Home » Residential (Page 2)

Category Archives: Residential

2018 Construction Spending Forecast – Mar 2018

3/15/18

Preliminary data is in for total year 2017 construction spending, 2017 construction starts and 2018 starting backlog. The following forecast is developed using the current data.

2018 Construction Spending Forecast – Mar 2018

A brief note on 2017.

2017 Spending Wrap Up

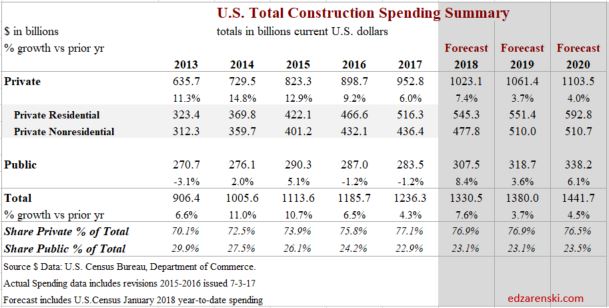

Total construction spending in 2017 now stands at $1.233 trillion, an increase of 4.0% over 2016.

Residential spending, up 10.5% for the fifth consecutive year above 10% growth, leads all construction spending in 2017 for the seventh consecutive year. Nonresidential Buildings finished the year up 2.3%. Only Non-building Infrastructure did not improve over 2016, down 3.8% for the year. However, Non-building Infrastructure had been at an all-time high for the previous two years.

2017 spending finished below my forecast due to performance in Educational, Office, Power and Highway, four of the five largest markets which together make up half of all nonresidential spending. All came in lower than forecast. However, some of these markets are prone to very large post-annual upward revisions and that has the potential to add to 2017 spending when those revisions are released in July 2018. For instance, in the July 2017 revisions, Power spending for the previous year, 2016, was revised up by 10%.

History shows spending has been revised up 53 times in the last 60 months. I expect to see future revisions smooth out spending in unusually low periods and increase total 2017 spending above this forecast. Both April and July preliminary spending appear statistically too low. The average post-annual total spending revision for the last five years is +2.8%. The post-annual revision to 2016 was only 2.2%. Revisions due for release on July 1, 2018, if even only a +1% revision to 2017, would adjust total 2017 spending up to $1,245 billion. This would slightly alter the 2018 forecast.

2018 Spending Total All Construction

Total All 2018 construction spending is forecast to increase 7.6% to $1.330 trillion.

Nonresidential Buildings spending forecast for 2018, up 9%, will be supported by Manufacturing and Educational. Non-building Infrastructure returns to strong growth of 8%, with potential to hit a new all-time high due to very large projects in Power and Transportation. Residential spending in 2018 slows to growth under 6% after six years all over 10%/year.

Dodge Data 2017 construction starts increased 3% from 2016. However, starts are always revised upward in the following year. I expect revisions will show 2017 starts increased by more than 6% over 2016. Even with that revision, 2017 starts posted the lowest growth since 2011, weighted heavily by the slowdown in residential starts.

Total starting backlog for 2018, currently at an all-time high, has increased on average 10%/year the last three years. 80% of all Nonresidential spending within the year will be generated from projects in starting backlog. Public share of new construction starts are up only 10% in 3 years. But due to long duration job types, 2018 starting backlog is up 30% in the last 3 years.

None of this spending forecast includes any projections for potential work from future infrastructure stimulus.

Current$ vs Constant$

Construction spending reached a new current $ high in 2017 at $1,236 billion. The previous high in current $ was $1,161 in 2006. Spending first surpassed that in 2014 and has been increasing since. But that is in current $, which includes inflation.

Comparing current $ spending to previous year spending does not give any indication if business is increasing. The inflation factor is missing. If spending is increasing at 4%/year in a time when inflation is 6%/year, real volume is declining by 2%.

Although 2018 current $ spending will reach $1,330 billion, after adjusting for 4.5% to 5% inflation, 2018 constant $ volume will increase to only $1,270 billion. When comparing inflation adjusted constant dollars, 2018 spending will still be lower than all years from 1998 through 2007. In 2005 constant $ volume reached a peak at $1,450 billion. At current rates of growth, we would not eclipse the previous high before 2022.

While spending in current $ is 7% higher than the previous high spending, volume is still 14% lower than the previous high volume.

For more on Inflation Adjusted spending see Construction Spending is Back

Jobs and Volume

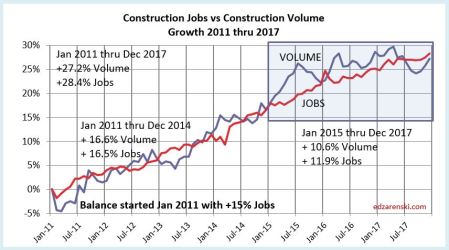

The period 2011-2017 shows both spending and jobs growth at or near record highs.

A spending forecast of 7%+ in 2018, or nearly $100 billion in construction spending, demands a few words on jobs growth. Construction requires about 5000 workers for every added $1 billion in construction volume. Construction jobs have never increased by 500,000 in one year. However, $100 billion in added spending is not the same as $100 billion in volume, and jobs growth is based on volume.

Although spending will increase 7%-8%, construction inflation has been hovering near 4.5% to 5% for the last five years. Real volume growth in 2018 after inflation is expected to be near 3% or $40 billion. That would mean the need, if there are no changes in productivity, is to add only about 200,000 additional workers in 2018, a rate of jobs growth that is well within reach. That is less than the average jobs growth for the last seven years.

Construction added 1,339,000 jobs in the last 5 years, an average of 268,000/year. The only time in history that exceeded jobs growth like that was the period 1993-99 with the highest 5-year growth ever of 1,483,000 jobs. That same 1993-99 period had the previous highest 5-year spending and volume growth going back to 1984-88.

Construction added 185,000 jobs in the last 4 months, Nov17-Feb18. That’s happened, for any 4-month period, only 5 times since 1984. The last time was 2005-06, during the fastest rate of spending increases since 1984.

Total all spending increased 55% since 2010, but there was 30% inflation. Real total volume since 2010 has increased by only 25%. Jobs increased by 30%, 5% in excess of volume growth. But the results are much different for Residential than Nonresidential.

Nonresidential spending increased 43% since 2010, but there was 30% inflation. Real nonresidential volume since 2010 has increased by only 12%. Jobs increased by 27%, 15% in excess of volume growth.

Residential spending increased by 110% since 2010, but after inflation, real residential volume increased by only 57%. Jobs increased by only 37%, 20% short of volume growth.

For more on Jobs see Construction Jobs and Residential Construction Jobs Shortages

Residential Buildings Spending

Total Residential spending in 2017 finished at $523 billion, up 10.6% from 2016. This is the 5th consecutive year that residential spending exceeded 10% annual growth. Average spending growth the last six years is 13%/year.

Residential spending in 2017 was 50% single family, 13% multi-family and 37% improvements. In 2011, improvements was 48% of residential spending.

Census does not include flood damage repairs (house shell remains intact but gut renovate) in improvements but does include full flood damaged structure replacements (structure rebuild permit classified as new) in improvements.

Residential spending is more dependent on new starts within the most recent 12 months than on backlog from previous starts. Total starts for the last 6 months are the highest since 2006, but % growth has slowed considerably. New starts in 2017 posted only 2% growth, but I expect that to be revised up to at least 4%. Similar growth of 6%-7% is expected for 2018. Slower growth is now expected after 5 years (2012-2016) of new starts increasing at an average 20%/year.

Residential 2018 spending growth is forecast to increase only 6% after five years over 10%. Total residential spending in 2018 is forecast at $552 billion.

Residential spending will reach a 12-year high in 2018. Residential spending reached its current $ peak of $630 billion in 2005. Current 2018 pending is still 13% below that peak. In constant $, adjusted for inflation, all years from 1998 through 2007 were higher than 2018. In constant $, 2018 spending is still 27% below the 2005 peak.

Residential buildings construction spending in constant $ reached $523 billion in 2017. Previous spending adjusted to equivalent 2017$ shows that all years from 1996 through 2007 had higher volume than 2017. Volume reached a peak $748 billion in 2005. Only the years 2004-2006 had higher spending in current $. The 2005 current $ peak of $630 billion is still 17% higher than 2017, but 2017 volume is still 30% lower than peak volume.

Nonresidential Buildings Spending

Nonresidential Buildings spending in 2017 finished at $419 billion, up only 2.7% from 2016.

