Home » Behind the Headlines (Page 15)

Category Archives: Behind the Headlines

Behind The Headlines – Construction Backlog

1-16-17

tables updated 2-1-17

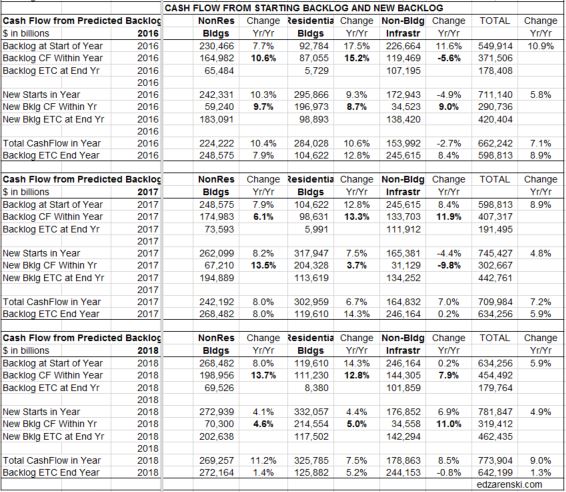

New Backlog is the total value of project revenues under contract that are about to start construction, or new starts. The entire value of a project is considered in backlog when the contract is signed. Projects booked in December 2016 or before are in backlog at the start of 2017. Simply referencing total backlog does not give a clear indication of spending within the next calendar year. Just because backlog is up going into a new year does not necessarily mean revenues will be up that year. You must understand some very important distinctions about backlog to determine how much revenue will occur within the next year.

Projects, from start to completion, can have significantly different duration. Whereas a residential home may have a duration of 8 or 9 months, an office building could have a duration of 18 to 24 months and a billion dollar infrastructure project could have a duration of 3 to 4 years.

Backlog at the start of 2017 could include revenues from projects that started last month or as long as several years ago. For a project that has a duration of several years, the amount in starting backlog at the beginning of 2017 is not the total backlog amount recorded for the project at its start date, but is the amount remaining to complete the project or the estimate to complete (ETC).

The only way to know how much of total backlog that will get spent in the current year and following years is to prepare an estimated cash flow from start to finish for all the projects that have started in backlog. Then add up the amounts from all projects in each month to find the cumulative cash flow in that month, or in that year.

Construction Starts provide the values entering backlog each month. Except for residential, new project starts within the year contribute a much smaller percentage to total spending in the first year than all the backlog ETC on the books at the start of the year. New residential projects contribute the most to spending within the year started because generally residential projects have the shortest duration. Residential projects started in the first quarter may reach completion before the year is over. New infrastructure projects generally have the longest duration and may contribute some share of project value to backlog spread over the next several years.

The distinction between backlog, backlog ETC and cumulative cash flow is necessary to predict spending. For example:

We start the year with $100 billion of residential projects in backlog and $100 billion of infrastructure projects in backlog. All of the residential projects could have durations of 12 months or less. Therefore residential spending could total $100 billion within the year. However, the infrastructure projects could have durations of 2 years, 3 years or 4 years. Spending from infrastructure backlog this year might total only $50 billion with $30 billion in spending occurring next year and $20 billion the following year. Although both sectors start the year with the same total amount in backlog, we can see the amount spent within the year is determined by the duration of the projects and the cash flow schedule.

Backlog totals may not be a good indicator of total revenue spending within the year. In fact, backlog could be up and total revenues for the year could end up lower than the previous year. Unless you have a clear picture of the types and duration of projects that make up the backlog, you will not have a clear picture of spending activity in the coming year.

See Also Construction Backlog 2017 3-21-2017

Are We at New Peak Construction Spending?

1-4-17

Total construction spending peaked in Q1 2006 at an annual rate of $1,222 billion. For the most recent three months it has averaged $1,172 billion. It is currently at a 10 1/2 year high at just 4% below peak spending. But that ignores inflation.

In constant inflation adjusted dollars spending is still 18% below the Q1 2006 peak.

