Home » 2019

Yearly Archives: 2019

2020 Construction Forecast Briefs

2020 Construction Forecast Briefs

12-23-19 updated 1-4-20

updated 1-4-20 – The construction spending forecast for 2019 is revised up to $1,304 billion, still a decrease of 0.2% vs 2018. Almost all of the revision up is residential spending that was added in Oct and Sept Census spending revisions released 1-3-20.

The forecast for 2020 construction spending is $1,360 billion, up 4.5% over 2019.

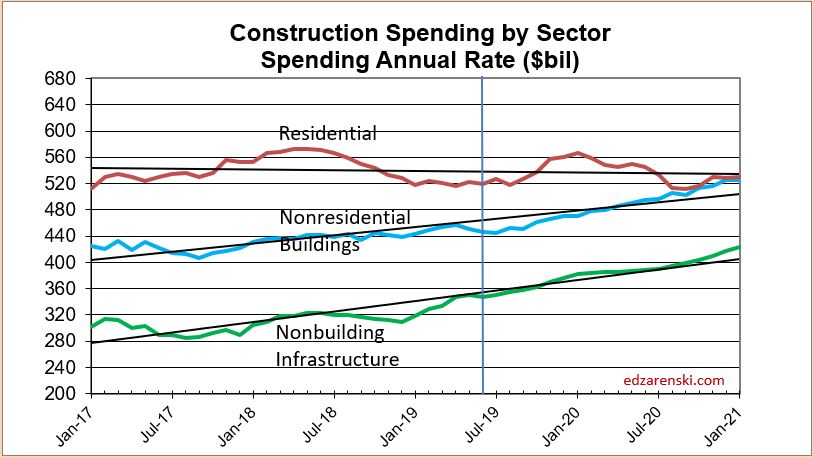

Total Spending increased 9%/yr. from 2012 to 2016, then in 2017 and 2018 slowed to 4%/yr. Spending declined <1% in 2019 and is forecast up 3% to 4% for both 2020 and 2021.

New construction starts, as reported by Dodge Data and Analytics, increased 7%/year in 2016 and 2017, but only 3% in 2018. Starts are forecast to decline slightly in 2019 and 2020.

New construction starts data captures a share of the total market or a portion of all construction spending, on average about 60% of all construction. In this analysis every market is adjusted by its own individual market share factor.

Applying the market share factors, starts are forecast up slightly in both 2019 and 2020.

Backlog reaches a post-recession high starting 2020, up 20% from 2017, up 100% from 2013. Starts and backlog growth are forecast to remain below 3%/year gain or decline over the next few years. Total spending has only slight gains in 2021 and 2022.

Backlog at the beginning of the year or new starts within the year does not give an indication of what spending will be like within the year. Backlog increases if new starts during the year is greater than spending during the year. An increase in backlog could be a level rate of market activity for a longer duration. It takes several years for all the starts in a year to be completed. Cash flow shows the spending over time.

The best indicator of future construction activity is the sum of the projected cash flow generated by all the construction starts that have been recorded.

plots updated 1-4-20

Spending cash flow predicted from Dodge Starts and construction spending to date.

A what if scenario in which new construction starts drop by 10%:

On average about 20% of new nonresidential construction starts gets spent within the year started, 50% is spent in the next year and 30% is spent in future years. (For residential the spending curve is more like 70%-30%). If new starts drop by 10% this year, that has only a -2% impact on total nonresidential buildings spending for this year. It would be -5% next year, -3% after. If starts drop a second year, the same impacts occur, shifted one year out, and the total impact for both years is added.

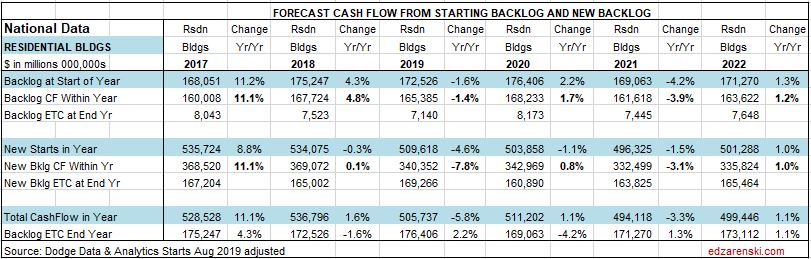

Only about 30% of residential spending within the year comes from backlog and 70% from new starts. If residential new starts drop 10% that impacts total residential spending by 7% in that year.

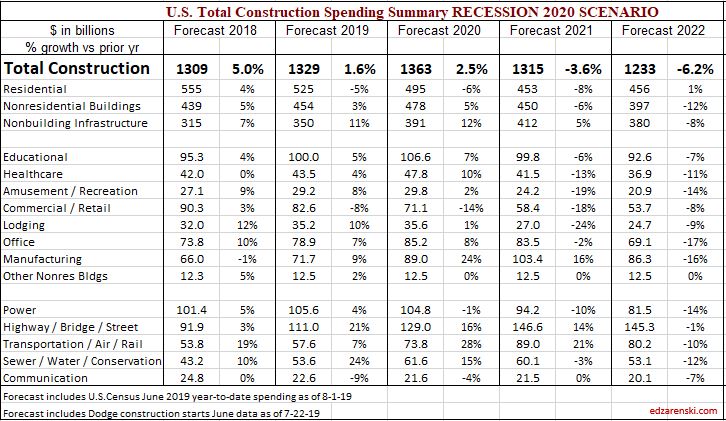

Nonresidential Buildings starts (excluding Terminals) have reached a new high every year since 2009, but the last three years starts are up only 2% to 3%/year. Every market posted increases in 2017 and 2018. Only Commercial/Retail and Amusement/Recreation declined in 2019. Backlog for Office Buildings, which includes data centers, is up 100%+ since 2015. Spending is still up 4% in 2020 but then with the slowdown in starts forecast in 2020, backlog growth stalls and spending slows in 2021-2022.

Nonresidential buildings markets advancing in 2020-2021 are Educational, Healthcare, Office and Manufacturing. Markets declining are Amusement/Recreation, Commercial/Retail and Lodging.

