Home » Articles posted by edzarenski (Page 21)

Author Archives: edzarenski

Ahead of the Sept Construction Spending Forecast

10-25-17

On November 1, September construction spending will be released. The September spending release is always a solid turning point for the 2017 forecast. Here’s a few facts leading into the forecast which will incorporate this data and be posted soon after the 11-1-17 spending release.

2017 construction spending will come in at $1,250 billion, up 5.5% from 2016.

Largest $ contributors to growth in 2017 spending: Residential $56b, Commercial Retail $12b, Office $6b.

Largest $ declines in 2017 spending: Manufacturing -$8b, Public Works -$6b.

Total construction spending averaged 8%/yr growth last 6 yrs (2014 & 2015 at 11%). Expect 6% in 2018, 5% in 2019

Construction spending on Infrastructure leads growth for the next 3 years and it has nothing to do with an infrastructure spending bill.

Infrastructure spending in 2018 is led by Power and Transportation markets.

Most of the 2018 spending in the Power market will be generated from starts in 2016. Equally strong 2017 starts will generate most of the Power spending in 2019.

Public construction spending in 2018 will reach highest yr/yr growth rate in over 10 years powered by Educational spending.

Commercial/Retail spending in 2018 slows but most other nonresidential buildings still show strong growth, especially Office and Educational.

Residential spending slows to a crawl after more than 100% growth in last 6 years. Currently predicting only 5% to 6% growth over next 2 years.

Residential spending may change during the year because, while spending in all other markets is dependent on starting backlog, residential spending is primarily dependent on new starts within the year

Largest $ contributors to growth in 2018 spending: Power $22b, Office $15b, Educational $10b, Transportation $5b.

Largest $ declines in 2018 spending: none greater than -$2b.

Nonresidential Buildings and Infrastructure construction will both hit new all-time highs for starting backlog in 2017 and 2018. Both will see a 9% increase in spending in 2018.

Infrastructure construction spending never dropped due to the recession as much as Nonresidential Buildings or Residential.

Nonres Bldgs dropped 35% from $438bil in 2008 to $284bil in 2011.

Residential dropped 60% from $630bil in 2005 to $252bil in both 2010 and 2011.

Infrastructure declined only 8% from $274bil in 2009 to $251bil in 2011. It rebounded to $305bil in 2015, a new high.

Nonres Bldgs spending is just 3% below the previous high but residential is still 16% below 2005.

In constant$, adjusted for inflation, Nonres Bldgs peaked at $537bil in 2000 and Residential peaked at $755bil in 2005.

Nonres Bldgs is still 21% below the inflation adjusted peak. Residential is still 30% below.

Infrastructure reached an inflation adjusted peak in 2009 at $300bil. It hit a new high in 2016 at $313bil and in currently down 6% from that high. It will set a another new high in 2018.

Watch for the new 2017-2018 Spending Forecast to be posted within the week after the September data is released 11-1-17.

These other recently posted articles also have information relative to the 2017-18 forecast

Is Infrastructure Construction Spending Near All-Time Lows?

Construction Starts and Spending Trends 2017-2018

Is Infrastructure Construction Spending Near All-Time Lows?

10-10-17

Is Infrastructure construction spending near all-time lows? This question is raised because I saw comments to this affect recently posted on a major national construction professional organization twitter feed.

First, this raises several other questions:

- Exactly what construction markets are being referenced as infrastructure?

- Does this reference include public work only, or both public and private?

- Are educational and health care being included as infrastructure?

- Does this reference constant inflation adjusted spending?

The construction markets typically referred to as infrastructure, in order of largest to least volume, include; Power, Highway, Transportation, Sewage/Waste Water, Communications, Water Supply and Conservation. Sometimes also considered are Educational (3rd after Highway), Healthcare (after Transportation) and Public Safety (2nd smallest).

If only public work is included, everything changes. Most (90%+) of Power spending is private, so it represents less than 3% of public work. The largest contributors in this case are: Highway (32% of public work), Educational (25%), Transportation (11%), Sewage (8%) and Water Supply (4%). No other market is greater than 3% of public work.

And finally, is the reference to current dollars as originally spent within each year, or to constant inflation adjusted dollars, adjusting all historical expenditures to constant 2017 dollars? Any comparison to determine if real growth has occurred should be in constant dollars, in this case all adjusted to 2017.

Typical infrastructure, not including educational, healthcare or public safety, but including all public and private sector work produces this result:

However, the most likely reference is to typical public infrastructure, not including educational, healthcare or public safety. This scenario includes only the public sector work of typical infrastructure and eliminates private spending. This eliminates 90%+ of all power work, 30% of transportation and 100% of communications, in total, more than $100 billion in current dollars. This is the result:

In both instances, the lows, whether using current or constant dollars, occurred between 1993 and 2004. The highs are recent, all occurring from 2007 to 2016. 2017 spending dropped somewhat from 2016, but this is still prone to revision, which is always up.

To answer the question, Is Infrastructure construction spending near all-time lows? NO! Infrastructure construction spending is not at or even near all-time lows. Public sector infrastructure is lower than All infrastructure, but All infrastructure is not even near recent lows. It is near all-time highs!

Infrastructure construction spending in June-August dropped to the lowest since November 2014. However, this was not unexpected. Cash flow models of infrastructure starts from the last several years show monthly spending dips and peaks. Current dips in spending are being caused by uneven project closeouts from several years ago. The actual current backlog is at an all-time high and spending will follow the expected cash flow.

Infrastructure starting backlog hit a new all-time high in 2017 and will again in 2018. Public Infrastructure new starts reached all-time highs in 2013 and 2015 and are on track to go higher in 2017. 80% of infrastructure spending within the year comes from backlog at the start of the year and that backlog may be comprised of jobs one, two, three and even four years old.

Infrastructure spending in 2017, although down slightly from the all-time high reached in 2015 and nearly equaled in 2016, will reach a new high in 2018.