2017 spending finished below my forecast due to performance in Educational and Office. Educational starts increased 6%+/year for the last three years, but spending increased only 4%/year the last two years. Office starts increased nearly 30% in 2016, but spending increased only 3% in 2017. I suspect either big upward revisions to 2017 spending or large increases in backlog will boost 2018 spending in these two markets.

Nonresidential Buildings new starts are up 60% in four years. 2018 starting backlog is the highest ever, up 15% from 2017. Nonresidential Buildings 2018 starting backlog is 50% higher than at the start of 2014, the beginning of the current growth cycle.

Starting backlog has increased for five years at an average 10%/year. Spending from starting backlog, up 10% in 2018, increased for five years at an average 9%/year.

For 2018, Educational spending is projected to increase 14%, the best increase since 2007. Starting backlog increased 10%/year for the last three years. Manufacturing posted several very large project starts in 2017. Spending is projected to increase 12% in 2018.

Nonresidential Buildings spending in 2018 is forecast to reach a new high, $459 billion, an increase of 9.5% over 2017, surpassing the previous 2008 high. Educational and Manufacturing make up 55% of the growth.

For the Full Expanded 2018 Construction Spending Forecast – Nonresidential Bldgs

Nonresidential buildings construction spending in constant $ (inflation adjusted $) reached $419 billion in 2017. In 2018 it will reach $439 billion. Constant $ spending shows all years from 1996 through 2010 had higher volume than the 2018 forecast. Volume reached a peak $536 billion in 2000 and went over $500 billion again in 2008. In constant $ 2018 is still 18% below that 2000 peak.

Non-building Infrastructure Spending

Total non-building infrastructure spending in 2017 dropped to $293 billion, down 3.7% from 2016.

Non-building Infrastructure spending, always the most volatile sector, dropped to yearly lows from June through September, the lowest since November 2014. However, this short dip was predicted. Cash flow models of Infrastructure starts from the last several years predicted that dips in monthly spending would be caused by uneven project closeouts from projects that started several years ago, particularly in Power and Highway markets.

Current backlog is at an all-time high and spending is expected to follow the increased cash flows from the elevated backlog. Environmental Public Works (Sewage/Waste disposal down 14%, Water Supply down 9% and Conservation/Dams & Rivers down 7% in 2017) posted the largest declines in 2017 and accentuated the declines in the infrastructure sector. The sector was expected to increase in the last quarter 2017. All three markets posted increases in the 4th quarter, up 8% over the 1st nine months of 2017.

Non-building Infrastructure 2018 starting backlog is the highest ever, up 10%+ each of the last 3 years. Transportation terminals new starts in 2017 jumped 120%. Rail project starts increased more than 100%. Starting backlog for all transportation work is the highest ever, up 100% in the last two years. Transportation spending is projected to increase 20-25%/year for the next two years.

No future growth is included from infrastructure stimulus and yet 2018 spending is projected to increase by 8%.

Non-building Infrastructure will reach a new high for spending in 2018. Spending reached an all-time high in 2015 and stayed within 0.3% of that high for 2016. A 3.5% decline in 2017 was more of a decline than expected, but there may still be upward revisions to the preliminary total.

Non-building Infrastructure spending in 2018 is forecast to reach $319 billion, an increase of 8.6% over 2017.

My forecast for 2018 is predicting every infrastructure market will post gains, but it is the Power and Transportation markets that account for most of the growth in 2018. Transportation new starts in 2017 grew 120% due to massive new air terminal and rail projects. Spending growth in the Power market is not quite so apparent. Combined Power new starts are down for both 2016 and 2017, but the spending gains are coming from projects that started in 2015, a year in which starts were up over 120%.

Adjusted for inflation, spending in 2018 will be nearly equal to the all-time highs reached in 2015 and 2016.

Non-building Infrastructure construction spending in constant $ reached $294 billion in 2017. Recent highs were posted in 2015 and 2016 at $305 billion and $304 billion and 2018 is expected to reach $319 billion. Previous spending adjusted to equivalent 2017$ shows that 2008 and 2009 were both just slightly higher than $300 billion. Constant $ volume reached a peak $313 billion in 2016. Spending in current $ hit new highs in 2015 and 2016. This is the only sector that has current $ and constant $ at or near all-time highs.

Public Infrastructure and Public Institutional

Only 60% of all Non-building Infrastructure spending, about $170 billion, is publicly funded. That public subset of work averages growth of less than $10 billion/year.

Only about 25% of all Nonresidential Buildings spending, about $100 billion, is publicly funded, mostly Educational.

- Infrastructure = $300 billion, 25% of all construction spending.

- Infrastructure is about 60% public, 40% private. In 2005 it was 70% public.

- Public Infrastructure = $170 billion. Private Infrastructure = $130 billion.

- Power and Communications are privately funded infrastructure.

- Nonresidential Buildings is 25% public (mostly institutional), 75% private.

- Educational, Healthcare and Public Safety are Public Nonres Institutional Bldgs

- Public Commercial construction is not included.

- Public Institutional = $100 billion, mostly Education ($70b).

Public Infrastructure + Public Institutional = $270 billion, 23% of total construction spending.

Public Infrastructure + Institutional average growth is $12 billion/year. It has never exceeded $30 billion in growth in a single year.

See also Publicly Funded Construction

See also Down the Infrastructure Rabbit Hole

Public Spending

Public construction is a subset of Nonresidential Buildings and Non-building Infrastructure and about 1% of Residential.

The two largest markets contributing to public spending are Highway/Bridge (32% of total public spending) and Educational (26%), together accounting for nearly 60% of all public construction spending. At #3, Transportation is only about 10% of public spending. Environmental Public Works combined makes up almost 15% of public spending, but that consists of three markets, Sewage/Waste Water, Water Supply and Conservation. Office, Healthcare, Public Safety and Amusement/Recreation each account for about 3%.

2017 spending was down 1%, but has been at or near the all time high for three years.

Total public spending for 2017 finished flat at $284 billion with most major public markets down for the year. By far, the largest Public spending declines in 2017 are Sewer and Waste Disposal which is 7% of public markets, it was down 16% and Highway/Bridge, down only 3.5%, but Highway is 32% of all public spending.

Public spending hit a low in June 2017. It has been increasing since then, Public Educational, in the second half 2017 up 10% from the low point, now at a post recession high. We can expect to see another six months of growth before spending levels off in mid-2018.

Due to long duration job types, 2018 starting backlog is up 30% in the last 3 years. In 2018, 40% of all spending comes from jobs that started before 2017. Leading 2018 growth are Educational (+15%) and Transportation (+35%), with a combined total forecast 20% growth in public spending.

Current levels of backlog and predicted new starts gives a projection that Public Non-building Infrastructure spending will reach an all-time high in 2018 and again in 2019.

Total Public spending in 2018 is forecast to reach $307 billion, an increase of 8% over 2017, the best growth in 10 years.

Educational and Transportation will contribute equally and together account for almost 60% of the Public spending growth in 2018. Transportation new starts in 2017 grew 120% due to massive new air terminal and rail projects. Educational new starts total for the last three months posted the highest quarter in at least seven years. The 2nd highest quarter was also within the last 12 months, so still contributes fully to 2018 spending. 2018 signifies a turn-round in Public spending which has not posted significant growth since the recession.

Public spending is 10%, $30 billion, below 2009 all-time highs, most of the deficit coming from declines in Educational, Sewage/Waste Water and Water Supply. In 2018, Highway and Transportation are at all-time highs.

Click here for a formatted printable PDF Construction Spending Forecast – Summary Mar 2018

See these posts for additional info

2018 Construction Spending Forecast – Nonresidential Bldgs

Starts Trends Construction 2018 Forecast – Fall 2017 11-8-17

Backlog Construction 2018 Forecast – Fall 2017 11-10-17

For more on Jobs see Construction Jobs / Workload Balance 11-7-17

For effects of inflation see Constant Dollar Construction Growth 11-2-17

Construction Activity Notes 4-25-18

Notes on March 2018 Construction Spending

2018 Construction Outlook Articles Index

Articles Detailing 2018 Construction Outlook

Links will open in a new tab

These links point to articles here on this blog that summarize end-of-year data for 2017 and present projections for 2018.

