Home » Spending (Page 11)

Category Archives: Spending

Predictions – 2015 Spending for Nonresidential Construction Markets

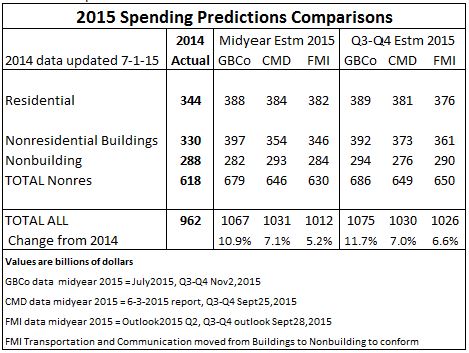

Compiled in one neat table, here are 2015 predictions from eleven construction data firms for spending growth in nonresidential markets. Several firms provided mid-year estimates and recent estimates. Some provided only mid-year and some just recent estimates. Midyear estimates are separated so changes can be seen to current estimates.

Actual spending put-in-place for September year-to-date (YTD) became available November 2nd and new construction starts for October became available November 23rd.

There is a wide range of variance in predictions with the closest spreads at 9% and the widest spreads in lodging and manufacturing markets. It will be interesting to look back at this chart when the final numbers for 2015 become available in February 2016 to see how we did.

- One recent estimate published in Engineering News Record (ENR) magazine 11-16-15 lists 7% growth for manufacturing buildings. Each of the first nine months in 2015, the year over year growth has ranged between 40% and 60%, so the huge growth expected has been apparent for some time. Even if the last three months drop 15% below the current average we will still finish the year up 40%.

- For growth in educational buildings to fall to only 3%, the last three months would need to drop 15% below the current six month average, a change we will not very likely see.

- The spread on lodging is 18%, from the low estimate of 15% to high of 33%. YTD lodging through nine months is up 31% over last year. To finish at less than 25% growth in 2015, spending for the next three months would need to drop 20% from current levels.

We get a chance to tweak these numbers a little tighter when October spending gets released on December 1st.

Construction Spending – What You Need to Know About YTD Mo/Mo Yr/Yr

Common comparisons published in news reports for construction spending are, from best to worst:

- Current year-to-date vs same period previous year. YTD

- Current month vs previous month. Mo/Mo or MOM

- Current month vs same month last year. Yr/Yr or YOY

- Number of months to current value since last time that value achieved.

In some cases a comparison uses Not Seasonally Adjusted (NSA) dollars and in other cases Seasonally Adjusted Annual Rate (SAAR) dollars. NSA dollars is the actual amount spent within the month. SAAR dollars represents the annual rate that monthly amount would generate based on the normal proportion typical spent within that month. Typical spending is always much higher in summer months than winter to produce the same SAAR.

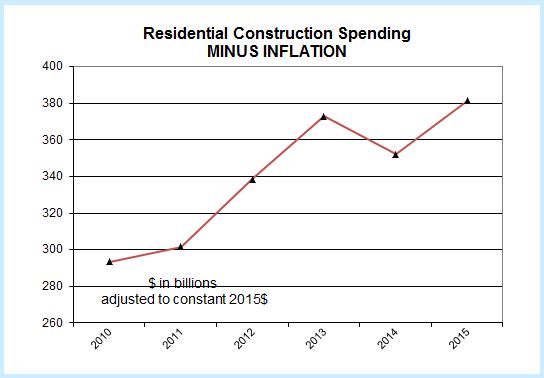

Year-to-date is the best comparison. It increases in strength as more months are added to the YTD. It is a value that gives a strong indication of growth over the previous year. Comparisons must be made using Not Seasonally Adjusted (NSA) dollars. Although it does lack adjustment for inflation, only one year of inflation is involved. Not adjusting for inflation is explained as the difference between current dollars and constant dollars.

Current month to month (MOM) comparisons are not generally affected by inflation but may not give a clear indication of movement due to monthly fluctuations. Comparisons absolutely must be made using Seasonally Adjusted Annual Rate (SAAR) dollars. It is a gross error to make month to month comparisons using NSA dollars, since there is a normal spending curve that shows the percent of total annual spending can vary considerably from month to month, sometimes by as much as 10%. This variation is accounted for in the SAAR.

