Home » Posts tagged 'nonresidential' (Page 4)

Tag Archives: nonresidential

Construction Spending 2016 – Midyear Summary

Summary 2016 Construction Spending

9-7-16

Total Construction Spending for July reached a seasonally adjusted annual rate (SAAR) of $1.15 trillion, level with June which was revised upwards by $20 billion or nearly +1.8%. Monthly spending always gets revised in subsequent months. This year every month but May, which remained nearly unchanged, has been revised upwards, by an average of +1.4% and as much as 3.4%. Monthly values are subject to revision for two months after the first release and once again in May of the following year.

This plot, Construction Spending vs New Starts Cash Flows, shows actual spending (SAAR) by sector through July 2016 and projected trends of spending out to July 2017.

Previously I wrote that we should expect a short duration downturn in spending occurring between January and March. The expected monthly spending cash flows that would be generated from uneven new starts over the last two years indicated that a slowdown in spending would occur during the first quarter 2016. As it turns out, first quarter spending was much stronger than expected, averaging $1.17 trillion SAAR, primarily due to outstanding results in February and March for residential spending. But then April and May experienced significant declines, dropping to an average of only $1.14 trillion SAAR, down almost 3% from Q1. Now with June and July spending both up 1% from the April and May lows, it looks like we may be past that short duration downturn.

Total Construction Spending year-to-date (YTD) through July is up 5.6% over the same seven months 2015. Spending slowed in April and May from a 1st quarter average of $1.17 trillion that reached close to a 10 year high and falls just 4% short of the all-time high. However, it must be noted, that compares unadjusted current dollars, values of all dollars current in the year spent.

When comparing inflation adjusted constant dollars, all dollars adjusted to the same point in time, we can see 2016 spending is still 18% below the 2006 highs.

Total spending YTD through July is slightly ahead of what I predicted back in December, but it’s slightly below what I expected for May, June and July . I expect 2nd half spending to average above $1.2 trillion SAAR, but slightly lower than I originally forecast.

I’ve revised my 2016 spending forecast down slightly to total $1.190 trillion, up 7% from $1.112 trillion in 2015.

How does actual spending YTD compare to my prediction at the beginning of the year?

- Total predicted YTD through July $638.2b, actual YTD $647.7b (+$9.5bil, +1.5%).

- Residential predicted YTD $245.1b, actual YTD $259.2b (+$14.1bil, +5.8%).

- Nonresidential Bldgs predicted YTD $236.9b, actual YTD $228.1b (-$8.8bil, -3.7%).

- Non-building Infrastr predicted YTD $156.2b, actual YTD $160.5b (+$4.3bil, +2.8%).

Where are the revisions?

The single largest reduction in spending is in Nonresidential Buildings Manufacturing. Although there are other variances, that could account for the entire revision downward. Predicted construction starts for Manufacturing was lowered by nearly 35% after the initial start-of-year forecast was made.

Non-building Infrastructure spending increase is being supported by a 20%+ increase in power, which I didn’t expect. New starts for power projects have increased more than 20% since the initial forecast.

Residential construction had unusually large gains in February and March, almost all of that in residential renovations, offset only partially in April through July by declines mostly in new single-family housing.

Here’s my revised 2016 spending forecast based on YTD spending and new construction starts through July, compared to my prediction in December 2015.

- Total predicted Dec 2015 $1,206.2b, July 2016 $1,189.9b (-$16.3bil, -1.4%).

- Residential predicted Dec 2015 $473.8b, July 2016 $481.8b (+$8.0bil, +1.7%).

- Nonresdntl Bldgs predicted Dec 2015 $439.2b, July 2016 $410.9b (-$28.3bil, -6.4%).

- Non-bldg Infrastr predicted Dec 2015 $293.2b, July 2016 $297.3b (+$4.1bil, +1.4%).

Spending and construction starts are often confused by some analysts who refer to starts data as spending. Starts represent total project value recorded in the month the project begins. To determine spending activity, starts values must be spread out over the duration of the projects. Spending is dependent on cash flows each month generated from all previous construction starts. Cash flows expected based on Dodge Data construction starts are indicating a return to growth in spending in the 2nd half 2016. (See chart above Index Actual Construction Spending vs New Starts Cashflows).