Most Recently Published

July Construction Starts Fall but 3moAvg at New High

Construction Spending June 2018 8-1-18

June Construction Starts Reach New Highs 7-25-18

Construction JOLTS – What’s wrong with this picture? 7-10-18

Construction Spending 2016-2017 Revisions 7-1-18

New Construction Starts May 2018 Near All-Time High 6-24-18

Construction Spending April 2018 – 6-1-18

Notes on March 2018 Construction Spending 5-2-18

Construction Activity Notes 4-25-18

2018 Construction Spending Forecast – Nonresidential Bldgs 3-28-18

2018 Construction Spending Forecast – Mar 2018

Construction Economics Brief Notes 3-10-18

Construction Spending is Back 3-9-18

Publicly Funded Construction 2-28-18

PPI Materials Input Index 2-20-18

Down the Infrastructure Rabbit Hole 2-16-18

Inflation in Construction 2018 – What Should You Carry? 2-15-18

Residential Construction Jobs Shortages 2-3-18

2018 Construction Spending – Briefs 1-26-18

Cautions When Using PPI Inputs to Construction! 1-15-18

Indicators To Watch For 2018 Construction Spending? 1-10-18

Spending Summary 2018 Construction Forecast Fall 2017 12-3-17

Backlog 2018 Construction Forecast Fall 2017 11-10-17

Starts Trends 2018 Construction Forecast Fall 2017 11-8-17

In What Category is That Construction Cost? 11-15-17

Construction Jobs / Workload Balance 11-7-17

Constant Dollar Construction Growth 11-2-17

Is Infrastructure Construction Spending Near All-Time Lows? 10-10-17

Summary

2018 Construction Spending Forecast – Mar 2018

2018 Construction Spending – Briefs 1-26-18

Spending Summary 2018 Construction Forecast Fall 2017 12-3-17

Construction Spending is Back 3-9-18

2017 Results

2018 Construction Spending Forecast – Mar 2018

Spending Summary 2018 Construction Forecast Fall 2017 12-3-17

2018 Starting Backlog & New Starts

2018 Construction Spending – Briefs 1-24-18

Backlog 2018 Construction Forecast Fall 2017 11-10-17

Starts Trends 2018 Construction Forecast Fall 2017 11-8-17

Construction Starts and Spending Patterns 9-26-17

2018 Spending Forecast

2018 Construction Spending Forecast – Mar 2018

2018 Construction Spending – Briefs 1-26-18

So, About Those Posts “construction spending declines…” 10-4-17

Construction Spending Almost Always Revised UP 5-1-17

Nonresidential Buildings

2018 Construction Spending Forecast – Nonresidential Bldgs 3-28-18

2018 Construction Spending Forecast – Mar 2018

2018 Construction Spending – Briefs 1-24-18

Nonres Bldgs Construction Spending Midyear 2017 Forecast 7-24-17

Residential

2018 Construction Spending Forecast – Mar 2018

Residential Construction Jobs Shortages 2-3-18

Infrastructure Outlook

2018 Construction Spending Forecast – Mar 2018

Down the Infrastructure Rabbit Hole 2-16-18

2018 Construction Spending – Briefs 1-24-18

Is Infrastructure Construction Spending Near All-Time Lows? 10-10-17

Infrastructure – Ramping Up to Add $1 trillion 1-30-17

Calls for Infrastructure Problematic 1-12-17

Public Construction

2018 Construction Spending Forecast – Mar 2018

Publicly Funded Construction 2-28-18

Spending Summary 2018 Construction Forecast Fall 2017 12-3-17

Infrastructure & Public Construction Spending 3-5-17

Materials

PPI Materials Input Index 2-20-18

Jobs

Residential Construction Jobs Shortages 2-3-18

Construction Jobs / Workload Balance 11-2-17

Construction Jobs Growing Faster Than Volume 5-5-17

Inflation

Inflation in Construction 2018 – What Should You Carry? 2-15-18

Constant Dollar Construction Growth 11-2-17

Construction Inflation Index Tables UPDATED 2-12-18

Construction Cost Inflation – Commentary updated 2-13-18

US Historical Construction Cost Indices 1800s to 1957

Residential Construction Jobs Shortages

2-3-18

During the period including 2011 through 2017, we had record construction spending, up 50% in 5 years, moderate inflation reaching as high as 4.6% but averaging 3.8%, record construction volume growth (spending minus inflation), up 30% in 5 years and the the 2nd highest rate of jobs growth ever recorded.

Residential spending was up 90% in 5 years, but real residential volume up only 50%. Residential inflation, at 6%/year, was much higher than all construction. Jobs increased only 33%.

Construction added 1,339,000 jobs in the last 5 years. The only time in history that exceeded jobs growth like that was the period 1993-1999 with the highest 5-year growth ever of 1,483,000 jobs. That same 93-99 period had the previous highest spending and volume growth. 2004-2008 would have reached those lofty highs but the residential recession started in 2006 and by 2008 spending had already dropped 50%, offsetting the highest years of nonresidential growth ever posted.

The point made here is the period 2011-2017 shows spending and jobs at or near record growth. Although 2017 slowed, there is no widespread slowdown in volume or jobs growth.

This 2011-2017 plot of Construction Jobs Growth vs Construction Volume Growth seems to show there is no jobs shortage. In fact it shows jobs are growing slightly faster than volume. But that just does not sit well with survey data from contractors complaining of jobs shortages. So how is that explained?

There have been cries from some quarters, including this blog, that the answer lies in declining productivity. There seems to be plenty of workers, but it now takes more workers to do the same job that took fewer in the past. As we will see, that is part of the answer, but doesn’t explain why some contractors need to fill vacant positions. To find data that might answer that question about a jobs shortage we must dig a little deeper.

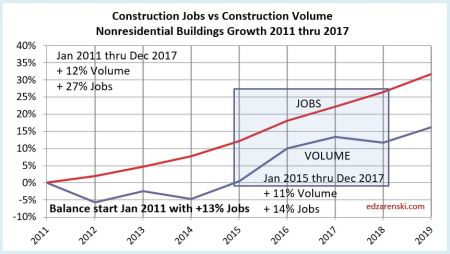

The total jobs vs volume picture masks what is going on in the three major sectors, Residential, Nonresidential Buildings and Non-Building Infrastructure. A breakout of jobs and volume growth by sector helps identify the imbalances and helps explain construction worker shortages. It shows the residential sector at a jobs deficit.

7 years 2011-2017 – % Jobs growth vs % Volume growth

- Totals All Construction Jobs +31%, Volume +30%

- Nonres Bldgs Jobs +27%, Volume +19%

- Nonbldg Hvy Engr Jobs +21%, Volume +12%

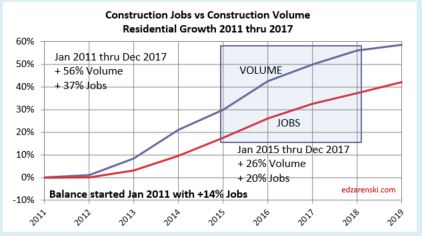

- Residential Jobs +40%, Volume +54%

The totals show jobs and volume almost equal, data that supports the 2011-2017 totals plot above and what we would expect in a balanced market. But severe imbalances show up by sector. Both nonresidential sectors show jobs growth far outpaced volume growth. Residential stands out with a huge deficit, with jobs way below volume growth.

Just looking at 2017 growth shows the most recent imbalances.

2017 % jobs growth vs % volume growth

- Totals All Construction Jobs +3.4% Volume -0.8%

- Nonres Bldgs Jobs +3.3% Volume -1.6%

- Nonbldg Hvy Engr Jobs +1.7% Volume -6.0%

- Residential Jobs +3.5% Volume +4.2%

Census recently released initial construction spending for 2017, totaling $1.230 trillion, up only 3.8% from 2016. What is somewhat disconcerting is that 2017 construction spending initial reports growth of 3.8% do not even match the total inflation growth of 4.6% for 2017, indicating a -0.8% volume decline. However, as does always occur, I’m expecting upward revisions (estimated +2%) to 2017$ construction spending on 7-1-18. If we don’t get an upward revision, then 2017 will go down as the largest productivity decline since recession. Even if we do get +2% upward revision to 2017$ spending, 2017 volume would be revised up to +1.2% and jobs growth will still exceed volume growth.

Let’s look a little deeper at the data within the sectors. Each chart is set to zero at Jan 2011 so we can see the change from that point, the low point of the recession, until today. At the bottom of each chart is shown a Balance at start. That represents the cumulative surplus or deficit of jobs growth compared to volume growth for the previous 10 years prior to Jan 2011. If there are no changes in productivity, or no surplus or deficit to counteract, then jobs should grow at the same pace as volume.

There are slight differences between the data in the three sector charts and the total construction chart. The sector charts use annual avg data and the totals chart uses actual monthly data.

