Home » Labor (Page 2)

Category Archives: Labor

Construction Jobs / Workload Balance

11-7-17

The last time construction jobs and workload were balanced was 2005. From 2006 through early 2011, workload dropped 15% greater than the decline in jobs. In other words, compared to 2005, contractors started the post-recession period in 2011 with 15% less workload on hand compared to the number of workers kept on staff and that resulted in the period 2006-2011 posting the largest productivity decline ever recorded.

For a discussion on data plotted 2001 to 2011, see this post Jobs vs Construction Volume – Imbalances. In the 2001-2011 plot above, jobs and workload are set to zero baseline in Jan 2001. This shows all of 2001 through 2004 that jobs/workload was balanced. The gap between the red and the blue lines above is the variance from zero change in Jobs/Workload balance. By Jan 2011 there was a 15% workload deficit.

The 1st quarter of 2011 was a dramatic turning point. Both jobs and work volume began to increase. To visualize the variance since Jan 2011, the following plot resets jobs and workload to zero baseline in Jan 2011.

From Jan 2011 to Jun 2015, construction volume increased 24% in 4 1/2 years. Staffing output increased 19% in the same period. Contractors may still feel the effects from not being able to grow staff at that same pace as volume during that period. However, we did see the larger work volume increases make up 5% of the 15% workload deficit from the previous period 2006-2011, but it loses sight of the fact that after almost five years we had not recouped the entire lost work output from all the other 10% staff imbalance that still remained.

Work output is defined as jobs x hours worked. Construction volume is defined as spending minus inflation.

From Jul 2015 to Oct 2017, volume increased just over 1% but jobs output grew by almost 7%. During that two year period, new jobs created plus the change in hours worked by the entire workforce grew 6% more than workload. Jobs increased greater than construction volume increased. The plot shows most of that variance occurred in 2015.

Shifting the time periods slightly gives another impression of the data, overall not much different. In discussions about Construction skilled labor shortages, it’s important to understand, both construction spending and volume are at record growth levels and jobs, since recession, and in last 3 yrs, have matched volume growth.

Overall, in the seven-year post-recession period Jan 2011 to Oct 2017, volume increased 25% and jobs output increased 26%. There seems very little room to be calling this a jobs shortage. Of course, this does not address skills.

So here we are most of the way through 2017 and if we look back at the last 11 years, not only are jobs once again increasing faster than workload, but also in total since 2005 we still have 14% staff that would need to be absorbed by new workload to return to the previous jobs/workload productivity balance.

Maybe it’s time we stop calling this a jobs shortage and start referring to it as a productivity challenge that needs to be turned around.

For an expansion of more information on this topic see Jobs vs Construction Volume – Imbalances posted 8-8-17. Included is the 2001-2011 plot that explains all of 2001 through 2011.

Also, Feb 208 article breaking out residential and nonresidential sectors shows surplus in nonres and deficit in residential Residential Construction Jobs Shortages

Jobs vs Construction Volume – Imbalances

8-8-17

From January 2001 to June 2017, jobs growth exceeded construction volume growth by 13%. The attached plots show the imbalances in growth.

Jobs growth is # of jobs x hours worked.

Volume is construction spending adjusted for inflation, or constant $.

Sometimes rapid spending growth is accompanied by higher than average inflation. This occurred in the 1990’s and again in 2005-2006. While spending seems to indicate rapid growth, much of the growth in cost is inflation and volume growth can be significantly lower, even sometimes negative, as occurred in 2005-2006. However, jobs growth during these rapid spending growth periods appears to track much more in line with spending growth. This leads to over-hiring and a loss of productivity occurs.

There are two distinct periods when jobs growth advanced more rapidly than real construction volume, 2005-2006 and mid-2015 to mid-2017. In the eight year period in between, either jobs fell faster or, after January 2011, volume increased faster. If spending growth is used to compare, then jobs growth falls far short of construction spending. But, due to inflation, spending is not the correct parameter to compare to jobs. Jobs must be compared to volume. Since 2001, the imbalance shows jobs growth has exceeded volume growth.

2001 through mid-year 2017, jobs exceeded volume growth by 13%.

2001-2004 jobs and volume growth were nearly equal.

2005-2006 jobs growth exceeded volume growth by 20%. During this period, construction spending and volume reached a peak. From late 2004 into early 2006, we experienced 20% growth in spending, the most rapid growth period on record. But that was also the period of the most rapid inflation growth on record. Residential volume peaked in early 2006 but then dropped 20% by the end of 2006. Nonresidential spending was increasing, but almost all of the growth was inflation. Nonresidential volume remained flat through 2006. Inflation was greater than spending growth, so volume declined. Although volume declined, hiring continued and jobs increased by 15%.

2007-2010 volume exceeded jobs growth by 4%. Spending decreased by 30%. Both volume and jobs were in steep decline. More jobs declined than volume, however, this period started with nearly 20% excess jobs. For January 2010 to January 2011, jobs bounced around near bottom, but volume dropped 8% more. 2010 ended with an excess of 15% jobs. January 2011 was the low-point for jobs.

2011-June 2015 volume exceeded jobs growth by 10%. Spending increased by almost 40% and inflation was relatively low at only 3%/yr. This period helped absorb more than half of the excess jobs that were created in 2005-2006 and remained after 2010. By mid-2015, jobs exceeded volume by only 7%.

June 2015-June 2017 jobs growth exceeded volume by 7%. Spending increased by 7%, but inflation was 7% over the same period. Although volume was up and down, over this two-year period through June 2017 we posted zero growth in volume. All of the increase in spending was inflation. Jobs increased 7% in two years.

For the last 5 years, 2012-2016, jobs averaged 4.5%/yr. growth Construction spending averaged 8.5%/yr. growth. Inflation, currently hovering around 4.5%, averaged about 3.5%/yr. during this period. So real volume growth was only 4% to 5%. In the first few years of the recovery, 2011-2014, the gap narrowed and volume improved over jobs, but for the last two years, jobs have been increasing faster than volume.

I do expect spending to continue at a 6% to 7% growth rate at least through 2018. But also, I expect inflation at 4% to 4.5%. If the spending forecast holds, and if jobs growth comes into balance, then that would indicate only a 2% to 3% jobs growth rate from now through 2018.

