Home » 2020

Yearly Archives: 2020

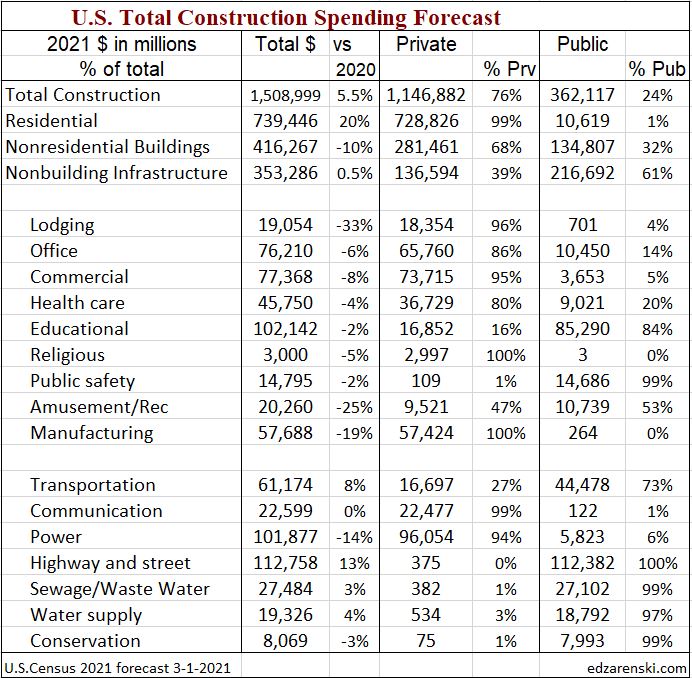

Public/Private Construction Spending Forecast 2020-2021

12-18-20

Public Starts and Backlog

Leading into 2020, the Public markets with the highest growth in new starts the previous two years were Transportation and Public Works. Transportation terminals and rail starts were up 15% over two years, 25% in the last three years. Backlog nearly doubled in three years because a large portion of those starts is very long duration projects. Public works starts were up 13%, 20% in three years, and backlog is up 40%. Infrastructure projects typically have the longest duration. Projects contribute spending sometimes up to 5 or 6 years.

Public work backlog leading into 2020 was up an average 8%/year for the last three years. Some of this is very long-term work that started construction in 2017 and it will still contribute spending for the next several years. 40% of all public spending in 2020 comes from projects that started prior to Jan 2019.

2020 losses in new construction starts impact the forecast for the next few years. Total new starts in 2020 for Public work dropped 9%. Transportation starts fell 20%, Educational starts fell 11% and Public works fell 6%. Amusement/Recreation starts fell 40%. Highway/Bridge starts increased 4%.

2021 Starting Backlog for all Public work is down 5%. Backlog for Transportation projects drops only 4%, and that leaves 2021 still 2nd only to the all-time high in 2020. Both Educational and Public Works backlogs drop 7%. Amusement/Recreation backlog falls 40%. Highway backlog increases 3%. Of all public work in backlog at the start of 2021, 43% comes from projects that started prior to Jan 2020.

Public Spending

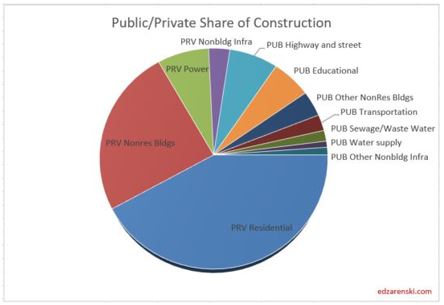

The two largest markets contributing to public spending are Highway/Bridge (30% of total public spending) and Educational (25%), together accounting for 55% of all public construction spending. At #3, Transportation is only 12% of public spending. Environmental Public Works combined makes up 15% of public spending, but that consists of three markets, Sewage/Wastewater, Water Supply and Conservation. Office, Healthcare, Public Safety and Amusement/Recreation account for about 3% to 4% each.

Highway is 100% public and Public Works 98%. Educational is 80% public, Transportation 70%, Amusement/Rec 50% and Healthcare 20%.

Total public spending for 2020 is projected to finished up 5% at $350 billion. Spending for every major public market is projected to finish up in 2020. By far, the largest Public spending increases measured in dollars for 2020 are Educational, Transportation and Public Safety.

Total public spending in 2021 is projected to finished up 5% at $370 billion. Transportation provides most of the gains in 2021 and Public Works adds some, but this forecast may come down without support from Highway or Educational.

Public Infrastructure and Public Institutional

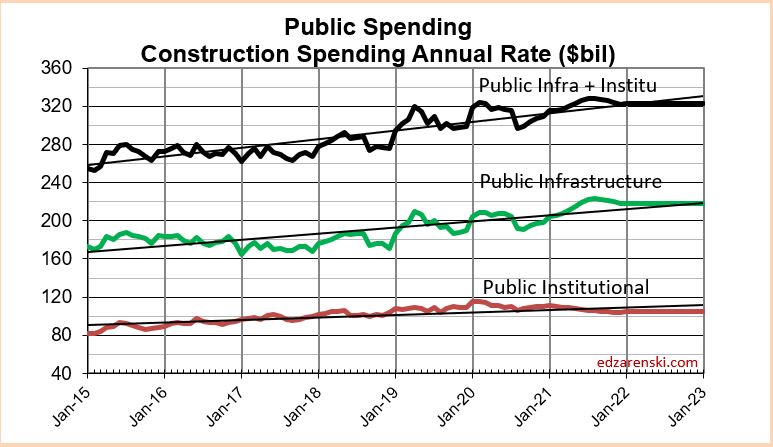

A bit less than 60% of all Non-building Infrastructure spending, $198 billion in 2020, is publicly funded. That public subset of work has averaged growth of $5 billion/year from 2013 through 2019, with maximum growth of $16 billion in 2019. 2020 increased only $4 billion. In 2020, Non-Building Infrastructure spending makes up about 60% of Public spending.

About 30% of all Nonresidential Buildings spending, $141 billion in 2020, is publicly funded. It’s mostly Educational. That public subset of work has averaged growth of $6 billion/year from 2013 through 2019, with maximum growth of $10 billion in 2017. 2020 increased $14 billion. In 2020, Nonresidential Buildings spending makes up about 40% of Public spending.

- Infrastructure = $349 billion, ~25% of all construction spending.

- Infrastructure is about 57% public, 43% private. In 2005 it was 70% public.

- Public Infrastructure = $198 billion. Private Infrastructure = $150 billion.

- Power and Communications are mostly privately funded infrastructure.

- Nonresidential Buildings is 30% public (mostly institutional), 70% private.

- Educational, Healthcare and Public Safety are Public Nonres Institutional Bldgs

- Public Commercial construction and Amusement/Rec. are not included.

- Public Institutional = $110 billion, mostly Education ($86b).

Public Infrastructure + Public Institutional = $308 billion, 22% of total spending.

Public Infrastructure + Institutional average growth is $12 billion/year. This subset has never exceeded $30 billion in growth in a single year. In 2019 spending increased $20 billion. With 10 months data posted, 2020 is forecast to increase $17 billion.

Although total all public spending may increase for 2021, the select group of Infrastructure + Institutional likely to be funded by an Infrastructure stimulus bill shows 2021 growth is uncertain and may remain flat.

See Also

Down the Infrastructure Rabbit Hole

Infrastructure – Ramping Up to Add $1 trillion

Pandemic Impact on Construction, Dec. 2020

12-15-20

By far the greatest impact of the pandemic on construction is the massive reduction in new nonresidential construction starts in 2020 that will reduce construction spending and jobs for at least the next two years.

In the Great Recession, beginning in Q4 2008, nonresidential buildings new construction starts fell 5%, then fell 31% in 2009 and 4% in 2010. Spending began to drop by Dec 2008, then dropped steadily for the next 24 months. Spending dropped 40% over that next two years. During that period, residential starts and spending fell 70%.

