Construction Inflation Cost Index

Note: The post you’ve reached here was originally written in Jan 2016. For the latest information follow this link to the newest data on Inflation. 8-15-19

ESCALATION / INFLATION INDICES

Thank You. edz

Jan. 31, 2016

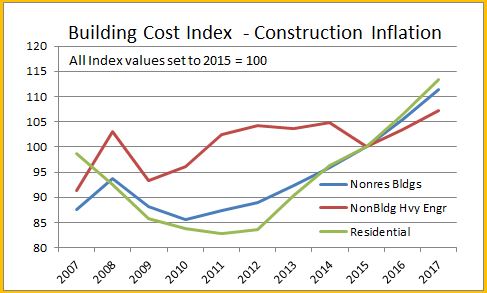

Construction inflation for buildings in 2016-2017 is quite likely to advance stronger and more rapidly than some estimators and owners have planned.

Long term construction cost inflation is normally about double consumer price inflation. Construction inflation in rapid growth years is much higher than average long-term inflation. Since 1993, long-term annual construction inflation for buildings has been 3.5%/yr., even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8%/yr.

For the period 2013-2014-2015, nonresidential buildings cost indices averaged just over 4%/yr. and residential buildings cost indices average just over 6%/yr. I recommend those rates as a minimum for 2016-2017. Some locations may reach 6% to 8% inflation for nonresidential buildings but new work in other areas will remain soft holding down the overall average inflation. Budgeting should use a rate that considers how active work is in your area.

Infrastructure projects cost indices on average have declined 4% in the last three years. However, infrastructure indices are so unique that individual specific indices should be used to adjust cost of work. The FWHA highway index dropped 4% in 2013-2014 but increased 4% in 2015. The IHS power plant cost index gained 12% from 2011-2014 but then plummeted in 2015 to an eight year low. The PPI industrial structures index and the PPI other nonresidential structures index both have been relatively flat or declining for the last three years.

These infrastructure sector indices provide a good example for why a composite all-construction cost index should not be used to adjust costs of buildings. Both residential and infrastructure project indices often do not follow the same pattern as cost of nonresidential buildings.

Anticipate construction inflation of buildings during the next two years closer to the high end rapid growth rate rather than the long term average.

Overtime Isn’t Always What It Seems – Lost Productivity Construction

1-30-16

It is sometimes necessary when the situation dictates to increase working hours to achieve a shortened schedule. However, numerous studies can be found to support that Overtime results in lost productivity. There are other factors that affect productivity, but just to address the topic of Overtime, for the moment they will be ignored. This productivity loss set of data is from Applied Cost Engineering, Clark and Lorenzoni, Marcel Dekker, Inc., 1985.

As both hours and number of days worked increases over 5 days and 8 hours, productivity declines. 5 days and 8 hours is considered the norm = 0% productivity loss. Any increase in hours or days above this norm reduces productivity. All values approximate and % loss is loss of production on ALL hours worked.

5 days and 8 hours = 40 hrs @ 0% productivity loss = 40 hrs productive

5 days and 10 hours = 50 hrs @ 7% productivity loss = 46.5 hrs productive

5 days and 12 hours = =60 hrs @ 12% productivity loss = 53 hrs productive

6 days and 8 hours = 48 hrs @ 3% productivity loss = 46.5 hrs productive

6 days and 10 hours = 60 hrs @ 17% productivity loss = 50 hrs productive

6 days and 12 hours = 72 hrs @ 25% productivity loss = 54 hrs productive

7 days and 8 hours = 56 hrs @ 7% productivity loss = 52 hrs productive

7 days and 10 hours = 70 hrs @ 20% productivity loss = 56 hrs productive

7 days and 12 hours = 84 hrs @ 28% productivity loss = 60.5 hrs productive

Not only does overtime produce lost hours, but the cost of the overtime hours increases. Hours over 8 might cost 1.5x normal rate. Days over 5 might cost 2x normal rate. Increasing days and hours rapidly balloons the cost of completing the work. However, if absolutely necessary to meet unusual schedule demands, the cost vs time to complete work can be modeled for each scenario and the least destructive option (whether that be cost constrained or time constrained) can be agreed upon by all parties. The best choice is always that which requires the minimum added cost to achieve the restricted schedule.

See this blog post for an example Construction Overtime – A Common Miscalculation

IF Another Recession, What Would Happen to Construction?

