Home » Posts tagged 'inflation' (Page 6)

Tag Archives: inflation

Are We at New Peak Construction Spending?

1-4-17

Total construction spending peaked in Q1 2006 at an annual rate of $1,222 billion. For the most recent three months it has averaged $1,172 billion. It is currently at a 10 1/2 year high at just 4% below peak spending. But that ignores inflation.

In constant inflation adjusted dollars spending is still 18% below the Q1 2006 peak.

Current headlines express exuberance that we are now at a 10 1/2 year high in construction spending but fail to address the fact that is comparing dollars that are not adjusted for inflation.

In the 1st quarter of 2006 total spending peaked at a annual rate of $1.2 billion and for the year 2006 spending totaled $1,167 billion. We are within a stone’s throw of reaching that monthly level and 2016 will reach a new all-time high total spending by a slim fraction. But all of that is measured in current dollars, dollars at the value of worth within that year, ignoring inflation.

Adjusting for inflation gives us a much different value. Inflation adjusted dollars are referred to as constant dollars or dollars all compared or measured in value in terms of the year to which we choose to compare. To be fair, we must now compare all backdated years of construction to constant dollars in 2016. What would those previous years be worth if they were valued in 2016 dollars?

By mid-2017 total construction spending will reach a new all-time high, but in constant inflation adjusted dollars will still be 17% below 2006 peak. We will not reach a new inflation adjusted high before 2020.

Residential construction spending is still 32% below the 2006 peak of $690 billion. In constant inflation adjusted dollars it is 39% below 2006 peak.

Nonresidential Buildings construction spending is only 3.5% below 2008 peak of $443 billion. However, in constant inflation adjusted dollars it is 18% below 2008 peak.

Non-building Infrastructure construction spending pre-recession peaked in 2008 at at an annual rate of $290 billion. However, post recession it peaked in Q1 2014 at $314 billion. It is now 8% below the 2014 peak. In constant inflation adjusted dollars it is 12% below the 2014 peak.

For more on inflation SEE Construction Cost Inflation – Midyear Report 2016

Saturday Morning Thinking Outloud #5 – Jobs Growth

For all of 2014-2015-2016

- Total Construction jobs increased from 5,950,000 to 6,700,000, +12.6%

- Total Construction spending increased from $960bil to $1,170bil, +22%

BUT, much of that spending increase is inflation. We need to compare to constant dollars which = Volume. Inflation was particularly high in residential work, over 15% for the 3 years, which means $1.00bil in spending 3 years ago would be worth more than $1.15bil today. Converting everything to constant Oct 2016 dollars, after inflation we get:

- Total Construction volume increased from $1,070bil to $1,170bil, +9.4%

So, for the 3 years, jobs increased by 12.6% while real work volume increased by 9.4%.

A more thorough analysis, which takes hours worked into consideration, shows from the Jan 2011 bottom of the recession in construction to current, both jobs and volume have increased equally by 28%. But jobs growth is often out-of-balance with real volume growth. In the beginning of the recession years of 2008-2011 firms let go of people much faster than work volume declined. 2009 showed a big gain in productivity. By 2010-2011 firms hadn’t let go enough to match the loss in spending. Then from 2012-2014 workload grew faster than firms filled jobs. Since 2011 we are sort of on an even keel.

For the last 3 years, jobs increased more than real construction volume. I pointed this out in my last detailed jobs report. The 6 months from Oct 2015 – March 2016 encompassed the fastest new construction jobs growth period in a decade. It’s no surprise to me that jobs growth has been slow since March this year. Frankly, I wouldn’t be the least bit surprised if it remains slow for awhile. When we look at jobs growth vs. volume growth, there is reason to believe that slow jobs growth is not entirely due to labor shortages. Part of the blame is due to recent over-hiring.

Saturday Morning Thinking Outloud #3 – Construction Jobs

Why the big slow down in construction jobs this Year? Is work volume on the decline? Are labor shortages to blame?

These days, the most talked about reason for slower jobs growth is the lack of experienced workers available to hire. In fact, recent surveys indicate about 70% of construction firms report difficulty finding experienced workers to fill vacant positions and the Job Openings survey has been at highs for several months. That certainly cannot be overlooked as one reason for slower jobs growth, but that is not the only reason?

Although recent growth has slowed, even with all this talk of difficulty finding experienced construction workers, there has been very good jobs growth. For the 5 ½ year period from the low point in January 2011 to the present (August 2016) we added 1,240,000 construction jobs.

- Jobs increased by 23% in 5 ½ years.

- Spending growth increased 52% in that same 5 1/2 years.

Why is it that jobs don’t increase at the same rate as construction spending? Because much of that spending growth is inflation, not true volume growth. Volume is construction spending minus inflation. To get volume, convert all dollars from current $ in the year spent into constant $ by factoring out inflation.

- Spending growth is not a true measure of increase in real volume.

- Jobs growth should not be compared to spending growth.

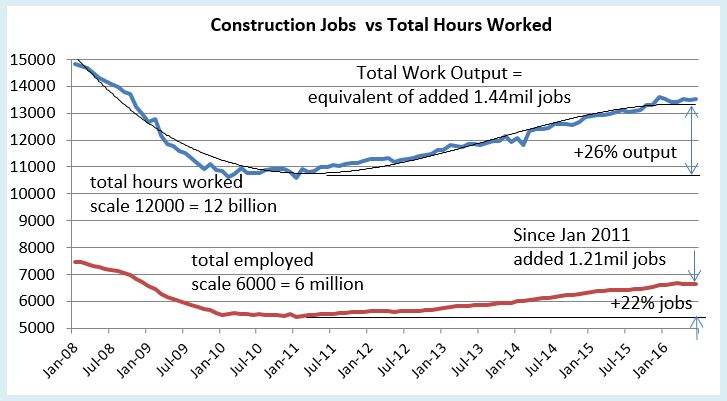

Now that we have spending converted to volume, we need to adjust jobs to get real work output. The total hours worked affects the entire workforce so has a significant impact on output.

- Jobs is not a true measure of work output.

- Jobs x hours worked gives total work output.

Spending must be factored to remove inflation and jobs should be factored to include any change in hours worked.

- In the 5 1/2 years from Jan 2011 to mid 2016, real construction volume and jobs/hours real output both increased by 28%.

Now we see over the long term, job/hours and real volume are moving in tandem. But there are always short term periods when they do not and that causes ups and downs in productivity.

In 2014-2015, jobs/hours grew by 11%, the fastest growth for a two-year span in 10 years. Real volume of work increased by 16% producing a real net increase in productivity. But productivity had declined significantly in 2010 and 2011. It’s not unusual to see productivity balancing out over time. In part, this is due to companies balancing their total employees with their total workload.

From October 2015 through March 2016, jobs growth was exceptional. 214,000 construction jobs were added in 6 months, topping off the fastest 2 years of jobs growth in 10 years. That is the highest 6-month average growth rate in 10 years. That certainly doesn’t make it seem like there is a labor shortage. However, the jobs opening rate (JOLTS) is the highest it’s been in many years and that is a signal of difficulty in filling open positions.

- For the 6-month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of consecutive months jobs growth in 10 years. Then, after 3 months of job losses, July, September and October show modest gains.

I would expect growth such as we’ve had for two years and then that 6 month period to be followed by a slowdown in hiring as firms try to reach a jobs/workload balance. It appears we may have experienced that slowdown. Jobs declined for four of five months from April through August. Keep in mind, this immediately follows the fastest rate of jobs growth in 10 years. But it also tracks directly to three monthly declines in spending. (I predicted this jobs slowdown in my data 9 months ago. I predicted the 1st half 2016 spending decline more than a year ago).