In 2020, nonresidential buildings starts fell 24%, but the six months from Apr-Sep, starts fell 33%. Starts are forecast to fall 4% in 2021. Nonres Bldgs spending began to decline in Aug, is now down 10% from Feb high and is forecast to drop steadily the next 20 months, for a total decline of 25%. This time around residential starts and spending are increasing.

The measure of decline due to Pandemic delays and shutdowns is not the difference between Q3 vs Q1 growth or spending. Nor is the impact measured by the current difference in ytd performance vs 2019. The measure of decline due to Pandemic delays and shutdowns is the difference between what was forecast for growth pre-pandemic vs actual growth.

New construction starts projected for 2020:

- Total 2020 Construction Starts now forecast down -11%, pre-pandemic forecast was up 2%

- Nonresidential buildings now down -22%, pre-pandemic forecast was up 1%

- Non-building infrastructure now down -15%, pre-pandemic was up 2%

- Residential new starts now up 1%, pre-pandemic was up 2.5%.

New starts for 2021 were originally forecast up 1.5% to 2% in all sectors. The current 2021 forecast shows residential up 4.5%, nonresidential buildings up 4.6% and non-building infrastructure up 11%. Residential is already at a new high, but nonresidential buildings and non-building infrastructure will still be lower than 2018.

Future impact from delays/cancellations and reduced starts

Total construction starts year-to-date for 10 months through October are now down only -11% from 2019 ytd. Total starts had been down -14% to -15% ytd for the previous four months. Nonresidential buildings starts are down -24% ytd and non-building infrastructure starts are down -14% ytd. Residential starts are now up ytd +2% from 2019.

The most recent four months total residential starts, Jul-Aug-Sep-Oct’20, posted the highest 4mo total since 2005. The next highest 4mo total since 2005 was for the period Nov-Dec’19-Jan-Feb’20. So, the two best 4mo periods of new residential construction starts in the last 15 years have occurred in 2020. In August, residential starts posted an all-time high. Much of the spending from these starts carries into 2021 and supports residential spending growth in 2021.

The following table shows, for each market, the current forecast for new construction starts. With exception of residential, spending in all other markets, due to longer schedules, is most affected by a decline in new starts, not in the year of the start, but in years following. Some effects of reduced starts have not even begun to show up in the data. A 20% decline in new nonresidential starts in 2020 results in a huge decline in spending and jobs in 2021-2022. Residential spending hit bottom in May 2020 and ultimately will post an increase in 2020. Nonresidential Buildings spending will not hit bottom until 2022.

Dodge updated their Outlook to show 2020 construction starts for nonresidential buildings fall on average 20%, less in some markets, but -30% to -40% in a few markets. Only warehouses is up. Non-building starts fall on average 15%. Only Highway/Bridges is up. Residential starts may post an unexpected gain in 2020 and are forecast to climb 4.5% in 2021.

Starts lead to spending, but that spending is spread out over time. An average spending curve for nonresidential buildings is 20:50:30 over three years. Only about 20% of new starts gets spent in the year they started. 50% gets spent in the next year. The effect of new starts does not show up immediately. If new nonresidential buildings starts in 2020 are down 22%, the affect that has on 2020 is reduced spending by -22% x 20% = – 4.4%. The affect it has on 2021 is -22% x 50% = -11%. In 2022-2023 the affect is -22% x 30% = -6.6%.

Many nonresidential buildings have durations that last 24 to 36 months, with peak spending 12 to 18 months from now. With the 22% drop in new starts this year, that peak spending 12 to 18 months from now will be impacted negatively. Some nonbuilding markets have project durations that go out 5 or 6 years, so the impact of a decline in 2020 starts may be felt at least until 2025.

Starting Backlog

Starting backlog is the estimate to complete (in this analysis taken at Jan 1) for all projects currently under contract. The last time starting backlog decreased was 2011.

Backlog leading into 2020 was at all-time high, up 30% in the last 4 years. Prior to the pandemic, 2020 starting backlog was forecast UP +5.5%. Due to cancelations, that has been retroactively reduced to +2.7%.

Starting backlog pre-pandemic forecast for 2021 was UP +0.3%. Due to fewer new starts in 2020, that has now been reduced to -10.6%. By far, the greatest impact is due to nonresidential buildings for which backlog declined by 17%.

If construction starts in 2020 do not outperform 2020 construction spending, then 2021 starting backlog will be lower than 2020. My current forecast (2020 starts down -10.7%) indicates 2021 starting backlog will be down by -10%. Spending declines into 2021 and remains depressed through 2023.

80% of all nonresidential spending in any given year is from backlog and could be supported by jobs that started last year or 3 to 4 years ago. Residential spending is far more dependent on new starts than backlog. Only about 30% of residential spending comes from backlog and 70% from new starts.

Some of the projects delayed or canceled started before Jan. 2020. When one of those projects is delayed, the portion of the project delayed gets shifted and remains in future backlog longer. When one of those projects is canceled, the portion of the project not yet put-in-place gets removed from 2020 and future backlog. Not only does that reduce future backlog but also that retroactively reduces the backlog that was on record at the start of 2020. Therefore, 2020 backlog is reduced by cancelations and future backlog is increased by delays, but reduced by cancellations and a loss of new construction starts.

Future impact on Backlog from delays/cancellations and reduced starts

Projects in starting backlog could have started last month or last year or several years ago. Many projects in backlog extend out several years in the schedule to support future spending. Current backlog at the start of 2020 would still contribute some spending for the next 6 years until all the projects in backlog are completed.

Total starting backlog will fall -11% for 2021 and -4% for 2022. Due to new starts declining by 22% in 2020, Nonresidential buildings backlog drops -17% for 2021 and drops -7% for 2022. For non-building infrastructure, a drop of 15% in 2020 starts results in a drop of 8.7% in 2021 starting backlog.

Reductions in starts and starting backlog lead to lower spending. Residential construction is going counter to the trend and will post positive results for new starts, backlog and spending for the next two years. Nonresidential buildings will experience the greatest reductions in new starts, backlog and spending through 2022.

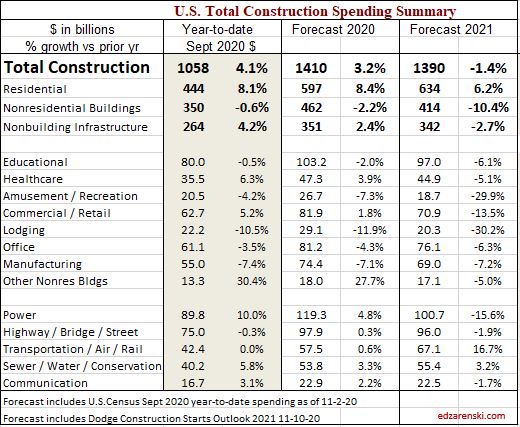

The next table shows spending year-to-date (ytd) through October (released 12-1-20) along with spending forecast for the year. 2nd quarter construction spending activity low-point was down only 5.5% from the Feb peak. Construction spending through October ytd is up 4.3% with Residential ytd up almost 10%.

Almost every market has a weaker spending outlook in 2021 than in 2020, because of lower starts in 2020. Although starts are forecast down -15% to -20% in 2020 and then up +5% to +15% in 2021, the drop in starts in 2020 has the greatest impact on reducing spending in 2021. Most of the reduced spending impact from the lost starts is felt in the future, when those lost projects would have been reaching peak activity at the midpoint of construction. Nonresidential buildings starts in 2020, now down 28% the last seven months. Lowpoint of spending from lost 2020 starts is late 2021- early 2022.

Residential spending looks stable heading into 2021, Nonresidential Buildings spending drops -2% to -3% each quarter in 2021. By Q4 2021, nonresidential buildings spending is down 15% from Feb 2020. When looking at Total Construction Spending for 2021, residential growth obscures the huge declines in nonresidential.