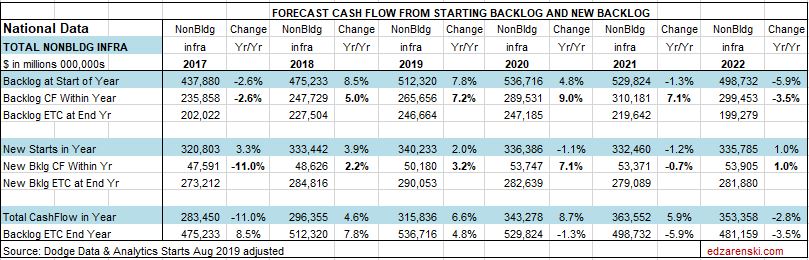

Non-building Infrastructure starts (including Terminals), up 4% in 2019, are at an all-time high. The two markets with the largest share of new starts are Highway/Bridge and Transportation. Transportation terminals and rail starts are up 30% in the last three years, but backlog has nearly doubled because a large portion of those starts is very long duration projects. Starts are forecast up only 1% in 2020 but backlog peaks in 2021. Spending increases are in the 6% to 8% range at least for the next two years.

Spending in recent years has been boosted by Transportation terminals, Highway and Public Works projects. Power is flat or down slightly.

Residential starts averaged 19%/year growth from 2012 to 2016 but slowed to 5%/year for 2017 and 2018. Starts declined in 2019 and are forecast to decline again in 2020.

The outlook for residential construction spending has improved slightly. Previous forecast had residential spending in 2019 down 6% and 2020 up only 2%. That’s been revised to now forecast 2019 down 4.5% and 2020 up 5%. Spending holds steady in 2021.

If spending is increasing 3%/year at a time when inflation is 5%/year, then real volume is declining. In the last two years, spending increased only 3%, but construction inflation totaled 9%, therefore

in two years, real volume declined by 6%, yet jobs increased by 7.5%.

Since early 2018, jobs have been increasing while construction volume is declining. The volume of work in the last two years does not support jobs growth.

Volume, spending adjusted for inflation in Constant 2017$

Nonresidential Buildings will post declines in volume in 2020 & 2021. Residential volume gains 1% in 2020 but slips again in 2021. Non-building Infrastructure will increase volume about 3%/year. Overall, total construction volume declined in 4 of the last 6 quarters and is forecast to drop slightly in 2 or 3 quarters in 2020.

One of the best predictors of construction inflation is the level of activity in an area. When the activity level is low, contractors are all competing for a smaller amount of work and therefore they may reduce margins in bids. When activity is high, there is a greater opportunity to bid on more work and bids can be higher. The level of activity has a direct impact on inflation.

Volume declines should lead to lower inflation as firms compete for fewer new projects. However, if jobs growth continues while volume declines, then productivity continues to decline and that will add to labor cost inflation.

Jobs vs Volume growth set to base year 2011

Average long-term nonresidential buildings inflation excluding recession years is 4.2%.

Average long-term (30 years) nonresidential construction cost inflation is 3.5% even with any/all recession years included.

Nonresidential buildings cost inflation for 2018 and 2019 averaged 5%. It’s predicted closer to 4.5% for 2020 and 4% for 2021.

Residential buildings cost inflation for 2018 and 2019 averaged 4%. It’s predicted at 3.75% for 2020 and 2021.

For more on the 2020 Forecast see these

2020 Construction Spending Increases, but Volume is Down

12-10-19 updated 1-4-20

2020 Construction Forecast

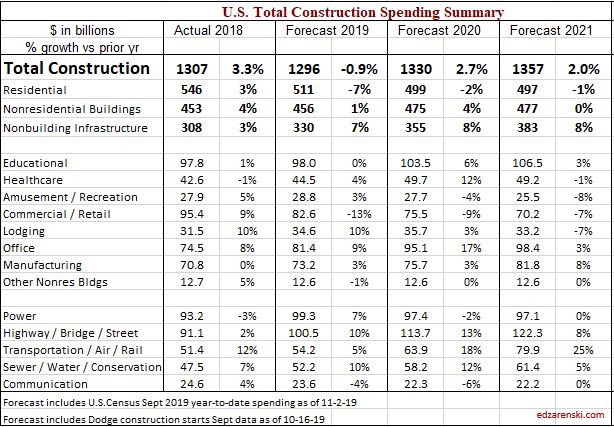

Construction Spending for 2019 finishes flat for Nonresidential Buildings, Up 7% for Non-building Infrastructure and Down 5% for Residential.

Spending UNadjusted for inflation.

After adjusting for inflation, we see that real construction volume is down. Only Non-building Infrastructure realizes gains in 2019 & 2020. Nonresidential Buildings Volume has been up and down since Q1 2017. Residential volume has been declining since early 2018.

Volume, spending adjusted for inflation in Constant 2017$

I’m predicting Nonresidential Buildings will post declines in volume in 2020 & 2021. Residential gains 1% in 2020 but slips again in 2021. Non-building Infrastructure will increase at about 3%/year. Overall, total construction volume declined in 4 of the last 6 quarters and is forecast to drop slightly in 2 or 3 quarters in 2020.

Volume declines drive labor to slower growth. We had 6 years of 250,000-300,000 annual growth. Jobs will increase only 150,000 in 2019. In 2020, it could be lower to 100,000.

After 2006, and all the way to 2017, jobs and volume growth were pretty equal. Since 2017 there is a divergence forming. That can’t be sustained.

Jobs vs Volume growth set to base 2006

See the Jobs analysis here Expect Construction Jobs Growth to Slow in 2020

The plot below shows the predicted spending from modeling Dodge data new construction starts. Overlaying this plot is the actual census spending. You can see the actual value follows pretty closely to the predicted. None of this data is adjusted for inflation.

Spending predicted from Dodge Starts and actual spending to date.

Healthcare and Office are strong markets in 2020, as well as Highway, Transportation and Public Works. Backlog is strongest for Non-building Infrastructure leading into 2021. In the three years since 2017, backlog in Transportation is up 80%, Environmental Public Works up 40%. Within nonresidential buildings, Office backlog is up 60%, Educational is up 15% and Healthcare up 25%. Commercial Retail is the only market with a decline in backlog over this three year period, down 15%.

Table of Spending by Market Type. updated 1-4-20

A reminder, You can’t interpret new construction starts directly to backlog or spending. Starts growth is one thing, but starts data requires cash flow modeling to get spending. Why are Transportation starts for 2018+2019 down 35% but both 2019 and 2020 spending are up? Because in 2017, the year before the data in this table, starts were up 75% and much of that was very long duration work, some that potentially has peak spending 3 to 4 years out, so is still adding a boost to 2020 spending and backlog.

For more on the 2020 Forecast see these:

2020 Construction Forecast Briefs

Expect Construction Jobs Growth to Slow in 2020

Expect Construction Jobs Growth to Slow in 2020

12-6-19

The construction spending forecast for 2020 indicates 2% growth. But predicted 2020 construction inflation is slightly higher than 4%. So, real construction volume in 2020 decreases by 2%. Jobs should follow volume growth, yet history shows that in non-recessionary periods, even with volume declining, jobs usually continue to increase, but perhaps at a slower rate.