When comparing to the same month last year (YOY), the question arises, “Is any big change in YOY caused by the current month performance or by the performance in the same month last year?” Again, YOY is missing adjustment for one year of inflation. Comparison can be NSA or SAAR dollars.

Number of months/years since current value was last achieved is almost always presented as a current dollar comparison. When dealing with cost, because of the long duration often involved it would be much better if it were a constant dollar comparison to account for construction inflation. However, construction inflation may not be readily available and this type of comparison is rarely if ever published using constant dollar comparisons. Comparison should use either entire year total dollars or should use SAAR dollars.

Current dollars = dollars are reported in the value of the year reported 2008=2008$, 2015 = 2015$. 99% of news reports use current dollars and therefore do not account for the influence of inflation.

Constant dollars = all dollars adjusted to represent dollars in the year of comparison. Adjusts for inflation so 2008$ in this case are converted to equivalent 2015$.

It’s not to hard to understand why we need to use constant dollars when you think of it in terms of buying products like food or heating oil. Today heating oil costs $1.90/gallon. In 2008 heating oil cost $3.50/gallon. So, with respect to oil, $350 in 2008 dollars is no different than $190 in 2015 dollars.

In addition to the Year-to-date growth values, here’s two more less common stats for looking at the same information.

Percent change from the last cycle high current$ (contant 2015$)

- Residential – Q1 2006 $390b vs $$680b -43% (-50%)

- Nonresidential Buildings – Q1 2008 $392b vs $$439b -11% (-22%)

- Nonbuilding Infrastructure – Q1 2008 $298b vs $$286b +4% (-10%)

Percent change from the recent recession low current$ (contant 2015$)

- Residential – Q1 2011 $390b vs $$239b +64% (+48%)

- Nonresidential Buildings – Q1 2011 $392b vs $$267b +49% (+35%)

- Nonbuilding Infrastructure – Q1 2008 $298b vs $$243b +22% (+13%)

Constant dollars makes a huge difference in the statistics. Just take a look at Nonresidential buildings. Current dollars would indicate we are now only 11% below the previous high and we’ve had growth of 49% from the recession low. Constant dollars adjusting for inflation shows we are still 22% below the previous cycle high and we’ve had growth of only 35% since the recession lows.

You can find a complete section providing constant dollar cost comparison in my quarterly report. Access the report through the Featured Economic Report tab at the top of this blog

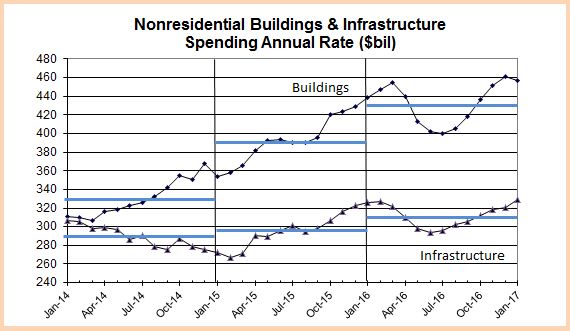

Erratic Pattern Ahead for 2016 Construction Spending. Why?

The good news is 2016 construction spending will be up across the board, although growth will vary between the three major sectors, residential, nonresidential buildings and nonresidential infrastructure. This post is about how we will get there.

This plot shows a three year pattern of spending for nonresidential construction. The seasonally adjusted annual rate is plotted every month and the horizontal bars show the total average spending for each year.

I often include a linear trend line in my plots because it’s good to be reminded of the long term direction and rate of growth rather than the monthly fluctuations. I’ve removed the trend lines from this plot to make a point. A fairly typical growth year shows spending finishing the year at a higher rate than when we started. The total spending for the year (shown by the horizontal bars) is the sum of the unadjusted monthly values, which is the same as the average of the monthly adjusted rates of spending. The plot above shows spending for buildings totals of $330 billion in 2014, $390 billion in 2015 and $430 billion in 2016.

If spending always occurred evenly we would see a smooth constant slope plot line indicating the rate of growth, sometimes punctuated with minor monthly declines but over the long term up at a constant rate. The plot for buildings shows a pretty constant growth pattern from March 2014 to March 2016. We see a few slight monthly dips and a flat spot in mid-2015, but overall fairly constant growth.