YTD spending for Nonresidential Buildings is currently -1.2% and my 2020 forecast shows Nonres Bldgs ending the year down -2.1%. Some forecasters are predicting spending for nonresidential buildings will end the year down much worse compared to 2019. It would now be difficult to move the end-of-year forecast %change by much, with already 10 months recorded at an average of -1.2%. Also, some forecasts for 2021 predict spending for nonresidential buildings will increase. Remember, most of the reduced spending impact from the lost starts is felt when those lost projects would have been reaching peak spending.

Nonresidential Buildings construction will take several years to return to pre-pandemic levels. Although nonresidential buildings spending is forecast down only -2%, the gapping hole left by the 15%-25% drop in 2020 construction starts will mostly be noticed in 2021 spending. Project starts that were canceled, dropping out of new backlog between April and September 2020, would have had midpoints, or peak spending, April to September 2021. Nonbuilding project midpoints could be even later. The impact of reduced new starts in 2020 is reduced spending and jobs in 2021 and 2022.

Construction Jobs are projected to fall in 2021. While 2021 Residential spending will climb about 10%, Nonresidential building spending is forecast to drop -10% and Non-building spending drops -4%.

A recent AGC survey of construction firms asked, how long do you think it will be before you recover back to pre-COVID-19? The survey offered “longer than 6 months” as an answer choice. Less than 6 months was the right answer for residential, but my current forecast for full recovery of nonresidential buildings work is longer than 6 years.

Where is Construction Outlook Headed?

The greatest impact to construction spending from fewer new starts in 2020 comes in 2021 or early 2022, when many of those projects would have been reaching peak spending, near the midpoint of the construction schedule. Nonresidential starts in 2020 are down 15%-25%. Residential starts are up 2%.

Construction Spending for October https://census.gov/construction/c30/pdf/release.pdf…

Up 1.3% from Sept. Sept rvsd up 0.4%. Aug rvsd up 1%

Year to date (ytd) spending is up 4.3% over Jan-Oct 2019. Oct SAAR is now only 2% below Feb highpoint.

However, residential spending ytd is up 9.6%, nonresidential building spending is down -1.2%. Both are expected to keep heading in the direction currently established.

Nonresidential Buildings construction will take several years to return to pre-pandemic levels. Although nonresidential buildings spending is down ytd only -1.2% (as of October data), the gapping hole left by the 15%-25% drop in 2020 construction starts will mostly be noticed in 2021 spending. Project starts that were canceled, dropping out of revenues between April and September 2020, would have had midpoints April to September 2021. Nonbuilding project midpoint could be even later. The impact of reduced new starts in 2020 is reduced spending and jobs in 2021 and 2022.

Construction Jobs are projected to fall in 2021. While 2021 Residential spending will climb about 10%, Nonresidential building spending is forecast to drop -10% and Non-building spending drops -4%.

After adjusting for inflation, Residential volume is up about 4% to 5%, Nonresidential buildings volume is down about -14% and Non-building volume will finish down -8%. Jobs should follow suit.

If jobs increase faster than volume, productivity is declining. Also that means inflation is increasing.

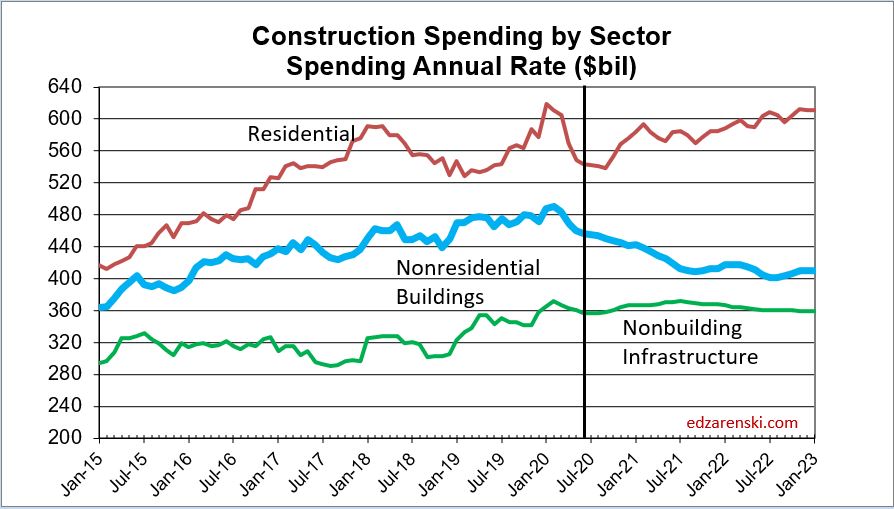

Spending is approximately 50% residential, 30% nonresidential buildings and 20% nonbuilding infrastructure.

Residential Construction Booming

RESIDENTIAL Construction Spending for October Up 2.9% from Sept

Sept spending rvsd up 1.5%, Aug rvsd up 3.5%

August highest new starts monthly total ever.

Year to date Oct. spending now up 9.6% over Jan-Oct 2019

Oct monthly SAAR now 2% higher than Feb highpoint.

Residential construction starts for Jul-Aug-Sep-Oct’20 posted the highest 4mo total ever. 2nd highest was Nov-Dec’19-Jan-Feb’20. In the last 12 months residential construction starts have posted 7 of the top 10 best months ever. Also, spending in Aug, Sep and Oct is the highest since the previous residential boom in 2005-2006. Spending is now already +2% higher than previous high in Feb and 2020 finishes up +10%. Spending climbs +10% higher in 2021.

Advanced Preconstruction Presentation – Construction Economics 11-4-20

Attached

EdZ Presentation Construction Economic Forecast 11-4-20 HW w notes

Here’s a few short notes

- 2020 spending will close the year UP.

- 2021 will get dragged down by declines in nonresidential buildings.

- Reduced new construction starts in 2020 impact 2021 far more than they impact 2020.

- Residential spending has returned to now only 2% less than the pre-pandemic peak in February.

- There will be hidden inflation not showing up in wages or material costs – lost productivity, acceleration.

There are other analysts reports that 2020 total construction spending will finish the year down -2%. Here’s why that will not happen.

Through August, year-to-date spending is up +4.2%. To finish the year down -2% (with only 4 months to go) would require each month of the final 4 months spending to come in at -14% year-over-year (yoy =compared to the same month last year). Not a single month this year has posted spending yoy lower than last year. Also, -14% yoy for 3 months would idle more than 1 million jobs for 4 months. That would make the final 4 months of 2020 the absolute worst period ever recorded.

September data is in (not included in the presentation) and makes it even more unlikely. Year-to-date September spending is up 4.1%, so Oct, Nov, and Dec would have to each post yoy spending of -20% for the year to end down 2%.

Similarly, the data show by an even wider margin, nonresidential buildings spending will not end 2020 down -10%.

This table updates the slide included in this presentation. It includes September spending year-to-date and Dodge Outlook 2021 for new forecast on construction starts in both 2020 and 2021.

Construction Forecast Update 10-16-20

UPDATES to Construction Outlook 10-16-20 based on

- Forecast includes US Census Aug 2020 year-to-date spending 10-1-20

- Forecast includes Dodge September construction starts 10-15-20

- Actual Jobs data includes BLS Jobs to Sept (12th) issued 10-2-20

This update accompanies pandemic-13-midyear-construction-outlook

Total construction starts year-to-date for 9 months through September are down 14%. Total starts have registered down -14% to -15% YTD for the last four months.

Residential new starts are down year-to-date only 1% from 2019. However, the last three months total residential starts posted the 2nd highest 3mo total in 15 years. The highest 3mo total since 2005 was for the period Dec’19-Jan-Feb’20. So two of the best 3mo periods of new residential construction starts in the last 15 years have occurred in 2020.