This plot shows the forecast volume decline in 2020. For the 2020 forecast we already have 80% of all nonresidential spending in backlog. Since new starts account for only 20% of the spending in the year, a 10% drop in new starts from forecast affects only 20% of the spending, so has only a 2% impact on the total. Nonresidential shows flat to moderate gains in 2020.

Residential forecast will be much more dependent on new starts in 2020. About 70% of residential spending within the year comes from new starts within the year, so quick or large changes in new starts has a huge effect on spending for the year. Residential spending is down 10% from early 2018 but residential volume after accounting for inflation is down 15% since that early 2018 peak.

Simply stated, there has not been any volume growth in the last two years to support jobs growth. In constant $, there was no volume growth in any sector in 2018. In 2019 and 2020, only Non-building Infrastructure shows growth, 2%-3%/yr.

This plot shows predicted 2020 jobs growth of 1.5% or just over 100,000 jobs. Since volume is forecast to decline, any jobs growth in 2020 will increase the disparity between jobs and volume growth. The disparity has been increasing since early 2018. It’s a 15% difference right now. Within a year that could be 20%.

To emphasize the growing difference, look at these two plots, actually, the same plot just modified to account for the 15% bust in 2006.

By accounting for the 15% difference in 2006, essentially, resetting the baseline to 2006, it shows all other years up to 2017 were pretty well-balanced growth. With the exception of 2006 and now 2018-2019, for almost every year from 1997 to 2019 jobs grew pretty closely aligned with volume. A big spread occurred in 2006, then growth remained balanced through 2017. The spread now is near the same as it was in 2006.

Construction jobs growth slowed substantially the last two quarters. I predicted jobs growth would slow because volume growth had already been declining since early 2018 when volume reached a peak of $1,300 billion. Volume is now $1,170 billion, down 10% in 20 months. After 6 years of jobs increasing at an average 275,000/year, jobs are up only about +150,000 in the last year, but only +48,000 in the last 7 months. The rate of jobs growth is now the slowest in 7 years. I expect this trend to continue.

The plot of jobs growth below shows current growth rate is below an annual rate of 150,000 jobs/year and it is expected to remain there through 2020, potentially dipping as low as 100,000.

I’d be surprised if jobs start to decline, but that certainly could be envisioned and it would help explain away some of the disparity in growth shown on the Jobs/Volume plot up above.

see also Construction Jobs and JOLTS

Advancing Construction Presentation 12-3-19

This short construction economics slide deck was presented at Hanson Wade’s Advancing Construction – Enterprise Risk Management Dec 2019 Miami, FL

Construction Economic Forecast pdf-notes-edz-presentation 12-3-19

To Support Construction Jobs, We Need Volume

11-2-19

12-6-19 plots updated to include Nov jobs and Oct spending.

Construction Spending IS NOT Construction Volume.

I read an analyst report this week that stated construction jobs growth isn’t keeping pace with construction volume growth. The reference appeared to be to construction spending. That fails to apply inflation to convert construction spending to construction volume, so compares apples to oranges. Spending must be adjusted for inflation to get real volume growth. Jobs MUST be compared to volume.

For over two years now, construction volume growth has not supported construction jobs growth we’ve seen. I expected jobs growth to slow down. I’ve been saying this for over a year. This sure looks like it.

For 2018 jobs growth averaged over 300k. Since January 2019 the rate of jobs growth has dropped from 300k to 150k.

Current projected new starts data IS NOT supporting construction volume growth for the next 2 yrs. Growth of 3%/yr in non-building infrastructure will be offset by declines in residential buildings and flat nonresidential buildings. Therefore, there is no real volume support for jobs growth.

This plot adjusts construction spending by taking out inflation to get real construction volume growth. Last year of real volume growth was 2016. Yet jobs continue to climb. This can’t continue. The plot above shows it has slowed.

Construction jobs growth has slowed considerably over last 2Q, as expected. While construction jobs are up about +150k in last year, jobs (through Nov) increased only +48k in the last 7 months. I’m expecting this trend to continue. In fact, I wouldn’t be the least bit surprised to see in the near future some months when construction jobs decline. The fact is, construction volume simply does not support jobs growth.

Total construction volume, spending after accounting for inflation, has been down for 5 of the last 6 quarters. Volume peaked from Q1 2017 to Q1 2018, but the last year of real volume growth was 2016. Volume is flat or down while jobs continue to rise. This can only mean contractors will be at risk of being top-heavy jobs if a downturn comes.

Caution is advised if putting emphasis on construction JOLTS, which has been climbing to new highs. From mid-2006 to mid-2007, JOLTS reached near the then all-time high. But construction volume, starting in mid-2006, was already on the downward slope. Volume peaked in early 2006 and fell 10% by mid-2007. Construction did not begin shedding jobs until late 2006, but mid-2007, job losses were well underway. Within 12 months, more than 500,000 jobs were gone. Within 18 months, construction jobs were down 1.5 million.

Construction spending annual rate will increase by 3% in the next 12 months, but volume in constant $ after inflation will remain flat. In Q42020-Q12021 spending slows to less than inflation, so volume begins a modest decline. Growth of 3%/yr in non-building infrastructure will be offset by declines in residential buildings and flat nonresidential buildings. Jobs will continue to grow and spread the imbalance even more.

The construction jobs slow down has been in the cards for a long time. With all the talk of skilled labor shortages, there’s been little discussion of the unsustainable excess jobs growth. Maybe it’s about time to change the conversation.

Construction Starts > Cashflow > Backlog > Spending

The path from construction starts to spending is not direct and not quite as simple as you might think. Spending is the market activity measure that drives all construction economics, so that’s where we need to get too. With an appropriate modeling technique we can get from new starts to predicted spending in a few steps.

New Construction Starts (construction starts referred to here is Dodge Data & Analytics New Construction Starts) is excellent data for forecasting. The following forecast is entirely developed from starts data. No actual spending is incorporated into this forecast. The purpose is to show that using the data properly can produce an accurate forecast.

The starts data is a survey. As in any survey, starts represents a portion of new construction activity. Study shows the survey size varies with each market from about 40% to 70% of actual. Starts data captures a share of the total market or a portion of all construction, on average about 60% of all construction.