(This analysis does not include any spending projections from an infrastructure investment bill).

Highway spending is currently benefiting from projects that started in 2015 but that have unusually high value and long duration. They contribute spending well into 2018 beyond the duration that typical projects have ended.

Transportation Terminal starts in the first three months of 2017 were more than three times higher than any three-month period in the previous five years. However, 2017 spending is still affected by uneven starts from two to three years ago, holding down gains in the 2nd half. Transportation will show only a 1% gain in 2017 but produces double digit gains in 2018.

Infrastructure construction spending is near all-time HIGHS and has been for the last several years. That is not meant to indicate there is no need for infrastructure investment. I think the need is well established, particularly for public infrastructure. However, I’ve been writing about infrastructure for more than a year, pointing out the level of activity in this sector and the difficulty that will arise when we try to increase work volumes. The approach to adding new work and the discussions surrounding this approach should reference accurate data, and that should include an accurate representation of current workload and future ability to absorb more work.

For much more in-depth related to infrastructure construction see this post Infrastructure Spending & Jobs

So, About Those Posts “construction spending declines…”

You know those articles you’ve been seeing, “Worst year for construction spending since 2010″, well there’s some truth to that, BUT

2017 is the 6th year of the expansion. It has slowed, but… Here comes the BUT!

10-4-17 – Construction numbers are at all-time highs! Slowing or not, activity is very strong. Looking behind the headlines, here’s what we see;

Residential construction spending is slowing the most, from +11% in 2017 to only +2% in 2018 after six years averaging 13%/yr. Nonresidential buildings spending this year just kept up with the rate of inflation (4%), none-the-less, it’s at record highs. It doubles that rate of growth to 8% in 2018. Non-building infrastructure, down 2% in 2017, next year expect growth of 10%+, coming from long duration jobs.

The real performance numbers in Infrastructure are completely hidden. Spending was near flat for three years. But during that time, contrary to every other sector which experienced inflation of 15%, Non-building Infrastructure experienced deflation of 7%. (Gee, didn’t I read somewhere that activity within a sector is a primary driver of inflation?) Anyway, flat spending means volume really increased by 7% during that time. Spending by itself never tells the whole story!

There were some expected dips in spending recently, Manufacturing, Power, Highway, and there will be more in early 2018. BUT, there are also expected boosts in spending, Office, Commercial/Retail. Some of these already have matched up with the forecast, and there are more to come in 2018, Power, Transportation.

All Nonresidential Backlog is at record highs.

Buildings and Infrastructure will both hit new all-time highs for starting backlog in 2017 and again in 2018. For four years, from 2010 to 2013, all nonresidential backlog remained fairly constant. Since then, backlog for infrastructure is up 30% and for buildings it’s up 60%. (75% to 80% of nonresidential spending within the year comes from backlog at the start of the year. For residential, 70% of spending comes from new starts within the year.) Buildings will hit spending records in both 2017 and 2018. Infrastructure spending will hit a new high in 2018.

Ignoring for the moment that comparing any month to the same month last year can be grossly misleading as to the direction the markets are headed (for reasons explained in other recent posts on this blog), 2017 total spending growth is the lowest % yr/yr growth since 2011 (not 2010). Does that make it “worst”?

Spending will gain +5.6% in 2017, the least gain in six years. Last year was +6.5%, 2013 was +6.6%. The average for the last six years is +8%. So 2017 is the worst. Pretty damn good worst!

August Construction Spending 10-2-17

Data released 10-2-17

Preliminary Report August Construction Spending

August construction spending was posted today at $1.218 trillion, up 0.5% from the 1st revision to July.

- Residential spending is up 0.5% from July, up 12.3% YTD.

- Nonresidential Buildings spending is up 1.8% from July, up 4.5% YTD.

- Non-building Infrastructure is down 0.5% from July, down 3.4% YTD.

Year-to-date through August posted at $806 billion, up 4.7% from same period 2016.

What you should know – Revisions:

Since the bottom of the recession in January 2011, through June 2017 (78 months), spending vs the prior month was 1st reported down 42 times. Values were revised up 64 times, but not all months turned positive. After revisions, spending was down vs the prior month fewer than 20 times.

Monthly values are revised the next two months after initial release. Spending has been revised UP 15x in last 18 months. The average revision in following two months is +1.0%. This table shows the growth before and after revisions this year. Notice, spending was 1st reported down vs the prior month 5 times through June. After revisions spending is down only twice.

All values for the year are revised again in following May data report. The final revision has been UP 49 of the last 53 months. Average post-annual revision 2016 +2.2%; 2015 +4.3%; 2014 +4.4%. The average post-annual revision for the last 4 years is just over 3%.

Year-over-year and year-to-date comparisons of construction spending are generally understated by about 2% to 3% until the final revision of spending data is posted in May the following year.

Year-to-date construction spending through August is posted at $806 billion, up 4.7% from same period 2016. However, the post-annual revision has already been applied to all months in 2016. The same revision will not be applied to 2017 data until May 2018 data is published next year, so current YTD is always understated. Based on post-annual revisions for the last 4 years, adjustments range between +2% and +4%. The most recent six months has averaged +2.4%. So YTD 2017 spending will very likely increase and could be in the range of 6% to 8%.

Market Specific Revisions

Specific markets vary both higher and lower than the average revision. For example Power has been revised on average +10%, while Educational was revised less than 2%. Highway and Transportation revisions have averaged less than 1% over the last 18 months.

Construction Spending Revisions After 1st Release Through August Data:

Every month this year except April has been revised UP. The April data looks like such an anomaly (largest monthly decline since the recession) that I expect next May we will see April get revised up by +1% to +1.5%. July data gets revised next month and I expect to see an additional +1% to +1.5%.

- Total Construction UP 49 of last 53 months, avg 3.7%/mo.

- Total Construction UP 17 of last 19 months, avg 2.5%/mo.

