See Also this update Construction Forecast Update 10-16-20

SEE ALSO Pandemic #14 – Impact on Construction Inflation

Midyear Construction Outlook 8-14-20 based on

- Actual Spending data includes revisions 2018-2019 issued 7-1-20

- Actual Jobs data includes BLS Jobs to July (12th) issued 8-7-20

- Forecast includes US Census June 2020 year-to-date spending 8-3-20

- Forecast includes Dodge construction starts Midyear Update 8-6-20

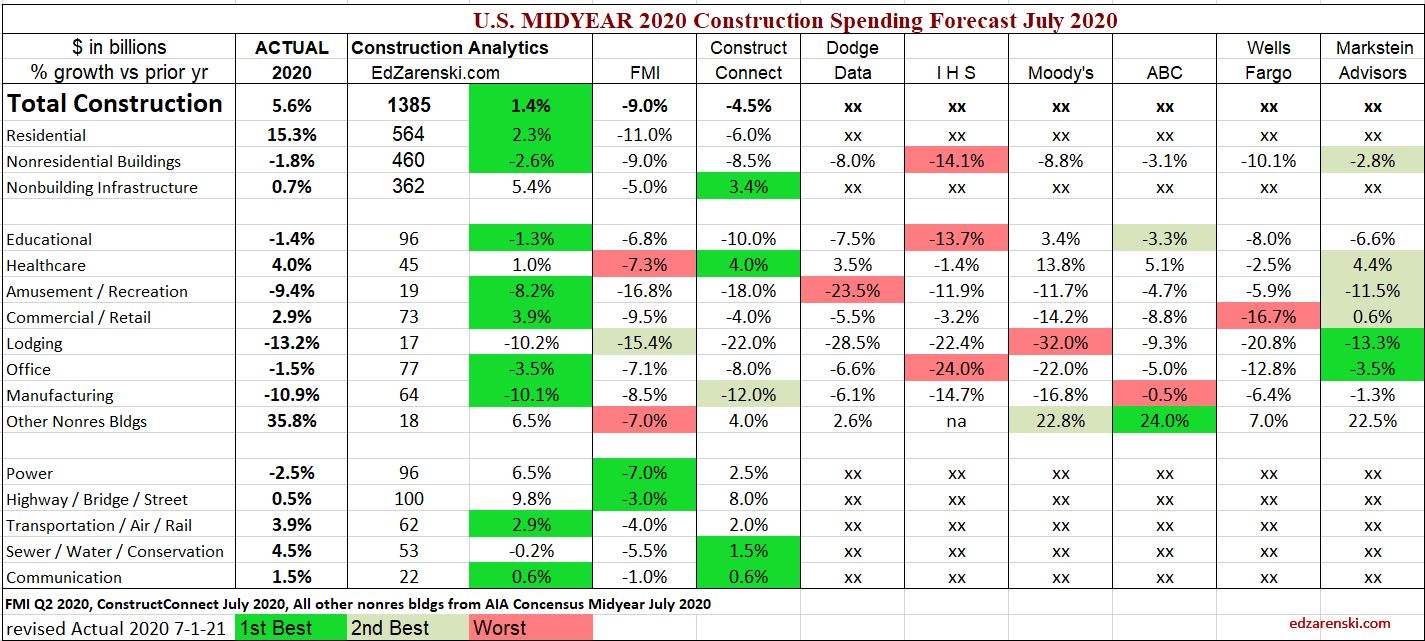

The first important thing to note is that the US Census, on 7-1-20, revised all spending data back several years. This is an annual occurrence. This analysis includes all revised data, which adds about $30 billion to 2018, $60 billion to 2019, half of all adding to residential, and revises 2020 data. Not everyone has yet updated to this recently revised data, so you may see differences when comparing forecast reports among several firms. If needed, refer to the percent.