Also SEE Construction Jobs Growing Faster Than Volume 5-5-17

and Is There a Construction Jobs Shortage? 3-10-17

Here is the 11-7-17 extension of latest info Construction Jobs / Workload Balance

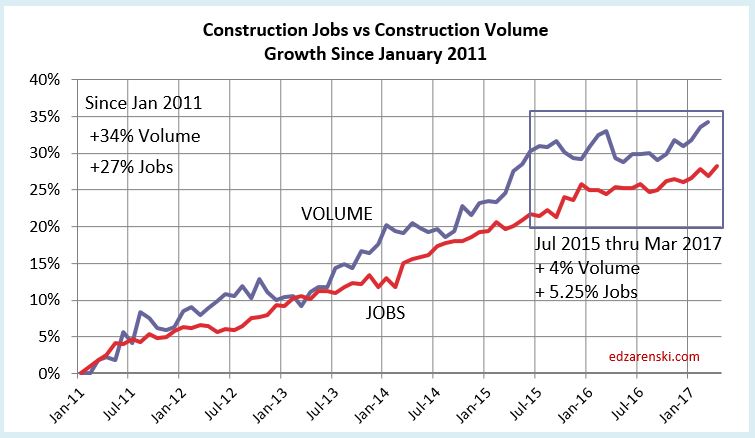

Construction Jobs Growing Faster Than Volume

5-5-17

Jobs growth slowed in the last two months adding only 6,000 construction jobs since February. However, a longer term look at jobs x hours worked vs volume growth gives better information.

In the following plot Jobs (red line) = # of jobs x hours worked and Construction Volume (blue line) = construction spending in constant $ (adjusted for inflation). Unless we make these two adjustments we cannot compare jobs to construction spending and get any meaningful analysis from the data.

I’ve written about this in-depth in these two articles.

A Harder Pill To Swallow! and Is There a Construction Jobs Shortage?

You can see in the plot above from Jan 2011 to Mar 2013 both jobs growth and volume growth balanced. Then again by August 2014 jobs growth caught up to volume growth. It was the period from Aug 2014 to Jul 2015 when volume took off and climbed much faster than jobs growth. But then, since July 2015, jobs have been increasing faster than construction volume growth.

In a plot of this information back to 2005, it would show that by the end of 2010 there were already excess jobs. That is discussed in the attached articles. During the expansion, firms hired more employees than real work volume could support, then during the recession, firms held onto far more staff than was required to perform the available declining work volumes. So the chart above would start 2011 with an excess of jobs and really we needed to see work volume increase faster than jobs starting in 2011.

Long term, having started 2011 with not enough volume to support the remaining staff, we see two periods of growth in which jobs and volume were balanced, only one period where volume exceeded jobs growth and then this latest period, for the last 21 months, in which jobs are growing faster than volume.

There are many reports of job shortages and they appear to be genuinely accurate assessments, primarily regarding some very specific skilled labor positions. However, long term jobs vs volume data shows there is far more in play than not enough workers to hire. In fact, for the last 21 months, hiring has exceeded workload and that simply does not indicate an overall worker shortage.

A Harder Pill To Swallow!

4-8-17

I’ve been saying for a long time the data doesn’t show a construction jobs shortage.

In total, construction jobs have been increasing faster than construction volume (spending minus inflation). But, to get a better picture we need to look at jobs vs volume by sector, Residential and Nonresidential. Then we need to look at history.

Since 2009, RESIDENTIAL volume has increased 49%, jobs increased 22%. This is partly explained by absorption of excess staff retained during recession.

From 2006 to 2009 volume decreased 53% but jobs decreased only 36%, leaving a significant amount of excess jobs.

It looks like from 2009 to 2016 there has not been enough jobs growth to support the volume growth, BUT…

Residential net changes just since 2006, volume is down 29% while jobs are down 22%. We are not nearly back to pre-recession productivity.

Since 2009, NONRESIDENTIAL BUILDINGS volume is down by 10% but jobs are up 13%. By no means, if we look at just these 7 years, does this look like a jobs shortage.

Even previous years imbalance would not account for a need to add that many jobs. From 2006 to 2009 volume increased 2% but jobs decreased 15%. In a previous report Is There a Construction Jobs Shortage? I explained why this may occur following a prior top-heavy jobs expansion during a period of high inflation.

Nonresidential net changes just since 2006, volume is down 8% but jobs are down only 3%. Again, we are not nearly back to pre-recession productivity.

For both residential and nonresidential buildings, comparing post-recession growth to pre-recession 1996-2006 $ Put-In-Place per Job, productivity is down 21%, or we currently have 100/(100-21) = 27% more jobs now than it took before to get the same amount of work done.

If the current construction expansion period is viewed as having a jobs shortage, that claim demands that we must accept, since pre-recession, productivity has declined by 21% and the reason there is now a jobs shortage is that it takes 27% more jobs to put in place construction than it did on average from 1996 to 2006.

In my opinion, that’s a harder pill to swallow than a jobs shortage.

For more related to this discussion see Is There a Construction Jobs Shortage?

Is There a Construction Jobs Shortage?

3-10-17

The imbalance between construction spending and construction jobs is nothing new. It’s been going on for years. It reflects more than just worker shortages. It captures changes in productivity due to activity. It also helps explain why sometimes new jobs growth rates do not follow directly in step with spending growth. A big part is that it reflects hiring practices. That imbalance can be affected by either over or under-staffing and that can be affected by inflation.

2000-2008 The Expansion

For the 1st several years, nonresidential construction spending was flat or down. Then for two years spending was up only slightly, but constant $ volume (spending inflation adjusted) had actually decreased. Nonresidential jobs fell from 2001-2003 but then grew for several years during this period when constant $ volume was decreasing, creating productivity losses.

On the other hand, residential spending grew 80%, but after adjusted for inflation, volume grew only 23%. Most staffing increases during this period were for residential construction and jobs/volume growth was pretty consistent. Residential saw mixed productivity during this period. In 2006 residential volume had already started declining.

It is not uncommon when work is plentiful that productivity declines. In 2004-2005, spending increased by 24%, but inflation was hovering around 8% to 9%/year. Constant $ volume (spending after inflation) increased by only 6%. Jobs grew faster, by 9%. Net productivity decline.