Nonresidential buildings starts are down 26% and non-building infrastructure starts are down 18%.

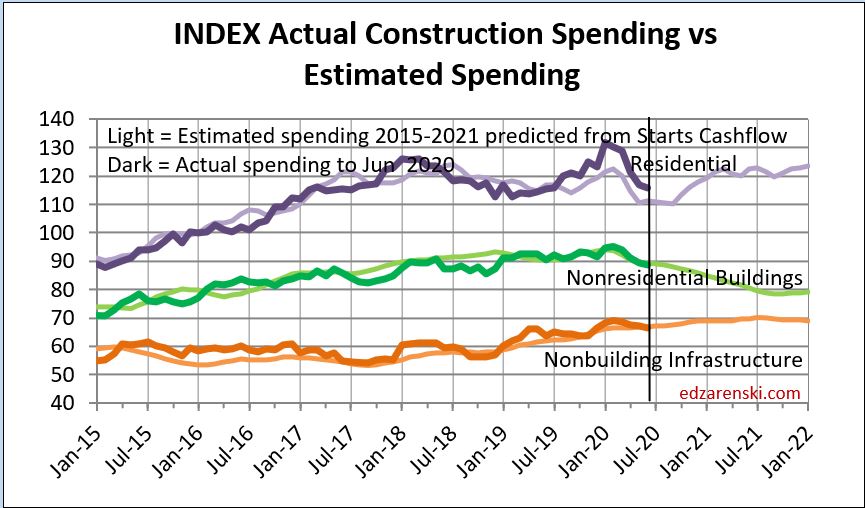

This chart shows a comparison of the cash flows predicted from new all construction starts vs the actual spending. Over time, the cash flows do a very good job of predicting where spending is headed. Note the divergence of residential in Jun-Jul-Aug 2020. Actual spending finished on avg 3%/mo higher than predicted. In 3 months the actual spending pushed 10% higher than predicted. This may be a reflection of forecasting too high an amount for delays and cancelations.

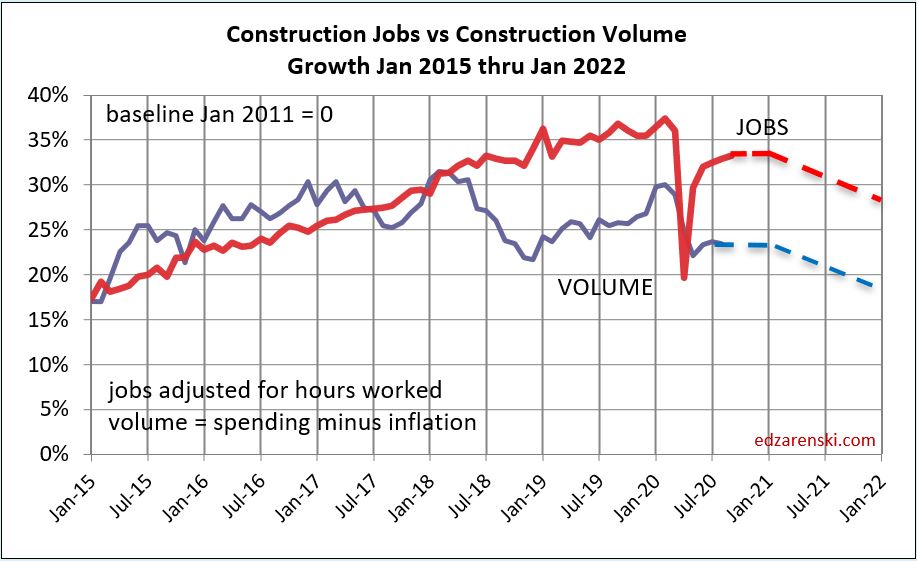

Construction Spending drives the headlines. Construction Volume drives jobs demand. Volume is spending minus inflation. Inflation $ do not support jobs. Current outlook shows (recent) peak volume was 2017-2018. Volume is forecast to decline every year out to 2023.

Construction jobs gained slightly in Sept, but are still down 5% (400,000) from Feb peak. Construction may experience only slight jobs improvement in 2020 (residential spending is increasing), but nonresidential buildings declines through 2021 will drive construction jobs lower over next 18 months.

Jobs are supported by growth in construction volume. We will not see construction volume return to Feb 2020 level in the next three years. This time next year, volume will be 5% lower than today, 14% below the Feb 2020 level.

This is why the construction industry will have a hard time justifying growth in jobs. After 12 years of fairly even growth in jobs vs volume, that relation broke in 2018. Volume is currently at a 5-year low, well below jobs. Declining work volume is indicating by this time next year we may be down 600,000 jobs below the Feb 2020 high.

The following table shows which markets have the largest (and smallest) changes in new construction starts. With the exception of residential, due to longer durations, spending in all other markets is most affected by a decline in new starts, not in this year, but in years following. Residential spending hit bottom in May, will post an increase in 2020. Nonres Bldgs spending won’t hit bottom until 2022.

A recent AGC survey of construction firms asked the question, How long do you think it will be before you recover back to pre-Covid? The survey offered “longer than 6 months” as an answer choice. My current forecast is longer than 6 years.

Some effects have not even begun to show up in the data. A 20% decline in new nonres bldgs starts in 2020 means a huge decline in spending and jobs in 2021-2022. How long before construction returns to the level it was at in Feb? 6 to 8 years.

Many nonresidential buildings have durations that last 24 to 36 months, with peak spending 12 to 18 months from now. With the drop in new starts this year, that peak spending 12 to 18 months from now will be impacted. Some nonbuilding markets have project durations that go out 5 or 6 years, so the impact of a decline in 2020 starts may be felt at least until 2025.

If construction starts in 2020 do not outperform 2020 construction spending, then starting backlog Jan. 1, 2021 will be lower. My current forecast (starts down 11%) is indicating 2021 starting backlog will be down by almost 10%. Spending declines into 2021 and remains depressed through 2023.

The last time starting backlog decreased was 2011. Starting backlog will fall 10% in 2021 and 2% in 2022. Except for residential, about 80% of annual spending comes from starting backlog.

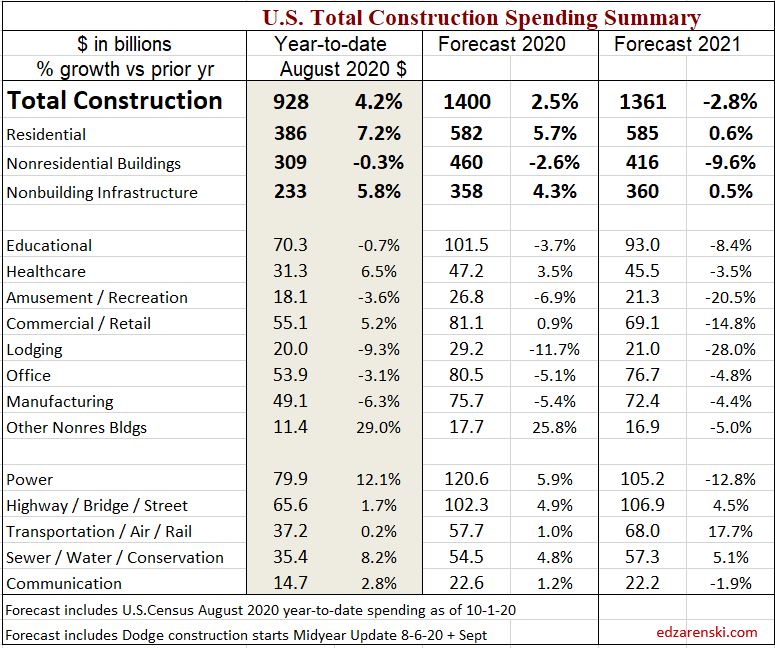

The next table shows spending year-to-date through August (released 10-1-20) and the spending forecast for the year. 2nd quarter construction spending activity low-point is down only 5.5% from the Feb peak. Construction spending in August YTD is up 4.2%.