Current headlines express exuberance that we are now at a 10 1/2 year high in construction spending but fail to address the fact that is comparing dollars that are not adjusted for inflation.

In the 1st quarter of 2006 total spending peaked at a annual rate of $1.2 billion and for the year 2006 spending totaled $1,167 billion. We are within a stone’s throw of reaching that monthly level and 2016 will reach a new all-time high total spending by a slim fraction. But all of that is measured in current dollars, dollars at the value of worth within that year, ignoring inflation.

Adjusting for inflation gives us a much different value. Inflation adjusted dollars are referred to as constant dollars or dollars all compared or measured in value in terms of the year to which we choose to compare. To be fair, we must now compare all backdated years of construction to constant dollars in 2016. What would those previous years be worth if they were valued in 2016 dollars?

By mid-2017 total construction spending will reach a new all-time high, but in constant inflation adjusted dollars will still be 17% below 2006 peak. We will not reach a new inflation adjusted high before 2020.

Residential construction spending is still 32% below the 2006 peak of $690 billion. In constant inflation adjusted dollars it is 39% below 2006 peak.

Nonresidential Buildings construction spending is only 3.5% below 2008 peak of $443 billion. However, in constant inflation adjusted dollars it is 18% below 2008 peak.

Non-building Infrastructure construction spending pre-recession peaked in 2008 at at an annual rate of $290 billion. However, post recession it peaked in Q1 2014 at $314 billion. It is now 8% below the 2014 peak. In constant inflation adjusted dollars it is 12% below the 2014 peak.

For more on inflation SEE Construction Cost Inflation – Midyear Report 2016

Saturday Morning Thinking Out Loud #6

Just a few thoughts on forecasting construction spending

If we look at actual data through September, with ~75% of the actual annual construction spending already in the year-to-date and only 25% of annual spending in the estimate to complete in the 4th quarter, if forecasts for year-end totals are not already within 2.5% of the final, that means the projections for the final quarter are off by more than 10%.

Cash flows from construction starts are the strongest predictor of total spending next month. Projects that already started are in backlog. Backlog is used to develop projections for spending. For next month we already have 96% of all work in backlog. The remaining 4% will be new starts next month. For two months out we have 92% and for three months out we have 88% already in backlog. So, the uncertainty on spending in the near term is pretty low. Even averaged over a quarter rather than being exact every month, it takes a major event to have a big miss on projections for the next quarter.

Although exact monthly values in spending may be difficult to predict, trends for monthly changes in spending are easier to predict. Often these trends have very small changes month to month. Monthly changes in spending of +/- 5% are uncommon and changes of +/- 10% are quite rare.

Some forecasts I’ve seen for construction spending would demand that month to month changes in the final quarter exceed 20% to 30%. It’s just not going to happen folks.

Saturday Morning Thinking Outloud #5 – Jobs Growth

For all of 2014-2015-2016

- Total Construction jobs increased from 5,950,000 to 6,700,000, +12.6%

- Total Construction spending increased from $960bil to $1,170bil, +22%

BUT, much of that spending increase is inflation. We need to compare to constant dollars which = Volume. Inflation was particularly high in residential work, over 15% for the 3 years, which means $1.00bil in spending 3 years ago would be worth more than $1.15bil today. Converting everything to constant Oct 2016 dollars, after inflation we get:

- Total Construction volume increased from $1,070bil to $1,170bil, +9.4%

So, for the 3 years, jobs increased by 12.6% while real work volume increased by 9.4%.

A more thorough analysis, which takes hours worked into consideration, shows from the Jan 2011 bottom of the recession in construction to current, both jobs and volume have increased equally by 28%. But jobs growth is often out-of-balance with real volume growth. In the beginning of the recession years of 2008-2011 firms let go of people much faster than work volume declined. 2009 showed a big gain in productivity. By 2010-2011 firms hadn’t let go enough to match the loss in spending. Then from 2012-2014 workload grew faster than firms filled jobs. Since 2011 we are sort of on an even keel.