The easiest way to understand this is to compare total annual construction starts to total annual spending. National construction starts from 2016 to 2019 range from $750 billion/year to $800 billion/year, while spending in this period ranges from $1,200 billion/year to $1,300 billion/year. From this we see starts data captures a share of about 60% of the total construction market.

The total starts survey averages about 60% of the actual market. In this analysis every market is adjusted by its own individual market share factor. The adjusted starts represent the full amount of starts that would generate the full amount of spending.

To predict spending activity from new construction starts, the starts data must be spread over time using appropriate cash flow curves. On average about 20% of new construction starts gets spent within the year started, 50% is spent in the next year and 30% is spent in years three and four. The cash flow curves used in this model are specific to each market type and can vary from the average.

Applying a market survey factor to develop full magnitude of spending and an expected duration for all starts, depending on market type, to produce a forecast cash flow from starts data, the predicted pattern of spending is developed. The factors have been shown to produce a reliable prediction of total future market activity.

Backlog at the beginning of the year or new starts within the year does not give an indication of spending within the year. New starts within the year could contribute spending spread out over several years. Total cash flow in the year, or spending, could include cash flow from projects that started or entered backlog years ago.

Backlog increases if new starts during the year is greater than spending during the year. However, an increase in backlog does not necessarily indicate there will be an increase in market activity. An increase in backlog could represent a level rate of market activity, but for a longer duration.

Cash flow provides the best indicator of how much and when spending will occur. Cash flow from all previous starts gives a prediction of how spending will change monthly from all projects in backlog. Cash flow totals of all jobs can vary considerably from month to month, are not only driven by new jobs starting but also old jobs ending, and are heavily dependent on the type, size and duration of jobs.

Total of all national construction starts increased every year since 2008. New starts slowed to +2% in 2018 and are forecast at a potential decline of 0.2% in 2019. Backlog is still up leading into 2020 but after that starts and backlog are forecast to remain flat or decline over the next few years. Total spending declines in 2022. However, as the next tables will show, work distribution is uneven with residential declining and nonresidential up.

Nonresidential Buildings starts (excluding Terminals) reached a new high every year since 2009. The last three years starts are up 3% to 4% per year. Every market posted increases in 2017 and 2018. Only Commercial/Retail declined in 2019. The largest increases over the last two years were Educational and Office Buildings. Spending is still strong in 2020 but then with the slowdown in starts forecast in 2020, backlog growth stalls and spending slows in 2021-2022.

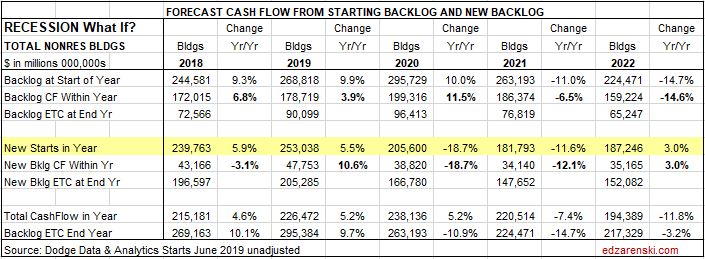

75%-80% of all Nonresidential Buildings spending within the year will be generated from projects that were booked in starting backlog at the beginning of the year.

Nonbuilding Infrastructure markets total spending amounts to only about 70% of nonresidential buildings markets. The largest infrastructure markets are Highway/Bridge and Power but the largest increases in new starts recently are in Transportation (including all terminals) and Environmental Public Works. Transportation starts are up 25% in the last last three years and backlog to start 2020 is up 80%. Public Works starts are up 22% and backlog is up 30%

Nonbuilding Infrastructure starts can be erratic with a long pattern of up then down years. Starts (including Terminals) gained only 2% in 2019 but that is only low because Power, the largest market overall saw starts decline by 7%. Total infrastructure starts are at an all-time high.

Infrastructure backlog peaks in 2020 and remains high into 2021. Spending increases are in the 6% to 8% range at least for the next two years. Infrastructure projects typically have the longest duration. Projects contribute spending sometimes up to 5 or 6 years. The largest spending increases in 2020 are in Transportation and Highway projects.

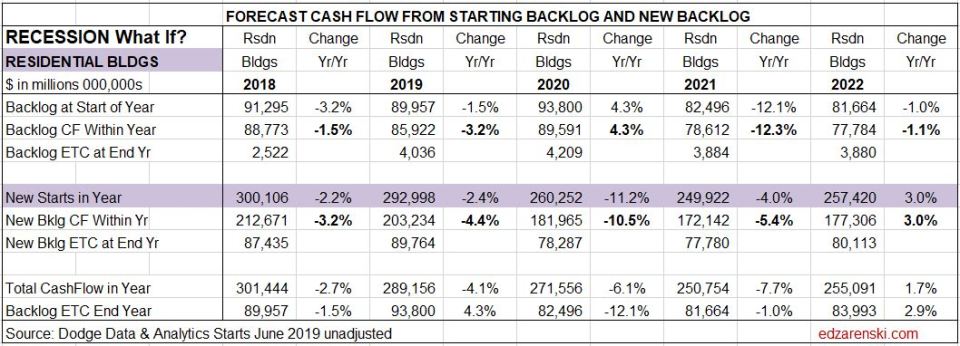

The Residential table shows that most of the spending in any year is cash flow from new starts. For short duration residential spending, single-family residential and renovations work, approximately 75% of the spending occurs in the year of the starts and 20% in the following year.

For long duration residential spending, typical of multifamily residential, approximately 50%-55% of the spending occurs in the year of the start, 35%-40% in the next year and only 5%-10% occurs two years out.

Only 25% (for short duration SF and Reno) to 50% (for longer duration MF) residential spending within the year comes from work that was booked in backlog at the beginning of the year. The performance of residential spending in the year is very much dependent on new starts.

The level of activity has a direct impact on inflation. When the activity level is low, contractors are all competing for a smaller amount of work and therefore they may reduce bids. When activity is high, there is a greater opportunity to bid on more work and bids can be higher.

Residential construction saw a slowdown in inflation to only +3.5% in 2015. However, the average inflation for six years from 2013 to 2018 was 5.5%. It peaked at 8% in 2013. Residential construction spending dropped an unexpected 6% in 2019 and after adjusting for inflation that is a 10% decline in construction volume. Typically, large declines in volume are accompanied by declines in inflation. National average residential construction inflation for 2019 is now at 3.8%. 2020 is forecast at 3.75%.