Spending Breakout by Sector

Residential construction spending for July totaled a SAAR of $452 billion, remaining near level for the last four months. Residential spending YTD through July is up 6.5% over 2015. Spending slowed in April and May from a very strong 1st quarter average that reached close to a 10 year high. The current 3-month average is just 1% below the 1st quarter and is still at its highest since the 2nd half of 2007 but is 10% below the current dollar all-time high in 2006. I’m still expecting some upward revisions to June or July residential spending.

Residential spending just experienced the strongest three-year stretch of spending growth on record, up 60% in 2013-2014-2015. After taking out inflation, volume growth was only 31%, but that is still the strongest ever for three consecutive years. Spending growth in 2016 will reach only +9%. After adjusting for inflation that represents volume growth of less than +4%, the slowest in 5 years. New starts YTD (as reported by Dodge Data) although down from the 1st quarter, are still near post-recession highs. Starts from late 2015 and early 2016 will still be generating spending into early 2017. 2017 will repeat nearly identical to 2016. What we may be seeing is that it might be difficult to register another year of very high percentage growth in 2016 or 2017 because it is being measured against the 2015 10-year high. Another factor limiting very high growth may be a limited supply of labor to expand the workforce.

Total Nonresidential SAAR spending for July is $701 billion, down slightly from June, but monthly SAAR has varied only +/- 1% for the last six months. YTD spending compared to 2015 is up 5.1%. Nonresidential spending also slowed in April and May but is now up 1.5% from those lows. The current 3-month average is up slightly from the 1st quarter and is just 3% below the pre-recession 2008 current dollar high.

Nonresidential Buildings spending for July totaled a SAAR of $403 billion, down slightly from June but up 1.3% from the May dip. Spending YTD for nonresidential buildings through July is up 8.0% over 2015. The current 3-month average of $403 billion is up slightly from the 1st quarter but is still 9% below the peak in 2008.

Non-building Infrastructure spending for July fell to a SAAR of $289 billion, down only slightly over for the last four months. YTD spending through July is up only 1.3% over 2015. Spending began to slow in April and May and is now at the 2016 low. The current 3-month average is down 4% from the 1st quarter. However, spending on nonbuilding infrastructure reached an all-time high in the first half of 2014 and has remained near those highs through 2015 into the 1st quarter of 2016.

9-7-16

Public spending average for the 1st six months of 2016 is the highest since 2010 and is up 10% from the 2014 low point. YTD public spending is up 0.2% from 2015. All of Highway plus 80% of Educational makes up 55% of all public construction spending. The next largest markets, all of Sewage/Wastewater plus 70% of Transportation accounts for only 19% of public sending. All other markets combined make up less than 20%.

The biggest mover to total public spending this year is educational spending. Public educational spending is up only 4.0% YTD, but because it represents almost 25% of all public spending, it’s has a bigger net impact of +1.0% on moving the trend up than any other single public market. Public commercial spending is up 36.6% YTD but has only a 1% market share of public work. Highway and street is up 2.6% YTD. At 30% of total public that results in a net move of +0.8%. Office, public safety, power, sewage/waste disposal and water supply are all down YTD by a combined -5.3%. At a combined market share of 21% that nets a -1.1% reduction in YTD public spending.

Private spending is dominated by a 52% market share of residential work. At 6.6% growth that nets 3.4% growth in private spending. Several of the nonresidential building markets have high YTD growth (and/or a large market share of private work); lodging +30%, office +27%, Amusement +22%, commercial +10% and power +8%. These five markets combined represent 29% of private spending and combined are up +15% YTD for a net impact of +4.4% to private work.

For a base of reference, here’s a few points in spending history.