Initial impact on spending from project delays/shutdowns

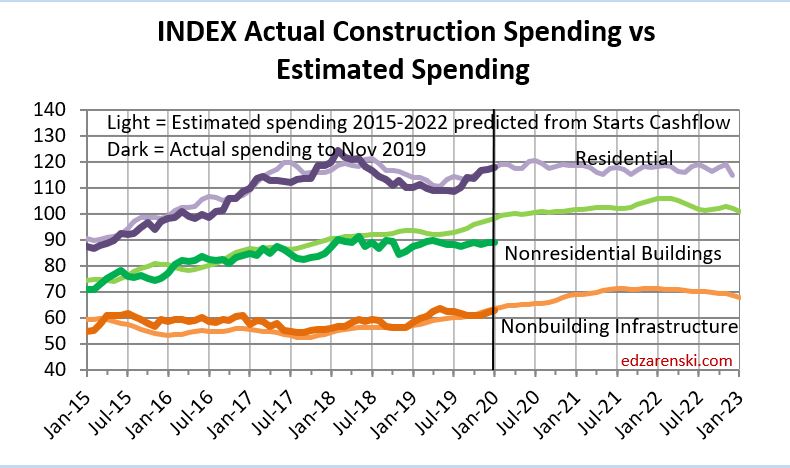

This compares the current construction spending data to a 2020 Forecast from April 1 before any Pandemic Impacts were recorded. It compares actual to what was expected Pre-Pandemic. The change in year-to-date (ytd) all occurred in 2nd quarter data. In fact, 1st quarter ytd growth was forecast at 7% and it came in at 9.5%. 2nd quarter growth was forecast at 6.8% and it came in at 1%.

Construction Spending 2020 year-to-date (ytd) thru June vs 2019

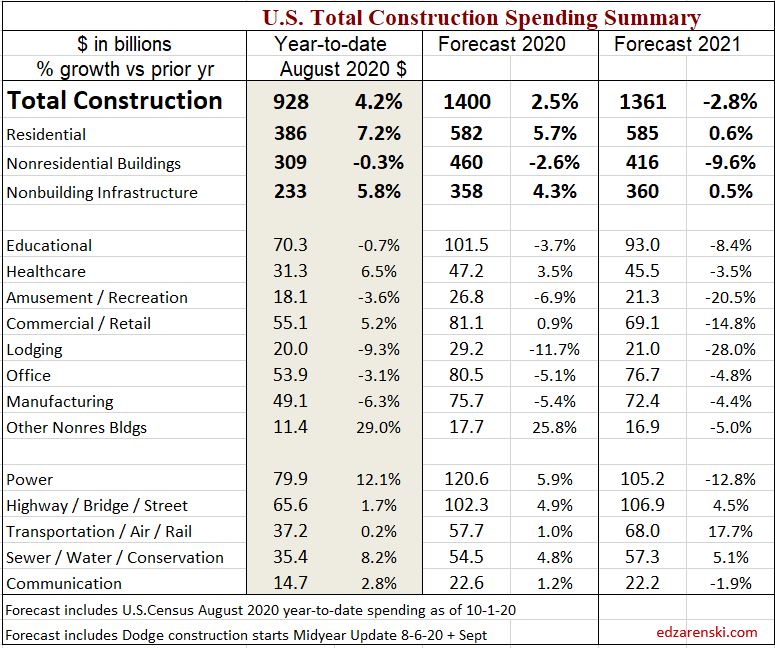

Actual ytd vs Pre-Pandemic Forecast ytd. Nearly all this change is due to projects delayed/shutdown.

- Nonres Bldgs down 2.4% ytd in 6mo vs pre-pandemic forecast

- NonBldg UP 3.0%

- Residential down 4.9%

- TOTAL down 1.9%

The measure of decline due to Pandemic delays and shutdowns is not the difference between Q1 and Q2 growth in ytd spending. Nor is the impact measured by the current difference in ytd performance vs 2019. It’s the difference between what was forecast for ytd growth pre-pandemic vs actual ytd growth.