- Residential revised UP 30 of last 31 months, avg 6.8%/mo.

- Residential UP 18 of 19 avg 3.6%/mo.

- Commercial UP 18 of 19 avg 5.7%

- Educational UP 13 of 19 avg 1.7%

- Power UP 19 of 19 avg 10.7%

- Commercial/Retail May +6.7%, June +3.8%, July +3.7%

- Lodging May +4.3%, June +0.2%, July +1.4%

- Educational May -0.7%, June +3.4%, July -1.8%

- Transportation May +3.5%, June +2.1%, July -1.8%

Spending Forecast

2017 construction spending is expected to reach $1,252 billion, up 5.6% from 2016. Average annual rate of spending will increase to $1,300 at year end. I wouldn’t be surprised to see future revisions to Mar-Apr-May spending smooth out that erratic period and add to total $ 2017.

In my forecast, I rely on the revision data by market to add a conservative adjustment for expected normal revisions.

My current Forecast has spending year-to-date through August up nearly 6% over 2016. Spending in the 2nd half 2017 will increase 1.5% to 2% over the 1st half 2017 and will increase more than 5% over the 2nd half 2016.

- All sectors have already hit spending lows for the year and will increase 4% to 8% over the next six months.

- Infrastructure will finish the year with totals down 2%, but the annual rate of spending could potentially increase 8% from July to year end. 2018 shows 11% growth.

- Nonresidential Buildings may finish up 5% in 2017, the sixth consecutive year of growth. For 2018 expect 8% growth.

- Residential spending will be up nearly 12% for 2017, the sixth year over 9%. Spending growth in 2018 slows to 2%.

- Backlog and the share of spending within the current year from that backlog is at an all-time high for nonresidential buildings and non-building infrastructure.

- Public work for 2017 will finish down 1.5%. By far the largest public spending declines are in Environmental Public Works, especially Sewer and Waste Disposal.

- Public spending is headed for a sizable rebound in 2018, up 9%.

- Every large Public category is forecast to show solid growth from the 4th qtr 2017 through all of 2018.

- This analysis does not include any spending projections from an infrastructure investment bill.

- Largest declines 2017; Manufacturing -11% ytd; Environmental Public Works -16% ytd.

- Largest increases 2017; Office +10% ytd; Commercial +16% ytd; Residential +13% ytd.

See this article Construction Starts and Spending Trends 2017-2018 for more on spending trends

Construction Starts and Spending Patterns

9-26-17

Construction Starts and Spending trends may not be apparent unless you look deep into the last few years of data.

Construction spending is strongly influenced by the pattern of continuing or ending cash flows from the previous two to three years of construction starts.

Current month/month, year/year or year-to-date trends in starts often do not indicate the immediate trend in spending.

Power market starts and spending provides a good example. Power starts peaked in 2015 at an all-time high, up 142% from 2014 and more than the prior two years combined. Yet Power spending was down 6% in 2015 and up only 3% in 2016. This happened because Power starts were also at an all-time high in 2012, just below the 2015 level, and those starts drove 2014 spending to an all-time high, but then tapered off in 2015. Those peak starts from 2015 will still be contributing spending for several years to come, long beyond typical jobs, and that drives up typical spending growth because it adds more than typical number of months that contribute spending.

Power starts dropped 11% in 2016 and continue to drop in 2017. Year-to-date and year over year comparisons to 2016 show Power starts down in all respects. For the 1st six months of 2017, Power starts are down four out of six months compared to same month in 2016 and year-to-date through June is down a total 20%.

Even though Power starts have been declining since the 2015 high point, Power had several periods with an exceptionally high value of new starts, some of these periods 2x to 3x the normal rate of growth and a year or two longer duration than typical; late 2014, Jan-May 2015, Feb-Jun 2016 and again in Feb-Jul 2017. When we have old, long duration jobs that are still contributing to monthly spending, spending goes up. A large share of the cash flow or monthly spending from all those exceptional starts will occur in 2018 and 2019. Those jobs will elevate Power spending 15% to 20% in 2018 and also in 2019.

- Pattern of cash flows from construction starts is indicating substantial acceleration in spending over next six months in all sectors, perhaps most notable in infrastructure.

- Infrastructure jobs from 2014 with longer than average duration will continue into 2018. These break the average balanced cycle of one month of old jobs ending for every new month of jobs starting. That will increase spending in 2018.

This simplified example shows what happens to monthly spending growth when a long duration job first influences spending past the typical duration and then when it ends. In the example here, starts grow at 1% per month and have a typical duration of 5 months. One month has an unusually large project start that will last for 10 months. A typical month of spending has cash flow from 5 months of starts, but the long duration project creates 6 months of cash flows for the period beyond typical duration.

Notice what happens and when it occurs. When the large project starts it has no unusual affect on spending. When it first extends beyond typical duration, it has a massive +20% growth effect on spending, even though starts had only been increasing at 1%/month for the previous 5 months. When it ends it has a similar downward effect, again, even though starts had been increasing at 1%/month.

Spending growth (or declines), both when an extra large job causes it to increase and then when the extra job ends, is almost entirely influenced by the long duration project, not by normal monthly starts growth rate.

2017 construction spending is expected to approach $1,250 billion, up 6% from 2016. Average annual rate of spending is going to increase 5% from $1,240 to $1,300 at year end. I wouldn’t be surprised to see future revisions to Mar-Apr-May spending smooth out that erratic period and add to total $ 2017.

- All sectors have already hit spending lows for the year and will increase 4% to 8% over the next six months.

- Infrastructure will finish the year with totals down 2% to 3%, but the annual rate of spending could potentially increase 8% from July to year end. 2018 shows 10% growth.

- Nonresidential Buildings are up 4% in 2017, the sixth consecutive year of growth. For 2018 expect 8% growth.

- Residential spending will be up more than 10% for 2017, the sixth year over 9%. Spending growth in 2018 slows to 5%.