For the last 3 years, jobs increased more than real construction volume. I pointed this out in my last detailed jobs report. The 6 months from Oct 2015 – March 2016 encompassed the fastest new construction jobs growth period in a decade. It’s no surprise to me that jobs growth has been slow since March this year. Frankly, I wouldn’t be the least bit surprised if it remains slow for awhile. When we look at jobs growth vs. volume growth, there is reason to believe that slow jobs growth is not entirely due to labor shortages. Part of the blame is due to recent over-hiring.

Behind The Headlines – Construction Data

12-2-16

Just a few important facts here (that you won’t read in the headlines).

- Jobs have increased by 23% since the recession bottom January 2011. Construction spending has increased 52% in same period.

- Adjusting jobs for hours worked and spending for inflation, both work output and constant volume construction grew at 28% since recession bottom.

- Residential construction jobs are down 22% from the 2006 peak. In constant $ after inflation, real residential volume of work is down 39%.

- Nonresidential buildings construction jobs are down 8% from the 2008 peak. In constant $ after inflation, real nonres bldgs volume of work is down 17%.

- Construction spending average for the last 3 months is at a 10 year high. Construction volume in constant $ after inflation is still 18% below 10 years ago.

- Census construction data is ALWAYS revised in the following two months after initial release. Census updates all the values for the previous year, usually with the May data release (on July 1) the following year.

- In 2016, 7 times the first release of spending showed a decline vs the previous month. After revisions, the values show no declines vs the previous month.

- In the last 36 months, there were 16 spending releases that originally showed a decline vs the previous month. After revisions there were no mo/mo declines.

- It’s hard to add $100 billion in new construction spending in one year. Since 1993 it’s happened only 3 times; 2004, 2005 and 2015.

- It’s real damn hard to add $100 billion in new construction volume in a year. After adjusting for inflation, construction volume has never increased by $100 billion. It has increased by $75 billion 4 times and 3 more times by $50 billion.

- It takes about 6,000 jobs to put-in-place $1 billion of construction in a year. $100 billion in new work would require 600,000 new jobs in a year. The largest construction jobs growth ever recorded is about 700,000 jobs in 2 years.

- Now think of #9, #10 and #11 in terms of ONLY the Infrastructure sector. Infrastructure, about 25% of total construction spending, added spending more than $25 billion in a single year only once. The average annual growth for the past 20 years is less than $10 billion/year. The average growth in jobs (excluding all recessionary years because they would make the result approach zero) is about 25,000/year.

- The Aug-Sep-Oct 3mo average of construction starts for Nonresidential Bldgs (by Dodge Data) is the best 3mo since Q1 2008. Q1 2008 was the PEAK of the nonresidential buildings construction boom.

- More infrastucture projects started construction in the 1st 6mo of 2015 than any time in history. This will boost infrastructure spending through 2017. Infrastructure spending is low in 2016 due to a low volume of starts in 2014.

Saturday Morning Thinking Outloud #4 -YTD

11/26/16

In 2015, nonresidential buildings starts were very high in the beginning of the year and dropped off in the later part of the year. In 2016 it’s just the opposite. This skews year-to-date total comparisons and for most of this year makes it appear as if there may be no growth in new starts.

Here’s a simple example:

Let’s say 4 months in 2016 had starts of $6, 8, 10 and 12 billion and the same months in 2015 had starts of $10, 9, 8 and 7 billion. The year-to-date change for 2016 vs 2015 after the 1st month (6 vs 10) is down 40%. After two months it’s 14 vs 19 (6+8 vs 10+9), down 26%. In the 3rd month 2016 has better performance than 2015 (10 vs 8), but the year-to-date (24 vs 27), down 11%, is still strongly influenced by the earlier months. But in the 4th month we get 36 vs 34 and finally the year-to-date shows 2016 growth of 6% over 2015. That is the current scenario.