For instance, Residential construction spending thru Q2, as reported in the US Census June construction spending release, is up ytd 7.8%. But pre-pandemic it was forecast to be up 12.7% ytd after 6 months. Hence, residential spending has been impacted by a 12.7% – 7.8% = 4.9% decline from original forecast thru June.

Future impact on spending from lost construction starts

Part one of the decline in construction spending was due to delays/shutdowns. Part two will be the impact of reduced construction starts. That has very little affect right now, but will play out over the next few years. But remember once again, the impact in 2021 is not measured by the difference between 2020 and 2021, its the difference between current forecast for 2020/2021 and the pre-pandemic forecast for 2020/2021.

Year-to-date, total construction starts are down 14%. Residential new starts are down 5%, nonresidential buildings down 22% and non-building infrastructure starts are down 14%.

Dodge updated their forecast to show 2020 construction starts for nonresidential buildings fall on average 20%, less in some markets, but -30% to -40% in a few. Only warehouses is up. Non-building starts fall on average 15%. Only Highway/Bridges is up. Residential starts may fall only 5%-10%.

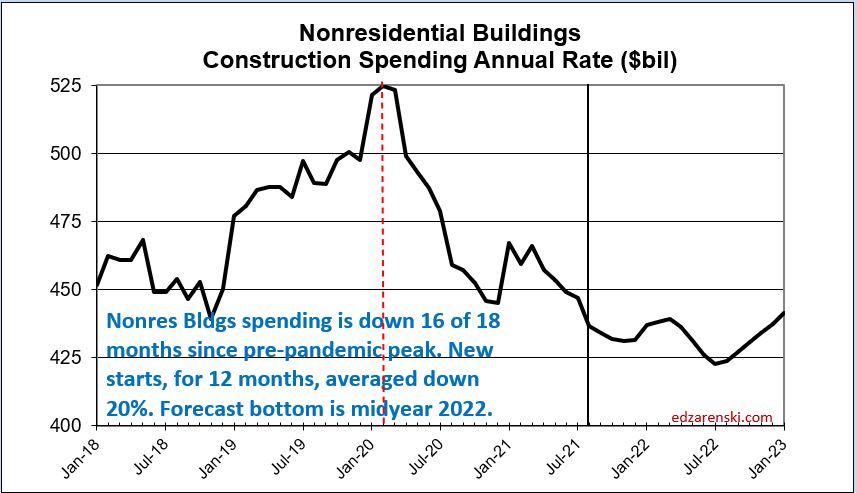

How those lowered starts affect spending is spread out over cash flow curves for the next few years. This has a major impact on jobs later in 2020 and all of 2021 into 2022. For nonresidential buildings, the greatest impact to spending and jobs affected by a reduction of new starts in 2020 occurs from 2021 into 2022 when many of those lost starts would have been reaching peak spending.

Only about 20% of new starts gets spent in the year they started. 50% gets spent in the next year. The effect of new starts does not show up immediately. If new nonresidential buildings starts in 2020 are down 22%, on average, the affect that has on 2020 is reduced spending by -22% x 20% = – 4.4%. But the affect it has on 2021 is -22% x 50% = -11%.

Construction Spending FORECAST 2020 vs Pre-Pandemic Forecast

This change in forecast incorporates reduced new construction starts for 2020 but also includes the impact from delays and shutdowns.

- Nonres Bldgs down 5.4% for 2020 vs pre-pandemic forecast

- NonBldg down 0.3%

- Residential down 6.5%

- TOTAL down 4.5% vs pre-pandemic forecast

Construction Spending FORECAST 2021 vs Pre-Pandemic Forecast

Nearly all this change due to a reduction in new construction starts in 2020. Notice, it is nonresidential buildings that are impacted the most, down 10% from the pre-pandemic forecast.