Nonresidential Buildings and Non-building Infrastructure, over seven years and the most recent three years, show jobs increasing far more rapidly than volume. Nonresidential Buildings started 2011 with a surplus of jobs after the recession, but Infrastructure started 2011 with a substantial deficit of jobs. Only in this last year did Infrastructure jobs reach long-term balance with work volume.

Nonresidential Buildings started 2011 with a 13% surplus of jobs and more than doubled it in the seven years following. I’ve suggested before it could be that a part of this surplus is due to companies hiring to meet revenue growth, and not inflation adjusted volume. Although nonresidential spending actually increased 43%, volume since 2010 has increased only 12%. Since 2010 there has been 30% nonresidential buildings inflation, which adds zero to volume growth and zero need for new jobs. A 43% increase in spending could lead companies to erroneously act to staff up to meet spending, or revenue, more than needed for the 12% volume increase.

This plot for residential work shows from 2011 to the end of 2017, we’ve experienced a 20% growth deficit in jobs. How many residential jobs does this 20% growth deficit represent? From Jan 2011 through Dec 2017, residential jobs increased from approximately 2,000,000 to 2,700,000. So the base on which the % growth increased over that time is calculated on 2,000,000. An additional 20% growth would be a maximum of 400,000 more jobs needed to offset the seven year deficit. But what about the imbalances that existed when we started the period?

During the residential recession from just 2005 through 2010, residential volume declined by 55%, but jobs were reduced by only 38%. For the entire period 2001-2010, total volume of work declined by 14% more than jobs were reduced. Some of the surplus jobs get absorbed into workforce productivity losses and some remain available to increase workload. It’s impossible to tell how much of that labor force would be available to absorb future work, so for purposes of this analysis an estimate of at least 5% seems not unreasonable. That would mean for 2011-2017, instead of a need for an additional 20% more jobs, the need could be reduced by 5% or 100,000 jobs.

This analysis shows a current deficit of 300,000 to 400,000 residential construction jobs. While it does also show nonresidential buildings jobs far exceed the workload and there are more than enough surplus jobs to offset the residential deficit, there would be several questions of how transferable jobs might be between sectors.

- Are there highly technical specialty jobs in Nonresidential Buildings that would not be transferable to Residential?

- What is the incidence of specialty workers engaging in work across sectors? i.e., job is counted in one sector but working in another sector.

- What has been the impact of losing immigrants from the construction workforce?

- Is the ratio of immigrant workers in Residential much higher than Nonresidential?

- Is the pay more attractive in Nonresidential construction?

- What, if any, percentage of the Residential workforce is not being counted? Day labor?

One thing is known for certain, high-rise multifamily residential buildings may often be built by a firm that is classified primarily as a nonresidential commercial builder. Therefore, some jobs that are counted as nonresidential are really residential jobs.

I think most of these would have a more negative impact on Residential jobs. However, there is some possibility that the overall deficit may not be quite as high as available data show (points 2 and 6). And there is always the possibility that we’ve crossed a threshold that has led to new gains in productivity, although to some extent, the stark differences between Residential and Nonresidential Buildings data might counter that proposition.

These two following report references both document that there is a large unaccounted for shadow workforce in construction. This workforce is probably mostly residential.

NAHB’s HousingEconomics.com “Immigrant Workers in the Construction Labor Force”

and these more recent reports adds volumes of data on immigrant labor

NAHB’s Jan 2018 Report on Immigrant Labor in Construction

Pew – U.S. Unauthorized Immigrant Total Dips to Lowest Level in a Decade NOV 2018

Unemployment and productivity includes only jobs counted in the official U.S. Census Bureau of Labor Statistics (BLS) jobs report. Both these reports document a large, unaccounted for shadow workforce in construction. By some accounts, 40% or more of the construction workforce in California and Texas are immigrant workers. Immigrants may comprise between 14% and 22% of the total construction workforce. It is not clear how many within that total may or may not be included in the U.S. Census BLS jobs report. However, the totals are significant enough that they would alter some of the results commonly reported.

The best way to see the implications that the available data do show is to look at productivity. The simplest presentation of productivity measures the total volume of work completed divided by the number of workers needed to put the volume of work in place, or $Put-in-Place per worker. In this case, $ spending is adjusted for inflation to get a measure of constant $ volume, and jobs are adjusted for hours worked.

As the Residential jobs deficit increases vs workload, this plot shows that $PIP is increasing. That makes sense. The workload continues to increase and the jobs growth is lagging, so the $PIP per worker goes up. For Nonresidential Buildings, the rate of hiring is exceeding the rate of new volume and therefore the $PIP is declining.

In boom times, residential construction adds between 150,000 and 170,000 jobs per year and has only twice since 1993 added 200,000 jobs per year. In the most recent several years expansion, residential has reached a high of 156,000 jobs in one year but has averaged 130,000 per year over 5 years. So it’s pretty unlikely that we are about to start adding residential construction jobs at a continuous rate of 200,000+ jobs per year.

If residential jobs growth were to increase by 50,000 jobs per year over and above current average growth, it would take 6 to 8 years to wipe out the jobs deficit in residential construction.

This problem is not going away anytime soon.

For more history on jobs growth see Is There a Construction Jobs Shortage?

For more on the imbalances of Res and Nonres jobs see A Harder Pill To Swallow!

For some hypotheses as to why nonresidential imbalances continue to increase see Construction Spending May 2017 – Behind The Headlines

Spending Summary Construction Forecast Fall 2017

3-15-18 see also 2018 Construction Spending Forecast – Mar 2018

12-2-17

Summary

Total construction spending in 2017 will reach $1,236 billion, an increase of 4.2% over 2016. Residential spending is above 10% growth for the 5th consecutive year.

Year-to-date construction spending growth through October is 4.1%.

Residential leads construction spending growth in 2017 for the seventh consecutive year, up 10.6%. My Nonresidential Buildings forecast has been lowered since July but finishes the year up 2.8%. Only Non-building Infrastructure will not improve over 2016, down 3.7% for the year. However, Non-building Infrastructure has been at an all-time high for the previous two years.

This forecast is down slightly since July due to reductions in both nonresidential buildings and non-building infrastructure. Educational, Office, Power and Highway, four of the five largest markets which together make up half of all nonresidential spending, were all lowered. Some of these markets are prone to very large post-annual upward revisions and that has the potential to add to 2017 spending when those revisions are released in July 2018. In the July 2017 revisions, Power spending for 2016 was revised up by 10%.

History shows spending has been revised up 51 times in the last 55 months. I wouldn’t be surprised to see future revisions smooth out spending in unusually low periods (April and July) and increase total 2017 spending above this forecast. I suspect revisions in July 2018 may show 2017 spending as high as $1,250 billion. The average post-annual total spending revision for the last five years is +2.3%. The total revision to 2016 was only 2.2%.

None of the spending detailed in this analysis includes any projections of potential work from future infrastructure stimulus.

Total construction spending in 2018 is currently forecast to reach $1,334 billion, an increase of 8.0% over 2017. For the first time since pre-recession, Non-building Infrastructure will lead all spending with potential to increase by 10% growth over 2017.

Non-building Infrastructure is forecast to lead 2018 spending with an increase of 10.2% due to very large projects in Power and Transportation. Nonresidential Buildings growth is strong for 2018, forecast up 9.3%. Residential spending in 2018 slows to only 5.7% growth after six years averaging 13%/year.

Total spending will reach a new high in 2018 for the third consecutive year. However, in constant $ adjusted for inflation, spending is just back to the level of 2008. The all-time constant $ high was reached in 2005. Adjusted for inflation, 2018 will still be 12% below that level. At current rates of growth, we would not eclipse the previous high before 2022.

Growth of 8% in 2018 or $100 billion in construction spending demands a few words on jobs growth. Construction requires about 5000 workers for every added $1 billion in construction volume. Construction jobs have never increased by 500,000 in one year. However, $100 billion in added spending is not the same as $100 billion in volume, and jobs grow based on volume. Although spending will increase 8%, construction inflation has been hovering near 4.5% to 5% for the last five years. Real volume growth in 2018 after inflation is expected to be just over 3% or $40 billion. That would mean the need, if there are no changes in productivity, is to add about 200,000 additional workers in 2018, a rate of jobs growth that is well within reach since that is below the average jobs growth for the last seven years.

Residential Buildings Spending

Total Residential spending in 2017 will finish at $523 billion, up 10.6% from 2016. Residential spending is above 10% growth for the 5th consecutive year.