Construction Starts for nonresidential buildings for the 1st 4 months in the 2nd half of 2016 (Jul-Oct) are 30% higher than the average of the 1st half 2016 and almost 40% higher than the same 4 months in 2015, and yet the year-to-date % change 2016 vs 2015 is ZERO.

To keep from being misdirected, year-to-date comparisons require knowing not only the direction of the current year trend but also the direction of the previous year trend.

The most recent 3 month (Aug-Sep-Oct) average of nonresidential buildings construction starts by Dodge Data represent the best 3 months since Q1 2008. Although year-to-date performance of zero growth would seem to indicate a slow down, starts are doing just fine. I’m forecasting the final two months of the year to be up 40% from 2015.

But wait, there’s more!

Every year, starts from the previous year are adjusted, always higher. 2016 starts won’t be adjusted up until 2017. But that means all current 2016 (un-adjusted) starts are being compared to 2015 that has already been adjusted up. This causes the year-to-date comparison to be always understated. The average adjustment to nonresidential building starts for the last few years has been about +5%. If that trend remains consistent then next year we should see that 2016 starts were approximately 5% higher than first posted and growth was really much better than current values would seem to indicate.

With 10 months of data in hand, year-to-date starts for nonresidential buildings show no change from 2015. However starts are doing very well and I’m predicting the 2016 volume of starts will lead to 8% growth in spending in 2017.

Saturday Morning Thinking Outloud #2 – Headlines

11-5-16

I publish a lot of analysis for various construction data. I also read many other articles posted by other pundits in the industry, including MSM news sources. What I would say regarding construction data is this; an informed knowledge of construction data and how it’s used helps you understand if some article you are reading is accurate or relevant.

What I try to do here is not only report on the latest significant construction data, but also explain how the data must be used to make accurate and valuable analysis.

Here’s just three examples of how news analysts get it wrong:

> Post new construction starts as if those numbers represent construction spending.

A new start this month worth $10 billion adds a huge amount to the starts this month and will most certainly drive up the mo/mo and yr/yr starts numbers. But that new project could take 24 or 36 or 48 months to complete, so we can’t discern the impact on spending until we cash flow the value of the project which gives us the spending over its complete life span. In any given month the total amount of all spending is the summation of the spending this month from all the projects still ongoing that have started in previous months. Spending next month is 95% dependent on the flow of projects that started over the last 24 or 36 months.

> Suggest that two to three months of declines in spending indicates a downturn.

One of the biggest factors that determines spending this month is the values contributed this month from all the previous starts not yet completed. In a sector such as nonresidential buildings, in which the average duration of a project might be 24 months, the amount of spending this month gets some contribution from projects that started in each of the previous 24 months. One of the greatest influences on spending in any given month is the fluctuation (which could have occurred many months ago) in the amount of starts. So sometimes when we see a monthly spending dip it has nothing to do with a current declining trend in overall spending, but might have more to do with erratic new starts up to 18-24 months ago.

Starts can be quite erratic. Although we might see annual starts climbing at a modest rate of 6% or 7% per year, within that year we might see starts increase or decline by 50% or 100% from month to month. This is normal. But what it does to spending, particularly when a very large volume of project spending (from some month in the past that had huge new starts) finishes and drops out of the current spending, it causes dramatic fluctuations from month to month. Much of what we see in month to month changes in spending was predetermined months ago by the pattern of starts.

Normal rates of new starts, if always constant in growth rate, would create a constant rate of growth in spending. Erratic rates of change in starts create erratic changes in spending when those projects come to an end.

> Compare current $ this year to any $ from years past, without taking inflation into consideration.

I recently read an article that claimed construction was back to pre-recession levels. What really was being identified in that article was that current 2016$ were back to the level of current 2006$. That’s like saying $100 today buys you the same products that $100 bought you in 2006. I bet it wouldn’t be too hard to find a few examples where that would not be true.