- Nonres Bld down 9.9% for 2021 vs pre-pandemic forecast

- NonBldg down 6.4%

- Residential UP 5.8%

- TOTAL down 2.5% vs pre-pandemic forecast

Future impact on backlog from delays/cancellations and reduced starts

Starting Backlog is the Estimate-to-Complete (ETC) value of all projects under contract at the beginning of a period. Projects in starting backlog could have started last month or last year or several years ago. Many projects in backlog extend out several years in the schedule to support future spending, so backlog growth in not an indicator that tracks year over year with spending. Current backlog at the start of 2020 would still contribute some spending for the next 6 years until all the projects in backlog are completed.

The last time starting backlog decreased was 2011. Starting backlog will fall 10% in 2021 and 2% in 2022. Except for residential work, about 80% of annual spending comes from starting backlog.

Some of the projects delayed or canceled started before Jan. 2020. When one of those projects is delayed, the portion of the project delayed gets removed from 2020 backlog, but then gets added to future backlog. When one of those projects is canceled, the portion of the project not yet put-in-place gets removed from 2020 and future backlog. Not only does that reduced future backlog but also that retroactively reduces the backlog that was on record at the start of 2020. Therefore, 2020 backlog is reduced by delays and cancellations and future backlog is increased by delays, but reduced by cancellations and a loss of new construction starts.

The following is the difference between what was forecast for backlog pre-pandemic and currently projected backlog based on delays, cancellations and reduced starts.

Backlog projected for the start of 2020:

- Total Construction down 3.6% vs pre-pandemic forecast

- Nonresidential buildings down 8.3%

- Non-building infrastructure up 0.5%

- Residential backlog down 2.2%, new starts down 5.4%

Although two thirds of Residential spending comes from new starts within the year, 2020 backlog is down 2.2%. 2020 new starts are down 5.4%.

The biggest changes to 2020 backlog are Manufacturing, Commercial/Retail and Amusement/Recreation, all down 10% to 15%.

Backlog projected for the start of 2021:

- Total Construction down 9.8% vs pre-pandemic forecast

- Nonresidential buildings down 15.1%

- Non-building infrastructure down 9.4%

- Residential backlog up 3.6%, starts up 8.4%

For 2021, Power and Environmental Public Works are down 20% and 10% respectively, but Nonresidential Buildings shows most of the losses. Lodging -40%, Amusement -28%, Manufacturing -26%, and Office and Commercial both down about 15%.

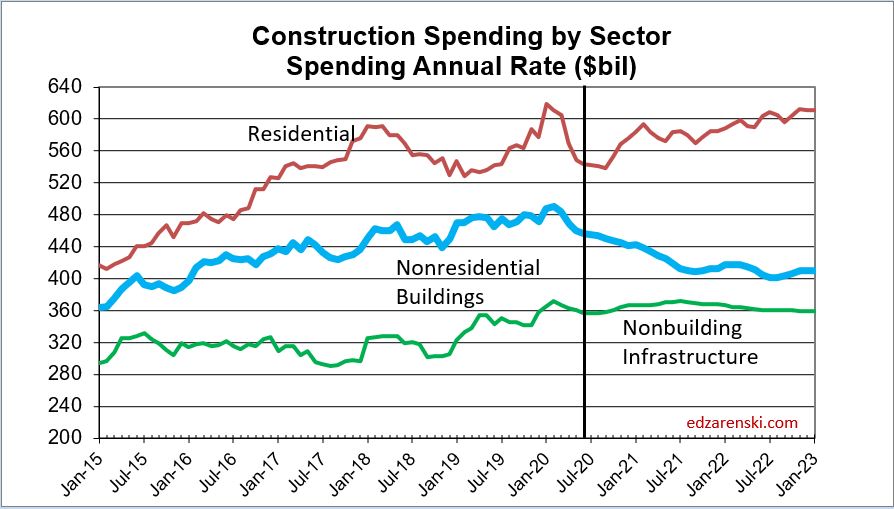

Spending Forecast 2020 – 2021

Now that we have highlighted the change in the forecast compared to the pre-pandemic forecast, let’s look at the current spending forecast for 2020 and 2021.