It is not so unusual to see jobs growth slowed for several months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years of jobs growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

If spending plays out as expected into year end 2016, then construction jobs may begin to grow faster in late 2016. However, availability could have a significant impact on this needed growth.

Availability already seems to be having an effect on wages. Construction wages are up 2.6% year/year, but are up 1.2% in the last quarter, so the rate of wage growth has recently accelerated. The most recent JOLTS report shows we’ve been near and now above 200,000 job openings for months. With this latest jobs report, that could indicate labor cost will continue to rise rapidly.

As wages accelerate, also important is work scheduling capacity which is affected by the number of workers on hand to get the job done. Inability to secure sufficient workforce could impact project duration and cost and adds to risk, all inflationary. That could potentially impose a limit on spending growth. It will definitely have an upward effect on construction inflation this year. If work volume accelerates, expect labor cost inflation to rise rapidly.

Construction Inflation >>> LINKS

- 10-24-16 Originally posted

- 2-11-22 added INFRASTRUCTURE index table Q4 2021

This post is preserved for the multitude of LINKS back to sources of cost indices and for the explanation of the difference between Input indices and Output or Final Cost Indices. For all latest indices plots and table see the latest yearly Inflation post.

2-20-25 SEE Construction Inflation 2025

2-1-23 SEE Construction Inflation 2023

2-11-22 SEE Construction Inflation 2022

11-10-21 See 2021 Construction Inflation

See the article Construction Inflation 2020

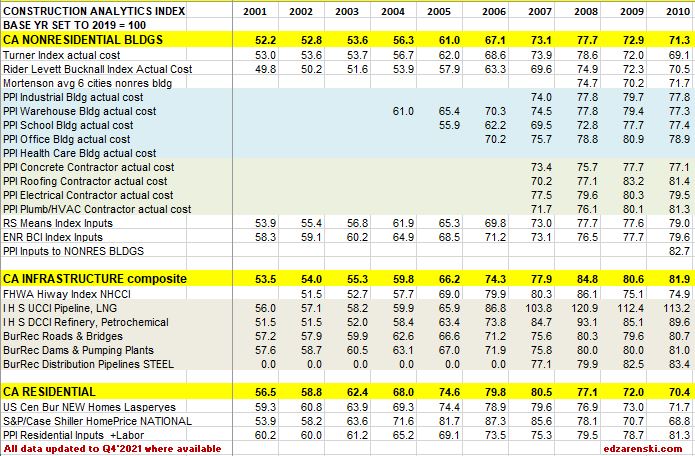

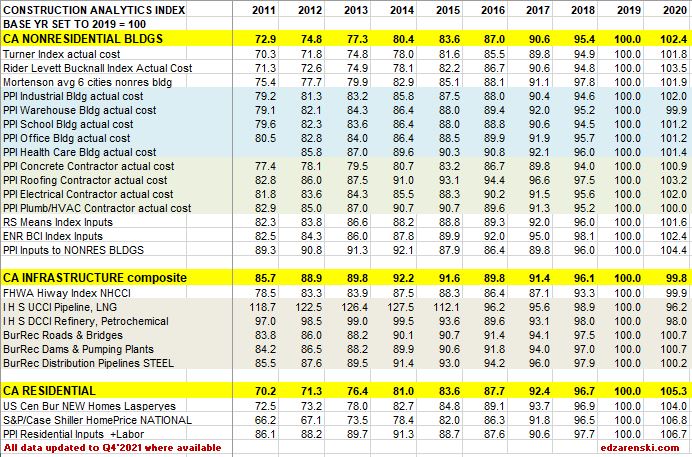

Construction Cost Indices come in many types: Final cost by specific building type; Final cost composite of buildings but still all within one major building sector; Final cost but across several major building sectors (ex., residential and nonresidential buildings); Input prices to subcontractors; Producer prices and Select market basket indices.

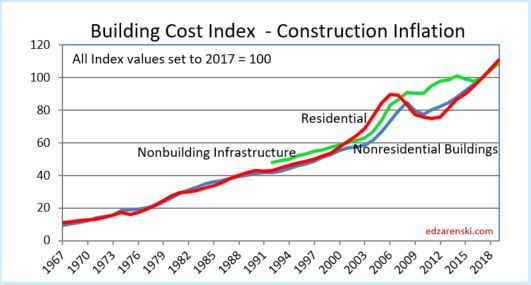

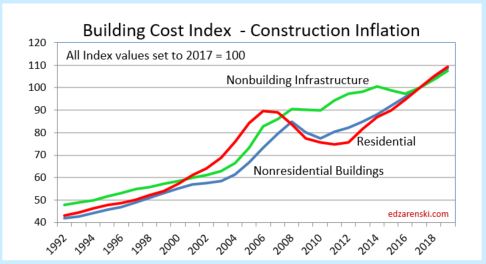

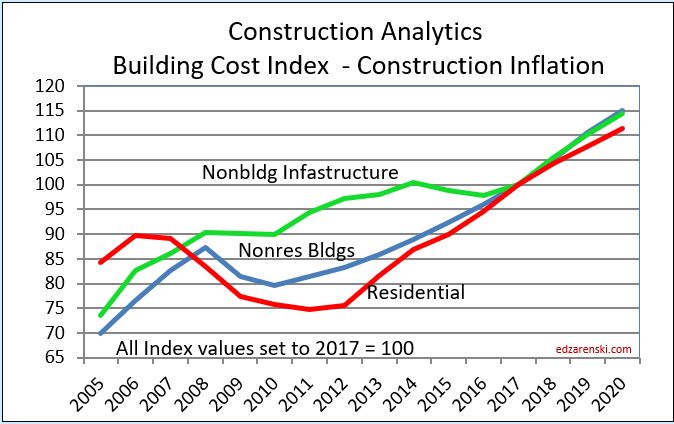

Residential, Nonresidential Buildings and Non-building Infrastructure Indices developed by Construction Analytics, (in highlighted BOLD CAPS in the tables below), are sector specific selling price (final cost) composite indices. These three indices represent whole building final cost and are plotted in Building Cost Index – Construction Inflation, see below, and also plotted in the attached Midyear report link. They represent average or weighted average of what is considered the most representative cost indicators in each major building sector. For Non-building Infrastructure, however, in most instances it is better to use a specific index to the type of work.

The following plots of Construction Analytics Building Cost Index are all the same data. Different time spans are presented for ease of use.

See the article Construction Inflation 2022

All actual index values have been recorded from the source and then converted to current year 2017 = 100. That puts all the indices on the same baseline and measures everything to a recent point in time, Midyear 2017.

All forward forecast values wherever not available are estimated and added by me.

Not all indices cover all years. For instance the PPI nonresidential buildings indices only go back to years 2004-2007, the years in which they were created. In most cases data is updated to include June 2019.

- June 2017 data had significant changes in both PPI data and I H S data.

- December 2017 data had dramatic changes in FHWA HiWay data.

SEE BELOW FOR TABLES

When construction is very actively growing, total construction costs typically increase more rapidly than the net cost of labor and materials. In active markets overhead and profit margins increase in response to increased demand. When construction activity is declining, construction cost increases slow or may even turn to negative, due to reductions in overhead and profit margins, even though labor and material costs may still be increasing.