Nonresidential Buildings indices have averaged 4.4% over the last five years and have reached over 5% in the last three years. But spending slowed dramatically in 2019. This forecast indicates spending in most nonresidential buildings markets will gain little in 2019, the slowest rate of growth post-recession. However, new starts in 2018 and 2019 boosted backlog and 2020 spending will post the strongest gains in four years. Strong gains in spending historically has led to accelerated inflation. National average nonresidential buildings construction inflation for 2019 is now at 4.8%. 2020 is forecast at 4.2%.

Construction Statistics – Behind The Headlines

Examples of how commonly reported construction data can often be misused – Construction Spending and Construction Starts

Construction Grew $41 billion, 3.3%, from 2017 to 2018

An increase in construction spending is often referred to as growth for the industry, but that is incorrect. Construction spending measures the change in the dollar value of work performed, not the volume of work performed.

The difference between spending (or revenue) and volume can be explained by a simple example, the Crate of Apples. A farm stand sold a crate of apples last year for $100. Costs have gone up. Today the same size crate of apples sells for $110. Farm stand revenues increased 10%, but the amount of business volume did not increase. Volume of sales is still one crate of apples. All the increase in revenue was inflation.

The $41 billion increase in construction spending from $1.266 trillion in 2017 to $1.307 trillion in 2018 is a 3.3% increase. However, construction inflation for that period averaged 4.7%. Construction inflation adds only cost, not volume, to the amount of work. Construction spending is measured in current dollars, actual dollars spent within the year in the value that year. Construction volume is measured in constant dollars, adjusted for inflation, so any and all years can be compared to each other.

Real construction volume adjusted for inflation actually decreased 1.4% from 2017 to 2018.

Total Construction volume, after accounting for inflation, has been down for five of the last six quarters. Construction volume peaked from Q1 2017 to Q1 2018, is now down 6% from the 2018 peak.

Construction volume is not directly reported. It is not a commonly referenced industry measure reported in the news. But it is a more important indicator of activity in the industry than spending. Volume is found only through analysis of spending and inflation data.

Another common misrepresentation using spending data relates to jobs growth. Jobs growth is often compared to spending growth where a 3% to 4% increase in jobs from year to year is substantiated if we have a similar 3% to 4% growth in spending. However, current $ spending is not yet adjusted for inflation and does not represent growth in real volume of work. Jobs must be compared to volume. Real volume increases are represented by constant $, or construction spending adjusted for inflation.

In the last 2 years jobs have increased by about 8% but real construction volume has decreased by about 6%. In recent years, construction volume has not supported jobs growth.

Construction Starts Predict Changes in Spending

Two very important criteria must be known about new construction starts in order to properly predict spending.

1st – To predict spending from new starts, the starts data must be spread over time using an appropriate cash flow curve. A simple illustrative spending pattern for nonresidential buildings starts, or a typical cash flow curve, for total starts within a year is: 20% of the revenue gets spent in the 1st year, 50% in the 2nd year and 30% in the 3rd year. This shows predicting spending in any given year is dependent on several previous years of starts.

Multi-billion $ highway projects, manufacturing facilities, power projects and transportation terminals often have much longer duration cash flow curves. In other words, if your intent is to predict construction spending in 2019, you need to know what starts were at a minimum in 2017 and 2018, and in many cases back to 2016 or even 2015.

Starts spread over time with cash flow curves predict spending.

2nd – For new construction starts survey sample to be used to compare to itself from year to year to predict growth in spending, sample size must be known. Starts data captures a share of the total market or a portion of all construction, on average about 60% of all construction. The easiest way to see this is compare total construction starts to total spending. Starts from 2016 to 2019 range from $750 billion to $800 billion while spending in those years ranges from $1,200 billion to $1,300 billion. From this we see starts capture a share of the total market. Any time a survey of a total population is used to forecast the total, the survey share of total must be considered. If sample size is not constant, the apparent growth in starts does not all reflect real growth in spending.

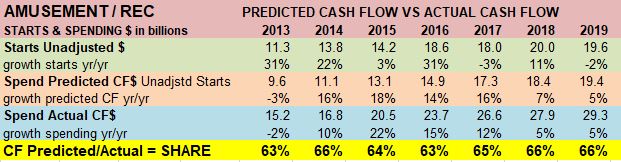

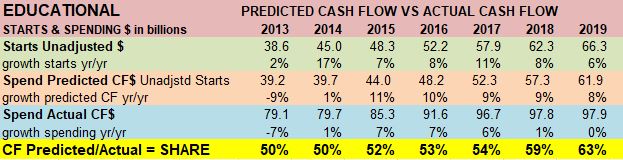

Amusement/Recreation is an example that shows starts that generate a predicted cash flow pretty well balanced with actual spending from year to year. The share of starts in the survey is fairly consistent never varying from 63% to 66% from year to year.

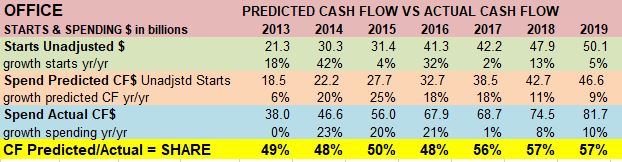

Office provides an example of variation in sample share of total. Starts generate predicted cash flow that increased substantially from 49% to 57% and remained higher compared to actual spending.

Office starts increased from $21 billion in 2013 to $50 billion in 2019. This data generates the predicted cash flow that is compared to actual spending. To predict total spending from unadjusted starts, unadjusted starts CF$ are factored up (divided by) share of total market. If the share of market captured in the survey remained constant then the predicted spending would remain close to 50%.

CF$ Predicted/Actual shows that Cash Flow Share of actual spending was 48%-50% for several years but then jumped to 56%-57%. The predicted cash flow generated from the increase in starts is not entirely representative of an increase in spending but represents the combined value of the expected increase in spending and an increase in share of market data captured.

Starts cash flow and starts survey share of total spending are never directly known or published. These factors are found only through analysis of the data.

The Educational market data shows a similar situation as Office data. Starts generate predicted cash flow that increased substantially compared to actual spending.

Starts data generate predicted cash flow to forecast spending. This requires tracking share of total market captured in the starts survey data to account for any growth in the market share captured vs growth in predicted spending.

Prelim 2019-2020 Construction Spending

Note 11-8-19 on September spending: Construction Spending in September is up 0.5% from August and still down 2.2% year-to-date (ytd) from 2018. Spending in Q3 averaged the same as Q1. Qtr/Qtr spending this year has ranged +/- 1%. Total 2019 spending will be down 1%. I’m expecting 2019 Nonresidential Buildings spending up less than 1%, Non-building Infrastructure up 7% and Residential spending down 6%.