2017 construction starts through August total $482 billion, down 1% compared to revised 2016. If 2017 gets revised as expected, even by only 4%, it will show +3% growth over 2016, but we won’t see that growth in the data until next year.

- Starts revisions for the period 2008-2015 averaged +5.8%/yr. For the period 2012-2015 revisions averaged +4.0%.

- The smallest revision to starts data since 2008 was +3.5%/yr. 2016 year-to-date through August revisions are +11%.

- Previous year starts are always revised upwards. Therefore, current year starts year-to-date growth is always understated.

- Starts have been increasing at an average rate of 11%/year for the last 5 years.

- After revisions, I expect 2017 will be the highest amount of new construction starts in 13 years.

Manufacturing spending was expected to fall in 2017 after peaking in 2015 from massive growth in new starts in 2014. However, a few months of exceptional 2015 starts will elevate 2018 spending and late 2016 starts will elevate 2019 spending.

Office spending, down slightly (temporarily) due to timing of completions from old jobs, is on track to reach 10% growth in 2017. Starts have been increasing since 2010 with the strongest growth period of new starts from Sept 2016 through June 2017. So, for the next 10 months we may see year/year comparisons negative, but that high volume of starts from Sept 2016 to June 2017 is going to elevate spending in 2018 and 2019.

Commercial spending early reports for June and July are both well below that predicted by starts cash flows and may be prone to substantial revisions. Commercial spending revisions have been up 17 of last 18 months an average of 6.0%/month. (10-2-17 Commercial spending was revised up by 4% for both June and July) Commercial starts have been increasing every year since 2010.

Educational has seen a slow but steady growth in new starts since 2012. Current dip in spending are not expected to continue. Cash flow from starts is indicating a steady climb in spending from now through the end of 2018.

Healthcare starts from 2015 are ending unevenly, rather than smoothly, causing temporary dips in spending. Growth resumes by Sept-Oct.

Transportation Terminal starts in the first three months of 2017 were more than three times higher than any three-month period in the previous five years. While this helped turn 2017 spending positive, 2017 is still affected by uneven starts from two to three years ago holding down gains in the 2nd half. Transportation will show only a 1% gain in 2017 but double digits gains in 2018. The high volume of 2017 starts has the most affect on 2019 spending.

Highway spending in 2018 will benefit from a scenario exactly as described above in the cash flow chart. Projects that started in 2015 but that have unusually long duration will contribute spending in 2018 beyond the duration that typical projects have ended. It is not recent new starts but old ongoing projects that will increase 2018 spending by 6%.

Public Works cash flow from starts has been indicating declines in spending since last summer. In fact, declines in public works spending (down 20% YTD in Sewage Waste Disposal) is the biggest drag on Infrastructure spending in 2017. However, now spending declines are expected to turn to growth in the 2nd half 2017 and continue growth through 2018.

(This analysis does not include any spending projections from an infrastructure investment bill).

See August Construction Spending 10-2-17 for more trends in spending.

See Starts Trends Construction Forecast Fall 2017 11-8-17 for updated trends in New Starts.

See Backlog Construction Forecast Fall 2017 11-5-17 for updated trend in Starting Backlog for 2018

Why Many Get Construction Spending Wrong

9-2-17

Construction spending for July was released yesterday, posted at $1.211 trillion, down 0.6% from an upwardly revised June. This is the sixth time in seven months of 2017 in which the initial release for monthly spending is down from the previous month. This is actually a very normal occurrence.

The 1st release of monthly spending vs the previous month has been down 15 times in the last 21 months. This may be what leads some analysts and pundits to write that construction spending is heading to recession. Nothing could be further from the truth!

For the last 21 months, in which 15 first reports showed a decline vs the previous month, 18 of the monthly values were revised up. After revisions, only five months remain down vs the previous month. Seven months are still pending further revisions, almost always up.

Construction spending is highly prone to revisions. After the 1st release it is revised each of the next two months and once again the following year. Spending has been revised UP 48 of the last 52 months, 92% of the time. The average upward revision for the last five years is +3.2%/month. In the last 52 months the upward revision averaged 3.7%.

Construction spending revisions after first release of data:

- Total Construction UP 48 of last 52 months, avg 3.7%/mo

- Total Construction UP 16 of last 18 months, avg 2.6%/mo

- Residential revised UP 29 of last 30 months, avg 7.0%/mo

- Residential UP 17 of 18 avg 3.8%/mo

- Commercial UP 17 of 18 avg 6.0%

- Educational UP 14 of 18 avg 2.2%

- Power UP 18 of 18 avg 12.0%

- Commercial/Retail May +3.9%, June +2.6%

- Lodging May +3.8%, June +1.1%

- Educational May +2.8%, June +3.6%

- Transportation May +3.6%, June +2.3%

January through May values have already been adjusted twice in these reports. June has one more revision next month and July gets revised twice. It’s quite likely both June and July values go up. All 2017 months still get one more revision next year when the May data is released (July 1). The post-annual total revision for the last 15 mo averages +2%, close to the long term average. First release values are ALWAYS being compared to previous values that have already been revised, 92% of the time UP. So first release values almost always understate performance. Since July 1st 2017, all 2016 monthly values have been revised three times so monthly releases this year starting with May have the most understated initial % comparison year-over-year because an un-adjusted release is being compared to a 3x-adjusted value.

When judging performance of monthly spending, it is reasonable to predict spending will get revised UP from the first release. Therefore, the most immediate monthly analysis you read, if based on initial release, 92% of the time is under-stating the performance of construction spending.

Construction spending forecasting not only must rely on performance year-to-date, but also on predictive analysis of how much revision there may be to current values. As an estimate, if monthly spending is initially posted as 2% down, 18/mo.averages indicate it will end up at least +2.6% higher after revisions, so would be a positive 0.6% growth month.

A few closing points:

Construction Spending 1st release for July is $1.211 trillion. Expect this to be revised up. YTD Jan-Jun revisions are UP 1.8%. Historical revisions last 5 years predict the final July value will be up 3% from the 1st release.