Comparisons of dollars over time almost always need to be made using constant dollars, that is, adjusted for inflation and all converted to the same point in time, usually today. Sure spending today is up more than 50% off the bottom and in current dollars is higher than the previous peak in 2006. But if we adjusted those 2006$ for inflation the dollars spent in 2006 would be worth much more today. Although current dollars are now higher than any time in the past, after adjusting for inflation we are still 18% below peak spending.

Saturday Morning Thinking Outloud #1 – Infrastructure

10-29-16

Can the construction industry even accommodate adding $1 trillion of new infrastructure spending over 10 years?

It takes about 5000-6000 new jobs to support $1 billion of new construction work for a year. For infrastructure the number is lower. So $100 billion per year continuous for next 10 years would support about 400,000 new jobs for 10 years. Well, that’s not how it will happen, so let’s look a little closer.

- Historically the fastest rate of growth in spending takes about 3 years to increase 50%. That is for selected markets, never for the entire industry.

- Infrastructure spending grew 50% in 4 years from 2004 to 2008, when that sector was half the size what it is today.

- Infrastructure, about 25% of total construction spending, added spending more than $25 billion in a single year only once. The average annual growth for the past 20 years is less than $10 billion/year.

- Historical growth in jobs rarely exceeds 300,000 new jobs per year. It has never averaged that rate of growth for more than a 3 year stretch. That is for the entire industry.

- Spending after inflation (real volume growth) for all construction increased an average of $50 billion per year for the last 4 years. The same is expected in 2017.

- Jobs increased an average of 250,000 per year for the last 4 years.

- We could expect approximately the same growth in volume and jobs in 2018.

So here’s what we know. The entire construction industry has been growing on average at about $50 billion in volume and 250,000 jobs every year in recent data. Even with the addition of a new influx of infrastructure work, most of that other growth is not going to go away. But how much growth can the entire industry accommodate without bursting at the seams. Let’s make some broad assumptions to see what happens.

Let’s assume for the next 10 years the normal rate of new construction growth gets cut in half. In reality it probably wouldn’t, but we need to push some numbers to extremes to see what happens. So normal new volume, not including any boost from new federal infrastructure spending, might only grow at $25 billion per year and that would absorb 100,000-125,000 new jobs per year. That accounts for HALF of the entire industry volume growth and jobs growth. How much room does that leave for new growth or expansion in industry growth rates?

If we fill the difference with work from added new infrastructure spending, we can add $25 billion per year in new infrastructure spending and that will add about 100,000 new jobs per year. To account for how the work might be contracted out, let’s just assume in the first year we commit to $250 billion in contracts that are spread over 10 years to get to $25 billion a year in spending. In the 2nd, 3rd and 4th years we could also commit each time to another $250 billion in 10 year contracts that spread the spending out to $25 billion per year for 10 years.

By year 4, we’ve added $100 billion per year in new spending that will stretch out for the next 6 to 10 years ( note: this pushes spending $1 trillion out to 13 years). This spread of money over time, or cash flow, results in increased spending in the government infrastructure markets by 50% in 4 years, matching the best ever industry growth rates. We’ve increased jobs by 100,000 per year for 4 years to a total of 400,000 new jobs and they will all have funds to continue work for the next 6 to 10 years. All that just due to added infrastructure spending.

But let’s not forget the rest of the industry. This would push total spending growth and total industry jobs growth to the highest rates of growth on record. So this is a scenario that is unlikely to be achieved, and it’s not very likely that growth like that could be sustained for very long. It’s also not likely the rest of all the new growth in the industry is going to get cut in half to leave room for new added infrastructure work. So, it’s possible total growth over the next 4 years would be less than anticipated here. This allows for no downturn at any time in the next 10 years.

It begins to seem like it might be pretty difficult to add $1 trillion in spending to the infrastructure construction sector, which is only 1/4 of the entire industry, to be spent in the next 10 years.

When sometimes we push numbers to extremes just to see what happens, we get an unexpected picture of what might, or might not, be possible.