10-3-19

Construction Spending in August is down slightly from July and down 2.3% year-to-date (ytd) from 2018. Spending for the last three months has remained flat. Qtr/Qtr spending has ranged +/- 2% for the last five quarters. Total 2019 spending will be down 0.5%. I’m expecting 2019 Nonresidential Buildings spending up 1%, Non-building Infrastructure up 8% and Residential spending down 6%.

Residential construction spending, down for six consecutive quarters, is now down 11% from Q1 2018. Residential volume (spending minus inflation), also down for six quarters, is down 16% from the Q1 2018 peak.

Some markets spending totals for 2019: Lodging +11%, Office +10%, Amusement and Healthcare both +5%, Commercial/Retail -14%, Highway +11%, Power +7%, Transportation +6%, Environmental Public Works (combined) +12%.

2020 forecast Starting Backlog for Nonresidential Buildings is currently up 6% and for Non-building Infrastructure is up 9%. Strong backlog leading into 2020 will increase spending in most nonresidential markets. Exceptions are: Commercial/Retail and Power backlog will decline. Residential spending is 65% dependent on new starts but Nonresidential spending is 80% dependent on backlog.

Forecast growth for 2020 is welcome since real construction volume, after accounting for 4% to 5% inflation, has been down for five of the last six quarters. Annual construction inflation since 2011 has been as high as 5.8%. For the last 3 yrs it has averaged 4.6%/yr. Construction spending for the last 3 years avg. annual growth is only 2.4%. When construction spending is lower than inflation, real volume is declining. Jobs must be compared to volume.

Total construction volume after inflation (quarterly avg) reached a peak in the 1st quarter of 2017 (which was then matched again in Q1 2018) and is now down 6% from the peak. Most of the volume decline was in Residential. Only Infrastructure has seen volume gains in the last two years. We have seen jobs growth slow in the last year, but the disparity between construction volume and jobs growth is the greatest ever. I expect to see a much more significant slow down in jobs growth.

Backlog growth over the past two years will provide the base for Nonresidential construction spending increases in 2020. Major backlog increases from 2018 to the start of 2020 are: Educational +12%, Office +25%, Commercial/Retail -14%, Highway +16%, Transportation +45% and Environmental +23%.

The forecast for 2020 spending is total $ up 3%, but Residential spending will be flat to down slightly.

Construction Spending Forecast strength over the next 18 months is all nonresidential. Current spending seasonally adjusted annual rate (SAAR) vs SAAR at the end 2020 shows Nonresidential Buildings now at $450bil will end 2020 at $500bil and Non-building Infrastructure, now at $340 billion, will end 2020 at $375bil. Residential is now at $510bil but will move up slightly then down to finish 2020 at $500bil.

SEE ALSO:

Spending Revisions 9-3-19. Nonresidential Increases. Residential Slows.

Midyear 2019 Construction Spending Forecasts Compared

Spending Revisions 9-3-19. Nonresidential Increases. Residential Slows.

Census Construction Spending released today revises data back to Jan 2013. 2018 spending was revised up by $13bil or 1% to $1.307 trillion. I expected upward revisions to 2018 residential that did NOT materialize. Almost all revision is to nonresidential.

Sizable upward revisions were posted to nonresidential buildings and non-building infrastructure for 2015, 2016 and 2017. Educational increased by $5.5bil in 2017 and Manufacturing by $4.3bil. Manufacturing also increased in 2015 and 2016. Power increased by 8%-10% in both 2015 and 2016 but decreased by 8% in 2018.

Nonresidential revisions added $15 to $20 billion in 2015, 2016 and 2017. This helps explain what would be excess growth in labor over this period, absorbing about 100,000 jobs.

It is unusual there were no sizable revisions to residential, the first I can ever remember there being no revisions to residential spending totals. It is not uncommon to see $10-$15 billion/year revisions to past years in residential. In this release, there were no annual revisions greater than $1 billion. However, for 2018, renovations was revised down by $4bil and single-family up by the same $4bil. I wouldn’t be surprised if all years 2013-2018 get revised next year. Typical annual revision is about +2.5%.

Biggest 2018 revisions: Commercial +$6bil, +6.6%; Educational +$3.5bil, +3.7%; Amusement/Rec +$1.5bil, +5.3%; Power -$7bil, -7%; Sewage $1.9bil, +8.5%; Water Supply +$1.5bil, +10.8%; Manufacturing +$5.6bil, +8.7%.

Biggest 2017 revisions: Educational +$5bil, +6%; Amusement/Rec +$1.7bil, +6.8%; Manufacturing +$4.3bil, +6.5%. Public Works +$5bil, +13%.

After revisions, 2018 construction spending growth was up (2.7% to 4.4%) in all sectors but still less than the increase in inflation (4% to 5%), so real market activity declined in all sectors. Average spending for 2018 was up 3.3%, but average construction inflation in 2018 was 4.8%, so real volume decreased by 1.6%.

Real market growth declined in all three major market sectors, Residential, Nonresidential Buildings and Non-building Infrastructure, however, performance varies by market. For example, in the Nonresidential Buildings sector, Educational, Healthcare and Manufacturing markets (almost 50% of the Nonres Bldgs sector) spending increased only 1% or less. With an average Nonres Bldgs Inflation rate of 5.1%, real volume in these three markets declined 4% to 5%. But Lodging, Office and Commercial markets spending increased 8% to 10%. After subtracting 5.1% inflation, real volume in these markets increased 3% to 5%.

For the Nonresidential Buildings sector, spending in 2018 increased by 4.4%, but nonres bldgs average inflation was 5.1% (i.e., Construction Analytics 5.1%, Turner 5.6%, RLB 4.6%, Mortenson 7.4%, PPI Bldgs 4.0% ). On average, nonres bldgs real volume in 2018 declined by 0.7%.

For the Residential Buildings sector, spending in 2018 increased by 2.7%, but res bldgs average inflation was 4.3%. On average, residential bldgs real volume in 2018 declined by 1.6%.

For the Non-building Infrastructure sector, spending in 2018 increased by 2.7%, but non-bldg infra average inflation was 5.6% (i.e., Highway 6.7%. Powerplants 3.2%, Pipelines 2.1%). On average, non-building infrastructure real volume in 2018 declined by 1.6%.

In 5 years from Jan 2011 through Dec 2015, total construction spending increased 40% but after inflation volume increased only 22%. Jobs adjusted for hours worked increased 21%, almost in balance. However, in the following 3 years from Jan 2016 through Dec 2018, spending increased 16%, but after 13% inflation, volume increased only 3%. Jobs adjusted for hours worked increased 12% during that 3-year period. Starting 2011, jobs exceeded work volume. At the end of 2018, the jobs/work volume imbalance was even greater.