In 2006, nonresidential work was starting to take off, increasing 45% from 2006 though 2008. During this period jobs increased by only 8% and volume added 16%. Excess volume was able to absorb a good portion of the jobs/volume imbalance from 2000-2006.

See the line chart below “Productivity = Annual $ Put-In-Place per worker. These up or down periods for each of these sectors discussed here can easily be seen in rising or falling $PIP volume on that chart, sectors plotted separately. The bar graph “Total Annual Productivity Change”, is the composite total of the three sector graphs.

Net volume in 2006 declined, but jobs increased another 5%. For the three-year period 2004-2006, spending increased by 28%, but after inflation, real volume increased by less than 5%. Jobs increased by 14%. Productivity declined by nearly 10%.

Heading into 2007, residential firms had excess staff, as measured by the negative imbalance of jobs/volume. Compounding productivity issues, when spending started to decrease significantly, it took longer for companies to downsize their workforce. The workforce was not reduced to match the volume of work lost. Residential construction was first to show the strain, already having started to decline in 2006 and continuing to decline through 2009.

2006-2010 The Residential Recession

Residential construction was 1st hit by the recession in early 2006. For the 4 years 2006-2009, residential volume dropped 55%. It remained flat for two more years, down a few more percent. Over six years starting 2006, residential jobs dropped only 40%.

The Annual $ PIP line chart above shows that for 2006-2009 there were only residential losses, or negative balance between jobs/volume. Both nonresidential sectors were improving slightly at the time. The total negative bars in those years is entirely due to residential.

2009-2011 The Nonresidential Recession

Nonresidential Buildings construction didn’t fall into recession until 2009. In the two years 2009-2010, nonresidential buildings lost over 30% in volume but only 22% in jobs.

This chart simply shows the imbalance between the number of jobs and the dollar volume of work put in place for each year compared to the year before. In a simple form that can be referred to as a change in productivity. In all these charts, jobs/year are adjusted for hours worked and dollars are always constant $ inflation adjust to 2016$.

In 2009 my chart shows a huge productivity gain. It is almost entirely due to Non-building infrastructure, which never did fall into deep recession. Combined residential and nonresidential buildings only in 2009 would have shown a net 1% gain.

2011-2012 Early Recovery

Starting 2011, firms had lost significant revenue but had retained more staff than needed. There was so much excess staff (in relation to how much total revenue was available) that almost no reasonable gains in spending could wipe away the losses in productivity. Volume improved by 1%, but hiring resumed and jobs grew by 1%. Due to excess staff still on payrolls, productivity showed a 6% decline.

For the next few years, when we look at jobs growth vs. volume growth, there is reason to believe that slow jobs growth (2011 through 2013) may not be all due to labor shortages. Although we lost more than 2 million jobs, there remained excess jobs when compared to the amount of volume that was available.

At least part of the blame for slower new jobs growth was that excess staff already on hand were being absorb by the new spending gains. For a period there was insufficient volume out in the market to support all the staff that had remained on board. Finally, there was increased revenues which would first reabsorb part of the excess labor before rehiring started.

2012-2016 The Construction Boom

It took three more years to see a significant move towards balancing jobs and real volume. In 2014, jobs increased 6% and constant volume increased 7%. For the first nine months of 2015, jobs increased 3% and volume increased 8%. This was a good productivity balance period.In the three years 2012-2014, volume increased 16% but new jobs grew by only 11%. The increased work volume absorbed a good portion of the excess staffing.

What reasons could cause contractors to think they need more staff?

One reason may be that contractors don’t typically track revenues in constant dollars, they track in current dollars. So any comparison to a previous year is to inflated data. To achieve business plan growth of 6%/year, is it necessary to grow staff by 6%/year? Not if during that period inflation is 4%. Then real volume growth is only 2%/year and new staffing needs are far less than anticipated.

Basing staffing needs on current $ revenue growth can lead to the same kind of over-staffing we saw going into the recession. In the three years 2004-2006, construction spending increased 30%. Jobs increased 16%. However, during that three-year period construction inflation was the highest ever recorded, composite inflation averaging greater than 8%/year. After inflation, real construction volume increased only 4% during that period. Hiring far exceeded the rate of real volume growth. There is the potential that contractor’s hiring could be swayed by highly inflated spending when actually volume is not as strong as thought.

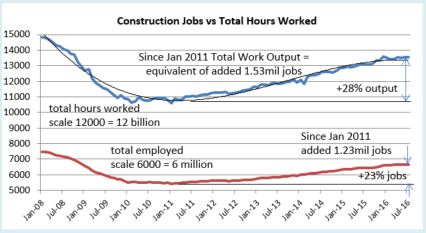

From the Jan 2011 bottom of the construction recession through Dec 2016, both work output (jobs x hours worked) and volume (spending after adjustment for inflation) increased equally by 29%.

(note: BLS revisions to hours worked, issued in the 3-10-17 release changed total growth output from 29% to 30%).

There are always unequal up and down years, but this longer term period shows balanced growth returned after a tumultuous period. We were so far down on the scale after the recession it seems reasonable that we experienced this re-balancing.

Both 2014 and 2015 show productivity gains. That is unusual in that there have not been two consecutive years of productivity gains in 23 years (while my jobs data goes back to 1970, spending data goes back only to 1993).

The trend changed in October of 2015. Now when we look at jobs growth vs. volume growth, there is reason to believe that any jobs growth slow-down may be at least in part due to recent over-hiring.

2014-2016 Record Jobs Growth

In the last three years, we’ve added 840,000 construction jobs. We’ve also increased hours worked to an equivalent to 880,000 jobs, growth of 15%. That’s a faster rate of growth in three years than the 2004-2006 construction boom. To help explain that growth, real volume in 2014-2016 was far greater than the volume in 2004-2006, or any other three-year period for that matter. The last time we’ve seen jobs growth like this was 1995-1999.

2012 through 2016 is the greatest construction boom on record, whether measuring unadjusted current $ spending or constant $ real volume after inflation, flying past the 2000-2005 boom and narrowly beating out 1995-2000. And we started 2017 with backlog at a record level, so the boom continues.