See Pandemic #11 – June Construction Spending Update for coverage of midyear spending year-to-date through June.

For 2020, the biggest declines are Manufacturing, Lodging and Amusement/Recreation, all down -8% to -10%. Commercial/Retail ends up +3.9% (this market is 60% Warehouse). Office and Educational are down -3% and -1%. Nonresidential buildings takes the brunt of declines in both 2020 and 2021.

In 2021, every nonresidential building market is down from 2020, some markets down 10% to 20%. Educational, Healthcare and Office are all down 3% to 5%. Non-building infrastructure Power market is down -11%, but Highway and Transportation are up +10% to 20%.

Almost every market has a weaker spending outlook in 2021 than in 2020, because of lower starts in 2020. Starts lead to spending, but on a curve, a good average for nonresidential buildings is 20:50:30 over three years. 20% of the total of all starts in 2020 gets spent in 2020 (yr1) and that represents also about 20% of all spending. 50% of the total value of 2020 starts gets spent in the following year, 2021. So, 50% of spending in 2021 is generated from 2020 starts. If starts are down 20% and 50% of spending comes from those starts, spending will be down 20% x 50% of the work.

Although starts are forecast down 15% to 20% in 2020 and UP 5% to 15% in 2021, the drop in starts in 2020 has the greatest impact on reducing spending in 2021. By June of 2021, spending is down 10% from Feb 2020 and volume is down 14%.

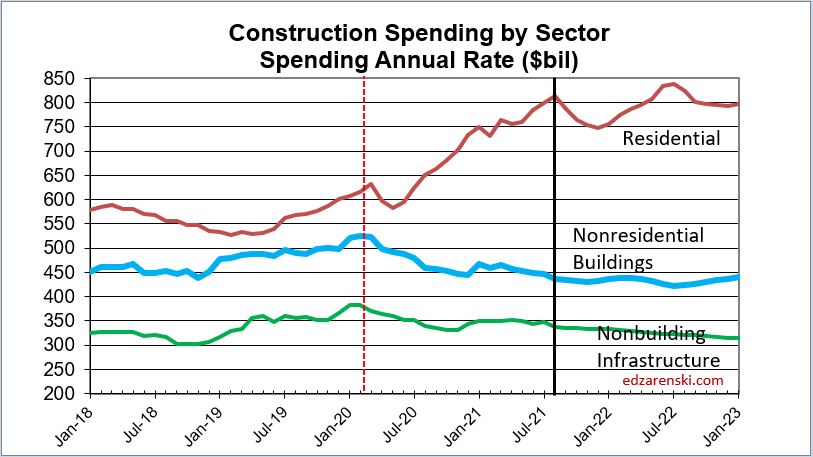

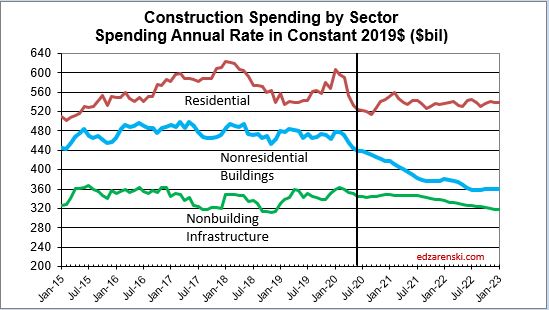

Before we can look at the effect on jobs, we need to adjust spending for inflation. The plot above “Spending by Sector” is current dollars. Here that plot is adjusted for inflation and is presented in constant $. Constant $ show volume. Notice residential remains in a narrow range after adjusting for inflation. No sector shows improvement in volume through Jan. 2023.

By far the greatest decline in volume is in the nonresidential buildings sector. Volume declines follow in line with spending declines. The greatest losses in 2020 are Amusement/Recreation, Lodging and Manufacturing. In 2021, every major nonresidential building market drops in volume.