Selling Price, by definition whole building actual final cost, tracks the final cost of construction, which includes, in addition to costs of labor and materials and sales/use taxes, general contractor and sub-contractor overhead and profit. Selling price indices should be used to adjust project costs over time.

quoted from that article,

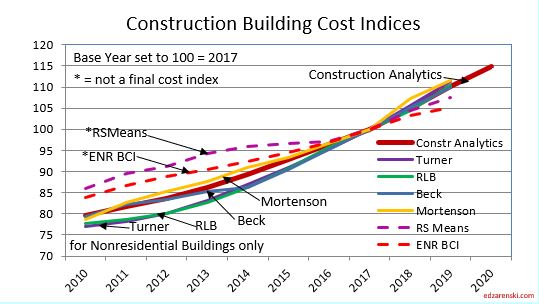

R S Means Index and ENR Building Cost Index (BCI) are examples of input indices. They do not measure the output price of the final cost of buildings. They measure the input prices paid by subcontractors for a fixed market basket of labor and materials used in constructing the building. ENR does not differentiate residential from nonresidential, however the index includes a quantity of steel so leans much more towards nonresidential buildings. RS Means is specifically nonresidential buildings only. These indices do not represent final cost so won’t be as accurate as selling price indices. RSMeans Cost Index Page RS Means subscription service provides historical cost indices for about 200 US and 10 Canadian cities. RSMeans 1960-2018 CANADA Keep in mind, neither of these indices include markup for competitive conditions. FYI, the RS Means Building Construction Cost Manual is an excellent resource to compare cost of construction between any two of hundreds of cities using location indices.

Notice in this plot how index growth is much less for ENR and RSMeans than for all other selling price final cost indices.

8-10-19 note: this 2010-2020 plot has been revised to include 2018-2020 update.

Turner Actual Cost Index nonresidential buildings only, final cost of building

Rider Levett Bucknall Actual Cost Index published in the Quarterly Cost Reports found in RLB Publications for nonresidential buildings only, represents final cost of building, selling price. Report includes cost index for 12 US cities and cost $/SF for various building types in those cities. Boston, Chicago, Denver, Honolulu, Las Vegas, Los Angeles, New York, Phoenix, Portland, San Francisco, Seattle, Washington,DC. Also includes cost index for Calgary and Toronto. RLB also publishes cost information for select cities/countries around the world, accessed through RLB Publications.

Mortenson Cost Index is the estimated cost of a representative nonresidential building priced in seven major cities and average. Chicago, Milwaukee, Seattle, Phoenix, Denver, Portland and Minneapolis/St. Paul.

Beck Biannual Cost Report in 2017 and earlier cost reports developed indices for six major U.S. cities and Mexico, plus average. In the most recent Summer 2021 report, while Beck provides valuable information on cost ranges for 30 different types of projects, the former inflation index is absent. Beck has not published city index values since 2017. Read the report for the trend in building costs. See discussion for Atlanta, Austin, Charlotte, Dallas/Fort Worth, Denver, Tampa and Mexico

Bureau of Labor Statistics Producer Price Index only specific PPI building indices reflect final cost of building. PPI cost of materials is price at producer level. The PPIs that constitute Table 9 measure changes in net selling prices for materials and supplies typically sold to the construction sector. Specific Building PPI Indices are Final Demand or Selling Price indices.

PPI Materials and Supply Inputs to Construction Industries

PPI Nonresidential Building Construction Sector — Contractors

PPI Nonresidential Building Types

PPI Materials Inputs and Final Cost Graphic Plots and Tables in this blog updated 2-10-19

PPI BONS Other Nonresidential Structures includes water and sewer lines and structures; oil and gas pipelines; power and communication lines and structures; highway, street, and bridge construction; and airport runway, dam, dock, tunnel, and flood control construction.

RS MEANS Key material cost updates quarterly

National Highway Construction Cost Index (NHCCI) final cost index, specific to highway and road work only.

The Bureau of Reclamation Construction Cost Trends comprehensive indexes for about 30 different types of infrastructure work including dams, pipelines, transmission lines, tunnels, roads and bridges. 1984 to present.

IHS Power Plant Cost Indices specific infrastructure only, final cost indices

- IHS UCCI tracks construction of onshore, offshore, pipeline and LNG projects

- IHS DCCI tracks construction of refining and petrochemical construction projects

- IHS PCCI tracks construction of coal, gas, wind and nuclear power generation plants

S&P/Case-Shiller National Home Price Index history final cost as-sold index but includes sale of both new and existing homes, so is an indicator of price movement but should not be used solely to adjust cost of new residential construction

US Census Constant Quality (Laspeyres) Price Index SF Houses Under Construction final cost index, this index adjusts to hold the build component quality and size of a new home constant from year to year to give a more accurate comparison of real residential construction cost inflation

TBDconsultants San Francisco Bay Area total bid index (final cost).

Other Indices not included here:

CoreLogic Home Price Index HPI for single-family detached or attached homes monthly 1976-2019. This is a new home and existing home sales price index.

Consumer Price Index (CPI) issued by U.S. Gov. Bureau of Labor Statistics. Monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. This index in not related at all to construction and should not be used to adjust construction pricing.

Jones Lang LaSalle Construction Outlook Report National Construction Cost Index is the Engineering News Record Building Cost Index (ENRBCI), a previously discussed inputs index. The report provides some useful commentary.

Sierra West Construction Cost Index is identified as a selling price index with input from 16-20 U.S. cities, however it states, “The Sierra West CCCI plays a major role in planning future construction projects throughout California.” This index may be a composite of several sectors. The link provided points to the description of the index, but not the index itself. No online source of the index could be found, but it is published in Engineering News Record magazine in the quarterly cost report update.

Leland Saylor Cost Index Clear definition of this index could not be found, however detailed input appears to represent buildings and does reference subcontractor pricing. But it could not be determined if this is a selling price index. A review of website info indicates almost all the work is performed in California, so this index may be regional to that area. Updated Index Page

DGS California Construction Cost Index CCCI The California Department of General Services CCCI is developed directly from ENR BCI. The index is the average of the ENR BCI for Los Angeles and San Francisco, so serves neither region accurately. Based on a narrow market basket of goods and limited labor used in construction of nonresidential buildings, and based in part on national average pricing, it is an incomplete inputs index, not a final cost index.

Vermeulens Construction Cost Index can be found here. It is described as a bid price index, which is a selling price index, for Institutional/Commercial/Industrial projects. That would be a nonresidential buildings sector index. No data table is available, but a plot of the VCCI is available on the website. Some interpolation would be required to capture precise annual values from the plot. The site provides good information.

CALTRANS Highway Cost Index Trade bids for various components of work and materials, published by California Dept of Transportation including earthwork, paving and structural concrete. Includes Highway Index back to 1972, quarterly from 2012.

Colorado DOT Construction Cost Index 2002-2019 Trade bids for various components of work published by Colorado Dept of Transportation including earthwork, paving and structural concrete.

Washington State DOT Construction Cost Index CCI for individual components or materials of highway/bridge projects 1990-2016

Minnesota DOT Highway Construction Cost Index for individual components of highway/bridge projects 1987-2016

Iowa DOT Highway Cost Index for individual components of highway/bridge projects 1986-2019

New Hampshire DOT Highway Cost Index 2009-2019 materials price graphs and comparison to Federal Highway Index.

New York Building Congress New York City Construction Costs compared to other US and International cities

U S Army Civil Works Construction Cost Index CWCCIS individual indices for 20 public works type projects from 1980 to 2050. Also includes State indices from 2004-2019

Eurostat Statistics – Construction Cost Indices 2005-2017 for European Countries

Comparative International Cities Costs – This is a comparative cost index comparing the cost to build in 40 world-wide cities If this International Cities Costs is a parity index, which involves correcting for difference in currency, then you must know the parity city in each country, which in the US I think is Chicago.