5-Year Construction Booms Compared to 2012-2016

- 2012 – 2016 current $ +$377 bil +48% — constant $ +265 bil +29%

- 2001 – 2005 current $ +$314 bil +39% — constant $ +30 bil <3%

- 1996 – 2000 current $ +$254 bil +46% — constant $ +235 bil +21%

Notice how little growth actually occurred in the five-year period 2001 through 2005. While there was significant spending growth, most of it was inflation, and 90% of it was residential. During that period composite inflation increased more than 35%. Also, nonresidential construction was having a setback, dropping 15% in volume in that five years. The real story out of the 2001-2005 boom period is to compare residential work.

- 2012 – 2016 Rsdn current $ +$211 bil +83% — constant $ +146 bil +46%

- 2001 – 2005 Rsdn current $ +$280 bil +80% — constant $ +132 bil +23%

Residential inflation 2001-2005 was a whopping 47%. But, total residential spending was up 80%. After adjusting for inflation, residential still added 23% to volume during that period. During both periods, residential volume grew more than jobs, so both periods had a net productivity gain.

Also in 2001-2005, nonresidential added 3% more jobs in a five year period in which volume dropped 15%. The very high levels of inflation help explain why staff may have grown to such excess during that period. Contractors were seeing revenues grow by 20%-30% and were slowly adding jobs in a period when real volume was dropping 3% per year.With the exception of residential growth, there was a downturn in other work. New jobs increased by only 11%, but due to rampant inflation, real volume increased by less than 3%. Nonresidential contributed all the negative productivity in 2001-2005.

2014-2015 Construction Spending for the Record Books

- 2014 to 2015 current $ +$206 bil +23% — constant $ +158 bil +16%

No two consecutive years of construction come close to equaling the real volume put-in-place during 2014-2015. The two years 2004-2005 had greater growth in spending, but most of that was inflation, so had little growth in volume. In fact, we would need to consider three consecutive years to come close to 2014-2015 and the three years that comes closest is 1996-1998 and that would still be a few percent short. This volume growth is driving huge jobs growth.

From October 2015 through March 2016, jobs growth was exceptional. During that 6 month period we added 215,000 construction jobs, the fastest jobs growth period in a decade. That period topped off the fastest two years of jobs growth in 10 years. Record increases in jobs growth are not what we might expect if there is a labor shortage.

And yet, the Jobs Opening and Labor Turnover Survey (JOLTS) is the highest it’s been in many years and that is a signal of difficulty in filling open positions. But, one of the known factors during a high level of market activity (lot’s of construction work – we are at record levels) is that workers know there is another and sometimes better job just down the road. During high levels of activity, unless the current employer is paying some kind of premium to keep them, workers may leave for greener pastures. That creates a high level of job churn.

Hiring Changes Lag Volume Changes

It is important to take note that it appears the two most recent six-month surges in jobs lag the period of greatest volume growth. I noted earlier that contractor staffing changes seem to lag movements in volume.

Since Sep 2015, jobs have been increasing more than real construction volume. For much of 2014 and 2015 construction spending real volume growth was exceeding jobs growth. Spending in 2016 slowed from the all-time record levels. That’s not totally unexpected as it would be highly unusual for that record level of growth to continue. But hiring continues.

Since Sept 2015, construction volume growth (spending minus inflation) slowed or stalled and completely contrary to what one would expect in a labor shortage, new jobs growth has been exceeding volume.

- From Sep15 to Mar16 jobs increased+3.3%, volume increased +1.6%

- From Mar16 to Aug16 jobs had no change, volume decreased -3.3%

- From Aug16 to Feb17 jobs increased +2.6%, volume increased +0.10%

This most recent six-month period posted 177,000 jobs, the 3rd best for any consecutive six months since 2005-2006. Although we experienced a slow down in new jobs through the middle of 2016, that was bracketed by two of the three strongest six month growth periods in more than 10 years. For 18 months Sep’15 to Feb’17, jobs are up 7% higher than volume. For 2012-2014 volume grew 6% more than jobs.

For 2017, several economists are predicting total construction spending will increase by just over 6% (including my estimate of 6.5%). However, I’m also predicting that combined construction inflation for all sectors will increase by about 4.5%. That leaves us with a net real volume growth of only 2.0%. Therefore, for 2017, I do not expect jobs to increase by more than 2.0%, or 140,000. That number seems hard to swallow given we are already at 98,000 in the first two months. But remember, jobs have been growing faster than volume for the last 17 months. We could be due for another no-jobs-growth absorption period.

If jobs increase more than 140,000 and both spending and inflation hold to my predictions, then jobs will continue to outpace volume and that will show up on my plot as a productivity loss for 2017. Jobs have been getting ahead of volume for 17 months. Contractors may still be hiring, lagging the movement in real volume growth. It will take the next few months to see if that is the case but I would expect jobs growth to slow or stop for the next few months and I would not attribute that to labor shortages. As we’ve seen before, we should expect jobs/volume to come back to balance. (post note: following Jan-Feb when, after revisions, we added 88k jobs, in the next 5 months we added only 13k jobs. Jobs growth almost stopped for 5 months.)

So, here we are powering our way through the greatest construction expansion ever recorded, with three years of jobs growth at a 11-year high and jobs growing faster than volume for the past 17 months. Does that seem like a jobs shortage to you?

For a continuation of this discussion see A Harder Pill To Swallow! and Construction Jobs Growing Faster Than Volume

Saturday Morning Thinking Outloud #3 – Construction Jobs

Why the big slow down in construction jobs this Year? Is work volume on the decline? Are labor shortages to blame?

These days, the most talked about reason for slower jobs growth is the lack of experienced workers available to hire. In fact, recent surveys indicate about 70% of construction firms report difficulty finding experienced workers to fill vacant positions and the Job Openings survey has been at highs for several months. That certainly cannot be overlooked as one reason for slower jobs growth, but that is not the only reason?

Although recent growth has slowed, even with all this talk of difficulty finding experienced construction workers, there has been very good jobs growth. For the 5 ½ year period from the low point in January 2011 to the present (August 2016) we added 1,240,000 construction jobs.

- Jobs increased by 23% in 5 ½ years.

- Spending growth increased 52% in that same 5 1/2 years.