Residential spending was expected to dip between May and October due to a low volume of work contributed from starts cash flows. The actual data shows, after reaching a seasonally adjusted annual rate (saar) of $536 billion in March, the high for the year, spending dropped 3% to 4% to as low as $515 billion saar three times and has averaged only $520 billion saar from April through October. New starts in Q1’17 reached an 11-year high, so I expect the rate of spending to increase at year end. Residential work will close out the year with 10.6% growth, the 5th consecutive year over 10%. Average growth the last six years is 13%/year.

Residential spending is 50% single family, 13% multi-family and 37% improvements.

Residential Improvements has posted 18% growth year-to-date. Single Family spending is up 9% while multi-family is up only 4%. That is compared to 2016 when improvements for the year finished up 10%, SF up 4% and MF up 5%. Census does not include flood damage repairs in improvements but does include full flood damaged structure replacements in improvements.

Total residential spending in 2018 slows to a forecast of $553 billion, only 5.7% growth over 2017.

Due to the shorter duration of projects, nearly 70% of residential spending within the year is generated from new starts. Unlike Nonresidential, backlog does not contribute nearly as much to Residential spending within the year. New Residential starts in Q1’17 reached an 11-year high. Residential starts are at a post-recession high.

Residential spending will reach a 12-year high in 2018. Adjusted for inflation, all years from 1996 through 2007 were higher. Inflation adjusted spending is still 30% below the all-time high reached in 2005.

Nonresidential Buildings Spending

Total Nonresidential Buildings spending in 2017 will come in at $420 billion, up only 2.8% from 2016.

Commercial/Retail is expected to finish the year with +13% growth and Lodging +9%. An unexplained surprise was Office, which by early indicators was predicted to show large gains in spending. Two independent sources reported new office starts in 2016 up 25% to 30%. Starting backlog coming into 2017 was near or at an all-time high. Spending was forecast to jumped at least 20% in 2017. Instead, spending posted declines from May to September and is now forecast to finish with only a 4% gain. This market accounts for the single largest miss in my forecast posted in Feb 2017.

The only major nonresidential building in decline this year is Manufacturing. Manufacturing spending was expected to fall in 2017 after peaking in 2015 from massive growth in new starts in 2014. Spending stayed close to that level in 2016. Based on cash flows from starts, spending was expected to decline in 14 of the last 18 months. It declined in 11 of those months. We are at the point of turn-around with only one monthly decline predicted in the next three months and no spending declines expected next year. For 2017, Manufacturing new starts are up 35%.

Nonresidential Buildings starts in the six months from Aug 2016 to Jan 2017 posted the (then) highest amount of new starts since Jan-Jun 2008, also the year Nonresidential Buildings spending peaked. Then new starts in the six months Apr-Sep 2017 just surpassed both those previous peak highs.

Nonresidential Buildings 2018 starting backlog is 50% higher than at the start of 2014, the beginning of the current growth cycle. Starting backlog has increased for five years at an average 10%/year. Spending from starting backlog, up 10% in 2018, increased for five years at an average 9%/year.

Total nonresidential buildings spending in 2018 is forecast to reach $458 billion, an increase of 9.3% over 2017. Office, educational and manufacturing make up 70% of the growth.

Nonresidential Buildings will reach a new high for spending in 2018, surpassing the previous 2008 high. However, adjusted for inflation, spending is 18% below the all-time high reached in 2000.

Non-building Infrastructure Spending

Total non-building infrastructure spending in 2017 drops to $293 billion, down 3.7% from 2016.

Non-building Infrastructure spending, always the most volatile sector, dropped to yearly lows from June through September. Infrastructure construction spending in August dropped to the lowest since November 2014. However, this was predicted. Cash flow models of Infrastructure starts from the last several years show current dips in monthly spending are being caused by uneven project closeouts from projects that started several years ago.

Current backlog is at an all-time high and spending will follow the expected increased cash flows from the elevated backlog. Environmental Public Works (Sewage/Waste disposal down 16%, Water Supply down 9% and Conservation/Dams & Rivers down 7%) posted the largest declines in 2017 and accentuated the declines in the infrastructure sector. The sector is expected to increase slightly in the last quarter 2017. In recent months there are already substantial gains being posted in Conservation and Transportation.

No future growth is included from infrastructure stimulus and yet 2018 is projected to increase by 10%.

Total non-building infrastructure spending in 2018 is forecast to reach $324 billion, an increase of 10.5% over 2017. My forecast for 2018 is predicting every infrastructure market will post gains, but it is the Power and Transportation markets that account for almost all the growth in 2018. Transportation new starts in 2017 grew 120% due to massive new air terminal and rail projects. Spending growth in the Power market is not quite so apparent. Combined Power new starts are down for both 2016 and 2017, but the spending gains are coming from projects that started in 2015, a year in which starts were up over 120%.

Non-building Infrastructure will reach a new high for spending in 2018. This sector had posted a new high in 2015 and nearly equaled that in 2016. Adjusted for inflation, spending in 2018 will be nearly equal to the all-time highs reached in 2015 and 2016.

Public Spending

Total public spending for 2017 remains flat at $287 billion with most major public markets down for the year.

At midyear, I expected Educational and Highway to support a Public spending increase in 2017. Those gains did not materialize. A decline in Highway spending offset small gains in Educational. By far the largest Public spending decline is in Sewer and Waste Disposal, down 16%.

Public spending hit the low for the year in July. It increased for the last three months, most recently by an 11% increase in Public Educational spending in October. We are now near the high for the year and can expect to see another six months of growth before spending levels off in mid-2018.

When you see graphics that present Residential, Nonresidential and Public spending all on the same plot, they are not additive. Only Residential and Nonresidential can be added to reach total spending. Public is a subset of Nonresidential, composed partly of Nonresidential Buildings (~40%) and partly Non-building Infrastructure (~60%), with a slight amount of residential.

The two largest markets contributing to public spending are Highway/Bridge, 32% of total Public spending, and Educational, 25% of Public spending. The third largest market, Transportation, is only about 10% of Public spending. Environmental Public Works combined makes up almost 15% of public spending, but that consists of three markets, Sewage/Waste Water, which accounts for 8%, Water Supply and Conservation. Office, Healthcare, Public Safety and Amusement/Recreation each account for about 3%.

All of Highway/Bridge is Public spending. Only 80% of Educational spending is Public and only 70% of Transportation is Public. Environmental Public Works markets are 99% Public.

Total Public spending in 2018 is forecast to reach $305 billion, an increase of 6.3% over 2017. Public spending in 2018 will reach the highest year over year growth since 2008.

Educational and Transportation will contribute equally and together account for almost 60% of the Public spending growth in 2018. Transportation new starts in 2017 grew 120% due to massive new air terminal and rail projects. Educational new starts total for the last three months posted the highest quarter in at least seven years. The 2nd highest quarter was also within the last 12 months, so still contributes fully to 2018 spending. 2018 signifies a turn-round in Public spending which has not posted significant growth since the recession.

See this companion post for Starts Trends Construction Forecast Fall 2017 11-8-17

After New Starts, dollars are tracked in Backlog, Backlog Construction Forecast Fall 2017 11-10-17

For more on Jobs and Workload see Construction Jobs / Workload Balance 11-7-17

For effects of inflation see Constant Dollar Construction Growth 11-2-17

Starts Trends Construction Forecast Fall 2017

11-8-17

It all starts here! Construction Starts Generate Construction Spending.

2017 construction starts through September total $557 billion Year-to-date (YTD), even with 2016. If/when 2017 gets revised as expected it will then show +3% to +4% growth over 2016, but we won’t see that growth in the revision data until next year.

- Previous year starts always later get revised upwards. Therefore, current year starts ytd growth is always understated.

- Revisions for the period 2012-2015 averaged +4%.

- Revisions to 2016 year-to-date through September are +10%.

- Starts have been increasing at an average rate of 11%/year for the last 5 years.

- Nonresidential Buildings and Nonbuilding Infrastructure are at or near all-time highs.

- Residential starts are at a post-recession high.

- New starts will generate record high 2018 starting backlog for every sector.

Nonresidential Buildings starts, averaged 13%/year growth for the last 4 years, even though there was a 1% decline in 2015. 2017 will post an 8% increase. The 6 months from Aug 2016 to Jan 2017 was the highest period of starts since Jan-Jun 2008, the year nonresidential buildings spending peaked. The 6 months Apr-Sep 2017 just surpassed both those previous peak highs. This will help support increases in nonresidential buildings spending for the next two years.