Construction Spending AVG 2017 Jan-Jul YTD ($1.226tr) has reached an all-time high. We’ve now posted three consecutive quarters of spending all averaging above $1.220 trillion. Spending is on track to total $1.250 trillion for 2017, up 5.5% over 2016.

Construction Spending avg YTD = $1.226tr, is up YTD 4.7% with revisions through May. Without revisions, the 1st releases would have averaged only $1.208tr, up only 3%.

Commercial Retail, Office and Residential lead 2017 construction spending gains, all over 10%. Office spending is at a record high.

After 5 months of stalled construction jobs growth, August added 28,000 jobs and put 2017 growth back on track towards 250,000 jobs. YTD is up 135,000. March thru July added only 19,000 construction jobs. Jan+Feb added 88,000, ending a six-month period, Sep16-Feb17, that added 167,000 jobs.

Harvey related jobs will be muted by jobs lost, I suspect for at least two months. There will be a period of slack records that will take some time to see the real effects of Harvey.

Further reading on this topic

June Construction Spending – What’s Up, or Down?

Jobs vs Construction Volume – Imbalances

8-8-17

From January 2001 to June 2017, jobs growth exceeded construction volume growth by 13%. The attached plots show the imbalances in growth.

Jobs growth is # of jobs x hours worked.

Volume is construction spending adjusted for inflation, or constant $.

Sometimes rapid spending growth is accompanied by higher than average inflation. This occurred in the 1990’s and again in 2005-2006. While spending seems to indicate rapid growth, much of the growth in cost is inflation and volume growth can be significantly lower, even sometimes negative, as occurred in 2005-2006. However, jobs growth during these rapid spending growth periods appears to track much more in line with spending growth. This leads to over-hiring and a loss of productivity occurs.

There are two distinct periods when jobs growth advanced more rapidly than real construction volume, 2005-2006 and mid-2015 to mid-2017. In the eight year period in between, either jobs fell faster or, after January 2011, volume increased faster. If spending growth is used to compare, then jobs growth falls far short of construction spending. But, due to inflation, spending is not the correct parameter to compare to jobs. Jobs must be compared to volume. Since 2001, the imbalance shows jobs growth has exceeded volume growth.

2001 through mid-year 2017, jobs exceeded volume growth by 13%.

2001-2004 jobs and volume growth were nearly equal.

2005-2006 jobs growth exceeded volume growth by 20%. During this period, construction spending and volume reached a peak. From late 2004 into early 2006, we experienced 20% growth in spending, the most rapid growth period on record. But that was also the period of the most rapid inflation growth on record. Residential volume peaked in early 2006 but then dropped 20% by the end of 2006. Nonresidential spending was increasing, but almost all of the growth was inflation. Nonresidential volume remained flat through 2006. Inflation was greater than spending growth, so volume declined. Although volume declined, hiring continued and jobs increased by 15%.

2007-2010 volume exceeded jobs growth by 4%. Spending decreased by 30%. Both volume and jobs were in steep decline. More jobs declined than volume, however, this period started with nearly 20% excess jobs. For January 2010 to January 2011, jobs bounced around near bottom, but volume dropped 8% more. 2010 ended with an excess of 15% jobs. January 2011 was the low-point for jobs.

2011-June 2015 volume exceeded jobs growth by 10%. Spending increased by almost 40% and inflation was relatively low at only 3%/yr. This period helped absorb more than half of the excess jobs that were created in 2005-2006 and remained after 2010. By mid-2015, jobs exceeded volume by only 7%.

June 2015-June 2017 jobs growth exceeded volume by 7%. Spending increased by 7%, but inflation was 7% over the same period. Although volume was up and down, over this two-year period through June 2017 we posted zero growth in volume. All of the increase in spending was inflation. Jobs increased 7% in two years.

For the last 5 years, 2012-2016, jobs averaged 4.5%/yr. growth Construction spending averaged 8.5%/yr. growth. Inflation, currently hovering around 4.5%, averaged about 3.5%/yr. during this period. So real volume growth was only 4% to 5%. In the first few years of the recovery, 2011-2014, the gap narrowed and volume improved over jobs, but for the last two years, jobs have been increasing faster than volume.

I do expect spending to continue at a 6% to 7% growth rate at least through 2018. But also, I expect inflation at 4% to 4.5%. If the spending forecast holds, and if jobs growth comes into balance, then that would indicate only a 2% to 3% jobs growth rate from now through 2018.

Also SEE Construction Jobs Growing Faster Than Volume 5-5-17

and Is There a Construction Jobs Shortage? 3-10-17

Here is the 11-7-17 extension of latest info Construction Jobs / Workload Balance

ARCHIVE – Construction Inflation Index Tables 2016 data

8-6-17 SEE ESCALATION / INFLATION INDICES For Current Updated Indices

10-24-16 original posted

1-27-17 updated index tables and plots

8-6-17 archived this for 1-27-17 2016 content – Linked Master Index Tables has updated data