Residential spending 2018 did get some monthly revisions, but the total was NOT revised up and unusual monthly variances were not revised away. This leaves 2018 with four months in which the spending varied from the statistical monthly average by more than 3 Std Dev. There are no other years outside of the 2006-2009 residential recession in which there were ANY monthly variances from statistical average reaching 3 Std Dev. For 60 months 2013-2017 the largest variance was 1.8 Std Dev.

Residential construction spending in 2018 looks more like the 2006-2009 recession than any growth years from 2001 to 2019. After the Feb 2018 high, spending declined in seven of the next ten months, then in 2019 declined in four of the next six months.

Residential construction spending declined in the last five consecutive quarters. The most recent quarter averaged $510 billion. The post-recession high was reached in Q1 2018 at $575 billion. Q2 2019 is down 10% from Q1 2018. July 2019 is down 12% from the Feb 2018 high.

Residential spending is forecast to increase through the end of 2019 but then is expected to decline in the 1st half 2020. The low by mid 2020 could match the current low of $510 billion. That would result in 7 out of 9 declining quarters.

Census doesn’t show the Renovations line item. Reno = (Total Rsdn minus SF+MF) is where the biggest residential declines occurred in 2018, down -$4bil, -2.3%. Residential Reno is down 13% in 2019 YTD.

WHAT IF? Construction Recession 2020

8-15-19

Talk these days isn’t whether or not we may slip into another recession, but when. Analysts are watching for signals. On any given day you can read articles pointing to why we are or why we are not headed into another recession. But, I wrote an article similar to this 3 years ago, so that opinion has been around awhile. I’m not taking a position here. I would just like to get a rough idea of implications, so I tested some data.

What would happen to this current construction recovery if we slip into recession?

If you think of a recession as having an immediate affect on total construction, like a quick drop in materials prices or cost of buildings, think again. Construction is sort of like an aircraft carrier, it takes a long time to turn around.

My starting baseline is my current construction spending and backlog forecast for 2019-2020 which includes YTD Spending and Starts through June. All spending and starts are current$, unadjusted for inflation. There is considerable strength in Nonresidential Buildings and Non-building Infrastructure starts and spending. There is weakness in residential.

NORMAL FORECAST current to Jul 2019 with no modifications

NORMAL FORECAST spending plots for the next 18 months.

Recession What If? Starting Point

The best indicator of future construction activity is the projected cash flow generated by all the construction starts that have been recorded. Construction starts mark the beginning of spending on new projects. Projects can take many months to reach completion, and the cash flow varies over the project time.

For the 2020 forecast, we can look at new starts and backlog.

Construction Starts YTD total as of June is down 8% from 2018. That’s expected to improve by year end.

Residential construction starts peaked in 2018. Starts have been sideways or in light decline since mid-2018. Year-to-date June 2019 starts are down 9% from 2018. Avg SAAR for 1st 6mo 2019 is $315bil, same 6mo last year was $340bil. Starting backlog is down 5% from 2017 to 2019. Spending is forecast down 5% in 2019 and up only 1% in 2020.

Nonresidential Buildings starting backlog increased 10%/year for the 4 years 2017-2020. Prior to this recession scenario analysis, nonresidential buildings spending was forecast up 10% in 2020 and 6% in 2021.

Infrastructure starting backlog has increased 15%/year for the 3 years 2018-2020. Prior to this recession scenario analysis, non-building infrastructure spending was forecast up 12% in 2020 and 8% in 2021.

For nonresidential buildings, 80% of all spending in any given year is already in backlog from starts prior to that year. For non-building infrastructure it’s 85%. Starting Jan. 1, 2020, 80% to 85% of all nonresidential spending in 2020 is already on record in backlog. For residential, only 30% of spending in 2020 is in backlog at the start of the year. Due to shorter duration, spending is more dependent on new starts within the year.

Backlog starting 2020 for the following six markets is at the highest starting backlog ever for each of the six markets. Also, these six markets account for 1/3rd of all construction spending. Much of the spending from these starts occurs in 2020.

These markets posted the best construction starts 12-month totals ever (in noted period).

- Manufacturing from Jun18>May19, up 36% in two years

- Office May18>Apr19, up 8%/yr for the last 4 years

- Educational Jun18>May19, monthly rate for 12 of the last 16 months increased by 20%.

- Public Works May18>Apr19, increased 30% in the last 24 months.

These very long duration markets posted best new starts ever.

- Highway Dec 17>Nov18, up 25% compared to prior 12 months, which was the 2nd best 12mo ever, with peak spending from those starts expected in 2020.

- Transportation (2yrs) Jan17>Dec18, up 25% from the prior 2 years, but with the peak 12 months up 35% from the prior 2 years, with peak spending 2020.

Growth in new starts and backlog for the last three years (2017-2018-2019):

- Manufacturing starts up 44%, backlog up 62%

- Office starts up 30%, backlog up 62%

- Highway starts up 45%, backlog up 70%;

- Transportation starts up 64%, backlog up 138%;

- Public Works new starts up 45%, backlog up 72%.

In the last two years, Commercial/Retail market starts are down 18% and 2020 starting backlog will be down 11%. The only other declines in 2020 starting backlog are Amusement/Recreation (-1%) and Power (-5%).

So, we are starting 2020 with the highest backlog on record after several years of elevated starts. However residential work is already down slightly while non-building infrastructure work is super-elevated. It is this elevated backlog that will mute the impact of a recessionary downturn.

What If? we reduce new starts

If a recession were to occur, it would substantially reduce future construction starts. Most, if not all, projects already started would move on to completion, but new starts will be cut back. However, the last “construction” recession started in 2006-2007 with declines in residential work. New starts in nonresidential buildings kept increasing into 2008. The “nonresidential” spending recession did not start until 2009, three years after the beginning of the residential decline.

To get an idea how another recession might affect construction spending, I kept all backlog growth predicted through 2019, but I reduced future new construction starts, for two years, starting Jan 2020. I’ve started the reductions for all sectors at Jan. 1, 2020 because residential starts and spending have already been in decline for more than a year.

- Residential starts reduced by 15% in 2020 and by 5% more in 2021

- Nonresidential buildings reduced by 20% in 2020 and by 10% more in 2021

- Infrastructure projects reduced by 10% in 2020 and by 5% more in 2021

This is only about 20% of the residential declines we experienced from 2006 to 2009, but I’m not anticipating another residential massacre. Residential has already been in decline for 12 months. The nonresidential buildings decline now is only half of 2008-2010. I reduced infrastructure by the least since there was only moderate decline in infrastructure work in 2009-2010, yet still I’ve reduced infrastructure twice as much as 2009-1010. I allowed for a 3% increase in new starts in 2022 across buildings sectors and a 2% increase in infrastructure.