That will all change in 2016.

The plot shows both buildings and infrastructure will experience multi-month declines in 2016. By midyear both will dip so low that the year over year comparison will drop to near zero percent. Spending on buildings will drop more than 10% from the 1st quarter 2016 high to the midyear low. (edit 11-16. Most recent analysis is showing the nonresidential buildings peak and drop is moved out about 4 to 6 months. The plot above does not reflect this most recent analysis.) Infrastructure will drop in a similar pattern but not as dramatically. Both will resume growth and finish the year at or near the yearly high. Together these major sectors make up 60% of total construction spending with residential being the other 40%. The magnitude of these declines will be large enough to drag total construction spending down for the period, but it too will resume growth and finish the year well above where it started.

What causes that pattern?

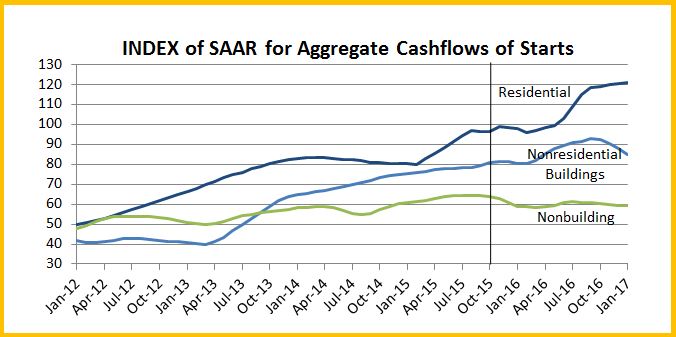

Spending in any given month is the sum total contributed by all the projects that started and are currently underway. That includes spending from projects that started recently with foundations just coming out of the ground and also projects that started 18 to 24 months ago that are near completion and near ready for occupancy. Spending is affected by the pattern of starts recorded over the previous 24 months. Only if that pattern is even in growth will spending be even in growth.

Let’s make some assumptions for an example that should be easy to understand.

- All projects take 20 months to build.

- The construction budget gets spent at a constant rate of 5% per month.

Of course, reality never occurs as simple as that, but it makes for an easy to understand example. With these simple assumptions we know this about spending;

- Every month includes some spending from all starts over the previous 20 months.

- New starts in any given month contribute only 1/20th or 5% to total spending that month.

- Predicted spending 3 months out includes only 15% from new starts, 4 months out 20%, etc.

Now, back to reality.

Nonresidential buildings spending in 2016 includes projects that started all the way back to mid 2014. From April 2014 to April 2015, concentrated mostly in mid to late 2014, there were several instances where monthly starts exceeded the previous month by 50%-60%, then settled back. Those were great months and indicated a huge growth spurt in nonresidential building construction. We see that growth from early 2014 all the way up to a peak in early 2016. Nonresidential buildings spending experienced growth of 9% in 2014 and 19% in 2015, with 9% growth predicted for 2016.

We don’t typically see a seesaw pattern in spending from the starts when all the projects are ongoing at the same time, we see flatter and steeper rates of spending growth. The six biggest months from that period averaged more than 30% higher than the current rate of new starts growth. So we’ve had a pause in the rate of increase for new starts. We see the big affect on the spending pattern when a very large volume of spending from starts 18 or 24 months ago reaches completion and drops out of the current month spending. That is what will happen in 2016.

New 2016 nonresidential buildings starts is not the cause of a 10% dip in spending in 2016. It is the completion of a very large volume of starts from 2014 that will no longer be contributing a large share to monthly spending. That will work itself out by year end. But for those who do not look at the patterns that contribute to current spending it will create quite a stir. Three to five months of consistent declines in spending will look like the end of recovery in nonresidential construction. It is not the end.

Construction Spending 2015 and 2016

Here’s a peak at expected annual Construction Spending for 2015 and 2016.