Construction Jobs – Behind The Headlines

10/13/16

Headline comparisons we read are often what happened this month versus last month or year-to-date versus last year. For comparisons to construction spending and jobs it is perhaps beneficial to look at recent and longer term trends. Here I will discuss construction jobs growth versus spending growth and highlight some of the pitfalls when comparing these values for productivity.

The most talked about reason for slower jobs growth is the lack of experienced workers available to hire. In fact, recent surveys indicate about 70% of construction firms report difficulty finding experienced workers to fill vacant positions. That certainly cannot be overlooked as one reason for slower jobs growth, but that is not the only reason?

Even with all this talk of difficulty finding experienced construction workers, there has been very good jobs growth. For the 5 ½ year period from the bottom in January 2011 to the present (August 2016) we added 1,240,000 construction jobs.

- Jobs increased by 23% in 5 ½ years with peak growth in 2014 and 2015.

- For the two years 2014+2015 we added 650,000 jobs, the largest number of new jobs in two years since 2004+2005.

In 2014-2015, jobs expanded by 11%, the highest number of jobs in a two-year span since 2004-2005 and the fastest two-year percent growth since 1998-1999. Peak growth was 6.1% in 2014 with slower growth in 2015. I expect even slower growth in 2016.

- For the 6-month period including Oct’15 thru Mar’16 construction gained 214,000 jobs, the fastest rate of consecutive months jobs growth in 10 years. Then, after 3 months of losses, July shows a modest gain.

Jobs growth from October 2015 through March 2016 was exceptional, 214,000 construction jobs added in 6 months, topping off the fastest 2 years of jobs growth in 10 years. That is the highest 6-month average growth rate in 10 years. That certainly doesn’t make it seem like there is a labor shortage. However, it is important to note, the jobs opening rate (JOLTS) is the highest it’s been in many years and that is a signal of difficulty in filling open positions.

I would expect growth like that to be followed by a slowdown in hiring as firms try to reach a jobs/workload balance, after such a robust period of jobs growth. It appears we may have experienced that slowdown. Jobs have been down four of the last six months and up most recently.

- Q2’16 jobs declined all 3 months. Keep in mind, this immediately follows the fastest rate of jobs growth in 10 years. But it also tracks directly to three monthly declines in spending. (I predicted this jobs slowdown in my data 9 months ago. I predicted the 1st half 2016 spending decline more than a year ago).

It is not so unusual to see jobs growth slowed in the 2nd quarter. It follows directly with the Q2 trend in spending and it follows what might be considered a saturation period in jobs growth. The last two years of jobs growth was the best two-year period in 10 years. It might also be indicating that after a robust 6 month hiring period there are far fewer skilled workers still available for hire. The unemployed available for hire is the lowest in 16 years.

Construction spending hit bottom at the same time as jobs, the 1st quarter 2011. For the same 5 ½ year period, Jan 2011 to Aug 2016, construction spending increased 52%, far more than jobs growth. For 2014+2015, spending increased close to 11% per year, the fastest spending growth in more than 10 years.

- For the same 6-months, Oct’15 thru Mar’16, Q4’15 spending was flat but by the end of Q1’16 spending had increased more than 4% in 6 months, to an annual rate of +8%.

- 2nd quarter 2016 spending came in 2% below 1st quarter.

- Total 1st half spending finished 7.2% above the 1st half 2015.

Although spending slowed in the 2nd quarter this year, in part it’s because the 1st quarter was so strong. They combined for a strong 1st half up 7.2% over last year.

Why is it that jobs don’t increase at the same rate as construction spending? Because much of that spending growth is just inflation, not true volume growth. Volume is construction spending minus inflation. To get volume we need to convert all dollars from current $ in the year spent into constant $ by factoring out inflation.

- Jobs growth should not be compared to spending growth.

- Spending increased 52% from Jan/Feb 2011 to Jul/Aug 2016.

- After adjusting for inflation from Q1 2011 to Q3 2016, we find that construction volume increased by 28% in 5 ½ years.