Why is it that jobs don’t increase at the same rate as construction spending? Because much of that spending growth is inflation, not true volume growth. Volume is construction spending minus inflation. To get volume, convert all dollars from current $ in the year spent into constant $ by factoring out inflation.

- Spending growth is not a true measure of increase in real volume.

- Jobs growth should not be compared to spending growth.

Now that we have spending converted to volume, we need to adjust jobs to get real work output. The total hours worked affects the entire workforce so has a significant impact on output.

- Jobs is not a true measure of work output.

- Jobs x hours worked gives total work output.

Spending must be factored to remove inflation and jobs should be factored to include any change in hours worked.

- In the 5 1/2 years from Jan 2011 to mid 2016, real construction volume and jobs/hours real output both increased by 28%.

Now we see over the long term, job/hours and real volume are moving in tandem. But there are always short term periods when they do not and that causes ups and downs in productivity.

In 2014-2015, jobs/hours grew by 11%, the fastest growth for a two-year span in 10 years. Real volume of work increased by 16% producing a real net increase in productivity. But productivity had declined significantly in 2010 and 2011. It’s not unusual to see productivity balancing out over time. In part, this is due to companies balancing their total employees with their total workload.

From October 2015 through March 2016, jobs growth was exceptional. 214,000 construction jobs were added in 6 months, topping off the fastest 2 years of jobs growth in 10 years. That is the highest 6-month average growth rate in 10 years. That certainly doesn’t make it seem like there is a labor shortage. However, the jobs opening rate (JOLTS) is the highest it’s been in many years and that is a signal of difficulty in filling open positions.

- For the 6-month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of consecutive months jobs growth in 10 years. Then, after 3 months of job losses, July, September and October show modest gains.

I would expect growth such as we’ve had for two years and then that 6 month period to be followed by a slowdown in hiring as firms try to reach a jobs/workload balance. It appears we may have experienced that slowdown. Jobs declined for four of five months from April through August. Keep in mind, this immediately follows the fastest rate of jobs growth in 10 years. But it also tracks directly to three monthly declines in spending. (I predicted this jobs slowdown in my data 9 months ago. I predicted the 1st half 2016 spending decline more than a year ago).

It is not so unusual to see jobs growth slowed for several months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years of jobs growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

If spending plays out as expected into year end 2016, then construction jobs may begin to grow faster in late 2016. However, availability could have a significant impact on this needed growth.

Availability already seems to be having an effect on wages. Construction wages are up 2.6% year/year, but are up 1.2% in the last quarter, so the rate of wage growth has recently accelerated. The most recent JOLTS report shows we’ve been near and now above 200,000 job openings for months. With this latest jobs report, that could indicate labor cost will continue to rise rapidly.

As wages accelerate, also important is work scheduling capacity which is affected by the number of workers on hand to get the job done. Inability to secure sufficient workforce could impact project duration and cost and adds to risk, all inflationary. That could potentially impose a limit on spending growth. It will definitely have an upward effect on construction inflation this year. If work volume accelerates, expect labor cost inflation to rise rapidly.

Construction Jobs – Is July a Turning Point?

8-6-16

The July jobs report issued yesterday gives us labor data to compare to spending. Here’s a few tweets I put out yesterday.

From Sep to Mar spending increased by 4.5% but jobs/hours increased by only 3% = productivity gains. Now seems to be reversing.

Since March, construction spending is down 3.7%, construction jobs are down 0.3%. Beginning to see 2015 productivity gains reset.

Last 12mo Residential Construction Spend up 3%, rsdn jobs up 5%. Next few months room for spend to grow with little jobs growth = Balance

Construction Workforce portion identified as in force but unemployed at 16 year low. Yes, there is a labor shortage.

While the immediate comparison we read is often what happened this month versus last month, for comparison to construction spending it is perhaps better to look at recent longer trends.

- For the 6 month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of growth in 10 years. Then, after 3 months of losses, July shows a modest gain.

- During that same period Q4’15 spending was flat but by the end of Q1’16 spending had increased more than 4% in 6 months, or at an annual rate of 8% to 9%.

- Even though some upward revision is expected for June spending, total Q2’16 spending will still be down 2% to 3% from Q1.

- Q2’16 jobs declined all 3 months, keeping in mind this immediately follows the fastest rate of growth in 10 years. But it also tracks directly to three monthly declines in spending.

- Since Q1 2011 the constant $ value of construction spending after inflation increased by 30%. Jobs/hours worked output increased by 28%.

It is not so unusual to see jobs growth slowed in these last few months. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

We got modest growth in July that I hope to see continue for the 2nd half 2016. I expect spending to experience strong growth in the 2nd half and jobs growth should follow closely, perhaps adding 125,000 to 150,000 more jobs. However, although I do expect both spending and jobs growth, jobs could be somewhat restrained by lack of available skilled workers.

Trump’s Wall

5-22-16 updated 1-7-19

Trump’s Wall

Recently I received a call from a major national news source. They asked for help understanding what it would take to build “Trump’s Wall.” I’m an estimator, so I provided some realistic analysis of what it would take.

The border with Mexico is almost 2000 miles long. There is already about 700 miles of fence. This analysis makes an assumption it would be necessary to build only 1000 miles of wall. Also, this estimate is based on the type of wall you see along highways, precast concrete sound and site barrier wall. In reality it would need to be significantly more robust than the typical highway sound-barrier wall, and I’ve taken that into consideration in my estimate. So here goes.

(9-1-16 >>In some other recent articles I’ve read they have suggested a 40 foot high concrete wall. Well, I don’t think you can build a 40 foot high unsupported concrete wall (no bracing at sides) without getting into extremely massive volumes of materials. Such a high concrete wall would need to be much thicker at the base than at the top and the foundation to prevent overturning would need to be massive. Typical rule of thumb for foundation to prevent overturning is the foundation needs to be ~40% as wide as the height of the wall. The volume of concrete would be 4x to 5x what I’ve estimated for the wall I’ve defined here and the excavation, back fill and formwork would add considerable time to complete. Order of Magnitude I guess 40 to 50 million cubic yards of concrete for wall and foundation. I would roughly guess such a massive poured concrete foundation and wall, if it could even be built, would cost THREE TO FOUR TIMES what I’ve estimated here and would require substantially more labor and might take twice as long or more to build.)