Residential ytd is up 7.2%. Single Family is +3.0%, multifamily is +2.7% and renovations is Reno +15.6%. Nonresidential buildings ytd is down -0.3% and Nonbuilding Infrastructure ytd is +5.8%.

Take note here, the YTD spending for Nonresidential Buildings is currently -0.3% and my 2020 forecast shows Nonres Bldgs ending the year down -2.6%. Some forecasters are predicting spending for nonresidential buildings will end the year down much worse than -2.6% compared to 2019.

With only 4 months remaining, in order for Nonres Bldgs spending to finish down even -5%, the monthly rate of spending compared to 2019 would need to drop to -14%/mo for each of the remaining 4 months of 2020. (8mo x avg -0.3% + 4 mo x avg -14%) / 12mo = -5% total for the year. To end the year down -8%, nonres bldgs spending for the next 4 months would need to come in 25% lower than 2019. That’s “Great Recession” territory.

How unlikely is this to occur? The greatest monthly declines in 2020 so far are July and August in which the monthly rate of spending dropped -3% to -4% compared to same month 2019. Essentially, for nonresidential buildings spending to end the year down -5%, the bottom would need to drop out of the nonresidential markets, beginning back on Sept 1 and continuing for the final 4 months of the year.

Not sayin’ it can’t happen. This is 2020!

Pandemic #14 – Impact on Construction Inflation

8-27-20 What impact will the pandemic have on Construction Inflation in 2020? Here’s Several inputs.

In April, and again in June, I recommended adding a minimum 1% to normal long-term construction inflation, to use 4% to 5% for 2020 nonresidential buildings construction inflation. Some of my peers were suggesting we would experience deflation. Only twice in 50 years have we experienced construction cost deflation, 2009 and 2010. That was at a time when business volume was down 33% and jobs were down 30%. Currently business volume and jobs are down 10% and by mid-2021 are forecast down 15%.

The Turner Construction Cost index for the Q2 is down 1% from Q1, effectively reporting 0% increase in the index year-to-date. But the Turner index year-to-date (avg Q1+Q2=1183) is still 3.6% higher than the average of Q1+Q2 2019 and 2.3% higher than the avg for all of 2019 (1156). So, while the index appears to show no gains in 2020, through the first six months it is already up 2.3% above the average 2019 index. http://turnerconstruction.com/cost-index

The Rider Levitt Bucknall Q2 2020 index is up 1.6% ytd, up 4.6% from the Q1+Q2 2019 average and up 3.1% above the 2019 average. https://s28259.pcdn.co/wp-content/uploads/2020/07/Q2-2020-QCR.pdf

The U.S. Census Single-Family house Construction Index is up 3.6% year-to-date through July. July 2020 is up 4.2% over July 2019. https://www.census.gov/construction/nrs/pdf/price_uc.pdf

Producer Price Index items for July construction reported by AGC on 8-11-20. Inputs to Nonres construction are down ytd -1.0% through July. Final Demand Nonres Bldgs is up 1.8% ytd through July. See https://www.agc.org/learn/construction-data/construction-data-producer-prices-and-employment-costs and https://edzarenski.com/2020/07/14/producer-price-index-year-to-date-june-july-2020/

UPDATE 10-14-20 NAHB reports thru September (Residential) Building Materials Up 4.4% in 2020. See PPI charts. Increases for lumber and ready-mix concrete are noted. LUMBER “Over the last five months, the PPI for softwood lumber has nearly doubled (+90.9%). Sharply higher lumber prices have added more than $17,000 to the price of an average new single-family home since mid-April.” CONCRETE “Prices paid for ready-mix concrete (RMC) rose 1.5% in September (seasonally adjusted), a monthly increase the magnitude of which is atypical of the commodity. The national PPI for RMC has increased by more than 1% just five of the 135 months since the end of the Great Recession. The average annual change in prices paid for RMC was 2.6% over the last decade.” https://www.eyeonhousing.org

R.S.Means quarterly cost index of some materials for the 2nd quarter 2020 compared to Q1: Ready-Mix Concrete 0%, Brick and Block +3%, Steel Items -2%, Wood products +3%, Roof Membrane +7%, Insulating Glass +6%, Interior Finishes -2%, Plumbing Pipe and Fixtures +7%, Sheet Metal +7%. https://www.rsmeans.com/landing-pages/2020-rsmeans-cost-index

U.S. manufacturing output posts largest drop since 1946. Think of all the manufactured products that go into construction of a new building: Concrete, steel, doors, windows, roofing, siding, wallboard, lighting, heating systems, wire, plumbing fixtures, pipe, valves, cabinets, appliances, etc. We have yet to see if any of these will be in short supply leading to delays in completing new or restarted work?

There have been reports that scrap steel shortages may result in a steel cost increase. The U.S. steel industry is in the most severe downturn since 2008, as steelmakers cut back production to match a sharp collapse in demand and shed workers. Capacity Utilization dropped from 82% to 56% in April. Now in mid-August, CapU is up to 61%, still very low. Steel manufacturing output fell by a third and is still down more than 25%. Until production ramps back up to normal levels there may be shortages or delays in delivery of steel products.

Since Q1, the cost of lumber has increase 120%, so expect residential inflation to increase faster than nonresidential. https://eyeonhousing.org/2020/08/average-new-home-price-now-14000-higher-due-to-lumber/ and revised http://nahbnow.com/2020/08/average-new-home-price-now-16000-higher-due-to-lumber/

Contractors have been saying they have difficulty acquiring the skilled labor they need. This has led to increased labor cost to secure needed skills.

But most important, this SMACNA report quantifies that labor productivity has decreased 18% to meet COVID-19 protocols. https://www.constructiondive.com/news/study-finds-covid-19-protocols-led-to-a-7-loss-on-construction-projects/583143/

Labor is about 35% of project cost. Therefore, just this productivity loss equates to 18% x 35% = 6.3% inflation. Even if, for all trades, the average lost time due to COVID-19 protocols is only half that, the added inflationary cost to projects is 3% above normal. I expect the Turner Nonres Bldgs index will reflect some added labor cost in the next two quarterly releases.

Post Great Recession, average nonresidential buildings inflation is 3.9%. For the last five years it’s 4.5%. Residential cost inflation averaged 4.1% and 4.5% for those periods. The 30-year average inflation rate for nonresidential buildings is +3.75%.

Almost every construction market has a weaker spending outlook in 2021 than in 2020, because approximately 50% of spending in 2021 is generated from 2020 starts and 2020 starts are down.

Typically, when work volume decreases, the bidding environment gets more competitive and prices go down. However, if materials shortages develop or productivity declines, that could cause prices to increase.

Add to these issues the fact that many projects under construction have been halted for some period of time and many more have experienced at least short-term disruption. The delays may add either several weeks to perhaps a month or two to the overall schedule, in which case management cost goes up, or it could add overtime costs to meet a fixed end-date.

We can expect some cost decline due to fewer projects to bid on, which typically results in sharper pencils. But we can also expect cost increases due to materials, labor cost, lost productivity, project time extensions, and/or potential overtime to meet fixed end-date.

I expect non-residential buildings inflation to range between 4% and 5% for 2020 and 2021, perhaps 5% to 6% for residential work.

Pandemic #13 – Midyear Construction Outlook

See Also this update Construction Forecast Update 10-16-20

SEE ALSO Pandemic #14 – Impact on Construction Inflation

Midyear Construction Outlook 8-14-20 based on

- Actual Spending data includes revisions 2018-2019 issued 7-1-20

- Actual Jobs data includes BLS Jobs to July (12th) issued 8-7-20

- Forecast includes US Census June 2020 year-to-date spending 8-3-20

- Forecast includes Dodge construction starts Midyear Update 8-6-20

The first important thing to note is that the US Census, on 7-1-20, revised all spending data back several years. This is an annual occurrence. This analysis includes all revised data, which adds about $30 billion to 2018, $60 billion to 2019, half of all adding to residential, and revises 2020 data. Not everyone has yet updated to this recently revised data, so you may see differences when comparing forecast reports among several firms. If needed, refer to the percent.

