes, there is a labor shortage.

While the immediate comparison we read is often what happened this month versus last month, for comparison to construction spending it is perhaps better to look at recent longer trends.

- For the 6 month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of growth in 10 years. Then, after 3 months of losses, July shows a modest gain.

- During that same period Q4’15 spending was flat but by the end of Q1’16 spending had increased more than 4% in 6 months, or at an annual rate of 8% to 9%.

- Even though some upward revision is expected for June spending, total Q2’16 spending will still be down 2% to 3% from Q1.

- Q2’16 jobs declined all 3 months, keeping in mind this immediately follows the fastest rate of growth in 10 years. But it also tracks directly to three monthly declines in spending.

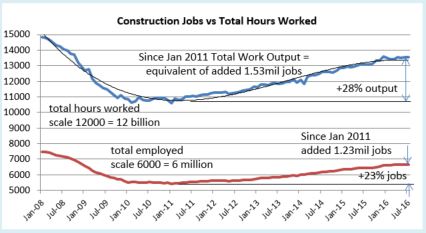

- Since Q1 2011 the constant $ value of construction spending after inflation increased by 30%. Jobs/hours worked output increased by 28%.

It is not so unusual to see jobs growth slowed in these last few months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

We got modest growth in July that I hope to see continue for the 2nd half 2016. I expect spending to experience strong growth in the 2nd half and jobs growth should follow closely, perhaps adding 125,000 to 150,000 more jobs. However, although I do expect both spending and jobs growth, jobs could be somewhat restrained by lack of available skilled workers.