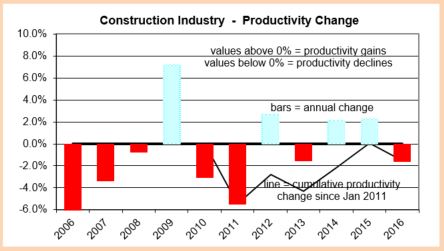

So, it looks like volume (+28%) still increased much more than jobs (+23%) in the same period and this would indicate increasing productivity. But this still is not the whole picture. Jobs need to be adjusted.

- Jobs needs to take into consideration the hours worked.

Before the dramatic decline in jobs from 2007 through 2010, hours worked ranged between 37hrs/wk and 38hrs/wk. But by 2015, and into 2016, hours worked has been consistently over 39hrs/wk. So not only did the workforce grow by 1.24 million jobs (+23%), but also the entire 7.0 million work force is working about 4% more hours/week. This must be considered to get net jobs, or work output.

- After adjusting for hours worked from Q1 2011 to Q3 2016, we find that net jobs growth increased by 28% in 5 ½ years.

- Since Q1 2011 the constant $ value of construction spending increased by 28%.

- Since Q1 2011 Jobs/hours worked output also increased by 28%.

Since Jan 2011, volume increased 28% and workforce output increased 28%, for a net productivity balance, but in 2011 we had a significant productivity loss and a smaller loss in 2013. The huge 2011 productivity loss is probably in part explained by the resumption of hiring after historic job cuts, particularly in 2009 when the work force was cut 16% but, while spending declined by 16%, work volume declined only 11%, which may have overshot the balance mark. That helps account for the huge productivity gain in 2009, but also leads to the losses in 2010 and 2011.

From Jan 2014 to Dec 2015 volume increased by 15% and workforce output increased by only 10.5%. Total hours worked compared to total constant value of spending shows productivity increased for those two years. Historically, we should not expect to see productivity growth continue for a third year and as of August it is down year-to-date.

I expected to see a turn-around in jobs growth in the 2nd half of 2016, and so far, for the 3-month period July-Sept we’ve added 34,000 jobs. That’s starting out perhaps a little slower than I thought. For much of 2014 and 2015 volume growth was exceeding jobs growth, but for 10 months from August 2015 through May 2016, volume growth mostly stalled and jobs growth, which just had 6 months of record high growth, exceeded volume growth by 3%. Only in the last few months has volume growth begun to outpace jobs growth again. But I suspect it is this slow down in real volume growth that has led to slow jobs growth. This leads me to think if spending plays out as expected into year end 2016, then construction jobs may begin to grow faster in late 2016. However, availability could have a significant impact on this needed growth.

Availability already seems to be having an effect on wages. Construction wages are up 2.6% year/year, but are up 1.2% in the last quarter, so the rate of wage growth has recently accelerated. The most recent JOLTS report shows we’ve been near and now above 200,000 job openings for months. With this latest jobs report, that could indicate labor cost will continue to rise rapidly.

As wages accelerate, also important is work scheduling capacity which is affected by the number of workers on hand to get the job done. Inability to secure sufficient workforce could impact project duration and cost and adds to risk, all inflationary. That could potentially impose a limit on spending growth. It will definitely have an upward effect on construction inflation this year.

For all of 2016 and 2017, I predict construction spending will increase about 15%, BUT after inflation construction volume will increase only about 6% to 7%, most of that in 2017. For all of 2016 and 2017, I predict jobs will grow by 350,000 to 450,000, only about 5% to 6%.

Reference Source Information:

U.S. Census released August Construction Spending 10-3-16

BLS released the September jobs Report 10-7-16

Reference Posts:

Construction Jobs Show 3rd Qtr Growth

Construction Jobs – Is July a Turning Point?

BLS Says +790,000 Construction Jobs by 2024. Let’s Look Behind The Headlines.

In a report released December 8, 2015 the Bureau of Labor Statistics (BLS) predicts jobs growth for industries. Construction is pegged as a leader with expected 790,000 new jobs from 2014 to 2024. Robert Deitz at NAHB provides a good summary of the BLS report.