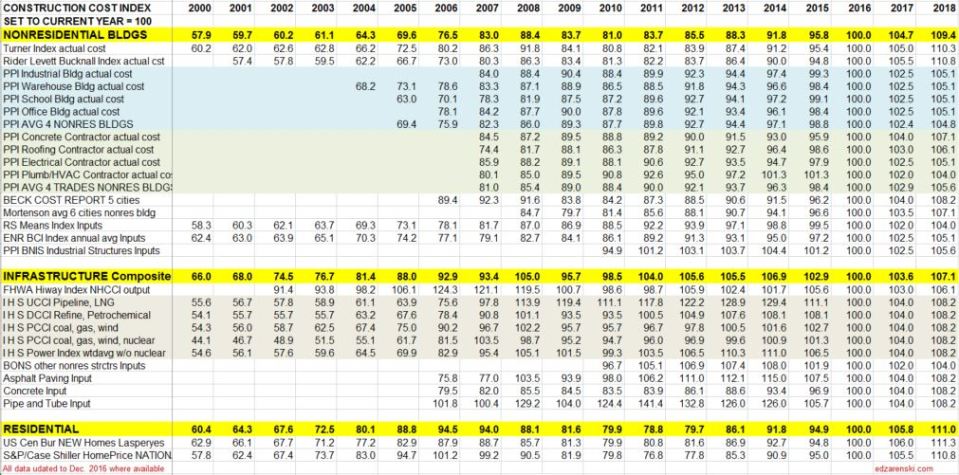

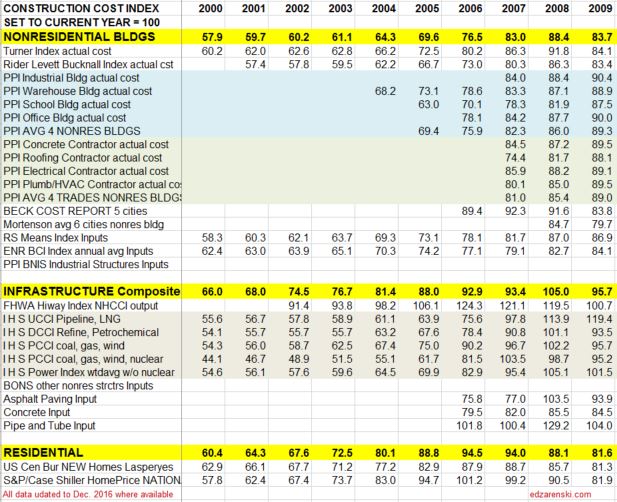

Construction Cost Indices come in many types: Final cost by specific building type; Final cost composite of buildings but still all within one major building sector; Final cost but across several major building sectors (ex., residential and nonresidential buildings); Input prices to subcontractors; Producer prices and Select market basket indices.

Residential, Nonresidential Buildings and Non-building Infrastructure Indices developed by Construction Analytics, (in BOLD CAPS), are sector specific selling price composite indices. These three indices represent whole building final cost and are plotted in Building Cost Index – Construction Inflation below and also plotted in the attached Midyear report link. They represent average or weighted average of what is considered the most representative cost indicators in each major building sector. For Non-building Infrastructure, however, in most instances it is better to use a specific index to the type of work.

Click Here for LINK to Cost Inflation Midyear Report 2016 – text on Current Inflation

All actual index values have been recorded from the source and then converted to current year 2016 = 100. That puts all the indices on the same baseline and measures everything to a recent point in time.

Not all indices cover all years. For instance the PPI nonresidential buildings indices only go back to years 2004-2007, the years in which they were created.

SEE Construction Inflation Index Tables For 2017 Tables

SEE BELOW FOR LARGER IMAGE

When construction is very actively growing, total construction costs typically increase more rapidly than the net cost of labor and materials. In active markets overhead and profit margins increase in response to increased demand. When construction activity is declining, construction cost increases slow or may even turn to negative, due to reductions in overhead and profit margins, even though labor and material costs may still be increasing.

Selling Price, by definition whole building actual final cost tracks the final cost of construction, which includes, in addition to costs of labor and materials and sales/use taxes, general contractor and sub-contractor overhead and profit. Selling price indices should be used to adjust project costs over time.

quoted from that article,

R S Means Index and ENR Building Cost Index (BCI) are examples of input indices. They do not measure the output price of the final cost of buildings. They measure the input prices paid by subcontractors for a fixed market basket of labor and materials used in constructing the building. These indices do not represent final cost so won’t be as accurate as selling price indices.

Turner Actual Cost Index nonresidential buildings only, final cost of building

Rider Levett Bucknall Actual Cost Index in RLB Publications nonresidential buildings only, final cost of building, selling price

IHS Power Plant Cost Indices specific infrastructure only, final cost indices

- IHS UCCI tracks construction of onshore, offshore, pipeline and LNG projects

- IHS DCCI tracks construction of refining and petrochemical construction projects

- IHS PCCI tracks construction of coal, gas, wind and nuclear power generation plants

Bureau of Labor Statistics Producer Price Index only specific PPI building indices reflect final cost of building. PPI cost of materials is price at producer level. The PPIs that constitute Table 9 measure changes in net selling prices for materials and supplies typically sold to the construction sector. Specific Building PPI Indices are Final Demand or Selling Price indices.

PPI Materials and Supply Inputs to Construction Industries

PPI Nonresidential Building Construction Sector — Contractors

PPI Nonresidential Building Types

PPI BONS Other Nonresidential Structures includes water and sewer lines and structures; oil and gas pipelines; power and communication lines and structures; highway, street, and bridge construction; and airport runway, dam, dock, tunnel, and flood control construction.

National Highway Construction Cost Index (NHCCI) final cost index, specific to highway and road work only.

S&P/Case-Shiller National Home Price Index history final cost as-sold index but includes sale of both new and existing homes, so is an indicator of price movement but should not be used solely to adjust cost of new residential construction

US Census Constant Quality (Laspeyres) Price Index SF Houses Under Construction final cost index, this index adjusts to hold the build component quality and size of a new home constant from year to year to give a more accurate comparison of real cost inflation

Beck Biannual Cost Report develops indices for only five major cities and average. The indices may be a composite of residential and nonresidential buildings. It can be used as an indicator of the direction of cost but should not be used to adjust the cost in either of these two sectors.

Mortenson Cost Index is the estimated cost of a representative nonresidential building priced in six major cities and average.

Other Indices not included here:

Consumer Price Index (CPI) issued by U.S. Gov. Bureau of Labor Statistics. Monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. This index in not related at all to construction and should never be used to adjust construction pricing.

Leland Saylor Cost Index Clear definition of this index could not be found, however detailed input appears to represent buildings and does reference subcontractor pricing. But it could not be determined if this is a selling price index.