Initial impact on spending from project delays/shutdowns

This compares the current construction spending data to a 2020 Forecast from April 1 before any Pandemic Impacts were recorded. It compares actual to what was expected Pre-Pandemic. The change in year-to-date (ytd) all occurred in 2nd quarter data. In fact, 1st quarter ytd growth was forecast at 7% and it came in at 9.5%. 2nd quarter growth was forecast at 6.8% and it came in at 1%.

Construction Spending 2020 year-to-date (ytd) thru June vs 2019

Actual ytd vs Pre-Pandemic Forecast ytd. Nearly all this change is due to projects delayed/shutdown.

- Nonres Bldgs down 2.4% ytd in 6mo vs pre-pandemic forecast

- NonBldg UP 3.0%

- Residential down 4.9%

- TOTAL down 1.9%

The measure of decline due to Pandemic delays and shutdowns is not the difference between Q1 and Q2 growth in ytd spending. Nor is the impact measured by the current difference in ytd performance vs 2019. It’s the difference between what was forecast for ytd growth pre-pandemic vs actual ytd growth.

For instance, Residential construction spending thru Q2, as reported in the US Census June construction spending release, is up ytd 7.8%. But pre-pandemic it was forecast to be up 12.7% ytd after 6 months. Hence, residential spending has been impacted by a 12.7% – 7.8% = 4.9% decline from original forecast thru June.

Future impact on spending from lost construction starts

Part one of the decline in construction spending was due to delays/shutdowns. Part two will be the impact of reduced construction starts. That has very little affect right now, but will play out over the next few years. But remember once again, the impact in 2021 is not measured by the difference between 2020 and 2021, its the difference between current forecast for 2020/2021 and the pre-pandemic forecast for 2020/2021.

Year-to-date, total construction starts are down 14%. Residential new starts are down 5%, nonresidential buildings down 22% and non-building infrastructure starts are down 14%.

Dodge updated their forecast to show 2020 construction starts for nonresidential buildings fall on average 20%, less in some markets, but -30% to -40% in a few. Only warehouses is up. Non-building starts fall on average 15%. Only Highway/Bridges is up. Residential starts may fall only 5%-10%.

How those lowered starts affect spending is spread out over cash flow curves for the next few years. This has a major impact on jobs later in 2020 and all of 2021 into 2022. For nonresidential buildings, the greatest impact to spending and jobs affected by a reduction of new starts in 2020 occurs from 2021 into 2022 when many of those lost starts would have been reaching peak spending.

Only about 20% of new starts gets spent in the year they started. 50% gets spent in the next year. The effect of new starts does not show up immediately. If new nonresidential buildings starts in 2020 are down 22%, on average, the affect that has on 2020 is reduced spending by -22% x 20% = – 4.4%. But the affect it has on 2021 is -22% x 50% = -11%.

Construction Spending FORECAST 2020 vs Pre-Pandemic Forecast

This change in forecast incorporates reduced new construction starts for 2020 but also includes the impact from delays and shutdowns.

- Nonres Bldgs down 5.4% for 2020 vs pre-pandemic forecast

- NonBldg down 0.3%

- Residential down 6.5%

- TOTAL down 4.5% vs pre-pandemic forecast

Construction Spending FORECAST 2021 vs Pre-Pandemic Forecast

Nearly all this change due to a reduction in new construction starts in 2020. Notice, it is nonresidential buildings that are impacted the most, down 10% from the pre-pandemic forecast.

- Nonres Bld down 9.9% for 2021 vs pre-pandemic forecast

- NonBldg down 6.4%

- Residential UP 5.8%

- TOTAL down 2.5% vs pre-pandemic forecast

Future impact on backlog from delays/cancellations and reduced starts

Starting Backlog is the Estimate-to-Complete (ETC) value of all projects under contract at the beginning of a period. Projects in starting backlog could have started last month or last year or several years ago. Many projects in backlog extend out several years in the schedule to support future spending, so backlog growth in not an indicator that tracks year over year with spending. Current backlog at the start of 2020 would still contribute some spending for the next 6 years until all the projects in backlog are completed.

The last time starting backlog decreased was 2011. Starting backlog will fall 10% in 2021 and 2% in 2022. Except for residential work, about 80% of annual spending comes from starting backlog.

Some of the projects delayed or canceled started before Jan. 2020. When one of those projects is delayed, the portion of the project delayed gets removed from 2020 backlog, but then gets added to future backlog. When one of those projects is canceled, the portion of the project not yet put-in-place gets removed from 2020 and future backlog. Not only does that reduced future backlog but also that retroactively reduces the backlog that was on record at the start of 2020. Therefore, 2020 backlog is reduced by delays and cancellations and future backlog is increased by delays, but reduced by cancellations and a loss of new construction starts.

The following is the difference between what was forecast for backlog pre-pandemic and currently projected backlog based on delays, cancellations and reduced starts.

Backlog projected for the start of 2020:

- Total Construction down 3.6% vs pre-pandemic forecast

- Nonresidential buildings down 8.3%

- Non-building infrastructure up 0.5%

- Residential backlog down 2.2%, new starts down 5.4%

Although two thirds of Residential spending comes from new starts within the year, 2020 backlog is down 2.2%. 2020 new starts are down 5.4%.

The biggest changes to 2020 backlog are Manufacturing, Commercial/Retail and Amusement/Recreation, all down 10% to 15%.

Backlog projected for the start of 2021:

- Total Construction down 9.8% vs pre-pandemic forecast

- Nonresidential buildings down 15.1%

- Non-building infrastructure down 9.4%

- Residential backlog up 3.6%, starts up 8.4%

For 2021, Power and Environmental Public Works are down 20% and 10% respectively, but Nonresidential Buildings shows most of the losses. Lodging -40%, Amusement -28%, Manufacturing -26%, and Office and Commercial both down about 15%.

Spending Forecast 2020 – 2021

Now that we have highlighted the change in the forecast compared to the pre-pandemic forecast, let’s look at the current spending forecast for 2020 and 2021.

See Pandemic #11 – June Construction Spending Update for coverage of midyear spending year-to-date through June.

For 2020, the biggest declines are Manufacturing, Lodging and Amusement/Recreation, all down -8% to -10%. Commercial/Retail ends up +3.9% (this market is 60% Warehouse). Office and Educational are down -3% and -1%. Nonresidential buildings takes the brunt of declines in both 2020 and 2021.

In 2021, every nonresidential building market is down from 2020, some markets down 10% to 20%. Educational, Healthcare and Office are all down 3% to 5%. Non-building infrastructure Power market is down -11%, but Highway and Transportation are up +10% to 20%.

Almost every market has a weaker spending outlook in 2021 than in 2020, because of lower starts in 2020. Starts lead to spending, but on a curve, a good average for nonresidential buildings is 20:50:30 over three years. 20% of the total of all starts in 2020 gets spent in 2020 (yr1) and that represents also about 20% of all spending. 50% of the total value of 2020 starts gets spent in the following year, 2021. So, 50% of spending in 2021 is generated from 2020 starts. If starts are down 20% and 50% of spending comes from those starts, spending will be down 20% x 50% of the work.

Although starts are forecast down 15% to 20% in 2020 and UP 5% to 15% in 2021, the drop in starts in 2020 has the greatest impact on reducing spending in 2021. By June of 2021, spending is down 10% from Feb 2020 and volume is down 14%.