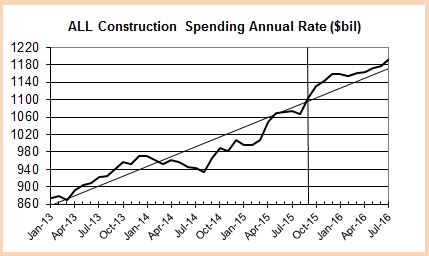

My predictions (GBCo) include the latest actual construction spending data released Nov. 2nd for September spending. This updated projection also includes revised future spending based on Dodge Data & Analytics construction starts released at the DDA Outlook 2016 conference Oct. 30th. My prediction for total spending in 2015, now at $1.075 trillion, hasn’t changed much (up 0.7%) since August. However, for next year my projection has increased from $1.150 to now expecting total spending of $1.190 trillion in 2016. Both projections will be further refined in my winter economic report.

Why are my predicted values so much higher than other estimates?

I put emphasis on using the cash flows from all previously recorded construction starts to predict future construction spending. I’ve talked about and documented in past reports the correlation between these two data sets. For 2015, with only three months left to go, 80% to 90% of all starts that will generate spending in the final three months are already in place.

Very little affect on total 2015 spending will be brought about by new construction starts in the 4th quarter. New starts could crash to a level less than one half of current trends and that would still not affect total spending enough to get below $1.050 trillion for the year. In order to have the final total spending come in less than $1.040 trillion, the rate of spending for each of the next three months would need to drop off to the level of a year ago. That is not what the cash flows are indicating. In fact, cash flows are indicating spending will increase in the final three months of 2015. The cash flow plot provides us with the direction and the rate of change, but not the actual value of spending.

With the September actual spending values included in the data, the statistical average of predicted spending for 2015 is $1.073 trillion. My cash flow analysis by sector predicts 2015 will finish at $1.075 trillion. In 11 out of 14 years, the actual final value has been within 0.5% of the predicted.

The statistical analysis gives a predicted range for total 2015 annual spending between $1.066 trillion and $1.086 trillion. The actual spending total has not fallen outside the statistical range since 2001, as far back as I’ve been tracking the data. I’m confident that total spending for the year will fall within this predicted range.

Construction Spending Projected 2015 Totals

Here’s a comparison of projections for total construction spending in 2015.

My numbers (GBCo) include the latest actual construction spending data released Nov. 2nd for September spending. This updated projection also includes revised future spending based on Dodge Data & Analytics construction starts released at the DDA Outlook 2016 conference Oct. 30th. My prediction for total spending in 2015, now at $1.075 trillion, hasn’t changed much (up 0.7%) since August. However, for next year my projection has increased from $1.150 to now expecting total spending of $1.190 trillion in 2016. The 2016 projection will be further refined in my year-end report.

With the September spending values in the data, the statistical average predicted spending for 2015 is $1.073 trillion. My cash flow analysis by sector predicts 2015 will finish at $1.075 trillion. In 11 out of 14 years, the actual final value has been within 0.5% of the predicted.

The statistical analysis gives a predicted range for total 2015 annual spending between $1.066 trillion and $1.086 trillion. The actual spending total has not fallen outside the statistical range since 2001, as far back as I’ve been tracking the data.

Here’s a summary of predictions for several of the major markets. Again, my predictions from earlier in the year haven’t changed too much.

In today’s data release from U.S. Census, spending for manufacturing buildings was lowered in both July and August, and September came in lower than I expected. That is the primary mover in the lower prediction for nonresidential buildings. Spending for manufacturing buildings is at an all-time high. Through September, spending on new manufacturing buildings has already reached an all-time annual high. Manufacturing buildings helped 2015 spending for nonresidential buildings reach 19% growth but this won’t continue and I expect 2016 growth of 10%.

Residential spending has been a nice surprise to the upside. The current rate of growth for the last 12 months is 17%/year and this rate of growth is expected to continue again in 2016.

Nonresidential Buildings Construction Spending 2015 – How Do Industry Predictions Compare?

Throughout the year a number of firms provide predictions of various construction data. Some firms provide estimates for all segments of construction. More firms provide estimates only for spending on nonresidential buildings. This is a summary of various firms estimates published in the 2nd quarter and also for those who’ve updated their estimate recently.

