Notre Dame Cathedral Repairs

I’ve read a few news articles that proclaimed charitable donations to Notre Dame may not be enough to cover the cost to rebuild the damaged cathedral roof. One article on Bloomberg news stated, “The cost might well run as high as 8 billion euros”.

I think it’s time some news sources engage with a professional architect, engineer and cost estimator before writing these articles. 8 billion Euros is enough to spend an astronomical amount to repair the damage!

One World Trade Center is the most expensive building built in the U.S. It cost $4 billion. It measures 3.5 million square feet (SqFt).

Some sources are saying the Notre Dame cathedral roof repair may cost more than $8 billion. The Notre Dame roof, as closely as I can determine from online data of the building, measures about 50,000 SqFt.

Just think about that.

I’m stretching my thought process to come up with a rough estimate that would cost as high as $250 million. Frankly, my rough estimate is quite a bit lower than that, and that would still be far more costly per SqFt than the most expensive building in the U.S.

I haven’t yet seen an architect / engineer estimate of the total area of the roof. I traded some emails with an architect who thought total area was 25,000 SqFt. I searched online and come up with potential area of roof at 50,000 SqFt. Here I’m using 50,000 SqFt.

I have not seen any other realistic cost estimates. But, the most expensive roof covering and roof structure I’ve ever estimated was less than $100/SqFt (in 2019 dollars).

My order of magnitude estimate (OME) (very general), for a unique, complex structure and premium roof covering could be $500/SqFt. Portions of this roof need to be quite ornate and also the estimate must include a ceiling structure. For a historical and rare roof plus inside work let’s double that estimate to $1000/SqFt. That’s 10x the cost of the most expensive roof I’ve ever estimated / built.

$1 billion would provide for $20,000/SqFt.

$8 billion would provide for $160,000/SqFt!

Even if my OME is 10x too low and I make a 10x adjustment, cost would then be $10,000/SqFt for a total cost = $500 million. That’s 100x more expensive than the most costly roof I’ve ever estimated. Frankly, I can’t come up with any conceivable scenario where it could cost that much.

footnote: 8 billion Euros is currently about $9 billion US dollars

Apr 2025 – News articles that I’ve seen state that the repair cost $700-$800 million.

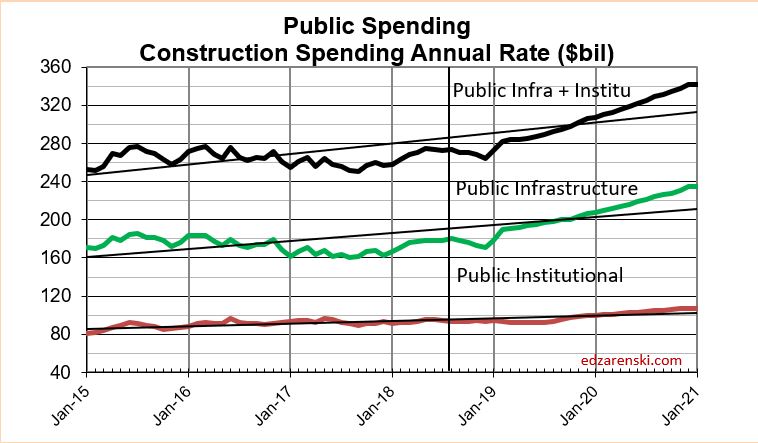

Public Infrastructure – Behind the Headlines

PUBLIC WORK AND INFRASTRUCTURE SPENDING

Most public work is non-building infrastructure, or public works type projects, but some public work is nonresidential buildings. In 2018, of $301 billion in public work, $177 billion (59%) is non-building infrastructure, $118 billion (39%) is nonresidential buildings, $6 billion is residential. The public subset of work in the last 25 years has grown by $20 billion/year only twice, during the construction boom of 2006-2007.

Excluding the worst recession years, the average annual growth of all publicly funded work since 2001 is $8 billion/year. In the four best construction boom years growth averaged $20 billion/year.

The two largest markets contributing to public spending are Highway/Bridge and Educational, together accounting for nearly 60% of all public construction spending. At #3, Transportation is only about 12% of public spending. Sewage/Waste Water and Water Supply add up to another 12% of public work. All other markets combined, none more than 4% of total public work, account for only 15% of public spending.

Non-Building Infrastructure sector, at a total of $313 billion in 2018, is less than 25% of all construction spending, mostly supported by the Power market. Power accounts for 33% of all non-bldg infrastructure spending. Highway represents 30% and Transportation about 15%. However, Power is 80% private; Highway is 100% public; Transportation 70% public.

60% of non-building infrastructure spending is publicly funded. Highway is a little more than half of all publicly funded non-bldg infrastructure work. The public non-bldg subset of work in the last 25 years has grown by $10 billion/year or more three times, 2006, 2007 and 2018. In 2006-2007, Highway accounted for most of that growth. In 2018, Transportation accounted for half the growth.

Excluding the worst recession years, the average annual growth of publicly funded non-bldg infrastructure work since 2001 is $5 billion/year. In the four best construction boom years growth averaged $12 billion/year.

Nonresidential Building sector, at a total of $434 billion in 2018, is 35% of all construction spending, mostly supported by the Educational and Commercial markets. Educational accounts for 22% of all nonresidential buildings spending, commercial 20%. However, Educational is 80% public, Commercial is only 4% public.