Total Construction Spending

- 8 years 1998-2005 up 77%

- 3 years 2003-2005 up 32%

- 3 years 2008-2010 down 30%

- 4 years 2012-2015 up 41%

Residential

- 8 years 1998-2005 up 133%

- 3 years 2003-2005 up 57%

- 3 years 2007-2009 down 60%

- 3 years 2013-2015 up 60%

Nonresidential Buildings

- 5 years 2004-2008 up 64%

- 3 years 2006-2008 up 45%

- 3 years 2009-2011 down 36%

- 2 years 2014-2015 up 25%

Non-building Infrastructure

- 7 years 1995-2001 up 56%

- 4 years 2005-2008 up 60%

- 3 years 2009-2011 down 8%

- 3 years 2012-2014 up 19%

See this post for expanded details on Construction Spending – Nonresidential Markets – Buildings and Infrastructure

See this post for expanded details on Construction Inflation

Construction Forecast 1st Look – What To Expect in 2016?

Construction spending may reach historic growth in 2016.

There are currently six estimates available forecasting 2016 total construction spending ranging from 6% to 10% growth, with an average of 8.7%. My forecast is 9.7%.

Total construction spending, forecast to grow 9.7% in 2016, could reach a total 30% for the three years 2014-15-16. The only comparable periods in the last 20 years are 29% in 2003-04-05 and 27% in 2013-14-15.

The current nonresidential buildings construction boom could become an historic expansion. Nonresidential buildings spending is forecast to grow 13.7% in 2016. Added to 8.8% in 2014 and 17.1% in 2015, the three-year total growth could reach 40% for 2014-15-16. The only comparable growth periods in the last 20 years are 40% in 2006-07-08 and 32% in 1995-96-97.

For perspective, residential spending increased 46% in 2013-14-15, similar to only one comparable period in the last 20 years, 48% in 2003-04-05.

Non-building infrastructure projects, in two of the last three years have barely shown any gains entirely due to declines in power plant projects. This will repeat in 2016.

This is still the 1st or 2nd most active 3 year period of growth in construction in more than 20 years, and it’s already been ongoing since 2013-2014. With the forecast for 2016, spending growth could reach a new three-year high.

From the middle of Q1 2016 to the end of Q3 2016, total spending will post six to eight months at an annual growth rate of 20%, but due to the dips at the beginning and the end of the year, total 2016 construction spending will finish at 9.7% growth. Construction spending momentum is not yet losing steam. We may be seeing the effects of a few years of erratic growth patterns and a shift from more rapidly changing commercial and residential work to slower growth institutional work.

Residential spending will slow several percent early in 2016 before resuming upward momentum to finish the year with 12% growth, slightly less than growth in 2014 and 2015. Periods of low new start volumes need to work their way thru the system and this produces growth patterns with periodic dips. The upward momentum will carry into 2017.

Nonresidential buildings spending will slow moderately in the next few months before we see a 15% growth rate through the middle of the year, only to see another slowdown late in 2016. Major contributions are increasing from institutional work in educational and healthcare markets. Office, commercial retail, lodging and manufacturing will decline considerably from 2015 but still provide support to growth.

Infrastructure projects spending will decline over the next six months due to the ending of massive projects that started 24 to 42 months ago. There will be large advances in spending midyear before we experience another slowdown later in 2016. Following a 0.5% increase in 2015, spending will increase only 1.2% in 2016, held down by a 10% drop in power projects, the second largest component of infrastructure work.

Construction added 1.0 million jobs in the five years 2011-2015. 800,000 jobs were added in the last three years. To support forecast spending, jobs need to grow by 500,000 to 600,000 in 2016-2017. Growth in nonresidential buildings and residential construction in 2014 and 2015 led to significant labor demand which has resulted in labor shortages in some building professions. Demand in 2016-2017 will drive up labor cost and may slow project delivery.

Spending growth, up 35% in the four-year period 2012-2015, exceeded the growth during 2003-2006 (33%) and 1996-1999 (32%) which were the two fastest growth periods on record with the highest rates of inflation and productivity loss. Construction spending growth for the period 2013-2016 is going to outpace all previous periods.