This estimate is based on 8″ thick precast heavily reinforced concrete wall panels set between steel columns 12’0 on center. Even if the concrete could be chipped away, the reinforcing bars would prevent passage. Columns are set in 6’0 dia. x 10’0 deep column foundations. Between column foundations under the wall is a continuous footing to help resist overturning of the wall. The wall extends 25 feet above grade and 5 feet below grade. Bottom of concrete footing under the wall is 7’0 feet below grade. Bottom of column foundations is 15’0 below grade. The wall would be much higher than the approximate 12′ shown in the representative photo.

The foundations included here are based on up-sizing components from a known design for a 15′ high prison un-climbable open-mesh fence. Even with an open mesh fence design, to overcome wind load, column footings were 2″0″ dia x 8’0″ deep concrete post foundations set every 8′ apart. This solid wall 25′ high would have enormously greater wind loads and it is the foundation that must be designed to prevent overturning.

Just to get quickly to the end, I calculated the final cost of a 25′ high precast wall, foundations, excavation and access roads in the vicinity of $25 billion (in 2016 $), $10 million per mile or slightly less than $2,000 per lineal foot of wall. I’m fairly certain this estimate is somewhat low and the actual cost due to the many unknowns would be higher. At the end I’ve pointed out some of the issues that could generate unknown costs.

One huge factor is inflation. Historical average construction inflation is greater than 4%/year. If a $25 billion wall takes 10+ years to build, the total cost over time assuming the historical average construction inflation would be $30 billion.

This is a summary of some of the results from the concrete wall estimate.

Materials

200 million square feet of precast concrete panels = 5.2 million cubic yards of concrete

5 million cubic yards of cast-in-place concrete foundations

Total cement to make the 10.2 million cubic yards of concrete = 2% of annual US cement production.

1.5 million tons of steel = 1.5% of annual US steel production.

25 million cubic yards of excavation required.

6 million cubic yards of that excavated earth must be hauled away and disposed since that volume will be replaced underground with concrete. That’s more than enough to completely fill the Superdome. Or, it’s enough to build a 20 foot wide earthen embankment 20 feet high and 100 miles long.

Delivering the Materials

250,000 truckloads of precast wall panels,

500,000 truckloads of ready mix concrete

50,000 truckloads of steel

200,000 truckloads to haul away excess excavated earth.

This is far from a complete list of materials, because in addition to building the wall, in some places you first need to build a road. Assume about 500 miles of road. You can’t get 1,000,000 truckloads of 30-40 tons each, cranes, excavators and auger drills to a construction site without at least building a compacted gravel road to get there.

Adds 2 million cubic yards of stone for construction equipment road.

Adds 100,000 truckloads of stone

Labor

It takes 5000 to 6000 workers to build $1 billion worth of construction in 1 year.

$25 billion x avg 5500 = 135,000 man-years, or 135,000 workers if it is to be built in 1 year. Or it would take 10,000 full-time workers 13.5 years to build this concrete wall.

If 1,000 men worked on the wall 5 days a week 8 hours a day, it would take 135 years to build it. Therefore, I made the assumption the project would be broken into 50 segments each 20 miles long and looked at two scenarios. What labor would be required to build it in 10 years or 4 years?

4 years: That will require 700 men AT EACH of 50 SEGMENTS concurrently to complete the wall in 4 years. That’s 35,000 men working for 4 years. That is 35,000 trades-worker jobs which does not include Architect, Engineering, Testing and General Contractors management personnel.

1,100,000 truckloads at 50 locations over 4 years is = 20 deliveries per day of 30 to 40 tons each at each of the 50 locations. That works out to 40 truck bypasses per day coming and going, so 30 ton trucks go by (some community) every 12 minutes at every one of 50 locations every workday for 4 years. It is very likely that heavy truck traffic will destroy many if not all the town roads used to access the 50 construction sites. The cost to repair/replace those existing roads is NOT included here, but I suspect it would be in the hundreds of millions.

The 4 year scenario is quite unlikely from just about every standpoint. Labor availability, engineering studies and site preparation of 50 (or more) job sites, mobilization of 35,000 men to 50 job sites, product supply, frequency of deliveries, overcrowding of job site. In reality, 700 men at a job site is probably far more than can be managed. In this scenario the number of job sites would need to be increased, probably to more like 150 to 200 individual job sites. While all aspects seem to limit this choice as viable, it is probably labor and material availability that would have the greatest impact.

10 years: To build the wall in 10 years would require 13,500 workers, or about 250 workers AT EACH of 50 SEGMENTS concurrently to complete the wall in 10 years. That’s 13,500 workers working for 10 years. That is 13,500 trades-worker jobs including General Contractors management personnel but not including Architect, Engineering, Testing, Manufacturing and Delivery.

1,100,000 truckloads at 50 locations over 10 years is = 8 deliveries per day of 30 to 40 tons each at each of the 50 locations. That works out to 16 truck bypasses per day coming and going, so 30 ton trucks go by (some community) every 30 minutes at every one of 50 locations every workday for 10 years. The same heavy truck traffic will destroy many if not all the town roads used to access the 50 construction sites, it just takes longer. The cost to repair/replace those existing roads is NOT included here.

The 10 year scenario is certainly not impossible. Labor availability and mobilization issues are reduced as are product supply and frequency of deliveries.

NOTE 1-7-19 New review of proposed steel barrier changes some materials and has a moderate overall affect on total cost, manpower and time to complete. In question is size of steel section that could withstand installation 25′ to 30′ tall unsupported. For a steel barrier estimate I used tube steel hollow structural sections (HSS) 8x8x3/8 set with 6″ spaces between. The summary from the estimate revises precast panels to 3 million tons of steel. The remainder of the summary is still valid. It changes a little. Total cost came in near $24 billion versus the original estimate for precast concrete wall at $25 billion. However if design would require a heavier section 8x8x1/2 then cost jumps to $29 billion. If design requires concrete filled tubes cost would go up by about $750 million. If 8×8 tubes are rotated 45 degrees, spacing can be reduced and open spaces between tubes can be reduced, steel cost would go down by about $1 billion. Foundation cost may or may not be reduced (by as much as $2 billion), but foundation design to prevent wall overturning is more dependent on wind load than on the weight of the steel above. In any case foundations are massive and still calculate out to about 5-6 million cubic yards of concrete and proximity of concrete batch plants to construction zones could be a major issue. Keep in mind none of this cost includes land acquisition, inflation, housing workers, change orders or building new plants to support job sites with materials.