8-15-19 See WHAT IF? Construction Recession 2020

1-27-16

The wheels of construction turn slowly.

There is plenty of talk these days of whether or not we may slip into another recession. On any given day you can read several articles pointing to why or why not we are headed into another recession. I’m not trying to take a position here. I would like to get a rough idea what would happen to this current construction recovery if we do slip into recession.

A starting baseline for this discussion is my forecast for 2016; total spending up 10%. nonresidential buildings up 14% after a 17% increase in 2015, residential up 12% following 13% in 2015 and non-building infrastructure up 1% for a total less than 2% in 2015-2016. So, you can see I’m not predicting a recession.

If you think of a recession as having an immediate affect on total construction, like a quick drop in materials prices or cost of buildings, think again. Construction is sort of like an aircraft carrier, it takes a long time to turn around.

The best indicator of future construction activity is the projected cash flow generated by all the construction starts that have been recorded. Construction starts represent the beginning of spending on new projects. Projects can take many months to reach completion. Some portion of the total project spending occurs in every month over the full duration of the project from start to completion.

We start 2016 with a backlog of projects that will generate about 70% of all the cash flow in 2016. It’s likely that most if not all of the projects already started would move on to completion. But new starts will be cut back.

To get an idea how another recession might affect construction spending, I kept all backlog as is but I reduced future new construction starts for the next two years (2016 and 2017) by 30% for residential and nonresidential buildings, and 15% for infrastructure projects. This mimics the declines we experienced from 2006 to 2009. I then allowed for a 5% increase across all sectors in 2018.

The result is a 5% drop in construction spending in 2016, still higher than 2014, but then a 10-15% drop in 2017 setting us back to near the same level as 2013.

These spending declines would cause a temporary loss of about 400,000 to 500,000 jobs.

Nonresidential buildings could still eke out a slight gain in 2016 but would drop 20% in 2017. Residential construction would drop about 5% in 2016 and then drop another 10-15% in 2017. Nonresidential infrastructure work would decline 10% in 2016, but then rebound to no change in 2017.

After two years of declines, in 2018 nonresidential buildings would climb back to near even with 2017, residential would grow 5% and infrastructure would remain flat. Total 2018 spending would climb only 2% over 2017 and would still only reach spending in 2013.

So, a 30% decline in activity for two consecutive years starting today would set us back four to five years, but the major affect would not be felt until 2017. If that were to happen, obviously spending would be revised, but also I would have much different predictions for inflation and jobs.

There’s a reason we see the dips and rises on the chart in both 2016 and 2017. It reflects the decline in the rate of new starts plus the remainder of old backlog finishing at varying end-dates. Also, given a constant amount of seasonally adjusted new starts, there is a difference in the actual amount of starts in winter months vs summer months. This plays out over time as dips and rises in spending. Spending activity will not be smooth in a recession.

What Did He Say? Fact Checker – Track Record

MY TRACK RECORD

Indoor Masters National Track Championships

masters age group 45-50

Mile – 4:41.7 – 4th place

3000m – 9:25.3 – 3rd place

Oh, wait. That’s not what you are here to read. You want my track record on construction economic forecasts. How good are my forecasts? Do they prove to be accurate? How do they compare to the rest of the industry forecasts? OK. Let’s have a look.

- Bullets show what I forecast.

This is what actually occurred. Actual is in red if I got it wrong.

From Jan 2013

- The ABI, McGraw Hill Dodge new starts and the Dodge Momentum Index (DMI) are all indicating a dip in nonresidential spending potentially from February through May 2013.

- Architecture Billings Index (ABI) went UP from May 2012 to January 2013 with only December down slightly (see figure B). This is a very good leading indicator for new construction work starting in Q3-Q4 2013.

- I expect a dip in nonresidential buildings work between January and May 2013, at which point all indicators point to sustained growth through year end.

From February 2013 through June 2013 actual spending on nonresidential buildings dropped by 2%. Then from June through November spending increased by 6%.

From Jan 2013

- As spending continues to increase, contractors gain more ability to pass along costs and increase margins. However, contractors almost always are playing catch-up. In the most recent three-month period, contractors’ costs began to climb faster than whole building costs went up, due to both increasing material costs and declining productivity.

- Once growth in nonresidential picks up and both residential and nonresidential are active, we will begin to see apparent labor shortages and productivity losses.