OECD International Purchasing Power Parity Index

Turner And Townsend International Construction Markets 2016-2017

Turner And Townsend International Construction Markets 2018

Rider Levitt Bucknall Caribbean Report 2018

US Historical Construction Cost Indices 1800s to 1957

Click Here for Link to Construction Cost Inflation – Commentary

2-12-18 – Index update includes revisions to historic Infrastructure data

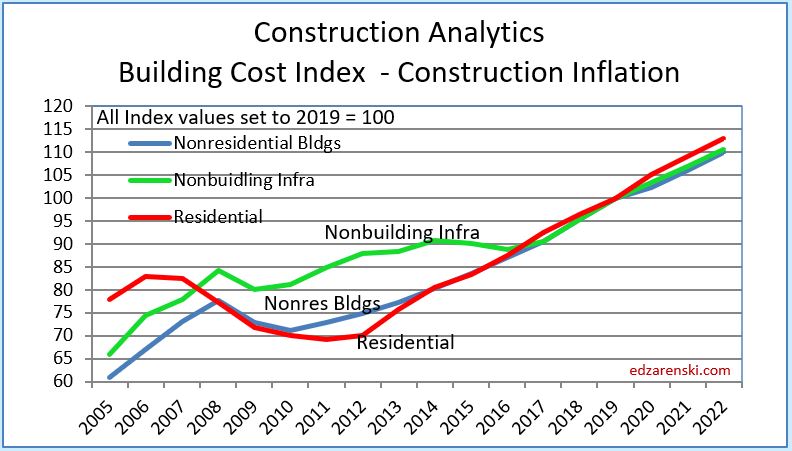

1-26-21 The tables below, from 2011 to 2020 and from 2015 thru 2023, updates 2020 data and provides 2021-2023 forecast.

NOTE, these tables are based on 2019=100. Nonresidential inflation, after hitting 5% in both 2018 and 2019, and after holding above 4% for the six years 2014-2019, is forecast to increase only 2.5% in 2020, but then 3.8% in 2021 and hold near that level the next few years. Forecast residential inflation for the next three years is level at 3.8%. It was only 3.6% for 2019 but averaged 5.5%/yr since 2013 and returned to 5.1% in 2020.

11-10-21 Follow the link at the bottom to 2021 Inflation

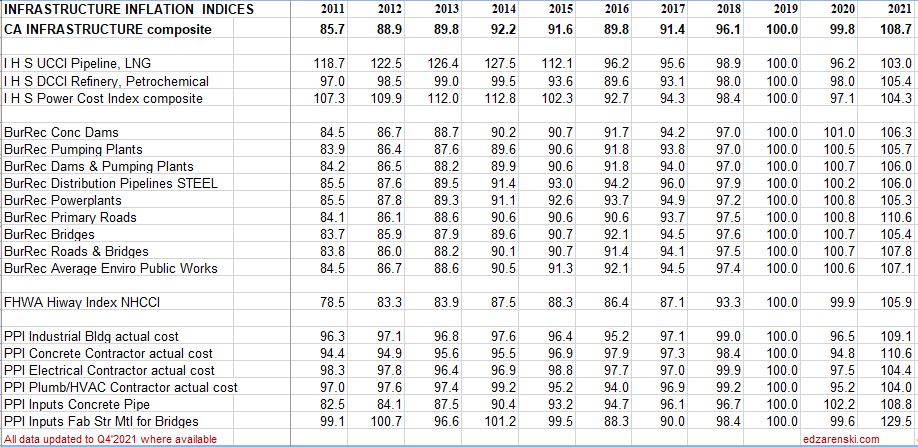

The Tables below 2001 to 2010 and 2011-2020 are updated to Q4 2021 with any revisions to past years posted on source websites.

The Table below 2015 to 2023 is updated to Q4 2021

How to use an index: Indexes are used to adjust costs over time for the affects of inflation. To move cost from some point in time to some other point in time, divide Index for year you want to move to by Index for year you want to move cost from. Example : What is cost inflation for a building with a midpoint in 2022, for a similar nonresidential building whose midpoint of construction was 2016? Divide Index for 2022 by index for 2016 = 110.4/87.0 = 1.27. Cost of building with midpoint in 2016 x 1.27 = cost of same building with midpoint in 2022. Costs should be moved from/to midpoint of construction. Indices posted here are at middle of year and can be interpolated between to get any other point in time.

All forward forecast values, whenever not available, are estimated by Construction Analytics.

2-13-23 Construction Inflation 2023

Steel Statistics and Steel Cost Increase Affect on Construction?

9-18-16 update Mar 2018

Recent articles suggest that steel cost is expected to increase and this will almost certainly affect the cost of construction. But just how much of an affect would a cost increase have on total building cost? The cost increase that is being talked about is the mill price cost of steel, or something like pipe and tube producer price (PPI), since pipe and tube is a world trade item, but not a Fab Steel PPI. None of these include total cost of steel installed. The PPI is the price after fabrication. Total cost is the contractor’s bid or selling price installed which includes all markups (or markdowns).

PPI Steel Materials Inputs plot updated 2-10-19 to include 2018 data

The questions we need to answer are:

- How much of a cost increase will we see in the raw product, manufactured raw steel?

- How much steel is used in a building?

- What affect will a raw material cost increase have on the cost of steel installed?

- How much does that change the cost of the building?

It might help to start with a basic understanding of steel manufacturing and use.

Basic Oxygen Steel (BOS) steel making uses between 25 and 35% recycled steel to make new steel. BOS steel usually has less residual elements in it, such as copper, nickel and molybdenum and is therefore more malleable than EAF steel so it is often used to make automotive bodies, food cans, industrial drums or any product with a large degree of cold working. Cold rolled steel is in this category which would include gypsum wall system steel studs and HSS Hollow Structural Sections.

Electric Arc Furnace (EAF) steel making contains more residual elements that cannot be removed through the application of oxygen and lime. It is used to make structural beams, plates, reinforcing bar and other products that require little cold working. EAF steel uses almost 100% recycled steel. Most steel that goes into a building or civil structure is in this category. 2/3rds of all steel manufactured in the US is EAF steel.

Typically quoted benchmark steel pricing that I’ve seen is based on either cold-rolled-coil sheet steel or hot-rolled-coil sheet steel. This is a common product used for the automotive industry or appliance, but not so much for the construction industry (steel studs vs structural steel). EAF Structural steel is nearly 100% dependent on recycled steel so is not as much affected by price changes of iron ore, as is BOS steel.

The United States is the world’s largest steel importer. Of the 30MMT imported, 50%+ of that comes from our top few import suppliers, Canada, Brazil, South Korea and Mexico. Russia supplies 7%-9%. No other country supplies more than 5% of our imports. China supplies less than 2% of our steel imports, The U.S. is responsible for almost 10% of global steel imports, more than double the second largest importer. The U.S. annually imports about $20-$25 billion of steel, $2 billion from Mexico.

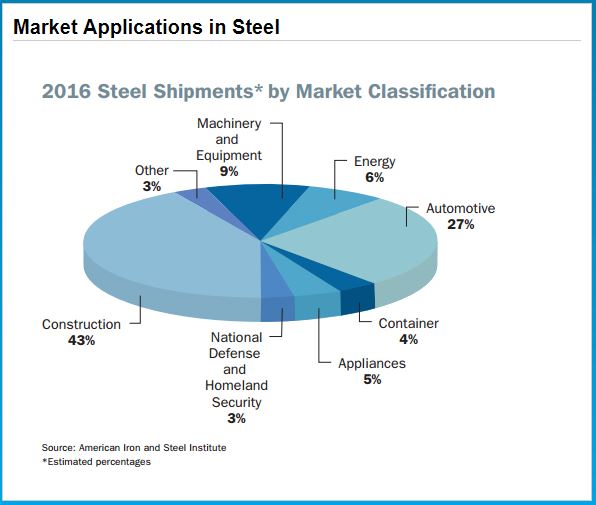

The United States consumes approximately 110 million tons of steel each year. More than 40 million tons is used in the construction industry. The next largest industries, automotive and equipment and machinery, together do not use as much steel as construction. The U.S. imports about 30% of the steel it uses.