The current available spending data through August allows an analysis of a select data set that gives a prediction of the year end result within +/- 1.5%. My current data predicts 2015 will finish with nonresidential spending at $393 billion, with a potential range between $387 billion and $400 billion. We will have even better data on November 2nd when the US Census publishes construction spending for the month of September. Once the September data is incorporated into the monthly totals, an analysis of a select data set provides a prediction of the year-end totals that has not varied more than +/- 1% from the end-of-year actual since 2002, as far back as the market data is available.

Residential Construction – Not All Data Tells The Same Story

The latest New Housing Starts numbers were released today. Residential growth is looking good and based on several inputs, I’m predicting an increase in residential construction spending next year. But let’s take a look at the variance you might get when looking at different data sets.

All the data below represents residential construction growth for the period from January 2011 until current, the last 4 years 8 months

New Construction Starts in $ (by Dodge Data Analytics) +19%/yr

New Housing Starts (number of new housing units) +20%/yr

Total Construction Spending +12.5%/yr

Volume (construction spending minus construction inflation) +7%/yr

The obvious first question is why don’t all the data agree? Without a lot more information on housing that cannot be answered here, but there are a few reasons that can be considered as cause for variation;

- the average size of housing units being built

- the quality of the components built into the housing units

- the cost to the contractor for the materials used

- the cost of labor wages to build the housing unit

I’m sure there are other reasons to consider as this is not intended to be a complete list of what might cause variances between starts and spending, but it does highlight that starts does not give an exact indication of the growth in spending. There is a fairly consistent growth rate in starts of 20%/year and yet construction spending in current dollars has been growing at only 12.5%/year. Furthermore, a sizable portion of that spending growth is just for inflation. After inflation is taken out we see real construction volume in constant 2015$ has been growing at only 7%/year.

I don’t have an answer to explain these variances. I’m highlighting the data to show these variances exist and we can’t always rely on one data set exclusively. Perhaps this will initiate a discussion as to why these data vary by so much.

Construction Spending Market Performance of Major Nonresidential Buildings 2015-2016

The Construction Spending BOOM in 2015 is being led by spending on nonresidential buildings. Spending on nonresidential buildings year-to-date (YTD) is +20%, +$41 billion. For housing the YTD is +11%, +$24 billion and for nonbuilding infrastructure projects YTD is -2.5%, -$5 billion.

Let’s take a look at the current growth trends to find out where they are headed.

In 2004-2006, residential spending was 55% of all construction spending. The annual growth in 2004 was 19% and in 2005 it was 15%. For the last 5 years residential spending has been only 32%-37% of total spending. In 2012 & 2013, residential led with annual spending gains of 13% and 19%. In 2014 & 2015, nonresidential buildings, also at 37% of total spending, led the gains at 9% and 19% growth. In 2016 the lead shifts back to residential with a projected growth of 14%. Infrastructure has not led growth since 2007 and 2008 when that sector had growth of 19% and 10%, at a time when residential spending was declining by 19% and 28%.

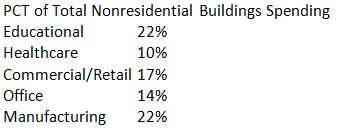

We can get a very good idea of nonresidential buildings spending and growth by looking at the five major markets. These five markets make up 85% of all nonresidential buildings construction spending and half of total 2015 construction spending growth.

See my blog post on October 11, 2015. I wrote:

“New nonresidential buildings construction starts cash flows indicate spending will continue to grow until Feb-Mar 2016, then drop consistently each month until Q3 2016. The decline is almost entirely due to big starts from Q3-Q4 2014 finishing and dropping out of the monthly spending numbers.”

More detail of how each market will perform, and why, follows.

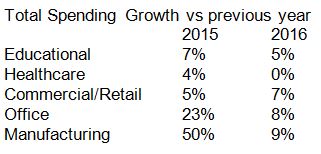

Educational Construction Spending 2016

Spending in 2016 is projected to grow +5% over 2015. Other industry projections for educational spending in 2016 range from 1.5% to 12% growth over 2015, with the average of those seven estimates at 6%. As of August 2015, project starts that will generate 60% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were up 12% from the same 8 months of 2014. Educational spending increased only 4% year-to-date 2015 from the same period 2014, but the current annual rate of growth is 11%. Monthly spending is increasing and should continue to do so at least until mid-2016 before dropping off slightly into year end.