Other nonresidential buildings that are publicly funded are: Public Safety – 100% public; Amusement/Recreation Facilities (i.e.’ Convention Centers, Stadiums) – 45% public; Healthcare – 20% public; Office – 13% public. None are more than 4% of total public spending.

Less than 30% of nonresidential buildings spending is publicly funded. Educational is 60% of all publicly funded nonresidential building. The public nonresidential building subset of work in the last 25 years has grown by $10 billion/year twice, in 2007 and 2008. Both times, Educational accounted for 75% of that growth.

Excluding the worst recession years, the average annual growth of publicly funded nonresidential building since 2001 is $4 billion/year. In the four best construction boom years growth averaged $8 billion/year.

Residential is 40% of all construction spending but only 2% of public spending.

Average post-recession growth in public infrastructure + public institutional jobs is about 40,000 jobs per yr. Maximum growth in a year was 60,000 jobs. Growth of $10 billion in spending in a year supports about 40,000 new jobs.

All public work in the last 25 years has grown by $20 billion/year only twice. The average annual growth of all publicly funded work since 2001 is $8 billion/year. In the four best construction boom years growth averaged $20 billion/year.

Total All Public Infrastructure construction, including non-building public works and nonresidential public buildings, already has 2019 and 2020 growth projections at historic capacity of +$20 to +$30 billion/year. Historically, even in the construction boom years of 2005-2008, we have never exceeded that growth volume, especially by another $10-$20 billion/year, nor added an additional 40,000-80,000 jobs per year above the average 40,000 or the maximum 60,000 jobs in a year.

Any government funding intended to increase public infrastructure construction would most likely be limited by industry growth rates to at best no more than $10-$20 billion a year.

See Marketwatch.com for additional notes I’ve posted regarding spending limits.

The above Marketwatch article links to a twitter thread I posted that summarizes Infrastructure limitations in a nutshell.

See also these articles for much more analysis on Infrastructure

2018/02/16 Down the infrastructure rabbit hole

2017/01/30 Infrastructure – Ramping up to add $1 trillion

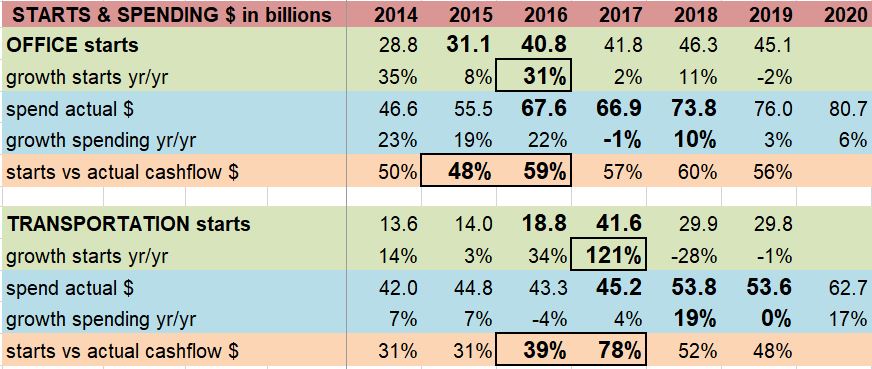

Construction Starts – Behind the Headlines

New Construction Starts data represents a share or a portion of all construction, on average about 60% of all construction. Dodge Data starts totaled approximately $740 billion and $785 billion for 2016 and 2017. Total construction spending was $1,246 billion in 2017 and $1,300 billion in 2018. What happens if within individual markets the share of information collected in the starts data is not constant from year to year?

Office starts increased by an average of 20%/year from 2012 to 2015. Spending increased by 20%/year from 2013 to 2016. But then in 2016, starts increased 31% and spending in 2017 turned to a 1% decline. 2018 spending gained only 10%. That was unusual and unexpected since 2016 starts indicated a very large increase in spending the following year.

Growth in starts can signify one of two things; future growth in spending, or growth in capturing a larger share of the market. To find share of market captured, starts need to be compared to the cash flow over the time for which those starts will be spent. Typical cash flows predict 20% gets spent in the year started, 50% in the following year and 30% in the 3rd year.

For the period 2011-2015, office starts compared to the value of cash flow over the next 3 years stayed within a range of 45% to 50% of total spent. For 2016 starts, the share of starts compared to cash flow of those starts jumped to 60%. In other words, the growth in spending in 2017 and 2018 did not correspond to the huge growth in starts in 2016. The 31% growth in 2016 starts did not produce future growth in spending but may have mostly represented growth in capturing a larger share of the market.

Analysis shows similar activity in Transportation starts versus spending and to a lesser extent is several other markets.

Construction Starts Data can vary year to year as a share of total market activity. Commonly used to predict future spending, the share of market captured in the starts data, if not consistent, can skew any use to forecast spending. Starts share of market must be analyzed before starts can be used to forecast future spending.

Inflation and Forecasting Presentation Advancing Precon & Estm Conf 5-22-19

This is a PDF of slides (including notes) from my

Construction Inflation & Forecasting Presentation

at Hanson Wade

Advancing Preconstruction & Estimating Conference

Dallas, TX 5-22-19

Advancing Pre-construction & Estimating conference 2019

Full EdZ Presentation Inflation-Forecasting w notes HW-APE 5-22-19 PDF