Why 400,000 construction jobs are not coming back

Reduced starts in 2020 has a major impact on jobs later in 2020 and all of 2021 into 2022. For nonresidential buildings, the greatest impact to spending and jobs occurs from 2021 into 2022 when many of those lost starts would have been reaching peak spending.

Jobs data show construction added 20,000 more jobs in July. After losing almost 1,100,000 jobs in March and April (out of a prior total 7,600,000), we regained 450,000 jobs in May and 160,000 in June. That leaves construction down 440,000 jobs from the February high point.

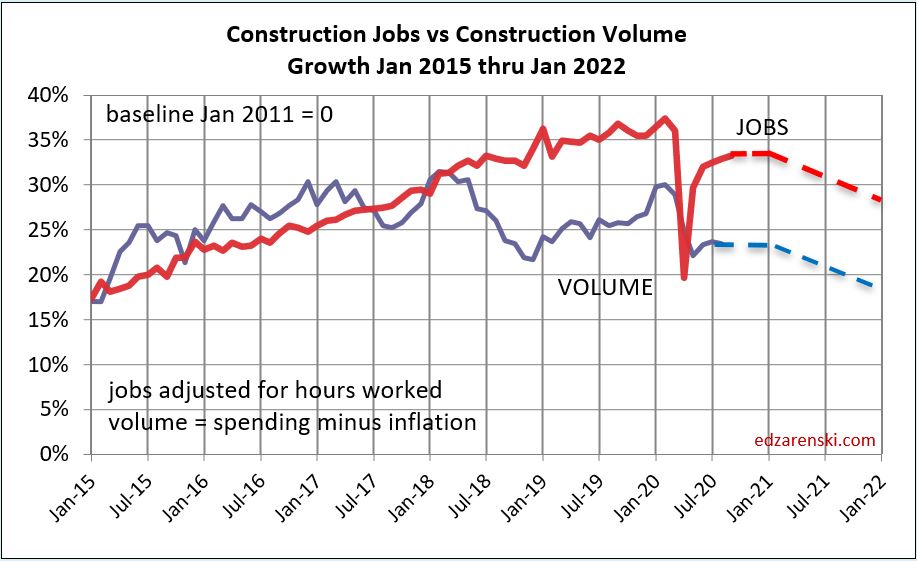

Jobs are down 6% from Feb to July, but construction spending is down 7% through June and volume (spending adjusted for inflation) is down 9%.

Although we may get slight jobs growth in the next few months, there is little to no volume growth to support it. Spending is currently down 7% from the Feb high and volume is down 9%. More spending declines are minimal through Q1 2021. Due to the large declines in new construction starts, we will begin to see additional spending and volume declines by spring 2021. Most of the decline will be in nonresidential buildings.