The Recession Scenario Results

The recession 2020 scenario keeps 2019 forecast intact and reduces new starts by 15%-20% in 2020 and 5%-10% in 2021, so imparts a two year downturn. It’s effects, begun Jan.1, 2020 could be translated over time, if say the same scenario started but 12 months later. Negative reaction in the market is quickest to happen for residential, delayed a year for nonres buildings and takes longest (2 years) for infrastructure, for reasons of longest duration type work and highest prior rate of backlog growth.

The recession affects are muted by the fortunate starting point of record high backlog. Residential construction spending will experience two to three declining quarters each of the next three years. But beyond Jun 2022, residential stabilizes and resumes growth. Residential is the only sector to post quarterly spending declines in 2020. Nonresidential buildings posts the 1st quarterly decline in Q1 2021 and has at least seven consecutive quarters of declines before flattening out in Q4 2022. Non-building Infrastructure experiences the 1st two consecutive quarters of decline starting Q4 2021 and reaches a low in Q4 2022. Due to the unevenness of growth, Total Construction spending increases through Q1 2020, posts two declining quarters in 2020 and three consecutive quarters of declines in each of 2021 and 2022.

RECESSION FORECAST spending plots for the next 30 months.

Here’s a reminder of the amount of reductions in new starts. I kept all backlog growth predicted through 2019, but I reduced future new construction starts, starting Jan 2020. I’ve started the reductions for all sectors at Jan. 1, 2020 because residential starts and spending have already been in decline for more than a year.

- Residential starts reduced by 15% in 2020 and by 5% more in 2021

- Nonresidential buildings reduced by 20% in 2020 and by 10% more in 2021

- Infrastructure projects reduced by 10% in 2020 and by 5% more in 2021

We still see an 11% increase in backlog in 2020, because we did not reduce 2019 starts, but spending from reduced new starts in 2020 drops 2020 cash flow within the year to slow growth of 2%. Reference the baseline spending chart to see prior to reducing starts 2020 spending was forecast to increase 7%. Backlog drops 7% in 2021 and then 11% in 2022. This model predicts a 4% decline in construction spending in 2021 (baseline was +3%) and a 5% drop in 2022 (baseline was -1%), setting us back to the level 2016-2017.

Starting Backlog is down 4.4% for 2023, but even modest new starts growth of 3% helps partially offset the decline in spending. Spending never drops below the level posted in 2015-2016.

The last recession started with residential in 2005 and ended with nonresidential in 2011. Total decline during that period set total spending back 12 years, although the setback was 15 years for residential, 7 years for nonresidential buildings and only 4 years for infrastructure. This mild recession causes a setback to 2015-2016 levels, back 6 years, and less for infrastructure.

RECESSION FORECAST current to Jul 2019 with reduced starts 2020-2021

Residential construction would drop about 6% in 2020 and then drop another 8% in 2021. Residential is far more dependent on new starts within the year for spending than on backlog. That’s why residential spending drops quicker than all other work.

Nonresidential buildings gain 5% in 2020 but then drop 6% in 2021 and 12% in 2022. The strength of backlog going into 2020 pushes most of the declines out to 2021 and 2022.

Non-building Infrastructure has so much work in backlog that this sector still posts spending gains in 2020 and 2021. It drops 8% in 2022. The strength of backlog going into 2020 pushes much of the declines out 2022.

The baseline forecast would have produced spending increases of 9% from 2020-2022. The recession scenario indicates a 7% decline. That magnitude of turn around would impact the jobs situation. We would probably not see any reduction in workforce in 2020 but the spending declines in 2021 and 2022 could lead to a temporary loss of about 200,000 jobs in 2021 and 300,000 jobs in 2022.

Educational 2019 spending is supported by a steady stream of strong starts that began in late 2017 and extended into summer 2018. Jun-Jul-Aug 2018 starts posted the best 3mo total starts ever and peak spending from those starts occurs from April 2019 to Jan 2020. Most spending in 2020 comes from projects that start in the 1st half of 2019. So far in 2019 starts are up 15% ytd over 2018.

Commercial Both store and warehouse starts dropped in 2018. Commercial starts are seeing strong gains from distribution centers (warehouses, which are in commercial spending). Since 2015 the 10% decline in retail stores is being hidden by the 50% increase in warehouses, which are at an all-time high. Stores are down 10% from the peak in 2016. Warehouses are down 5% in 2018 but increased 500% from 2010 to 2017.

Manufacturing Backlog is still very strong, but a drop in peak spending from the schedule of cash flows will lead to a period of moderate spending declines. After that, manufacturing spending increases steadily through the end of 2020. Current expectations are that manufacturing will finish the year up 8%. 2020 will be an extremely strong growth year, spending potentially increasing 20%+. Reductions in starts won’t show up as negative spending until 2022.

Office spending is expected to finish 2019 up 7% or less. New starts in 2018 were up 11% to a new high, but much of the peak spending, from over-sized long-duration projects, will benefit 2020 when I expect to see spending growth of 8%-11%.

Transportation starts have two main parts, Terminals and Rail. Some analysts include transportation in nonresidential buildings. That does not consider the following: airports include not only land-side terminals but also air-side runway work; rail includes platforms and all railway right of way work, which includes massive civil engineering structures. About half of all transportation spending is rail work. Construction Analytics follows U S Census construction spending reports which include all terminals and rail in Transportation.

Terminals and rail starts reached record highs in 2017 and record backlog in 2019. 2019 starting backlog is four times what it was in 2015.

However, much of that backlog is very long duration project spending that will occur in future years. Some of the project starts in 2016 and 2017 have an eight-year duration. From Oct’16 through Oct’18 there were sixteen $billion+ new project starts and seven $500million+ new starts. Some projects started in this period have peak spending occurring in 2020 and 2021.

Highway/Street/Bridge starts hit an all-time high in 2018. Current 2019 progress shows new starts leveling off. Starting backlog increased 70% in the last 3 years leading into 2020. A lot of this is long duration backlog that will provide for large increases in spending in from 2019 to 2021.

Environmental Public Works (Sewage, Water supply and Conservation) new starts all declined from 2014 through 2017. Then all showed 14% gains in 2018 and the forecast is +15% in new starts in 2019.