Healthcare Construction Spending 2016

Spending for healthcare is expected to remain flat with no growth in spending in 2016. Other industry projections for healthcare spending in 2016 range from 3% to 12% averaging 6% growth. As of August 2015, project starts already booked will generate 60% of all spending in 2016. New starts in 2016 generate about 25% of the total spending in 2016. If we get some very large new starts in the next few months, that could change total spending projections in 2016. Starts would need to increase 20% ( every month) over my projections for the next 16 months to reach 6% growth in spending next year.

Starts for the first 8 months of 2015 were down 4% from the same 8 months of 2014 and most recently have been declining. 2014 starts grew only 2% over 2013. Healthcare spending had an annual growth rate of 5% in the first eight months of 2015. The decline in new starts signals a projected decline in spending for the next 8 months. Spending growth resumes in mid-2016 but at a very low 3% annual rate and that from an already low rate of spending at the start of the year.

Commercial/Retail Construction Spending 2016

Spending in 2016 is projected to grow +7% over 2015. Other industry projections for office spending in 2016 range from 5.5% to 15% growth over 2015, with the average of those estimates at 10%. As of August 2015, project starts that will generate 55% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were up 17% from the same 8 months of 2014. Commercial spending increased 15% in the first half 2015 from the first half of 2014, but then spending declined by 8% in the last three months and may continue to decline for the next few months. Spending will resume a growth rate of 15% annual in the first 8 months of 2016. Commercial spending will peak in the second quarter 2016 before dropping again into year end.

Office Construction Spending 2016

Spending in 2016 is projected to grow +8% over 2015. Seven other industry projections for office spending in 2016 range from 7% to 18% growth over 2015, with the average of those seven estimates at 12%. As of August 2015, project starts that will generate 55% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were 23% lower than the first 8 months of 2014 Spending from 2014 starts will start to drop off in late 2015 and early 2016 and based on new starts in 2015, by mid-2016 the monthly rate of spending will start to decline, keeping totals for 2016 to less than 10% growth. Spending on office buildings in 2016 will peak in the 1st half year with the 2nd half coming in 10% lower.

Manufacturing Construction Spending 2016

Spending in 2016 is projected to grow +9% over 2015. Seven other industry projections for manufacturing buildings spending in 2016 range from 5% to 18% growth over 2015, with the average of those seven estimates at 11%. As of August 2015, project starts that will generate 70% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were only 6% lower than the first 8 months of 2014. However, even if starts for the next 4 months increase each month by 50% they will still not equal the amount of starts in the last 4 months of 2014. Total starts for 2015 are projected to finish 20% lower than 2014. That’s probably a good thing since 2014 starts were up 87% from 2013, the highest annual growth ever recorded for any market sector.

Spending from 2014 starts will start to drop off in late 2015. Spending reached a peak this year in the 2nd quarter but is expected to drop for the next five to six months. Spending on manufacturing buildings in 2016 will again peak in the 2nd quarter and then drop off into the end of the year.

Nonresidential Buildings Construction Spending Through 2016

New nonresidential buildings construction starts cash flows indicate spending will continue to grow until Feb-Mar 2016, then drop consistently each month until Q3 2016. The decline is almost entirely due to big starts from Q3-Q4 2014 finishing and dropping out of the monthly spending numbers. New starts in 2015 did not grow as much as in the previous two years. Although the predicted decline in monthly spending over 6 months is 8%, 2016 may finish with a rate of monthly spending higher than when it started.

The drop and recovery can vary from the predicted shown here and it’s not likely to be so smooth, but new starts from here on forward would really have to skew from a normal growth pattern by a lot to change this pattern by a little. Nonresidential buildings on average take about 20 to 24 months to complete, so every month we move out adds about 4% to 5% uncertainty to future spending.

This prolonged period of spending declines is sure to cause alarm in the headlines in mid-2016, but the decline and the reversal are supported in large part by starts already booked. Unless something dramatic and unexpected comes along to throw a wrench in the works, I’m expecting a pattern like this for 2016.

Total nonresidential buildings spending in 2016 will finish the year about 10% higher than 2015.