For 2013 and 2014 construction spending increased 7% and 10%. During that 2 year period, total labor and materials inputs increased only 2% to 3%, but construction inflation measured 4.5%. Margins increases drove up the total inflation cost. Available (nonworking) workforce declined to about 400,000, near the lowest on record. Productivity declined by 2%.

From Jan 2013

- Construction Spending for 2013 will be pushed higher by huge growth in residential construction, a rate of spending growth that increased by 30% from Q1 to Q4 2012

Residential spending in 2013 grew at a rate of 1.5% per month, largest one year growth since 2004.

From Jan 2013

- The National Association of Home Builders consensus estimate for new residential units is growth of 23% in 2013 and 33% in 2014. 2012 grew by 28%.

- The NAHB projections are for an increase of 150,000 units in 2013 and 230,000 in 2014, 20% and 27% growth the next two years. There’s a possibility we could achieve that. But, especially in 2014, that would exceed the fastest growth rates, both volume and total jobs, achieved in the last 30 years.

- Mark Zandi, economist for Moody’s, in the same article is quoted as saying his more optimistic forecast has residential construction growing to 1.1mil in 2013 and 1.7mil new housing starts in 2014, growth of 46% and then 54%. I say NO WAY

- A more reasonable projection is new housing starts may reach 850K to 900K in 2013 and 1.0 to 1.05 million in 2014, new homes growth rates of 15% to 20% and total residential spending growth of 12% to 15%. That still has the workforce expanding rapidly, but at least at a not unheard of rate.

Housing starts reached 925,000 in 2013 and 1,003,000 in 2014, well below the 30 year historical annual growth.

From Jan 2013

- Future escalation, in order to capture increasing margins, will be higher than normal labor/material cost growth. Lagging regions will take longer to experience high escalation.

- I’m advising a range of 4% to 6% for 2013, 5% to 7% for 2014 and 6% to 8% for 2015.

- Expect residential escalation near the upper end of the range.

Actual total construction cost inflation 2013 = 4.3%, 2014 = 4.7% 2015 = 2.9%. All inflation values were held to lower totals due to infrastructure work which did not have more than 2% inflation during that period and actually experienced deflation in 2015. Residential buildings inflation for 2013-14-15 was 8.9%, 7.1% and 4.1%.

Posted April 2014

- Construction Spending “residential buildings” expect $379 billion in 2014

- Construction Spending “nonresidential buildings” expect $325 billion in 2014

- Construction Spending “totals” expect $960 billion in 2014

Posted August 2014

- Construction Spending “residential buildings” expect $365 billion in 2014

- Construction Spending “nonresidential buildings” expect $314 billion in 2014

- Construction Spending “totals” expect $961 billion in 2014

2014 Residential spending = $354 billion

2014 Nonresidential spending = $320 billion

2014 Total Construction spending = $960 billion

These values prior to U.S. Census major correction to data.

Posted August 2014

- If you are pricing future construction jobs the way you always have, with 2-3 pct escalation, you are already in trouble!

- If you’re an owner with plans to construct a building in the future and you are inflating cost by only 2-3 pct, you’ve missed the boat.

Total construction inflation for 2013-14-15 was 4.3%, 4.7% and 2.9%. All years were reduced by a lack of inflation in infrastructure work. Inflation for nonresidential buildings was 3.5%, 4.2% and 4.8%. Residential buildings inflation was 8.9%, 7.1% and 4.1%.

Posted September 2014

- Real Construction Volume in 2014 (construction spending minus inflation) will grow less than 2 percent

Real construction volume in 2014 increased 4.9%. Commercial nonresidential construction started it’s current boom.

Posted Dec 2014

- Construction Spending “residential buildings” expect $405 billion in 2015

- Construction Spending “nonresidential buildings” expect $364 billion in 2015

- Construction Spending “totals” expect $1,040 billion in 2015

Posted Jan 2015

- Cash flow of new starts for nonresidential buildings indicates a 15% increase in the monthly rate of spending over the next 10 months.

- Both ABI and Starts cash flows indicate a mild slowdown in nonresidential buildings construction spending at the end of 2014 before a strong upturn in spending in 2015. Expect another drop in spending late in 2015

For the period Nov 2014 through Feb 2015, spending on nonresidential buildings stalled flat for 4 months. The monthly rate of spending increased 14% over the 10 months from Oct 2014 to September 2015. Since Sept 2015 spending has been flat.