Sierra West Construction Cost Index is identified as a selling price index but may be specific to California. This index may be a composite of several sectors. No online source of the index could be found, but it is published in Engineering News Record magazine in the quarterly cost report update.

Vermeulens Construction Cost Index can be found here. It is described as a bid price index, which is a selling price index, for Institutional/Commercial/Industrial projects. That would be a nonresidential buildings sector index. No data table is available, but a plot of the VCCI is available on the website. Some interpolation would be required to capture precise annual values from the plot. The site provides good information.

The Bureau of Reclamation Construction Cost Trends comprehensive indexes for about 30 different types of infrastructure work including dams, pipelines, transmission lines, tunnels, roads and bridges. 1984 to present.

Click Here for Link to Construction Cost Inflation – Midyear Report 2016

1-27-17 – Index updated to Dec. 2016 data

8-6-17 SEE Construction Inflation Index Tables For Updated 2017 Indices

June Construction Spending – What’s Up, or Down?

8-2-17

Here’s some headlines this month on the June Construction Spending release: Plummets in June; Largest one month drop in 15 years; Clearly Decelerating; US Construction Spending Just Collapsed; and my personal favorite, Construction Spending Plummets to Economic Crisis Levels.

Frankly, I have much more trust in my data than to suggest we are at crisis levels.

In the latest Census construction spending report, June spending dropped 1.3% from May, but May was revised down -0.7%. The consensus of economists predicted spending would be up +0.5% (from the original May value), so the data posted is actually 2.5% below consensus estimates.

I expected May to get revised up 0.6% and the initial June release would be flat vs the revised May value. So the actual came in 2.6% below my expectation.

June construction spending was posted at $1.205 trillion, down 1.3% from May and down 2.7% from March. With the revised data, the May Year-to-date (YTD) vs 2016 was only +5.5% (not +6.1% as initially reported) and for June it’s now +4.8%.

My opinion is this preliminary June value appears suspect. This is sort of like driving a well maintained car that gets 30 mpg and all of a sudden the gauges indicate 20 mpg for the latest tankful of gas. Although the road may be a little bumpy, there does not seem to be any serious mechanical problems, so we have to ask, why did gas mileage drop so much?

The April decline and the Apr-May-June decline are the single largest monthly and 3-month total non-recessionary declines on record. We would need to look at recession data to find similar declines. Spending drops like this just don’t normally occur, especially when cash flow patterns from starts predict 4% growth during the 3-month period. That’s a 6.7% miss over 3 months.

The largest declines in the June Seasonally Adjusted Annual Rate (SAAR) construction spending were Highway and Educational, together 60% of the total monthly decline. (There are other markets with greater mo/mo% declines, however most of those markets have a very small share of the total spending so don’t amount to much). Almost all of the largest declines are public work. In fact, the initial June release shows every public market declined. However, all ten other public markets together don’t equal half of the declines generated by these two major markets. Furthermore, for the past 3 months Highway spending shows a decline of 12.5%, and Educational spending is down 7.6% in 4 months. A review of data back to 2005 shows neither of these markets have ever had any periods where they’ve experienced declines of this magnitude. These would be record declines if they stick. Market trend data simply is not indicating to expect record declines at this time. So I consider these data suspect.

Construction spending initial release is always preliminary data. The June value, released August 1st, will be revised in each of the next two reports and then once again next year when all 2017 data is reviewed. The average revision to June spending data over the last 4 years (similar growth years to current expectations) is +4.8%.

There are three more opportunities for revision to the June data and two more to the May data. We will have a much better idea what really happened on October 1st, but we won’t know the final outcome until the final 2017 revision on July 1, 2018.

So, what data seems to indicate a trend contrary to current declines? The last 12 months of Dodge Data new starts for nonresidential buildings are the highest since 2008 and they peaked from August to October. Residential starts, at their highest since 2006, peaked from December’16 to March’17. Backlog is at an all-time high. There is no indication here that spending will plummet.

Also, one month of Educational or Highway new starts each generate about $250 to $300 million per month in spending, for the next 24 to 36 months. Normally, with some variation, we have the current month of new starts coming into backlog and one month of old starts ending. Since starts have been normal or high recently, the spending declines posted in June would imply that we’ve lost two to three months of backlog from current spending. Again, there are no indications that we have an extreme imbalance or a canceling of backlog.

Most of the nonresidential spending occurring right now is from projects that started between mid 2015 and the end of 2016. Nonresidential buildings projects that started in 2015 or earlier still make up one third of the spending in the 1st half of 2017. Non-building infrastructure projects that started in 2015 and earlier contributed 50% of spending in the 1st half of 2017. Residential projects have shorter duration so most spending is from more recent jobs, but we hit a 10 year peak in new residential starts just a few months ago. All sectors have fluctuations in spending and have down months but the index of long term cash flows out to completion shows normal backlog and spending growth across every sector.

I’m inclined to expect substantial upward revisions to June construction spending in the next two releases. No other data supports a big June drop.

Keep in mind, current construction spending is always being compared to previous months revised spending and growth is almost always being understated. Monthly spending has been revised UP 45 times in the last 48 months. All previous months and all 2016 data have been revised several times. The average revision to ALL spending data over the last 4 years is +3.9%/month. Since January 2016, the average revision is +3.0%/month. The average revision to June spending data over the last 4 years is +4.8%.

June data is un-adjusted preliminary data. Many of the news articles declaring construction spending was a miss are based on this preliminary data which very often gets revised away in following months. For example, The 1st 6 months of 2016 have already been revised up, three times each, by a total of 2.5%. All the months YTD in 2017 still have pending revisions. June 2017 vs June 2016 shows a percent growth of only +1.6%, but June 2016 has already been revised up by 4.7% and June 2017 has not yet been revised at all. June 2017 has a 90% chance of being revised up.

I predict after all the revision are in we will see that June spending did not drop to a low of $1.205 trillion, but that it was closer to $1.250 trillion.