Best case scenario, at the low end of cost at $22 billion, it would take 10,000 men 11 years to build 1000 miles of steel fence barrier. It is likely that the low end estimate is much to optimistic, citing some issues outlined below.

A word about HSS steel tubes. US annual production for Hollow Structural Sections in 2016 was 1.6 million tons per year. That annual demand does not go away if 3 million tons of tube steel is needed for a wall. Over a period of 10 years, at 0.3 million tons/year, steel needed for a wall would be 20%/year of tube steel production. To prevent shortages, production capacity must increase or that extra tube steel must be imported. The US imports about half of all the steel pipe and tube is uses in a year from South Korea, but most of that is oil industry pipe. Manufacturing mills typically cannot increase capacity by 20% in a year. So, this extra demand for tube steel would either cause shortages or increase imports.

Energy cost just to produce 3 mil tons of steel is enough to power 500,000 homes for 1 year. Energy to produce both steel and concrete probably more than doubles that number.

The money spent is enough to build 70,000 new homes or 500 new high schools.

Gasoline just for all truck deliveries is near 5 million gallons.

The concrete and steel materials gross to 2% of annual US cement production and 1.5% of annual US steel production (for a precast wall), but that represents close to 3% of steel used in construction. (The revised steel barrier reduces precast but increases the steel to 4% of US steel production. It represents 200% of annual tube steel production). About half of all US steel goes into your refrigerators, cars, etc., the other half goes into construction. The materials demand has far more affect than you might think on disrupting normal construction flow. Since it is all localized in one area of the country, the far southwest border, it could potentially represent 20% and 30% of the construction materials capacity in that area of the country, straining the capacity in that area and disrupting the normal volume of construction there for years. This would be detrimental to the rest of the construction industry growth in that area for that period.

This does not address the fact that manufacturing facilities to produce and fabricate the steel and deliver concrete needed at each of the 50 work sites ideally should be spread along this 1000-mile corridor, which is very unlikely. In fact, I suspect it more likely that some locations will not be in close proximity to a materials source, the result either driving cost up or extending duration beyond 4 years, or both. It could require building process plants along the path, for instance, ready-mix concrete batch plants and steel fabrication yards.

The time necessary for land acquisition, design, permitting, environmental study, mass material procurement, construction process planning and mobilization would be many months before construction begins. Although labor availability and the number of sites determines construction duration, 4 years would be a reasonable estimate for construction ONLY IF the 35,000 trades-workers needed can be mobilized simultaneously to 50 job sites, but that is not likely. The 4 years of construction starts when planning, design and permitting are complete. That might take 6 to 12 months.

Construction is experiencing what may be the tightest labor market in over 20 years. Since there are few if any available workers to shift to these new job site locations, we would need to assume much of this work is supported by creating nearly 35,000 new jobs. I looked at the Bureau of Labor Statistics Jobs for metropolitan areas within 100 miles of the border. Several serious problems arise.

In this localized area of the country, along a 1000 mile long 100 mile wide strip, 35,000 construction jobs could potentially be 12% to 15% and possibly as much as 20% expansion of the construction workforce. The maximum 30 yr historical rate of annual construction workforce expansion is 6% nationwide. Normal annual jobs growth is 3% to 4%/year. If one project were absorbing all of the jobs growth in an entire region, there would be no workers available in that region for any other construction activity growth for several years. That’s a major disruption to the local economies of several states.

Such an expansion would be extremely difficult to implement that quickly. The mobilization of 35,000 workers could take a very long time from initial ramping up to full employment, therefore extending the duration to complete the job. Many of these workers could be inexperienced adding further to the project duration. So reaching completion of this work with 35,000 workers would probably take much longer than 4 years. Adding time for planning and more time for ramping up labor, it could be 6 years.

Ramping up then down will soften the blow as the jobs begin to disappear at project completion. It could be pretty hard to generate enough new volume of work to keep all those men working. It will take new volume of $5 billion to $6 billion a year to keep all these workers working.

There’s a great deal to consider about the demand on the workforce to build a border wall, or fence. Let’s look just at Texas. In Texas, there are a total of 775,000 construction workers, the 2nd largest construction workforce in the country next to California. But checking all the major metropolitan statistical areas within 200 miles of the border there are only about 100,000 construction workers. Only about 20% of those workers conduct business in earthwork, concrete and steel, the trades required to build this fence. That’s only 20,000 workers available within 200 miles of the border.

Furthermore, the Texas/Mexico border is 1,250 miles long. If 20,000 workers were spread out evenly along the border (which is most certainly not the case), within any 200 mile stretch and within 200 miles inland, there would be only 3,200 available workers. In some well-populated areas there might be double that, approximately 6,000 workers, but in the less populated areas, there are far less than 3,000 workers within 200 miles of a proposed work zone.

Now let’s assume we need enough workers to build 100 miles of steel fence, somewhere within a 200-mile length and near a well populated area. That’s $2.5 billion of fence. We know that it takes about 5,000 workers a year (5,000 worker-years) to put-in-place $1 billion of construction. So, we need to fill 12,500 worker-years or job-years. That could be 12,500 jobs for 1 year or 1,000 jobs for 12.5 years. How many jobs get filled determines how long it will take to build 100 miles of fence. Well, there are nowhere near enough workers to fill 12,500 jobs to build 100 miles of fence in one year along many sections of the border. In the best case, most of 6,000 workers need to be accommodated with living quarters somewhere along a 200-mile stretch and 12,500 work/years divided by 6,000 available workers means it would take a little over 2 years to build 100 miles of fence.

So, 100 miles of fence would take over 2 years to build, ONLY IF this project could absorb every single available worker in these trades within 200 miles for a period of two years. At the same time, for that 2-year period, there would be no available workers in sitework, concrete and steel trades anywhere else within 200 miles to fill all other normal workload. In less populated areas with only half as many workers available, it would take twice as long, or more.