Posted March 2015

- Even if new starts turn flat for rest of 2015, starts already recorded are indicating Nonresidential buildings construction spending for 2015 will reach 15%+ growth. My closest competitor is forecasting 12.5% growth. The average of all other industry forecasts is 8% growth.

Spending for nonresidential buildings actually hit +17% growth over 2014.

Posted July 2015

- Construction Spending “residential buildings” expect $388 billion in 2015

- Construction Spending “nonresidential buildings” expect $397 billion in 2015

- Construction Spending “totals” expect $1,067 billion in 2015

2015 Residential spending = $390 billion

2015 Nonresidential spending = $387 billion

2015 Total Construction spending = $1068 billion

These values prior to U.S. Census major correction to data.

Posted July 2015

- Nonresidential Buildings spending growth 2015 vs 2014.

- My forecast (Average all others) [closest competitor]

- Educational 7.1% (3.8%) [5.6%]

- Healthcare 6.0% (3.9%) [4.0%]

- Commercial/Retail 5.5% (11.8%) [8.4%]

- Lodging 24.0% (13.7%) [17.1%]

- Office 21.1% (13.5%) [19.2%]

- Manufacturing 49.6% (15.9%) [24.6%]

Educational 6.7%

Healthcare 4.6%

Commercial/Retail 8.4%

Lodging 30.8%

Office 21.9%

Manufacturing 47.3%

So there you have it. Several years of forecasts and how they turned out. You can get an idea of my track record. You be the judge. 🙂

Construction Forecast 1st Look – What To Expect in 2016?

Construction spending may reach historic growth in 2016.

There are currently six estimates available forecasting 2016 total construction spending ranging from 6% to 10% growth, with an average of 8.7%. My forecast is 9.7%.

Total construction spending, forecast to grow 9.7% in 2016, could reach a total 30% for the three years 2014-15-16. The only comparable periods in the last 20 years are 29% in 2003-04-05 and 27% in 2013-14-15.

The current nonresidential buildings construction boom could become an historic expansion. Nonresidential buildings spending is forecast to grow 13.7% in 2016. Added to 8.8% in 2014 and 17.1% in 2015, the three-year total growth could reach 40% for 2014-15-16. The only comparable growth periods in the last 20 years are 40% in 2006-07-08 and 32% in 1995-96-97.

For perspective, residential spending increased 46% in 2013-14-15, similar to only one comparable period in the last 20 years, 48% in 2003-04-05.

Non-building infrastructure projects, in two of the last three years have barely shown any gains entirely due to declines in power plant projects. This will repeat in 2016.

This is still the 1st or 2nd most active 3 year period of growth in construction in more than 20 years, and it’s already been ongoing since 2013-2014. With the forecast for 2016, spending growth could reach a new three-year high.

From the middle of Q1 2016 to the end of Q3 2016, total spending will post six to eight months at an annual growth rate of 20%, but due to the dips at the beginning and the end of the year, total 2016 construction spending will finish at 9.7% growth. Construction spending momentum is not yet losing steam. We may be seeing the effects of a few years of erratic growth patterns and a shift from more rapidly changing commercial and residential work to slower growth institutional work.

Residential spending will slow several percent early in 2016 before resuming upward momentum to finish the year with 12% growth, slightly less than growth in 2014 and 2015. Periods of low new start volumes need to work their way thru the system and this produces growth patterns with periodic dips. The upward momentum will carry into 2017.

Nonresidential buildings spending will slow moderately in the next few months before we see a 15% growth rate through the middle of the year, only to see another slowdown late in 2016. Major contributions are increasing from institutional work in educational and healthcare markets. Office, commercial retail, lodging and manufacturing will decline considerably from 2015 but still provide support to growth.

Infrastructure projects spending will decline over the next six months due to the ending of massive projects that started 24 to 42 months ago. There will be large advances in spending midyear before we experience another slowdown later in 2016. Following a 0.5% increase in 2015, spending will increase only 1.2% in 2016, held down by a 10% drop in power projects, the second largest component of infrastructure work.