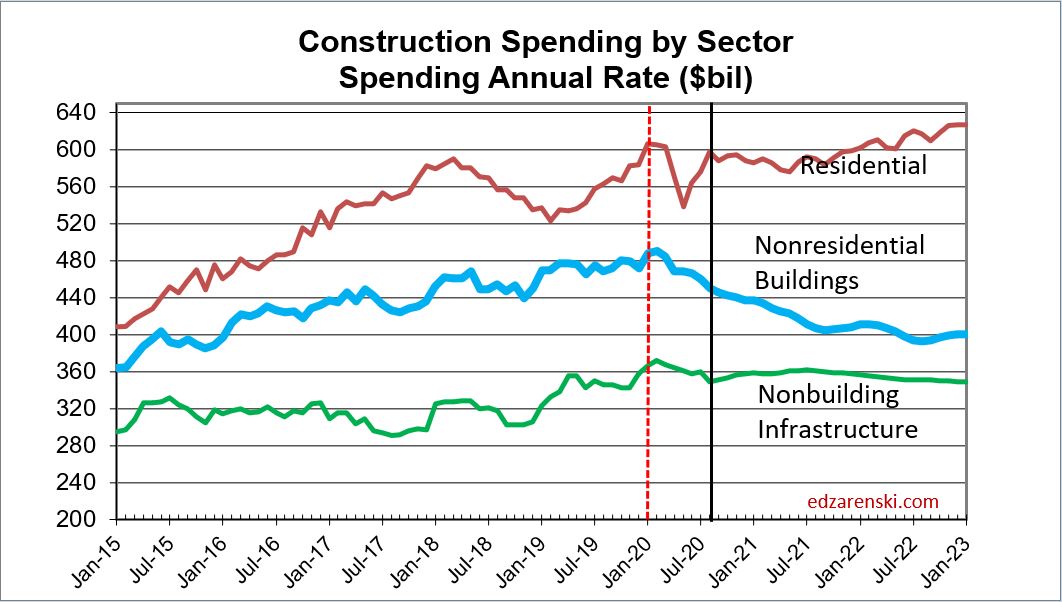

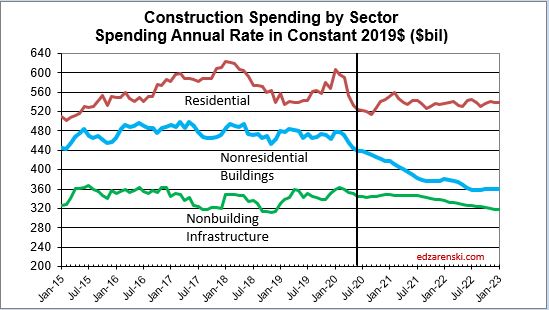

Before we can look at the effect on jobs, we need to adjust spending for inflation. The plot above “Spending by Sector” is current dollars. Here that plot is adjusted for inflation and is presented in constant $. Constant $ show volume. Notice residential remains in a narrow range after adjusting for inflation. No sector shows improvement in volume through Jan. 2023.

By far the greatest decline in volume is in the nonresidential buildings sector. Volume declines follow in line with spending declines. The greatest losses in 2020 are Amusement/Recreation, Lodging and Manufacturing. In 2021, every major nonresidential building market drops in volume.

Why 400,000 construction jobs are not coming back

Reduced starts in 2020 has a major impact on jobs later in 2020 and all of 2021 into 2022. For nonresidential buildings, the greatest impact to spending and jobs occurs from 2021 into 2022 when many of those lost starts would have been reaching peak spending.

Jobs data show construction added 20,000 more jobs in July. After losing almost 1,100,000 jobs in March and April (out of a prior total 7,600,000), we regained 450,000 jobs in May and 160,000 in June. That leaves construction down 440,000 jobs from the February high point.

Jobs are down 6% from Feb to July, but construction spending is down 7% through June and volume (spending adjusted for inflation) is down 9%.

Although we may get slight jobs growth in the next few months, there is little to no volume growth to support it. Spending is currently down 7% from the Feb high and volume is down 9%. More spending declines are minimal through Q1 2021. Due to the large declines in new construction starts, we will begin to see additional spending and volume declines by spring 2021. Most of the decline will be in nonresidential buildings.

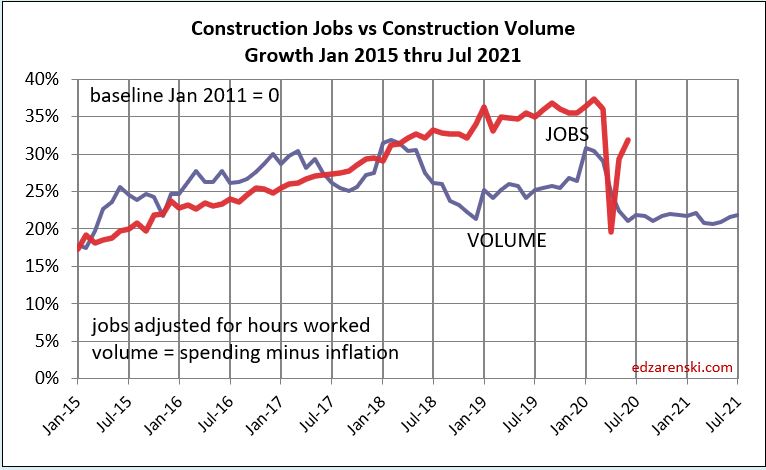

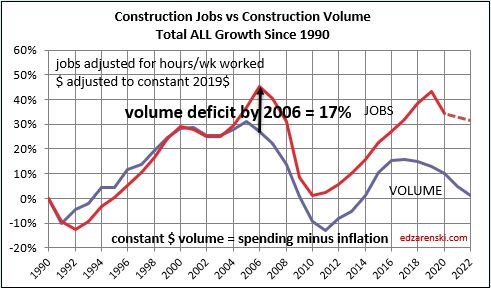

This annual plot back to 1999 shows construction spending vs construction volume. Volume is spending minus inflation. Notice, volume never recovered to peak 2005. Also notice, recent volume began to decline in 2018.

The long-term view of jobs vs volume shows an important point. With few exceptions jobs and volume grow equally. Setting a baseline to zero in 1990, there was a spread in 1992 that was nearly equalized by 1998. Jobs and volume growth remained near equal until 2004. Leading into 2006, spending increased by the most in 30 years. Jobs, which seem to lag slightly, grew 15% from 2004 thru 2006. But inflation posted the highest rate in 30 years. While jobs grew to meet spending growth, almost all the spending growth was inflation. By 2006, jobs growth exceeded construction volume by more than 15%.

As I said, with few exceptions, jobs and volume grow equally. If we modify history to reset the baseline to 2006 by increasing volume, the plot now shows that all years from 2006 to 2017 remained consistent in jobs growth vs volume growth. So, with exception of 1992 and 2004-2005, all years from 1990 to 2017 had consistent growth in jobs and volume.

Leading into 2017, spending once again reached a rate of near record growth, second only to 2004-2005. Again, jobs, which seem to lag slightly, grew to meet spending growth. But inflation posted the highest rate since 2006. Once again, jobs grew rapidly, but almost all the spending growth was inflation. By 2019, for the second time, jobs growth exceeded construction volume by almost 15%.

Jobs are supported by growth in construction volume, spending minus inflation. We will not see construction volume return to Feb 2020 level at any time in the next three years. This time next year, volume will be 5% lower than today, 14% below the Feb 2020 level.

We are currently down 440,000 construction jobs from the Feb high. We may regain 40,000 to 50,000 more jobs before the end of the year. But the declining work volume due to a reduction in new starts in 2020 is indicating by this time next year, not only is there no volume to regain 400,000 lost jobs, but we may lose another 200,000 jobs and be down 600,000 jobs below the Feb 2020 high.

The following plot is the same jobs and volume data as above, only plotted monthly rather than annually. Much of the fear decline of jobs in April has been corrected, but jobs are still down 440,000 from the February high. And yet, the plot shows jobs in excess of construction volume by about 12%.