Infrastructure starts posted a higher value of new construction projects in the 1st 6 months of 2015 than any 6-month period in history. 2016 is down just 2% from the peak 2015 starts and 2016 is the 2nd highest starts on record. Those early 2015 starts will still generate 10% of all spending in 2018. After revisions, 2017 starts may set a new peak high. This would set up infrastructure as the strongest growth sector for the next two years.

Residential starts in 2016 posted the best year since 2005-2006. New starts in 2016 were revised up by 5% to show an increase of 10% growth over 2015. That follows five years of growth averaging 20%/year. Initial values posted for 2017 show starts up by only 3.5%, however, the average revision for the past few years has been +2% to +4%, so 2017 will get revised higher. New starts in Q1 2017 reached an 11 year high.

All construction starts data in this report references Dodge Data & Analytics Starts data.

Care must be taken to use Starts data properly. It is regularly misinterpreted in common industry forecasting articles. Starts dollar values represent a survey of about 50% to 60% of industry activity, therefore Starts dollar values cannot ever be used directly to indicate spending. Also, Starts do not directly indicate changes in spending per month or per year. Only by including an expected duration for all Starts and producing a forecast Cash Flow from Starts data can the expected pattern of spending be developed. Finally, it is the rate of change in Starts Cash Flows that gives an indication of the rate of change in spending.

Cash flow is the best indicator of how much and when spending will occur. Cash flow from DDA starts gives a prediction over time of how spending from each month of previous starts will occur from all projects in backlog. Cash flow totals of all jobs can vary considerably from month to month, are not only driven by new jobs starting but also old jobs ending, and are heavily dependent on the type, size and duration of jobs.

Nonresidential Buildings

Retail/Commercial starts may finish flat or up just slightly for 2017, but that is compared to peak starts in 2016. Starts for the 12 months Aug 2016 – June 2017 posted 10% growth over the previous 12 months. Retail/Commercial starts have been increasing every year since 2010. In 2010, Warehouse starts were only 1/3 of Store new starts. In 2018, Warehouse starts will be 50% greater than Store starts. Warehouse starts have increased between 20%-40%/year for seven years and are now five times greater than in 2010.

Office construction starts have been increasing since 2010 with the strongest growth period of new starts in the 12 months July 2016 – June 2017, the highest 12 months on record, 60% higher than the previous 12 months. That high-volume period of starts is going to elevate spending in both 2018 and 2019 to come in higher than 2017. Office starts averaged year-over-year (YOY) growth of 20%/year for the last five years. Data centers are included in Office.

Educational starts are up 7% in 2017. Starts have averaged YOY growth of 8%/year for the last two years and have had slow but steady growth since 2012. The growth in starts will support growth in spending or the next three years.

Office, Retail and Educational markets comprise 60% of all nonresidential buildings. They are collectively responsible for 70% of the increase in 2017 nonresidential buildings starts.

Healthcare starts have quietly increased to a record high over the last 12 months, up 30% for the 12 months through August vs the previous 12 months.

Lodging starts may be flat or will be up only slightly in 2017, but from 2010 to 2016 averaged over 30%/year growth for six years. In 2018, Lodging may return to that six-year average growth.

Manufacturing is the only nonresidential building market that will NOT finish 2017 with new starts totals at or near post-recession highs. Manufacturing reached record high starts in 2014 and record spending in 2015. However, 2017 will post new starts 50% higher than initially predicted by Dodge.

Manufacturing spending was expected to fall in 2017 after peaking in 2015 from massive growth in new starts in 2014. Based on cash flows from starts, spending was expected to decline in 14 of the last 18 months. It did decline in 11 of those months. We are at the point of turn-around with only 1 monthly decline predicted in the next 3 months and no spending declines expected next year.

Non-building Infrastructure

Sewer/Water/Conservation, the three Environmental Public Works markets, posted declines in new project starts in 3 (sewer) or 4 of the last 4 years. Collectively, new starts in 2017 are the lowest in 5 years. Cash flow predicted from starts has been indicating spending declines since Q2-2016. In fact, spending has declined in 12 of the last 18 months. Cash flow still indicates more spending declines over the next 8 months.

Highway/Bridge/Street starts in the 2nd half of 2014 recorded the slowest rate of growth in the last 6 years. Starts that would normally be contributing spending through 2017 and into 2018 contributed a lower than normal volume of spending which will end in 2017. Had it not been for the extremely high volume of starts in the 1st 4 months of 2014, the most ever recorded in 4 consecutive months, 2017 spending would have dropped more than double the 4% spending decline now forecast.

Highway starts in the 1st 6 months of 2015 posted the next highest growth to early 2014. Spending in 2018 will benefit from those projects that started in 2015 but that have unusually long duration. They will contribute a higher rate of spending in 2018 beyond the duration that typical projects would have ended. It is not recent new starts but old backlog that is influencing 2017 and 2018 highway spending.

Transportation Terminal starts in the first three months of 2017 were more than three times higher than any three-month period in the previous five years. While this helped turn 2017 spending positive, 2017 is still affected by uneven starts from two to three years ago holding down gains in the 2nd half. Transportation will show only a 2% gain in 2017 spending but will post strong double digits gains in 2018 and again in 2019. Terminal buildings is reported in Dodge Starts in Other Institutional Buildings. However Census reports terminal spending in Transportation along with Rail and Dock spending. I adjust the starts data in my reports to conform to the Census construction spending reports.

Power market starts peaked in 2015 at an all-time high, up 142% from 2014 and more than the prior two years combined. The Power market was the prime contributor to the abnormally high infrastructure starts in the 1st 6 months in 2015. Power spending was down 6% in 2015 and up only 3% in 2016 because Power starts were also at an all-time high in 2012, just below the 2015 level, and those starts drove 2014 spending to an all-time high, but then spending from those old jobs tapered off in 2015.

Power starts dropped 11% in 2016 and are down slightly in 2017. Recently, there has been an unexpected large volume of power plant and pipeline starts that are driving 2017 power starts to come in about 40% higher than initially expected.

Even though Power starts have been declining since the 2015 high point, Power had several periods with an exceptionally high value of new starts, some of these periods 2x to 3x the normal rate of growth and a year or two longer duration than typical; late 2014, Jan-May 2015, Feb-Jun 2016 and again in Feb-Jul 2017. A large share of the cash flow, or monthly spending, from all those exceptional starts will occur in 2018 and 2019 and will drive spending to 10%+ gains.

Although starts are not tracked for Public vs Private, Highway, Educational, Environmental Public Works and Transportation make up more than 80% of all Public construction. Only Environmental Public Works starts are down. Educational, Transportation and Highway all have a positive outlook in new starts and predicted spending for 2018 which pushes public spending to post-recession highs.

Here’s how to use the Starts data and how it affects spending Construction Starts and Spending Patterns 9-26-17

Also, after New Starts, dollars are then tracked in Backlog, Backlog Construction Forecast Fall 2017 11-10-17

See the Spending Forecast Spending Summary Construction Forecast Fall 2017 12-2-17

Housing Starts vs Residential Construction Spending

2-18-17

Housing Starts (# of units started as reported by U.S. Census) can be erratic from month to month and short term changes in growth can sometimes be misleading. Trends should be looked at over longer term periods. New monthly starts on a seasonally adjusted annual rate (SAAR) basis for the last eight months through January 2017 have now averaged over 1,200,000. For the last four months starts have averaged 1,250,000. Permits have been following a similar pattern. Although starts versus permits varies considerably in some months, statistically they follow the same growth pattern. Growth in the number of new starts has been 5% to 25% per year due to erratic movement but in the longer term has averaged 18%/yr over six years since January 2011. We experienced an un-sustained start to recovery in 2010, but essentially we went through a protracted bottom between 500,000 and 600,000 new starts that lasted all throughout 2009-2010.

Dodge Data reports SAAR new residential construction starts by contract value in current dollars (not inflation adjusted). Unadjusted growth for the same six-year period increased from $120 billion SAAR to over $300 billion SAAR, or at an annual rate of over 25%/year. However, there was 25% residential cost inflation during that period. In constant 2016$, Dodge new residential starts growth averages 20%/year for six years since January 2011.

Now let’s look at construction spending, actual dollar value of work put-in-place. Here’s where the data has a disconnect.