Construction inflation is quite likely to advance more rapidly than some owners have planned. Long term construction cost inflation is normally about double consumer price inflation. Construction inflation in rapid growth years is much higher than average long-term inflation. Since 1993, long-term annual construction inflation for buildings has been 3.5%, even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8%.

For the last three years the nonresidential buildings cost index has averaged just over +4% and the residential buildings cost index just over +6%, however, the infrastructure projects index declined. The FWHA highway index, the IHS power plant index and the PPI industrial structures and other nonresidential structures indices have all been flat or declining for the last three years. This provides a good example for why a composite all-construction cost index should not be used to adjust costs of buildings. Infrastructure project indices often do not follow the same pattern as cost of buildings.

Anticipate construction inflation of buildings during the next two years closer to the high end rapid growth rate rather than the long term average.

Welcome to the New Year. What’s Up With Construction?

It’s been about two weeks since I wrote a blog post. With good reason. I’ve spent the last few weeks working sometimes 10 or 12 hour days getting all the information for and writing a construction economics report. Coming soon!

Here’s a few tidbits out of the mass.

The nonresidential buildings construction boom that is going on right now could become an historic expansion. I’m predicting 13.7% growth in 2016. Added to 8.8% in 2014 and 17.1% in 2015 that could be 39.6% growth in 3 years 2014-15-16.

Only 3 year periods back to 1993 that are comparable: 2006-07-08 40.1% and 1995-96-97 32%.

Similarly,

Total construction spending growth for the 3 years 2014-15-16 could reach 30%. I forecast 9.7% growth in 2016.

Only 3 year periods back to 1993 that are comparable: 2003-04-05 29% and 1998-99-2000 25%.

Well, there is one more comparable. The last three years of total construction spending growth for 2013-14-15 was up 27%, so this expansion is already ranked 2nd.

What we see here is the 1st or 2nd most active 3 year period of growth in construction on record back to 1993, and it’s already been happening for two or three years.

For perspective, residential spending for 2013-14-15 grew 46%! Similar only to residential spending in 2003-04-05 at 48%.

Welcome to the new year. So let’s go see if we can break some records.

Construction Spending Nonres Bldgs on a Roll > What it Means for Inflation

This is clearly going to measure up as the breakout year for spending on nonresidential buildings. Growth year-to-date (YTD) is up 18.3%. We will finish the year with total growth up 17%. The last time we saw growth like this was 2007. In fact, 2007 is the only time % growth (and $ volume growth) was ever larger than this year.

Since last December I have been predicting a range from 14% to 20% growth in 2015 nonresidential buildings spending. It looks like we will finish the year right in the middle of that range.

By far the largest $ contribution comes from the growth in manufacturing buildings, up 50% and up $23bil YTD. Next closest is office buildings, up 22% and up $8.3bil YTD. Lodging, Commercial-Retail, Educational and Amusement-Recreation are each up approximately $4bil YTD, quite impressive for Lodging and Amusement-Rec since they both total only $17bil YTD.

Nonresidential buildings spending will maintain greater than 10% growth in 2016 something achieved only 5 times in 25 years. Next year, educational and healthcare buildings will both contribute strongly to the total annual growth. Manufacturing, Office and Lodging will all settle back but still maintain 10% or greater growth. Commercial-retail, which had 3 years of substantial growth from 2012 to 2014 adding nearly 50% spending growth during that time, will grow only 2-3% next year.

With last year, this year and next, nonresidential buildings spending will reach growth of 40% in three years, a growth rate exceeded only once in history, during the last construction boom from 2006 to 2008. Along with that boom in spending came the highest construction inflation ever recorded, an average inflation over 8% per year for 4 years. I expect we are headed there again.

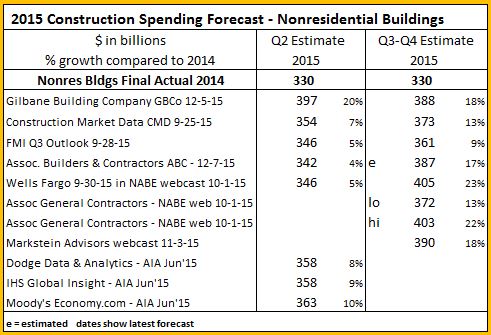

revised / updated table 12-9-15 to include ABC & BMarkstein forecasts.