This brief analysis of cost and constructability does not begin to address issues such as, how would a wall be built anywhere along the 1,000 miles of the Rio Grande river, the border between Texas and Mexico, the 4th largest river in the United States. Assuming such a wall must be built on US soil, a wall would then completely cut off river access from the United States? Or, how would a wall be built through the hundreds of miles of national parks and national wildlife refuges along the border without disrupting natural wildlife migration flow? And, how would it be designed along its 1,000 mile corridor to accommodate drainage across a solid impervious barrier? It seems impractical or at the very least massively environmentally disruptive.

You can see, the logistics would be enormous, impediments loom, adjacent communities would be adversely impacted, the cost is probably far more than the $25 billion estimated and it seems highly unlikely this could ever be completed during the course of a single president’s term.

Construction Volume Growing Faster Than Jobs, and That’s a Good Thing.

2-24-16

The most talked about reason for slower jobs growth is the lack of experienced workers available to hire. In fact, recent surveys indicate about 80% of construction firms report difficulty finding experienced workers to fill vacant positions. That certainly cannot be overlooked as one reason for slower jobs growth, but is that the only reason?

Even with all this talk of difficulty finding experienced construction workers, there is a lot of hiring going on. For the 5 year period 2011-2015 we added 1,100,000 construction jobs with the peak growth rate in 2014 at 6.1%. Jobs increased by 20% in 5 years.

For the two years 2014 + 2015 we added 650,000 jobs, the largest number of jobs in two years since 2004 + 2005. In that two years, jobs expanded by 11%, the fastest percent growth since 1998-1999, the fastest pace in 17 years. But peak growth was in 2014 with slower growth in 2015. I expect even slower growth in 2016.

Construction spending hit bottom at the same time as jobs, the 1st quarter 2011. For the same 5 year period 2011-2015 construction spending increased far more than jobs growth. Why is it that jobs don’t increase at the same rate a construction spending? Because much of that spending growth is just inflation. When describing a shortfall of construction workers, jobs growth should not be compared to spending growth. After adjusting for inflation from Q1 2011 to Q4 2015, we find that construction volume increased by 22% in 5 years.

Now it looks like over 5 years jobs seem to be growing nearly the same as construction volume. It even looks like productivity increased, but that’s still not the whole picture.

Real work output growth is total jobs adjusted by the hours worked each year. From 2011 to 2015 construction hours worked increased by 3.6% from near the lowest on record to the highest ever recorded. The reason this has such a huge effect is hours worked gets applied on all 6.5 million jobs, not just the new jobs added. So, a workforce that grew by 20% worked 3.6% longer hours showing that net total work output actually increased 24.3%.

This data shows that over the last 5 years new volume increased by 22% while work output to produce that volume increased by 24%. Data clearly indicates we have added more work output than the volume of work we have produced. This indicates a drop in productivity over the last 5 years.

It is not uncommon at all that productivity declines during rapid growth. This pattern of growth appears prominently in the last two expansions between 1996 and 2006. Firms may be increasing staff based on revenue without strict attention to real volume growth, only to then slow jobs growth and allow volume production to catch up.

By measuring to previous productivity levels, we could say the construction workforce is currently overstaffed. Of course, spending (and net volume after inflation) is expanding rapidly and with it so must the workforce. But, if there is any hope that eventually productivity will return to previous levels, then we must hope for a minimum increase of 2%+ in volume with no matching additional increase in new jobs or hours worked.

Over the next two years I predict construction spending will increase close to 20%, BUT construction volume will increase only 10%, most of that in 2017. In a previous post, “How Many Construction Jobs Will Be Needed” I predicted jobs will grow by 500,000 to 600,000, only about 8%.

Filling positions with workers less qualified than those who were lost accounts for some of the decline in productivity. Working longer hours also leads to productivity loss. To regain lost productivity, new workers need to gain experience AND overall hours need to be reduced and that workload replaced with new jobs. That’s certainly not likely to happen all in one year, but it may account for some of the reason why volume is currently growing faster than jobs, and that’s a good thing. I expect that will continue at least for the next two years.

Overtime Isn’t Always What It Seems – Lost Productivity Construction

1-30-16

It is sometimes necessary when the situation dictates to increase working hours to achieve a shortened schedule. However, numerous studies can be found to support that Overtime results in lost productivity. There are other factors that affect productivity, but just to address the topic of Overtime, for the moment they will be ignored. This productivity loss set of data is from Applied Cost Engineering, Clark and Lorenzoni, Marcel Dekker, Inc., 1985.

As both hours and number of days worked increases over 5 days and 8 hours, productivity declines. 5 days and 8 hours is considered the norm = 0% productivity loss. Any increase in hours or days above this norm reduces productivity. All values approximate and % loss is loss of production on ALL hours worked.

5 days and 8 hours = 40 hrs @ 0% productivity loss = 40 hrs productive

5 days and 10 hours = 50 hrs @ 7% productivity loss = 46.5 hrs productive

5 days and 12 hours = =60 hrs @ 12% productivity loss = 53 hrs productive

6 days and 8 hours = 48 hrs @ 3% productivity loss = 46.5 hrs productive

6 days and 10 hours = 60 hrs @ 17% productivity loss = 50 hrs productive

6 days and 12 hours = 72 hrs @ 25% productivity loss = 54 hrs productive

7 days and 8 hours = 56 hrs @ 7% productivity loss = 52 hrs productive

7 days and 10 hours = 70 hrs @ 20% productivity loss = 56 hrs productive

7 days and 12 hours = 84 hrs @ 28% productivity loss = 60.5 hrs productive

Not only does overtime produce lost hours, but the cost of the overtime hours increases. Hours over 8 might cost 1.5x normal rate. Days over 5 might cost 2x normal rate. Increasing days and hours rapidly balloons the cost of completing the work. However, if absolutely necessary to meet unusual schedule demands, the cost vs time to complete work can be modeled for each scenario and the least destructive option (whether that be cost constrained or time constrained) can be agreed upon by all parties. The best choice is always that which requires the minimum added cost to achieve the restricted schedule.

See this blog post for an example Construction Overtime – A Common Miscalculation