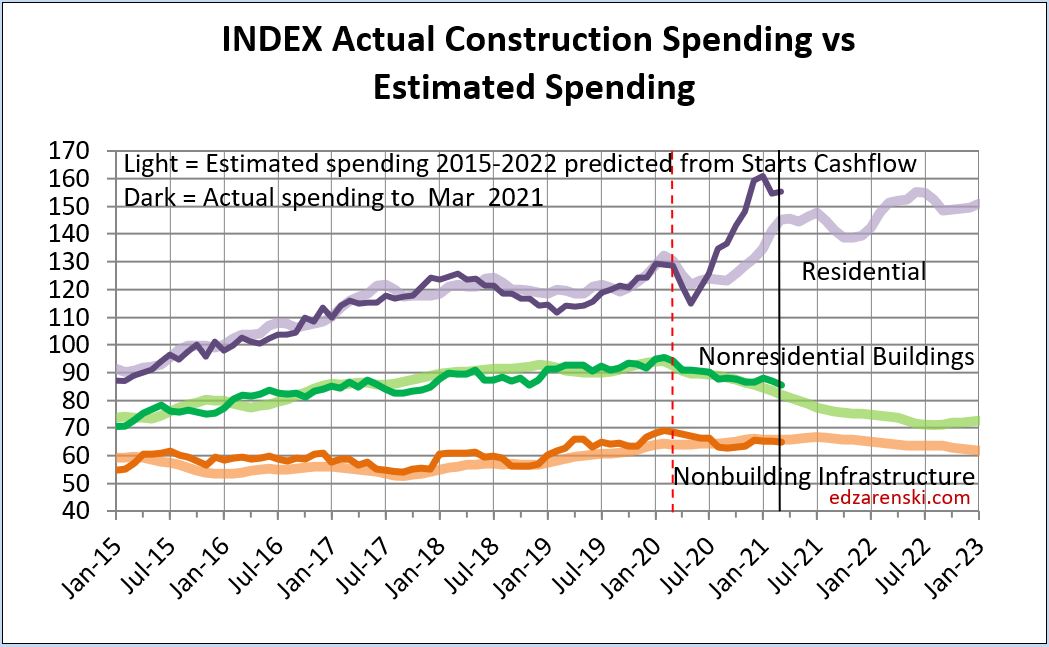

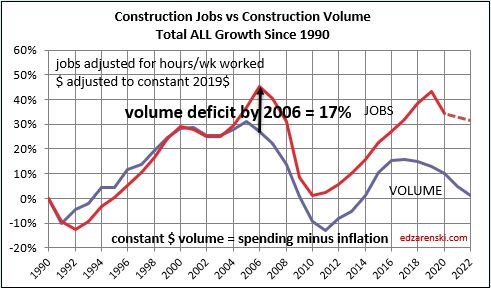

This annual plot back to 1999 shows construction spending vs construction volume. Volume is spending minus inflation. Notice, volume never recovered to peak 2005. Also notice, recent volume began to decline in 2018.

The long-term view of jobs vs volume shows an important point. With few exceptions jobs and volume grow equally. Setting a baseline to zero in 1990, there was a spread in 1992 that was nearly equalized by 1998. Jobs and volume growth remained near equal until 2004. Leading into 2006, spending increased by the most in 30 years. Jobs, which seem to lag slightly, grew 15% from 2004 thru 2006. But inflation posted the highest rate in 30 years. While jobs grew to meet spending growth, almost all the spending growth was inflation. By 2006, jobs growth exceeded construction volume by more than 15%.

As I said, with few exceptions, jobs and volume grow equally. If we modify history to reset the baseline to 2006 by increasing volume, the plot now shows that all years from 2006 to 2017 remained consistent in jobs growth vs volume growth. So, with exception of 1992 and 2004-2005, all years from 1990 to 2017 had consistent growth in jobs and volume.

Leading into 2017, spending once again reached a rate of near record growth, second only to 2004-2005. Again, jobs, which seem to lag slightly, grew to meet spending growth. But inflation posted the highest rate since 2006. Once again, jobs grew rapidly, but almost all the spending growth was inflation. By 2019, for the second time, jobs growth exceeded construction volume by almost 15%.

Jobs are supported by growth in construction volume, spending minus inflation. We will not see construction volume return to Feb 2020 level at any time in the next three years. This time next year, volume will be 5% lower than today, 14% below the Feb 2020 level.

We are currently down 440,000 construction jobs from the Feb high. We may regain 40,000 to 50,000 more jobs before the end of the year. But the declining work volume due to a reduction in new starts in 2020 is indicating by this time next year, not only is there no volume to regain 400,000 lost jobs, but we may lose another 200,000 jobs and be down 600,000 jobs below the Feb 2020 high.

The following plot is the same jobs and volume data as above, only plotted monthly rather than annually. Much of the fear decline of jobs in April has been corrected, but jobs are still down 440,000 from the February high. And yet, the plot shows jobs in excess of construction volume by about 12%.

Volume is set to decline at least for the next two years. There will be no volume growth to support jobs growth and long-term jobs growth already exceeds volume growth by 12%. This is not an environment that supports jobs growth.