The graphic chart above is by American Iron and Steel Institute.

Structural steel is the most widely used structural framing material for buildings used in the U.S. with nearly 50% market share in nonresidential and multistory residential buildings. Prior to the recession steel had a 60% market share.

Sources are also linked below.

What affect might a steel cost increase have on a building project? It will affect the cost of structural shapes, steel joists, reinforcing steel, metal deck, stairs and rails, metal panels, metal ceilings, wall studs, door frames, canopies, steel duct, steel pipe and conduit. Structural steel and reinforcing steel are hot-rolled long products, EAF steel. All the others are cold-rolled flat sheet BOS steel.

Here are some averages of the percentage of steel material costs as related to total project construction cost. For a building that is predominantly masonry, these percentages would be reduced considerably. For a heavy industrial building the percentages might be higher.

Assuming a typical structural steel building with some metal panel exterior, steel pan stairs, metal deck floors, steel doors and frames and steel studs in walls, then all steel material installed represents about 14% to 16% of total building cost.

Structural Steel only, installed, is about 9% to 10% of total building cost, but applies to only 60% market share of steel buildings. The other 6% of total building cost applies to all buildings.

Other steel is very likely higher to take into account any increased cost in major mechanical equipment such as chillers, pumps, fan powered boxes, cooling towers, tanks, generators, plumbing fixture supports, electrical panel boxes and cable trays.

If the structural steel subcontractor increases bid price by 10%, that raises the cost of the building by 1%, but if it is the mill price of steel that increases by 10% the increase to final building price is far less. It is the mill price of steel, rather than fabricated steel, that you would track in the producer price index (PPI).

The final cost of steel installed in a building is about four times the cost of the raw mill steel material used in making and installing the final product. Why so different? Well, for instance, structural steel cost includes: raw mill steel cost, delivery to shop, drafting, shop fabrication, shop paint, delivery to job site and shop markup. At the job site it includes: unload and sort, field installation crew, welding machine, crane and operator, contractor’s overhead and profit and sales tax.

Assuming a building as described above, a 10% increase in the cost of mill steel, which (material only) affects one fourth the cost of 16% of the total building cost, then a 10% increase in the cost of ALL mill steel may result in a composite price increase on a whole building of about 10% x ¼ x 16% = 0.4%. A 10% increase in the cost of mill steel just for structure may result in a composite price increase on a whole building of about 10% x ¼ x 10% = 0.25%.

So, if the mill cost of steel were to increase 10% from $700/ton to $770/ton prior to shop fabrication, for a $100 million building, that could add roughly 0.25% ($250,000) to the cost of the structural steel contract or roughly 0.4% ($400,000) to the total cost of all steel.

A 25% increase in mill steel could add 0.65% to final cost of building just for structure. It adds 1.0% for all steel in a building.

For a project such as a steel bridge, where not just 16% of cost is steel material, but potentially 40% to 60% of cost is steel, a 25% increase in mill steel might add as much as 3% to 4% to final cost.

links to relevant data

Steel Imports Report Global Steel Trade Monitor

Steel Capacity Utilization and Use American Iron and Steel Institute

Structural Steel Industry Overview AISC

World Steel Production – Consumption – Imports – Exports

Crain’s NY – Impact of steel tariffs already being felt in NYC

Construction Cost Inflation – Commentary 2019

1-28-20 See the new post Construction Inflation 2020

8-10-19 updated plots and commentary

General construction cost indices and Input price indices that don’t track whole building final cost do not capture the full cost of escalation in construction projects. To properly adjust the cost of construction over time you must use actual final cost or selling price indices.

Click Here for Link to a 20year Table of 25 Indices

Inflation in construction acts differently than consumer inflation. When there is more work available, inflation increases. When work is scarce, inflation declines. A very large part of the inflation is margins, wholesale, retail and contractor. When nonresidential construction was booming from 2004 through 2008, nonresidential final price inflation averaged almost 8%/year. This was at a time when input costs were averaging between 5% and 6%/year. When residential construction boomed from 2003 to 2005, inflation in that sector was 10%/year. But from 2009 through 2012 we experienced deflation, the worst year being 2009. Residential construction experienced a total of 17% deflation from 2007 through 2011. From 2008 to 2010, nonresidential buildings experienced 10% deflation in two years.

The following plots are all the same data. Different time spans are presented for ease of use.

8-10-19 note: this 2005-2020 plot has been revised to include 2018-2020 update.

Nonresidential Buildings – Since 1993, the 25-year long-term annual construction inflation has averaged 3.5%, even when including the recessionary period 2007-2011. Long-term average inflation, without recessionary declines, is 4% for 20 non-recessionary years since 1993. During rapid growth period of 5 years from 2004-2008, inflation averaged 8% per year. Since 2011, nonresidential buildings inflation has averaged 3.8%, averaging 4.25%/yr. for the last 4 years with a high of 5.1% in 2018.

Residential, from 2007- 2011 experienced 5 consecutive years of deflation, down 20%. In the 4-year boom just prior to that, 2003-2006, inflation averaged 9% per year. Residential inflation snapped back to 8.0% in 2013. It slowed to 4.4% in 2018 but has averaged over 5% for the last three years.

Construction Spending growth posted two separate 4-year periods of 40%+ growth, up 41% in 2012-2015 and up 40% in 2013-2016, exceeding the growth during the closest similar four-year periods 2003-2006 (+37%) and 1996-1999 (+36%), which were the two fastest growth periods on record with the highest rates of inflation and productivity loss. Growth peaked at +11%/year in 2014 and 2015, exceeded only slightly by 2004-2005.

Spending growth slowed to 7.0% in 2016 and only 4.5% in 2017. In 2018, spending dropped to a gain of only 3.3%. It’s expected, after revisions that 2019 spending will finish at a gain of less than 2%.

Producer Price Index (PPI) Material Inputs (excluding labor) costs to new construction increased +4% in 2018 after a downward trend from +5% in 2011 led to decreased cost of -3% in 2015, the only negative cost for inputs in the past 20 years. Input costs to nonresidential structures in 2017+2018 average +4.2%, the highest in seven years. Infrastructure cost are up near 5% and single-family residential inputs are up 4%. But material inputs accounts for only a portion of the final cost of constructed buildings.

Labor input is currently experiencing cost increases. When there is a shortage of labor, contractors may pay a premium to keep their workers. All of that premium may not be picked up in wage reports. Also, some of the labor inflation is due to lost productivity due to less skilled workforce. Unemployment in construction is the lowest on record. There is some sign of jobs growth slowing down in Q2 and Q3 2019, and potentially getting slower.

Nationally tracked indices for residential, nonresidential buildings and non-building infrastructure vary to a large degree. When the need arises, it becomes necessary that contractors reference appropriate sector indices to adjust for whole building costs.

Click Here for Link to a Table of 25 Index Values

ENRBCI and RSMeans input indices are prefect examples of commonly used indices that DO NOT represent whole building costs, yet are widely used to adjust project costs. An estimator can get into trouble adjusting project costs if not using appropriate indices. The two input indices for nonresidential buildings did not decline during the 2008-2010 recession. All other final cost indices dropped 6% to 10%.

