Attached

EdZ Presentation Construction Economic Forecast 11-4-20 HW w notes

Here’s a few short notes

- 2020 spending will close the year UP.

- 2021 will get dragged down by declines in nonresidential buildings.

- Reduced new construction starts in 2020 impact 2021 far more than they impact 2020.

- Residential spending has returned to now only 2% less than the pre-pandemic peak in February.

- There will be hidden inflation not showing up in wages or material costs – lost productivity, acceleration.

There are other analysts reports that 2020 total construction spending will finish the year down -2%. Here’s why that will not happen.

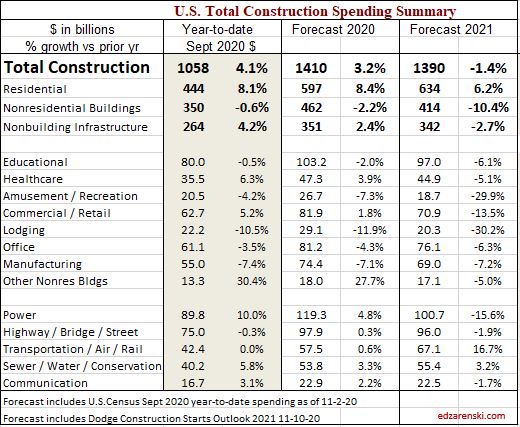

Through August, year-to-date spending is up +4.2%. To finish the year down -2% (with only 4 months to go) would require each month of the final 4 months spending to come in at -14% year-over-year (yoy =compared to the same month last year). Not a single month this year has posted spending yoy lower than last year. Also, -14% yoy for 3 months would idle more than 1 million jobs for 4 months. That would make the final 4 months of 2020 the absolute worst period ever recorded.

September data is in (not included in the presentation) and makes it even more unlikely. Year-to-date September spending is up 4.1%, so Oct, Nov, and Dec would have to each post yoy spending of -20% for the year to end down 2%.

Similarly, the data show by an even wider margin, nonresidential buildings spending will not end 2020 down -10%.

This table updates the slide included in this presentation. It includes September spending year-to-date and Dodge Outlook 2021 for new forecast on construction starts in both 2020 and 2021.