At the start of 2011, total residential spending had a monthly SAAR of $240 billion and at the end of 2016 was $470 billion, an increase of 16%/year for 6 years. To find real volume growth those values must be adjusted for inflation. After adjusting for inflation, the actual spending volume growth in 2016$ from 2011 through the end of 2016 increased from $305 billion to $465 billion, an increase of 52%, or an average increase of 9%/year for 6 years.

Furthermore, the number of residential construction jobs reported by BLS increased only 33% over that time, an average growth rate of less than 6%/year.

What could explain these differences?

The low rate of jobs growth compared to spending growth is partially explained by the fact that in the preceding few years, even though about 1.5 million jobs were lost, 40% of the workforce, staff was not reduced nearly at the same rate that residential construction volume declined (55%). There remained significantly more staff on payrolls than was needed to complete the amount of volume that was being built during the residential recession. When growth resumed, spending increased at a much faster rate than new jobs were added and the excess labor slack was reduced. I suspect also that a portion of the labor vs spending difference is explained by the fact that not all jobs are captured by BLS. It has been suggested that a large percentage of residential workforce in some southwestern states is undocumented.

The variance between starts and spending is a bit more complicated. We need to look at completions vs starts, the mix and size of housing units being built and the amount of spending related to renovations.

The most commonly reported housing statistic is housing starts. Also in that data series is housing completions. Housing completions are always lower than starts. For the last five years completions have averaged almost 15% less than starts. While the growth in starts averaged 18%/year, growth in completions from 2011 through 2016 averages less than 15%/year.

From 2011 to 2016 the average number of new single family (SF) units started increased from about 450,000 to 800,000. During that same period multi-family (MF) starts increased from 100,000 to 440,000. The percentage of MF units in total construction grew from 18% to 36% of total.

On average MF units are about half the size of SF units. Although the average size of SF homes increased about 10% during this period, the growth in the number of smaller MF units exceeded that of larger MF units by a factor of 2x. The ratio of smaller MF units doubled.

The share of MF units as a percent of all units doubled and the ratio of smaller vs larger MF units doubled. The total square feet of housing being built increased but did not grow at the same rate as the number of units. The average size of all units is getting smaller and therefore the constant cost per unit went down.

I suspect the increased ratio of smaller MF units and the percent increase of MF within the total number of all housing units has a big influence on the overall average cost per unit of total housing. That with the lower growth rate in completions helps explain why spending is not increasing at the same rate as overall number of housing unit starts. We are building more units per dollar spending because average unit size is smaller.

There is one more hidden factor to look at. That is, residential construction spending includes renovations. From 2009 through 2012 renovations totaled 45% of all residential spending. It began to decrease in 2013. For the last three years, renovation spending accounts for only 33% of all residential construction spending. Renovation spending has no comparable # of units or total square feet associated with it.

The impact this has, since the share of renovations spending is declining, is to increase the percent growth in residential spending attributable to housing units to greater than the 9% calculated above. Removing renovations work from total spending shows growth in real inflation adjusted spending specific to housing units averaged about 13%/year for 6 years.

Summarizing everything from above, since 2011:

On the surface it looks like this:

- Housing Starts # of units increased at 18%/year

- Residential new starts in unadjusted dollars increased 20%/year

- Residential construction spending increased 16%/year

After adjusting both units and spending we get:

- Inflation adjusted total residential spending increased 9%/year

- Inflation adjusted spending on units (excluding renovations) increased 13%/year

- Growth in the # of housing units completed increased 15%/year

- Share of Multifamily units has increased

- Average size of multifamily units has decreased

- Average size of all housing units being completed has grown smaller

- The growth in the number of units completed can exceed the growth in spending because the average constant value cost per unit has decreased

The growth in the number of housing unit starts is NOT an indicator to use for forecasting growth in residential construction spending or constant volume. Increases in the number of units alone will not give a realistic indication of growth in residential jobs or spending. The rate of growth in completions, combined with the ratio of the sizes of units, not just size of SF homes but average size of all SF and MF units, has a significant influence on the spending volume and can only be compared to inflation adjusted spending specific to units, that is, total spending minus renovations.

Construction Spending 2016 – Midyear Summary

Summary 2016 Construction Spending

9-7-16

Total Construction Spending for July reached a seasonally adjusted annual rate (SAAR) of $1.15 trillion, level with June which was revised upwards by $20 billion or nearly +1.8%. Monthly spending always gets revised in subsequent months. This year every month but May, which remained nearly unchanged, has been revised upwards, by an average of +1.4% and as much as 3.4%. Monthly values are subject to revision for two months after the first release and once again in May of the following year.

This plot, Construction Spending vs New Starts Cash Flows, shows actual spending (SAAR) by sector through July 2016 and projected trends of spending out to July 2017.

Previously I wrote that we should expect a short duration downturn in spending occurring between January and March. The expected monthly spending cash flows that would be generated from uneven new starts over the last two years indicated that a slowdown in spending would occur during the first quarter 2016. As it turns out, first quarter spending was much stronger than expected, averaging $1.17 trillion SAAR, primarily due to outstanding results in February and March for residential spending. But then April and May experienced significant declines, dropping to an average of only $1.14 trillion SAAR, down almost 3% from Q1. Now with June and July spending both up 1% from the April and May lows, it looks like we may be past that short duration downturn.

Total Construction Spending year-to-date (YTD) through July is up 5.6% over the same seven months 2015. Spending slowed in April and May from a 1st quarter average of $1.17 trillion that reached close to a 10 year high and falls just 4% short of the all-time high. However, it must be noted, that compares unadjusted current dollars, values of all dollars current in the year spent.

When comparing inflation adjusted constant dollars, all dollars adjusted to the same point in time, we can see 2016 spending is still 18% below the 2006 highs.

Total spending YTD through July is slightly ahead of what I predicted back in December, but it’s slightly below what I expected for May, June and July . I expect 2nd half spending to average above $1.2 trillion SAAR, but slightly lower than I originally forecast.

I’ve revised my 2016 spending forecast down slightly to total $1.190 trillion, up 7% from $1.112 trillion in 2015.

How does actual spending YTD compare to my prediction at the beginning of the year?

- Total predicted YTD through July $638.2b, actual YTD $647.7b (+$9.5bil, +1.5%).

- Residential predicted YTD $245.1b, actual YTD $259.2b (+$14.1bil, +5.8%).

- Nonresidential Bldgs predicted YTD $236.9b, actual YTD $228.1b (-$8.8bil, -3.7%).

- Non-building Infrastr predicted YTD $156.2b, actual YTD $160.5b (+$4.3bil, +2.8%).

Where are the revisions?

The single largest reduction in spending is in Nonresidential Buildings Manufacturing. Although there are other variances, that could account for the entire revision downward. Predicted construction starts for Manufacturing was lowered by nearly 35% after the initial start-of-year forecast was made.

Non-building Infrastructure spending increase is being supported by a 20%+ increase in power, which I didn’t expect. New starts for power projects have increased more than 20% since the initial forecast.

Residential construction had unusually large gains in February and March, almost all of that in residential renovations, offset only partially in April through July by declines mostly in new single-family housing.

Here’s my revised 2016 spending forecast based on YTD spending and new construction starts through July, compared to my prediction in December 2015.

- Total predicted Dec 2015 $1,206.2b, July 2016 $1,189.9b (-$16.3bil, -1.4%).

- Residential predicted Dec 2015 $473.8b, July 2016 $481.8b (+$8.0bil, +1.7%).

- Nonresdntl Bldgs predicted Dec 2015 $439.2b, July 2016 $410.9b (-$28.3bil, -6.4%).

- Non-bldg Infrastr predicted Dec 2015 $293.2b, July 2016 $297.3b (+$4.1bil, +1.4%).

Spending and construction starts are often confused by some analysts who refer to starts data as spending. Starts represent total project value recorded in the month the project begins. To determine spending activity, starts values must be spread out over the duration of the projects. Spending is dependent on cash flows each month generated from all previous construction starts. Cash flows expected based on Dodge Data construction starts are indicating a return to growth in spending in the 2nd half 2016. (See chart above Index Actual Construction Spending vs New Starts Cashflows).

Spending Breakout by Sector

Residential construction spending for July totaled a SAAR of $452 billion, remaining near level for the last four months. Residential spending YTD through July is up 6.5% over 2015. Spending slowed in April and May from a very strong 1st quarter average that reached close to a 10 year high. The current 3-month average is just 1% below the 1st quarter and is still at its highest since the 2nd half of 2007 but is 10% below the current dollar all-time high in 2006. I’m still expecting some upward revisions to June or July residential spending.