From 2010 to 2019, total final price inflation is 110/80 = 1.38 = +38%. Input cost indices total only 106/85 = 1.25 = +25%, missing a big portion of the cost growth over time.

CPI, the Consumer Price Index, tracks changes in the prices paid by urban consumers for a representative basket of goods and services, including food, transportation, medical care, apparel, recreation, housing. This index in not related at all to construction and should never be used to adjust construction pricing. Historically, Construction Inflation is about double the CPI. However for the last 5 years it averages 3x the CPI.

Taking into account the current (Jan 2018 12 mo) CPI of 2% and the most recent 5 years ratio, along with accelerated cost increases in labor and material inputs and the high level of activity in markets, I would consider the following forecasts for 2018 inflation as minimums with potential to see higher rates than forecast.

Residential construction, from 2007- 2011, experienced five consecutive years of deflation, down 20%. In the 4-year boom just prior to that, 2003-2006, inflation averaged +9% per year. Residential construction inflation saw a slowdown to only +3.5% in 2015. However, the average inflation for five years from 2013 to 2017 is 6%. It peaked at 8% in 2013. It climbed back over 5% for 2016 and reached 5.8% in 2017. For 2018, residential final cost inflation indexes are up only 4.5%. Residential construction inflation for 2019 is now about 4% to 4.5%.

A word about Hi-Rise Residential. About 95% of the cost of a hi-rise residential building would remain the same whether the building was for residential or nonresidential use. This type of construction is totally dis-similar to low-rise residential, which in large part is stick-built single family homes. Therefore, a more appropriate index to use for hi-rise residential construction is the nonresidential buildings cost index.

Nonresidential Buildings inflation, during the rapid growth period of five years from 2004-2008, averaged 8% per year. Inflation averaged near 4% per year for the 4 years 2014-2017.

Several Nonresidential Buildings Final Cost Indices averaged over 5% per year for the last 2 years and over 4% per year for the last 5 years. Nonresidential buildings inflation totaled 22% in the last five years. Input indices that do not track whole building cost would indicate inflation for those four years at only 12%, much less than real final cost growth. For a $100 million project escalated over those four years, that’s a difference of $8 million, potentially underestimating cost.

Nonresidential buildings spending slowed from 2017 to 2019 but is now entering a phase in which it may reach the fastest rate of growth in three years, which historically leads to accelerated inflation. Construction inflation for nonresidential buildings for 2018 and 2019 was 5%/yr. For 2020 expect 4.25%, rather than the long term average of 3.5% to 4.0%.

Non-building infrastructure indices are so unique to the type of work that individual specific infrastructure indices must be used to adjust cost of work. The FHWA highway index increased 17% from 2010 to 2014, stayed flat from 2015-2017, then increased 6%+ in 2018. The Highway index for 2019 is up about 6%. The IHS Pipeline and LNG indices increased in 2018 but are still down 20% since 2014. Coal, gas, and wind power generation indices have gone up only 6% in seven years. Refineries and petrochemical facilities have dropped 5% in 4 years but 2018 regained the level of 2013. Input costs to infrastructure are down slightly from the post recession highs, but most have increased in the last year. Input cost to Highways are up 5.0% and to the Power sector are up 3.6% in 2018. Work in Transportation and Pipeline projects has increased dramatically in 2017 and 2018.

Infrastructure power indices registered 2.5% to 3.5% gains in 2017 and again in 2018. Highway indices increased 6.6% in 2018. Anticipate 4% inflation for Power sector and at least 5%-6% inflation for Highway in 2019 with the potential to go higher in rapidly expanding markets, such as pipeline or highway.

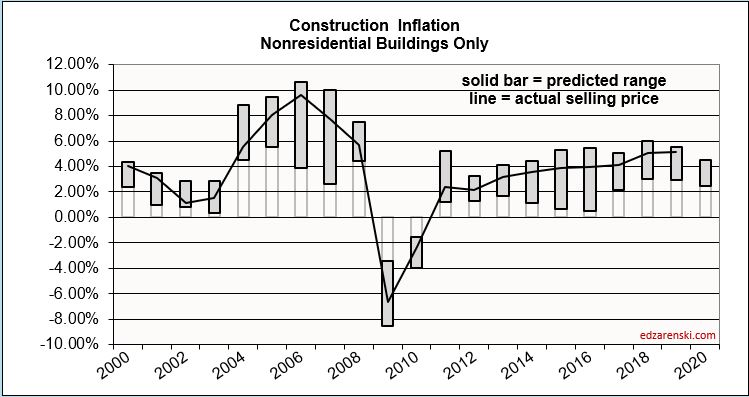

This plot for nonresidential buildings only shows bars representing the predicted range of inflation from various sources with the line showing the composite final cost inflation. Note that although 2015 and 2016 have a low end of predicted inflation of less than 1%, the actual inflation is following a pattern of growth above 4%. The low end of the predicted range is almost always established by input costs, while the upper end of the range and the actual cost are established by selling price indices.

8-10-19 note: this 2005-2020 plot has been revised to include 2018-2020 update.

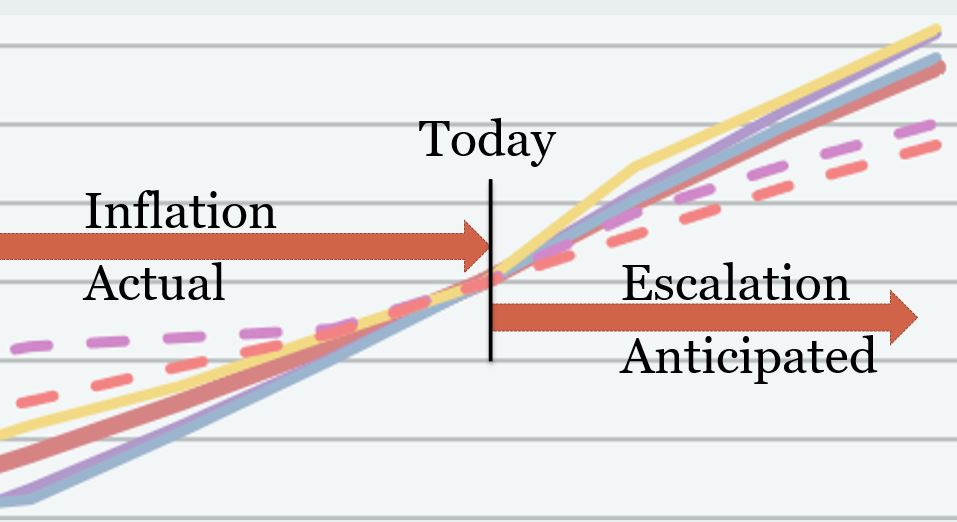

A word about terminology: Inflation vs Escalation. These two words, Inflation and Escalation, both refer to the change in cost over time. However escalation is the term most often used in a construction cost estimate to represent anticipated future change, while more often the record of past cost changes is referred to as inflation. Keep it simple in discussions. No need to argue over the terminology, although this graphic might represent how most owners and estimators reference these two terms.

In every estimate it is always important to carry the proper value for cost inflation. Whether adjusting the cost of a recently built project to predict what it might cost to build a similar project in the near future or adding an escalation factor to the summary of an estimate for a project with a midpoint 2 years out, or answering a client question, “What will it cost if I delay my project start by one year?”, whether you carry the proper value for escalation can make or break your estimate.

- Long term construction cost inflation is normally about double consumer price inflation (CPI).

- Since 1993 but taking out 2 worst years of recession (-8% to -10% total for 2009-2010), the 20-year average inflation is 4.2%.

- Average long term (30 years) construction cost inflation is 3.5% even with any/all recession years included.

- In times of rapid construction spending growth, construction inflation averages about 8%.