Nonres Bldgs Construction Spending Midyear 2017 Forecast

7-24-17

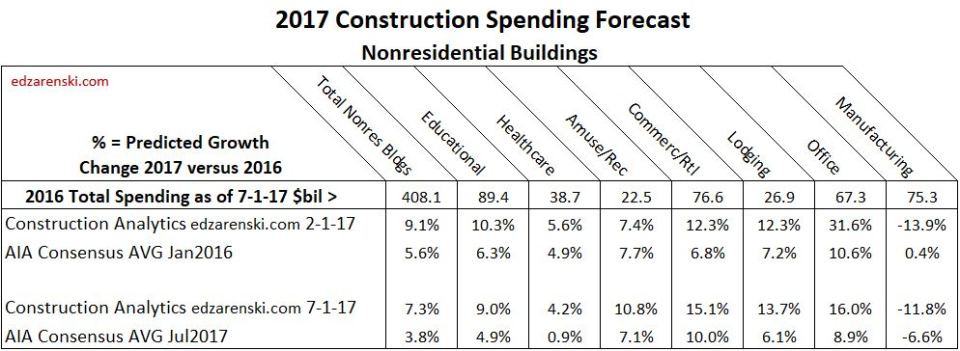

The AIA recently published the Nonresidential Buildings Consensus Forecast Midyear 2017 report. The consensus of seven firms projects spending growth for nonresidential buildings at 3.8% for 2017 and 3.6% for 2018. The largest growth in the AIA forecast for any building type for both years is 10% for 2017 Retail & Other Commercial. The highest reported total annual prediction from any firm is 4.4% for 2017 and 5.5% for 2018. AIA Midyear Consensus Report July 2017

Construction Analytics forecast for nonresidential buildings construction spending growth is +7.3% for 2017 and +10.7% for 2018. Growth in 2016 was 7.5%.

Year-to-date (YTD) spending for the 1st 5 months of 2017 is up +5.2%, led by Office and commercial, both near 15%. Estimate-to-complete (ETC) for the final 7 months is forecast at +8.1%. Total spending for Nonresidential Buildings in 2017 is forecast to increase 7.3% = $438 billion.

If spending were to slow to 3.8% growth for 2017, since YTD growth is already 5.2%, the rate of growth in the final 7 months would need to fall to only 2.4%. However, the predicted cash flow from construction starts shows very strong spending growth in the 2nd half 2017 and into 2018. Nonresidential Buildings construction starts for the last 12 months posted the highest average since 2007-2008. This is helping boost spending.

Outside of recession years, nonresidential buildings construction spending for the year dropped below 4% annual growth only twice in 24 years, since data has been tracked. In fact, right now spending needs to grow at 4.5% just to stay ahead of construction inflation. So any forecast of spending growth below 4.5% actually might suggest that construction is not expanding, but is contracting. All indications are that there are no recessionary effects right now and economic activity does not suggest we are headed for a non-recession low spending for nonresidential building construction. I don’t expect spending to drop to 4% growth for the next three years.

The pattern of nonresidential buildings construction starts for the last 30 months is indicating spending increases in the 2nd half of 2017 and is setting up 2018 for the highest ever starting backlog and record spending. Even if starts crash to zero growth for the remainder of the year, 2017 spending would drop by less than 1% and we still begin 2018 with record backlog.

New Office construction starts for the last 12 months are the best ever recorded, on track to reach a total 50% growth over two years. Retail/Commercial starts have averaged year-over-year (YOY) growth of greater than 10%/year for the last three years. Educational starts averaged YOY growth of 8%/year for the last two years. These three markets comprise 60% of all nonresidential buildings. Healthcare starts have quietly increased to a record high over the last 12 months. Every market except manufacturing will finish 2017 with new starts totals near or at post recession highs. Manufacturing reached record high starts in 2014 and record spending in 2015. All construction starts $ data in this report references Dodge Data & Analytics starts data.

Construction spending for Commercial/Retail, Lodging and Office construction all remain very strong with 2017 total growth near 15%. Educational (+9%) and healthcare (+4%) both show sizable gains after years of little to no growth.

92% of all construction spending in 2017 is already in backlog projects.

A scenario that would have Office spending drop down to 8.9% annual growth from the track it is on today (+15.4% YTD) would require a highly improbable and unprecedented non-recessionary decline in spending in the remaining months of 2017. To grasp the enormity of the decline needed, it would take canceling 8% of all ongoing office projects or new starts for the remainder of the year would need to drop by 50%.

Educational will show an increase in YTD gains in the 3rd quarter because increasing spending in 2017 will be measured against the lowest quarter (3rdqtr) in 2016. Healthcare may not show sizable YTD gains until 4th quarter, for which 2016 reached lowest spending of the year and 2017 will reach highest.

Total nonresidential buildings spending growth accelerates to 10+% in 2018, led by institutional and office spending.

Nearly all nonresidential buildings construction starts in 2016 are still contributing to spending. Since originally posted they have been revised up by 16%. Since most spending from new starts (approximately 50%) occurs in the year following the start, early spending projections based on original posted starts $ may understate 2017 spending.

Nonresidential construction is comprised of two very different sectors, nonresidential buildings and non-building infrastructure. Infrastructure spending is quite erratic, while nonresidential buildings spending, with only slight variation, has been climbing at a strong steady pace for more than 4 years. Some analysts track nonresidential total spending, but these two sectors perform so differently it is important to break them apart to track trends. Buildings spending is up 2% from Q2’16 and up 5% YOY. In the 2nd half 2017 YOY spending is expected to reach 8% over the same months from 2016. Worthy of note is that non-building infrastructure spending, even though down slightly, just experienced two years of record highs. It will hold down the overall nonresidential total performance, but still finish 2017 near record highs.

See this article from February comparing my starting forecast compared to the Jan 2017 AIA Consensus Nonresidential Bldgs 2017 Forecasts Vary