Residential spending just experienced the strongest three-year stretch of spending growth on record, up 60% in 2013-2014-2015. After taking out inflation, volume growth was only 31%, but that is still the strongest ever for three consecutive years. Spending growth in 2016 will reach only +9%. After adjusting for inflation that represents volume growth of less than +4%, the slowest in 5 years. New starts YTD (as reported by Dodge Data) although down from the 1st quarter, are still near post-recession highs. Starts from late 2015 and early 2016 will still be generating spending into early 2017. 2017 will repeat nearly identical to 2016. What we may be seeing is that it might be difficult to register another year of very high percentage growth in 2016 or 2017 because it is being measured against the 2015 10-year high. Another factor limiting very high growth may be a limited supply of labor to expand the workforce.

Total Nonresidential SAAR spending for July is $701 billion, down slightly from June, but monthly SAAR has varied only +/- 1% for the last six months. YTD spending compared to 2015 is up 5.1%. Nonresidential spending also slowed in April and May but is now up 1.5% from those lows. The current 3-month average is up slightly from the 1st quarter and is just 3% below the pre-recession 2008 current dollar high.

Nonresidential Buildings spending for July totaled a SAAR of $403 billion, down slightly from June but up 1.3% from the May dip. Spending YTD for nonresidential buildings through July is up 8.0% over 2015. The current 3-month average of $403 billion is up slightly from the 1st quarter but is still 9% below the peak in 2008.

Non-building Infrastructure spending for July fell to a SAAR of $289 billion, down only slightly over for the last four months. YTD spending through July is up only 1.3% over 2015. Spending began to slow in April and May and is now at the 2016 low. The current 3-month average is down 4% from the 1st quarter. However, spending on nonbuilding infrastructure reached an all-time high in the first half of 2014 and has remained near those highs through 2015 into the 1st quarter of 2016.

9-7-16

Public spending average for the 1st six months of 2016 is the highest since 2010 and is up 10% from the 2014 low point. YTD public spending is up 0.2% from 2015. All of Highway plus 80% of Educational makes up 55% of all public construction spending. The next largest markets, all of Sewage/Wastewater plus 70% of Transportation accounts for only 19% of public sending. All other markets combined make up less than 20%.

The biggest mover to total public spending this year is educational spending. Public educational spending is up only 4.0% YTD, but because it represents almost 25% of all public spending, it’s has a bigger net impact of +1.0% on moving the trend up than any other single public market. Public commercial spending is up 36.6% YTD but has only a 1% market share of public work. Highway and street is up 2.6% YTD. At 30% of total public that results in a net move of +0.8%. Office, public safety, power, sewage/waste disposal and water supply are all down YTD by a combined -5.3%. At a combined market share of 21% that nets a -1.1% reduction in YTD public spending.

Private spending is dominated by a 52% market share of residential work. At 6.6% growth that nets 3.4% growth in private spending. Several of the nonresidential building markets have high YTD growth (and/or a large market share of private work); lodging +30%, office +27%, Amusement +22%, commercial +10% and power +8%. These five markets combined represent 29% of private spending and combined are up +15% YTD for a net impact of +4.4% to private work.

For a base of reference, here’s a few points in spending history.

Total Construction Spending

- 8 years 1998-2005 up 77%

- 3 years 2003-2005 up 32%

- 3 years 2008-2010 down 30%

- 4 years 2012-2015 up 41%

Residential

- 8 years 1998-2005 up 133%

- 3 years 2003-2005 up 57%

- 3 years 2007-2009 down 60%

- 3 years 2013-2015 up 60%

Nonresidential Buildings

- 5 years 2004-2008 up 64%

- 3 years 2006-2008 up 45%

- 3 years 2009-2011 down 36%

- 2 years 2014-2015 up 25%

Non-building Infrastructure

- 7 years 1995-2001 up 56%

- 4 years 2005-2008 up 60%

- 3 years 2009-2011 down 8%

- 3 years 2012-2014 up 19%

See this post for expanded details on Construction Spending – Nonresidential Markets – Buildings and Infrastructure

See this post for expanded details on Construction Inflation

Construction Spending vs Dodge Starts vs New Housing Unit Starts

Read my last few blogs and all of this is detailed, but this is worth a look.

Dodge Data Construction Starts cash flowed shows a predicted spending pattern.

Actual spending is shown to compare to the prediction.

For another residential input we have new housing starts. Here I’ve spread activity out from start to completion like a cash flow to get monthly activity. History compares to actual spending and future compares to Dodge New Starts cash flow.

The time flow of activity generated by housing starts is much more important than the monthly starts themselves. It prompts us to look at a much longer term trend of housing starts than just whether they have moved up of down in the last month or quarter.

Modeling for nonresidential buildings and non-building infrastructure appears more accurate than residential. It looks like my prediction of cash flow from Dodge residential starts needs to move 2-4 months to the left.

5-4-16 The cash flow plot for residential has been revised to use a different duration for SF vs MF vs Reno.

Residential Work Flow From Housing Starts

Housing starts can be erratic. It’s not unusual to see monthly housing starts fluctuate up or down by 10%, sometimes 20%. But what affect does this have on the flow of housing work? Not as much as you might think.

Although housing starts is in units, not dollars, we can create a “cash flow” to see how the new starts generate activity over future months. To see the flow of work I’ve created a simple time flow of starts to show the activity generated for new housing starts.

About 2/3rds of housing starts are single family units. These might have a construction duration ranging from 6 to 9 months. The remaining 1/3rd of starts are multifamily units. Those could have construction duration of anywhere from 8 months to 16 months and in some cases longer. For this simple analysis I’ve used a work flow duration of 2/3rds at 7 months and 1/3rd at 17 months. Varying the duration longer or shorter by a few months will not have a big effect on the outcome. It changes the slope of the growth rate but does not change the consistency of the growth pattern.

A time flow of housing starts shows growth rates of; 2013 +13%; 2014 +10%; 2015+12%. Actual construction spending shows growth of 2013 +19%; 2014 +14%; 2015+13%.

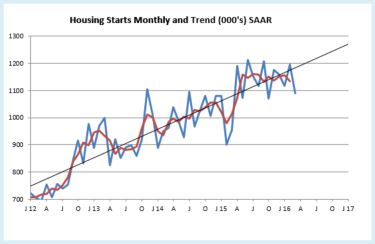

The chart above, “Housing Starts Monthly and Trend” shows the actual monthly starts values and a three month moving average. Monthly starts periodically peak and dip erratically. Look at February 2015, the biggest dip in 5 years. The 1st quarter 2015 was down 7% qtr/qtr. But then notice it took less than 4 months for starts to come right back to the trend line and the trend remained intact. 2015 finished up 11%. This is how the monthly housing starts (# of units) data goes.

The “Work Flow” chart plots the actual work load out over time from the month the work started to completion. The total work flow in any given month is the sum of the work contributed from starts in previous months that have yet to be completed. Residential work flow has averaged +12% for the last 3 years. In 2015, growth was 14%. The very steep climb in early 2013 activity reflects work generated from the 28% rise in new starts in 2012, the largest % increase in new starts in 30 years.

Starts in any given month have only a small % impact on the slope of change in every succeeding month until completion. This is the same concept as cash flow. Construction spending in any given month is the sum of all the ongoing projects from all previous months.

This next plot shows the same workflow, only Not Seasonally Adjusted, so it shows the winter dips in activity and the steeper rate of growth during the more productive months. Although the average slope of growth is similar to the SAAR plot, this shows the real total work activity in any given month varies from that shown by the SAAR plot. However, it is not erratic like the starts plot, it is smooth and repetitive year after year.

It would take a dramatic change in housing starts to significantly alter the progress of work flow and it would need to be a sustained change in starts. If a 20% decline is offset by an corresponding increase in the following month or months, then the future months of work flow will show little affect from the decline.

What Drives Construction Spending?

3-23-16

New construction starts drive construction spending. For all the discussion regarding the monthly rise and fall of spending, most of the spending in any given month is already predetermined since two thirds of all construction spending in the next 12 months comes from projects that were started prior to today. This is commonly referred to as backlog.

The pattern of spending does not follow the pattern of new starts which can fluctuate dramatically. It follows the pattern developed by the cashflow from all previous starts. Data for new construction starts is sourced from Dodge Data & Analytics. Cash flow is developed independently. Here’s a much simplified example of cashflow: a new $20 million project start is to be completed in 20 months, therefore we expect this project to generate $1 million of spending every month for the next 20 months.