Predictions – 2015 Spending for Nonresidential Construction Markets

Compiled in one neat table, here are 2015 predictions from eleven construction data firms for spending growth in nonresidential markets. Several firms provided mid-year estimates and recent estimates. Some provided only mid-year and some just recent estimates. Midyear estimates are separated so changes can be seen to current estimates.

Actual spending put-in-place for September year-to-date (YTD) became available November 2nd and new construction starts for October became available November 23rd.

There is a wide range of variance in predictions with the closest spreads at 9% and the widest spreads in lodging and manufacturing markets. It will be interesting to look back at this chart when the final numbers for 2015 become available in February 2016 to see how we did.

- One recent estimate published in Engineering News Record (ENR) magazine 11-16-15 lists 7% growth for manufacturing buildings. Each of the first nine months in 2015, the year over year growth has ranged between 40% and 60%, so the huge growth expected has been apparent for some time. Even if the last three months drop 15% below the current average we will still finish the year up 40%.

- For growth in educational buildings to fall to only 3%, the last three months would need to drop 15% below the current six month average, a change we will not very likely see.

- The spread on lodging is 18%, from the low estimate of 15% to high of 33%. YTD lodging through nine months is up 31% over last year. To finish at less than 25% growth in 2015, spending for the next three months would need to drop 20% from current levels.

We get a chance to tweak these numbers a little tighter when October spending gets released on December 1st.

Construction Spending Market Performance of Major Nonresidential Buildings 2015-2016

The Construction Spending BOOM in 2015 is being led by spending on nonresidential buildings. Spending on nonresidential buildings year-to-date (YTD) is +20%, +$41 billion. For housing the YTD is +11%, +$24 billion and for nonbuilding infrastructure projects YTD is -2.5%, -$5 billion.

Let’s take a look at the current growth trends to find out where they are headed.

In 2004-2006, residential spending was 55% of all construction spending. The annual growth in 2004 was 19% and in 2005 it was 15%. For the last 5 years residential spending has been only 32%-37% of total spending. In 2012 & 2013, residential led with annual spending gains of 13% and 19%. In 2014 & 2015, nonresidential buildings, also at 37% of total spending, led the gains at 9% and 19% growth. In 2016 the lead shifts back to residential with a projected growth of 14%. Infrastructure has not led growth since 2007 and 2008 when that sector had growth of 19% and 10%, at a time when residential spending was declining by 19% and 28%.

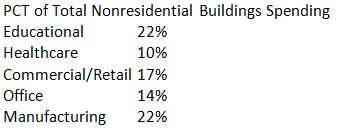

We can get a very good idea of nonresidential buildings spending and growth by looking at the five major markets. These five markets make up 85% of all nonresidential buildings construction spending and half of total 2015 construction spending growth.

See my blog post on October 11, 2015. I wrote:

“New nonresidential buildings construction starts cash flows indicate spending will continue to grow until Feb-Mar 2016, then drop consistently each month until Q3 2016. The decline is almost entirely due to big starts from Q3-Q4 2014 finishing and dropping out of the monthly spending numbers.”

More detail of how each market will perform, and why, follows.

Educational Construction Spending 2016

Spending in 2016 is projected to grow +5% over 2015. Other industry projections for educational spending in 2016 range from 1.5% to 12% growth over 2015, with the average of those seven estimates at 6%. As of August 2015, project starts that will generate 60% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were up 12% from the same 8 months of 2014. Educational spending increased only 4% year-to-date 2015 from the same period 2014, but the current annual rate of growth is 11%. Monthly spending is increasing and should continue to do so at least until mid-2016 before dropping off slightly into year end.

