Why the big slow down in construction jobs this Year? Is work volume on the decline? Are labor shortages to blame?

These days, the most talked about reason for slower jobs growth is the lack of experienced workers available to hire. In fact, recent surveys indicate about 70% of construction firms report difficulty finding experienced workers to fill vacant positions and the Job Openings survey has been at highs for several months. That certainly cannot be overlooked as one reason for slower jobs growth, but that is not the only reason?

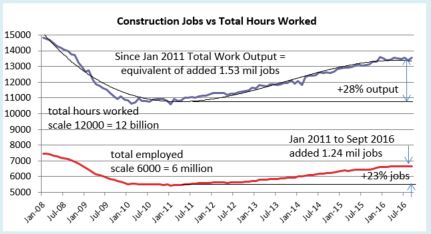

Although recent growth has slowed, even with all this talk of difficulty finding experienced construction workers, there has been very good jobs growth. For the 5 ½ year period from the low point in January 2011 to the present (August 2016) we added 1,240,000 construction jobs.

- Jobs increased by 23% in 5 ½ years.

- Spending growth increased 52% in that same 5 1/2 years.

Why is it that jobs don’t increase at the same rate as construction spending? Because much of that spending growth is inflation, not true volume growth. Volume is construction spending minus inflation. To get volume, convert all dollars from current $ in the year spent into constant $ by factoring out inflation.

- Spending growth is not a true measure of increase in real volume.

- Jobs growth should not be compared to spending growth.

Now that we have spending converted to volume, we need to adjust jobs to get real work output. The total hours worked affects the entire workforce so has a significant impact on output.

- Jobs is not a true measure of work output.

- Jobs x hours worked gives total work output.

Spending must be factored to remove inflation and jobs should be factored to include any change in hours worked.

- In the 5 1/2 years from Jan 2011 to mid 2016, real construction volume and jobs/hours real output both increased by 28%.

Now we see over the long term, job/hours and real volume are moving in tandem. But there are always short term periods when they do not and that causes ups and downs in productivity.

In 2014-2015, jobs/hours grew by 11%, the fastest growth for a two-year span in 10 years. Real volume of work increased by 16% producing a real net increase in productivity. But productivity had declined significantly in 2010 and 2011. It’s not unusual to see productivity balancing out over time. In part, this is due to companies balancing their total employees with their total workload.

From October 2015 through March 2016, jobs growth was exceptional. 214,000 construction jobs were added in 6 months, topping off the fastest 2 years of jobs growth in 10 years. That is the highest 6-month average growth rate in 10 years. That certainly doesn’t make it seem like there is a labor shortage. However, the jobs opening rate (JOLTS) is the highest it’s been in many years and that is a signal of difficulty in filling open positions.

- For the 6-month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of consecutive months jobs growth in 10 years. Then, after 3 months of job losses, July, September and October show modest gains.

I would expect growth such as we’ve had for two years and then that 6 month period to be followed by a slowdown in hiring as firms try to reach a jobs/workload balance. It appears we may have experienced that slowdown. Jobs declined for four of five months from April through August. Keep in mind, this immediately follows the fastest rate of jobs growth in 10 years. But it also tracks directly to three monthly declines in spending. (I predicted this jobs slowdown in my data 9 months ago. I predicted the 1st half 2016 spending decline more than a year ago).

It is not so unusual to see jobs growth slowed for several months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years of jobs growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

If spending plays out as expected into year end 2016, then construction jobs may begin to grow faster in late 2016. However, availability could have a significant impact on this needed growth.

Availability already seems to be having an effect on wages. Construction wages are up 2.6% year/year, but are up 1.2% in the last quarter, so the rate of wage growth has recently accelerated. The most recent JOLTS report shows we’ve been near and now above 200,000 job openings for months. With this latest jobs report, that could indicate labor cost will continue to rise rapidly.

As wages accelerate, also important is work scheduling capacity which is affected by the number of workers on hand to get the job done. Inability to secure sufficient workforce could impact project duration and cost and adds to risk, all inflationary. That could potentially impose a limit on spending growth. It will definitely have an upward effect on construction inflation this year. If work volume accelerates, expect labor cost inflation to rise rapidly.