- Nonresidential buildings inflation has average 3.7% since the recession bottom in 2011. It averaged 4.6% for the 4 years 2016-2019.

- Residential buildings inflation reached a post recession high of 8.0% in 2013 but dropped to 3.5% in 2015. It averaged 4.6% for the 4 years 2016-2019, but is at the low point of 3.3% in 2019.

- Although inflation is affected by labor and material costs, a large part of the change in inflation is due to change in contractors/suppliers margins.

- When construction volume increases rapidly, margins increase rapidly.

- Construction inflation can be very different from one major sector to the other and can vary from one market to another. It can even vary considerably from one material to another.

Click Here for Link to a Table of 25 Index Values

June Jobs Report Construction

June Jobs Report (May 15-Jun 18) released July 8

There have been no job gains in construction for the last 3 months. In fact we’ve lost 22,000 jobs since March and have only 46,000 new jobs year-to-date. I have to admit after the Apr and May losses, I expected a sizable jobs gain in June. However, for quite a while I’ve predicted spending would decline in Q1 and since a peak in Mar it’s been going down for 2 months. Lower spending would correlate to lower jobs.

Construction jobs are up 3.9% over the same period 2015, so a temporary slowdown should not have much effect. We have just gone through the best 3 years of construction jobs growth since 2004-2006. Perhaps we may experience a leveling out between spending and jobs. At any rate, I see construction spending increasing. There’s still a lot of spending growth in current backlog from starts, so I expect further increases in jobs.

The available unemployed pool dropped to the lowest in 16 years. That could also have some correlation with slow or no jobs growth, as it may mean the people to hire are not available.

Availability already seems to be having an effect on wages. Construction wages are up 2.6% year/year, but are up 1.2% in the last quarter, so the rate of wage growth has recently accelerated. The most recent JOLTS report shows we’ve been near 200,000 job openings for months. That with this latest jobs report could indicate labor cost will continue to rise rapidly.

As wages accelerate, also important is work scheduling capacity which is affected by the number of workers on hand to get the job done. Inability to secure sufficient workforce could impact project duration and cost and adds to risk, all inflationary. That could potentially impose a limit on spending growth. It will definitely have an upward effect on construction inflation this year.

Construction worker output Q2 2016 (# workers x hours worked) is up 3.7% over the same quarter last year, but up only 0.6% from Q1 2016.

Spending minus inflation (volume) has been growing faster than workforce output for the last few years. Since Jan 2011, volume has increased 20% and workforce output increased 26%, a net productivity loss, but since Jan 2014 volume increased by 16% and workforce output increased by only 12.5%. Total hours worked compared to total spending shows productivity has been increasing for the last two years. It would be unusual to see productivity growth continue for another year. This leads me to think if spending plays out as expected then construction jobs will grow by about 200,000 in 2016. Availability could have a significant impact on this needed growth.

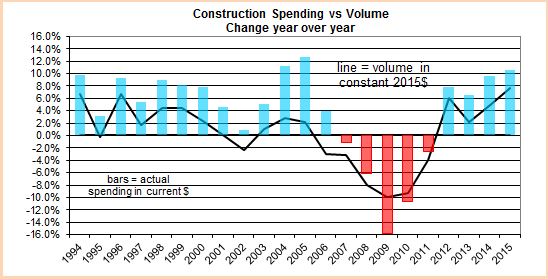

Construction Volume Vs Construction Spending

Construction volume is not the same as construction spending.

Spending is the number nearly everyone follows. Volume is spending minus inflation.

Two years that show the greatest differences between spending and volume highlight the affect of inflation. In 2004 and 2005 total construction spending grew by 11% and 12.5%, but after inflation, volume grew by only 3% and 2%. In the most recent year, construction spending in 2015 grew by 10.5% but total construction volume grew by only 7.5%.

For the four years 2012 through 2015 construction spending grew by 35% but after inflation volume grew by 21%. Inflation accounts for 14% of spending growth.

Annual construction inflation varies for residential, nonresidential buildings and nonresidential infrastructure, and it varies sometimes so widely that each should be used only to adjust that specific group. Since 1993, long-term annual construction inflation for buildings has been 3.5% per year, even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8% per year.

Historical average volume growth over the last 22 years is grossly distorted by the recession. Volume declined in 8 of those 22 years. In the worst three years of the recession, 2008, 2009 and 2010, volume declined by 28%. If we take out those three years the typical growth period averages are more apparent. The historical average volume growth in construction with recession data removed and after adjusting for inflation is 2% per year for 19 years.

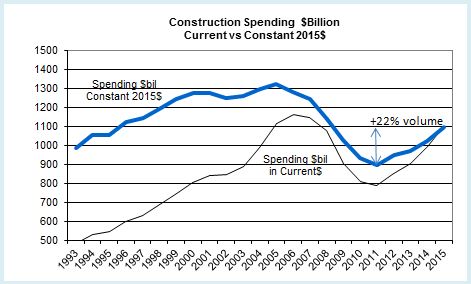

Adjusting for inflation is changing current dollars to constant dollars.

Current dollars = dollars are reported in the value of the year reported, 2008 = 2008$, 2015 = 2015$. News reports almost always refer to current dollars and therefore do not account for the influence of inflation.

Constant dollars = all dollars adjusted to represent dollars in the year of comparison. This adjusts for inflation so 2008$ (and all other years) are converted to equivalent 2015$.

It’s not too hard to understand why we need to look at constant dollars when you think of it in terms of building a house. For example, a 2,500 sf house built in 2001 may have cost $250,000 then to build. Today to build that exact same house may cost $400,000. The house is no different, so volume remains the same. The only thing that changed is inflation. With respect to constant dollars for the same volume, $250,000 in 2001 dollars would be equal to $400,000 in 2015 dollars.

The common comparison is to look at growth in construction spending from year to year. What that does not tell us is how much of the spending growth is inflation and how much is a real increase in construction volume.

Constant dollars makes a huge difference in the analysis. Adjusting all previous years of spending allows us to compare changes in volume growth from year to year. This plot of total construction dollars shows current dollars would indicate we are now only 7% below the previous high and we’ve had growth of 37% from the recession low. Constant dollars, adjusting for inflation, shows volume is still 17% below the previous cycle high and we’ve had growth of only 22% since the recession lows.

Construction Inflation Cost Index

Note: The post you’ve reached here was originally written in Jan 2016. For the latest information follow this link to the newest data on Inflation. 8-15-19

ESCALATION / INFLATION INDICES

Thank You. edz

Jan. 31, 2016

Construction inflation for buildings in 2016-2017 is quite likely to advance stronger and more rapidly than some estimators and owners have planned.

Long term construction cost inflation is normally about double consumer price inflation. Construction inflation in rapid growth years is much higher than average long-term inflation. Since 1993, long-term annual construction inflation for buildings has been 3.5%/yr., even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8%/yr.

For the period 2013-2014-2015, nonresidential buildings cost indices averaged just over 4%/yr. and residential buildings cost indices average just over 6%/yr. I recommend those rates as a minimum for 2016-2017. Some locations may reach 6% to 8% inflation for nonresidential buildings but new work in other areas will remain soft holding down the overall average inflation. Budgeting should use a rate that considers how active work is in your area.

Infrastructure projects cost indices on average have declined 4% in the last three years. However, infrastructure indices are so unique that individual specific indices should be used to adjust cost of work. The FWHA highway index dropped 4% in 2013-2014 but increased 4% in 2015. The IHS power plant cost index gained 12% from 2011-2014 but then plummeted in 2015 to an eight year low. The PPI industrial structures index and the PPI other nonresidential structures index both have been relatively flat or declining for the last three years.