Healthcare Construction Spending 2016

Spending for healthcare is expected to remain flat with no growth in spending in 2016. Other industry projections for healthcare spending in 2016 range from 3% to 12% averaging 6% growth. As of August 2015, project starts already booked will generate 60% of all spending in 2016. New starts in 2016 generate about 25% of the total spending in 2016. If we get some very large new starts in the next few months, that could change total spending projections in 2016. Starts would need to increase 20% ( every month) over my projections for the next 16 months to reach 6% growth in spending next year.

Starts for the first 8 months of 2015 were down 4% from the same 8 months of 2014 and most recently have been declining. 2014 starts grew only 2% over 2013. Healthcare spending had an annual growth rate of 5% in the first eight months of 2015. The decline in new starts signals a projected decline in spending for the next 8 months. Spending growth resumes in mid-2016 but at a very low 3% annual rate and that from an already low rate of spending at the start of the year.

Commercial/Retail Construction Spending 2016

Spending in 2016 is projected to grow +7% over 2015. Other industry projections for office spending in 2016 range from 5.5% to 15% growth over 2015, with the average of those estimates at 10%. As of August 2015, project starts that will generate 55% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were up 17% from the same 8 months of 2014. Commercial spending increased 15% in the first half 2015 from the first half of 2014, but then spending declined by 8% in the last three months and may continue to decline for the next few months. Spending will resume a growth rate of 15% annual in the first 8 months of 2016. Commercial spending will peak in the second quarter 2016 before dropping again into year end.

Office Construction Spending 2016

Spending in 2016 is projected to grow +8% over 2015. Seven other industry projections for office spending in 2016 range from 7% to 18% growth over 2015, with the average of those seven estimates at 12%. As of August 2015, project starts that will generate 55% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were 23% lower than the first 8 months of 2014 Spending from 2014 starts will start to drop off in late 2015 and early 2016 and based on new starts in 2015, by mid-2016 the monthly rate of spending will start to decline, keeping totals for 2016 to less than 10% growth. Spending on office buildings in 2016 will peak in the 1st half year with the 2nd half coming in 10% lower.

Manufacturing Construction Spending 2016

Spending in 2016 is projected to grow +9% over 2015. Seven other industry projections for manufacturing buildings spending in 2016 range from 5% to 18% growth over 2015, with the average of those seven estimates at 11%. As of August 2015, project starts that will generate 70% of all spending in 2016 are already booked.

Starts for the first 8 months of 2015 were only 6% lower than the first 8 months of 2014. However, even if starts for the next 4 months increase each month by 50% they will still not equal the amount of starts in the last 4 months of 2014. Total starts for 2015 are projected to finish 20% lower than 2014. That’s probably a good thing since 2014 starts were up 87% from 2013, the highest annual growth ever recorded for any market sector.

Spending from 2014 starts will start to drop off in late 2015. Spending reached a peak this year in the 2nd quarter but is expected to drop for the next five to six months. Spending on manufacturing buildings in 2016 will again peak in the 2nd quarter and then drop off into the end of the year.

Nonresidential Buildings Construction Spending Through 2016

New nonresidential buildings construction starts cash flows indicate spending will continue to grow until Feb-Mar 2016, then drop consistently each month until Q3 2016. The decline is almost entirely due to big starts from Q3-Q4 2014 finishing and dropping out of the monthly spending numbers. New starts in 2015 did not grow as much as in the previous two years. Although the predicted decline in monthly spending over 6 months is 8%, 2016 may finish with a rate of monthly spending higher than when it started.

The drop and recovery can vary from the predicted shown here and it’s not likely to be so smooth, but new starts from here on forward would really have to skew from a normal growth pattern by a lot to change this pattern by a little. Nonresidential buildings on average take about 20 to 24 months to complete, so every month we move out adds about 4% to 5% uncertainty to future spending.

This prolonged period of spending declines is sure to cause alarm in the headlines in mid-2016, but the decline and the reversal are supported in large part by starts already booked. Unless something dramatic and unexpected comes along to throw a wrench in the works, I’m expecting a pattern like this for 2016.

Total nonresidential buildings spending in 2016 will finish the year about 10% higher than 2015.