Volume is set to decline at least for the next two years. There will be no volume growth to support jobs growth and long-term jobs growth already exceeds volume growth by 12%. This is not an environment that supports jobs growth.

Pandemic #12 – Jobs & Starts Updated

8-7-20

Jobs data released today show construction added 20,000 more jobs in July. After losing almost 1,100,000 jobs in March and April (out of a prior total 7,600,000), we regained 450,000 jobs in May and 160,000 in June. That leaves construction down 440,000 jobs from the February high point.

Jobs are down 6% from Feb to July, but construction spending is down 7% through June and volume (spending adjusted for inflation) is down 9%.

Year-to-date, total construction starts are down 14%. Residential new starts are down 5%, nonresidential buildings down 22% and non-building infrastructure starts are down 14%. In April, I estimated jobs losses based on Dodge April forecast that new construction starts in 2020 would fall by 10-15% (see Pandemic Impact #4). Yesterday Dodge updated their forecast to show 2020 construction starts for nonresidential buildings fall on average 20%, less in some markets, but -30% to -40% in a few. Only warehouses is up. Non-building starts fall on average 15%. Only Highway/Bridges is up. Residential starts may fall only 5%-10%.

That lowers my forecast for 2021 and 2022.

How those lowered starts affect spending is spread out over cash flow curves for the next few years. This has a major impact on jobs later in 2020 and all of 2021 into 2022. For nonresidential buildings, the greatest impact to spending and jobs occurs from 2021 into 2022 when many of those lost starts would have been reaching peak spending.

Although we may get slight jobs growth in the next few months, there is little to no volume growth to support it. Spending is currently down 7% from the Feb high and volume is down 9%. More spending declines are minimal through Q1 2021. Due to the large declines in new construction starts, we will begin to see additional spending and volume declines by spring 2021. Most of the decline will be in nonresidential buildings.

Revisit Pandemic Impact #8 – Construction Outlook to compare this plot above to the forecast as of June 3 and to the original forecast at the start of this year.

Jobs are supported by growth in construction volume, spending minus inflation. We will not see construction volume return to Feb 2020 level at any time in the next three years. This time next year, volume will be 5% lower than today, 14% below the Feb 2020 level. In fact, volume began it’s decline in Q2 2018.

Almost every market has a weaker spending outlook in 2021 than in 2020. That’s because only about 20% of spending in the year is from new starts in the year. About 50% of spending from new starts in 2020 is spent in 2021. Although starts are forecast down 15% to 20% in 2020 and UP 5% to 15% in 2021, the drop in starts this year has the greatest impact in reducing spending in 2021.

Only about 20% of new starts gets spent in the year they started. 50% gets spent in the next year. The affect of new starts does not show up immediately. If new nonresidential buildings starts in 2020 are down 22%, on average, the affect that has on 2020 is reduced spending by -22% x 20% = -4.4%. But the affect it has on 2021 is -22% x 50% = -11%.

By June of 2021, spending is down 10% from Feb 2020 and volume is down 14%.

We are currently down 440,000 construction jobs from the Feb high. We may regain 40,000 to 50,000 more jobs before the end of the year. But the dropping work volume is indicating by this time next year we may lose another 200,000 jobs and be down 600,000 jobs below the Feb 2020 high.

Pandemic #11 – June Construction Spending Update

Construction Spending thru June year-to-date is still UP 5% over Jan-Jun 2019.

Here’s the Census Release of June Construction Spending census.gov/construction/c

Q2 2020 spending is down 4.8% from Q1 2020. Prior to the Pandemic impact, Q2 was predicted to be up 1% over Q1. So, then the drop is -5.8% from the initial forecast.

Comparing 2020 spending to 2019 shows a different story. Q1 2020 is up 9.5% vs Q1 2019. Q2 2020 is up 1.2% vs Q2 2019.

The monthly rate of spending, seasonally adjusted (saar), has declined every month since the Feb peak. For 3 months Jan, Feb, Mar, the saar of spending stayed within 0.25% of the peak. Now in June, the saar is down -6%. Most of the decline was in April, -3.5%. May dropped <2% mo/mo, and June declined <1%.

Residential year-to-date (ytd) spending is up almost 8% over 2019 (80% of that is renovations). In fact, SF+MF is up ytd only 2.8%, while renovations, which went from 33% of the market last year to 36% of the market now, is up 18% ytd. Residential has more downside due to reduction in new starts before resuming growth next year. While the 2nd half of 2019 increased at an average rate of 1%/month, The 2nd half of 2020 will decline by an average 0.5%/month. Residential spending for 2020 is forecast to finish flat to down 1%.

Non-building Infrastructure sector ytd is up 7% over Jan-Jun 2019. Biggest mover is the Power market up 17% ytd. Every market but Conservation is up ytd. Non-building spending is forecast to close out 2020 up 6% over 2019 with strength in Power and Highway.

Nonresidential Buildings spending ytd is level with 2019. Big movers up are Comm/Rtl up 6.7% and Public Safety up 42%.

The construction sector did not experience a massive loss of spending from project shutdowns in Q2. Q2 was down 5%-6% from the pre-pandemic forecast. Jun is down only 0.7% from May with half of all markets posting monthly gains.

AIA Consensus Forecast Nonresidential Bldgs Construction Spending to decline 8.1% for 2020. Is there even a path to get there? In the 1st 6mo ytd is up 0.25%. What would nonres bldgs need to post yoy in the 2nd half to end the year down 8.1%? Spending would need to post declines every month (yoy) for the next 6mo at a rate of -16.7%/month. However, the worst decline in Q2 was only -3.2%. It’s not likely at all that Nonres Bldgs spending will fall to that extent.

Here’s an example of the path it would take to get to the AIA Consensus Forecast for Commercial/Retail. The AIA 2020 Forecast is down 7.7%. But year-to-date Comm/Rtl is up 6.7%, a spread of 14.4%. (I’ll remind you again, it’s almost all warehouses). To drop 14.4%, from 6.7% in the 1st 6 months, to end down -7.7% at year end, the monthly rate in the 2nd half would need to be -28.8% each month. That’s not very likely.

For the next 6 months my yoy forecast for Nonres Bldgs spending is up 0.4%.

The BIG question here is, How much of the decline in Q2 was delays and how much was canceled permanently? There is no good report available that defines the total value of work stoppages and work cancellations.

Q2 spending was down 5%-6% from the pre-pandemic forecast. If all of that was work canceled, and therefore we keep those monthly yoy declines of 5%-6% for the rest of the year, then we could see 2020 spending for Nonres Bldgs finish down 2.5% to 3%. But it is not even suspected that all of the Q2 decline was work canceled. Expect most of that was work delayed. Therefore, 2nd half should perform better than Q2 and the forecast for Nonres Bldgs for 2020 is flat to up 1%.

The forecast now has 6 months of actual spending and 6 months remaining of forecast based on new construction starts and backlog. Cash flow forecast from backlog is reduced by delays and cancellations. This forecast projects about 20% for delays and about 2% for cancellations. Also new starts are forecast to drop about 10% in 2020.

The Starts cash flow model has predicted the spending pretty well. The forecast side shows residential has not yet hit bottom, but will grow after Q3 into 2021, while nonresidential buildings falls for the next 12 months.

Currently, the outlook for total construction spending in 2020 is up 1% to 2%. Prior to March the forecast was 6%, so the forecast, although still up 1-2%, has fallen about 5%.

Both Residential and Nonresidential Buildings are forecast within +/- 1% of 2019. Non-building Infrastructure is forecast up 6%-7%.

Currently, inflation in 2020 is expected to range about 3%-4%. If total construction spending grows only 1%-2%, real growth in volume (spending after inflation) is falling. For 2020 and 2021, volume is down. That will not support jobs growth.