These infrastructure sector indices provide a good example for why a composite all-construction cost index should not be used to adjust costs of buildings. Both residential and infrastructure project indices often do not follow the same pattern as cost of nonresidential buildings.

Anticipate construction inflation of buildings during the next two years closer to the high end rapid growth rate rather than the long term average.

What Did He Say? Fact Checker – Track Record

MY TRACK RECORD

Indoor Masters National Track Championships

masters age group 45-50

Mile – 4:41.7 – 4th place

3000m – 9:25.3 – 3rd place

Oh, wait. That’s not what you are here to read. You want my track record on construction economic forecasts. How good are my forecasts? Do they prove to be accurate? How do they compare to the rest of the industry forecasts? OK. Let’s have a look.

- Bullets show what I forecast.

This is what actually occurred. Actual is in red if I got it wrong.

From Jan 2013

- The ABI, McGraw Hill Dodge new starts and the Dodge Momentum Index (DMI) are all indicating a dip in nonresidential spending potentially from February through May 2013.

- Architecture Billings Index (ABI) went UP from May 2012 to January 2013 with only December down slightly (see figure B). This is a very good leading indicator for new construction work starting in Q3-Q4 2013.

- I expect a dip in nonresidential buildings work between January and May 2013, at which point all indicators point to sustained growth through year end.

From February 2013 through June 2013 actual spending on nonresidential buildings dropped by 2%. Then from June through November spending increased by 6%.

From Jan 2013

- As spending continues to increase, contractors gain more ability to pass along costs and increase margins. However, contractors almost always are playing catch-up. In the most recent three-month period, contractors’ costs began to climb faster than whole building costs went up, due to both increasing material costs and declining productivity.

- Once growth in nonresidential picks up and both residential and nonresidential are active, we will begin to see apparent labor shortages and productivity losses.

For 2013 and 2014 construction spending increased 7% and 10%. During that 2 year period, total labor and materials inputs increased only 2% to 3%, but construction inflation measured 4.5%. Margins increases drove up the total inflation cost. Available (nonworking) workforce declined to about 400,000, near the lowest on record. Productivity declined by 2%.

From Jan 2013

- Construction Spending for 2013 will be pushed higher by huge growth in residential construction, a rate of spending growth that increased by 30% from Q1 to Q4 2012

Residential spending in 2013 grew at a rate of 1.5% per month, largest one year growth since 2004.

From Jan 2013

- The National Association of Home Builders consensus estimate for new residential units is growth of 23% in 2013 and 33% in 2014. 2012 grew by 28%.

- The NAHB projections are for an increase of 150,000 units in 2013 and 230,000 in 2014, 20% and 27% growth the next two years. There’s a possibility we could achieve that. But, especially in 2014, that would exceed the fastest growth rates, both volume and total jobs, achieved in the last 30 years.

- Mark Zandi, economist for Moody’s, in the same article is quoted as saying his more optimistic forecast has residential construction growing to 1.1mil in 2013 and 1.7mil new housing starts in 2014, growth of 46% and then 54%. I say NO WAY

- A more reasonable projection is new housing starts may reach 850K to 900K in 2013 and 1.0 to 1.05 million in 2014, new homes growth rates of 15% to 20% and total residential spending growth of 12% to 15%. That still has the workforce expanding rapidly, but at least at a not unheard of rate.

Housing starts reached 925,000 in 2013 and 1,003,000 in 2014, well below the 30 year historical annual growth.

From Jan 2013

- Future escalation, in order to capture increasing margins, will be higher than normal labor/material cost growth. Lagging regions will take longer to experience high escalation.

- I’m advising a range of 4% to 6% for 2013, 5% to 7% for 2014 and 6% to 8% for 2015.

- Expect residential escalation near the upper end of the range.

Actual total construction cost inflation 2013 = 4.3%, 2014 = 4.7% 2015 = 2.9%. All inflation values were held to lower totals due to infrastructure work which did not have more than 2% inflation during that period and actually experienced deflation in 2015. Residential buildings inflation for 2013-14-15 was 8.9%, 7.1% and 4.1%.

Posted April 2014

- Construction Spending “residential buildings” expect $379 billion in 2014

- Construction Spending “nonresidential buildings” expect $325 billion in 2014

- Construction Spending “totals” expect $960 billion in 2014

Posted August 2014

- Construction Spending “residential buildings” expect $365 billion in 2014

- Construction Spending “nonresidential buildings” expect $314 billion in 2014

- Construction Spending “totals” expect $961 billion in 2014

2014 Residential spending = $354 billion

2014 Nonresidential spending = $320 billion

2014 Total Construction spending = $960 billion

These values prior to U.S. Census major correction to data.

Posted August 2014

- If you are pricing future construction jobs the way you always have, with 2-3 pct escalation, you are already in trouble!

- If you’re an owner with plans to construct a building in the future and you are inflating cost by only 2-3 pct, you’ve missed the boat.

Total construction inflation for 2013-14-15 was 4.3%, 4.7% and 2.9%. All years were reduced by a lack of inflation in infrastructure work. Inflation for nonresidential buildings was 3.5%, 4.2% and 4.8%. Residential buildings inflation was 8.9%, 7.1% and 4.1%.

Posted September 2014

- Real Construction Volume in 2014 (construction spending minus inflation) will grow less than 2 percent

Real construction volume in 2014 increased 4.9%. Commercial nonresidential construction started it’s current boom.

Posted Dec 2014

- Construction Spending “residential buildings” expect $405 billion in 2015

- Construction Spending “nonresidential buildings” expect $364 billion in 2015

- Construction Spending “totals” expect $1,040 billion in 2015

Posted Jan 2015

- Cash flow of new starts for nonresidential buildings indicates a 15% increase in the monthly rate of spending over the next 10 months.

- Both ABI and Starts cash flows indicate a mild slowdown in nonresidential buildings construction spending at the end of 2014 before a strong upturn in spending in 2015. Expect another drop in spending late in 2015

For the period Nov 2014 through Feb 2015, spending on nonresidential buildings stalled flat for 4 months. The monthly rate of spending increased 14% over the 10 months from Oct 2014 to September 2015. Since Sept 2015 spending has been flat.

Posted March 2015

- Even if new starts turn flat for rest of 2015, starts already recorded are indicating Nonresidential buildings construction spending for 2015 will reach 15%+ growth. My closest competitor is forecasting 12.5% growth. The average of all other industry forecasts is 8% growth.

Spending for nonresidential buildings actually hit +17% growth over 2014.

Posted July 2015

- Construction Spending “residential buildings” expect $388 billion in 2015

- Construction Spending “nonresidential buildings” expect $397 billion in 2015

- Construction Spending “totals” expect $1,067 billion in 2015

2015 Residential spending = $390 billion

2015 Nonresidential spending = $387 billion

2015 Total Construction spending = $1068 billion

These values prior to U.S. Census major correction to data.

Posted July 2015

- Nonresidential Buildings spending growth 2015 vs 2014.

- My forecast (Average all others) [closest competitor]

- Educational 7.1% (3.8%) [5.6%]

- Healthcare 6.0% (3.9%) [4.0%]

- Commercial/Retail 5.5% (11.8%) [8.4%]

- Lodging 24.0% (13.7%) [17.1%]

- Office 21.1% (13.5%) [19.2%]

- Manufacturing 49.6% (15.9%) [24.6%]

Educational 6.7%

Healthcare 4.6%

Commercial/Retail 8.4%

Lodging 30.8%

Office 21.9%

Manufacturing 47.3%

So there you have it. Several years of forecasts and how they turned out. You can get an idea of my track record. You be the judge. 🙂