Let me provide a few historical averages and break this down so we can see how it stacks up.

The prediction period is from 2014 through 2024, so all of 2014 is already in the BLS baseline. The average number of construction jobs in 2014 was 6,138,000 and BLS uses that baseline. BLS says 2024 will average 6,928,000 construction jobs, growth of 790,000 jobs over 10 years, from which we can infer 12.9% growth in 10 years or a 1.22% compounded growth rate.

In 2015 we’ve already gained 215,000 ytd through November. The average jobs for 2015 is currently 6,390,000, so that leaves 540,000 expected over the remaining 9 years. That would imply a growth rate of 8.5% in 9 years or an average compounded growth rate of only 0.9% per year.

Now here is where it gets interesting.

Spending growth is predicted by several firms between 5% and 10% per year for the next 4 years. My own forecast has 2016 growth at 11%. Average of forecasts for the period 2016-2019 are currently 8%, 7.5%, 6% and 7%.We need to take out inflation to get real volume growth, so we will assume 4% inflation per year for the next 4 years. Long term construction inflation is 3.5% per year, but in rapid growth years it has reached 6%-8% per year. For the period 2013-2015 construction inflation averaged 4%. Adjusting for inflation at 4% results in volume growth for 2016-2019 at 4%, 3.5%, 2% and 3%. This is much faster growth than the BLS average, so we will remain more conservative in this analysis.

Historical volume growth over the last 22 years is grossly distorted by the recession. Volume declined in 8 of those 22 years. In the three worst three years of the recession, 2008, 2009 and 2010, volume declined by 28%. When we take out those three years the typical growth period averages are more apparent. The historical average volume growth in construction with recession data removed and after adjusting for inflation is 2% per year for 19 years.

Jobs growth over the last 20 years averaged 1.6% per year, even when we include the catastrophic losses during the recession years of 2007 through 2010. The BLS is predicting 1.22% growth for 10 years, lower than the average with a recession. Without the four worst recession years of job losses the average growth jumps to 3.7% per year, almost triple the BLS predicted growth. Minus the recession years, there has never been a prolonged period where jobs growth has averaged growth less than 2% per year, so we shouldn’t expect such low growth.

BLS assumes productivity will increase 1% per year. This would lower the number of jobs needed. Construction productivity has never done this before. My records show over the last 20 years there has not even been two consecutive years of construction productivity increases. Long term productivity in the construction industry has declined by 1% per year. Data would indicate jobs growth must be greater than volume growth to make up for productivity losses.

We have differences based on my analysis of historical growth and productivity. Forecasts show expectations of rapid growth in the next few years. These differences would produce dramatically different estimates of jobs growth in coming years. How much different? Let’s see.

Let’s be conservative with assumptions. Based on:

- No productivity increases or losses. Therefore jobs will grow at the same rate as volume.

- Volume growth of 1.5% per year will be less than forecast and less than the historical non-recession average. This allows for some years to decline.

- There will be no recession, but there will be down years.

- Starting from 2015 baseline of 6,390,000 jobs

Jobs need to grow at 1.5% per year compounded for 9 years. That’s 14.3% in 9 years from the 2015 baseline of 6,390,000. Growing 14% in nine years adds 895,000 jobs by 2024. We’ve already gained 215,000 jobs in 2015. For the period of the BLS analysis, my conservative prediction is a total gain of 1,110,000 jobs over 10 years, 320,000 more than the BLS prediction.

Jobs reached a peak in 2006-2007 at 7,700,000. At conservative growth rates we will not reach the previous peak by 2024. However, if construction volume and jobs growth follow a little more closely to historical 20 year patterns, we will add 1,300,000 jobs from 2014 to 2024, but still be short of the previous peak. This scenario adds 500,000 to the BLS prediction.

If volume growth does reach forecast levels and if jobs growth does include some losses in productivity then my estimate for jobs is double BLS and we could reach the previous peak in jobs several years earlier.