Construction added 1.0 million jobs in the five years 2011-2015. 800,000 jobs were added in the last three years. To support forecast spending, jobs need to grow by 500,000 to 600,000 in 2016-2017. Growth in nonresidential buildings and residential construction in 2014 and 2015 led to significant labor demand which has resulted in labor shortages in some building professions. Demand in 2016-2017 will drive up labor cost and may slow project delivery.

Spending growth, up 35% in the four-year period 2012-2015, exceeded the growth during 2003-2006 (33%) and 1996-1999 (32%) which were the two fastest growth periods on record with the highest rates of inflation and productivity loss. Construction spending growth for the period 2013-2016 is going to outpace all previous periods.

Construction inflation is quite likely to advance more rapidly than some owners have planned. Long term construction cost inflation is normally about double consumer price inflation. Construction inflation in rapid growth years is much higher than average long-term inflation. Since 1993, long-term annual construction inflation for buildings has been 3.5%, even when including the recessionary period 2007-2011. During rapid growth periods, inflation averages more than 8%.

For the last three years the nonresidential buildings cost index has averaged just over +4% and the residential buildings cost index just over +6%, however, the infrastructure projects index declined. The FWHA highway index, the IHS power plant index and the PPI industrial structures and other nonresidential structures indices have all been flat or declining for the last three years. This provides a good example for why a composite all-construction cost index should not be used to adjust costs of buildings. Infrastructure project indices often do not follow the same pattern as cost of buildings.

Anticipate construction inflation of buildings during the next two years closer to the high end rapid growth rate rather than the long term average.

2016 Construction Outlook Articles

Articles Detailing 2016 Construction Outlook

Links will open in a new tab

These links point to articles here on this blog that summarize end-of-year data for 2015 and point to articles with projections for 2016.

Most Recently Published

Summary of 2017 Construction Outlook 2-21-17

How Much Does A Steel Cost Increase Affect Construction? 9-18-16

2015 Results

Construction Spending 2015-2016 – How Do The Forecasts Compare? 12-9-15

Construction Spending 2015 and 2016 11-9-15

Construction Spending Market Performance of Nonresidential Bldgs 2015-2016 10-15-15

New Starts and 2016 Starting Backlog

Construction Backlog 2017 3-20-17

New Construction Starts Leading Into 2017 1-24-17

Behind The Headlines – Construction Backlog 1-16-17

Starts Point to Robust 2017 Spending 10-20-16

New Construction Starts Much Better Than Might Appear 9-23-16

Spending Forecast

Forecast 2017 Construction Spending 1-7-17

2016 Construction Spending year end 1-3-17

Are We at New Peak Construction Spending? 1-4-17

Construction Spending Gets Revised UP 10-6-17

Construction Spending 2016 – Midyear Summary

1st Quarter 2016 Construction Spending and Forecast

Construction Forecast 1st Look – What To Expect in 2016? 1-14-16

Erratic Pattern Ahead for 2016 Construction Spending. Why?

Nonresidential Buildings

Construction Spending 2016 – Midyear Nonresidential Markets

Updated 1-23-16 Forecasts of 2016 Nonres Buildings Construction Spending % Growth

Construction Spending Market Performance of Nonresidential Bldgs 2015-2016 10-15-15

Residential

Construction Spending vs Dodge Starts vs New Housing Unit Starts 4-27-16

Residential Work Flow From Housing Starts 4-25-16

Housing Starts > Look a Little Deeper 11-18-15

Claryifying Housing Starts Numbers 11-6-15

Residential Construction – Not All Data Tells The Same Story 10-25-15

Infrastructure Outlook

Infrastructure – Ramping Up to Add $1 trillion 1-30-17

Infrastructure Outlook 2017 1-12-17

Calls for Infrastructure Problematic 1-12-17

Saturday Morning Thinking Out Loud #1 – Infrastructure 10-29-16

Public Construction

Infrastructure & Public Construction Spending 3-5-17

Public Construction Spending 2016-2017 10-21-16

Jobs

Construction Spending vs Jobs 2-9-17

Behind The Headlines – Construction Jobs 2-16-17

Construction Jobs Show 3rd Qtr Growth 10-7-16

How Many Construction Jobs Needed to Support 2016-2017 Spending Forecast? 1-12-16

Inflation

How Much Does A Steel Cost Increase Affect Construction? 9-18-16

Construction Inflation Cost Index 1-31-16

How Many Construction Jobs Will Be Needed to Support 2016-2017 Spending Forecast?

1-12-16

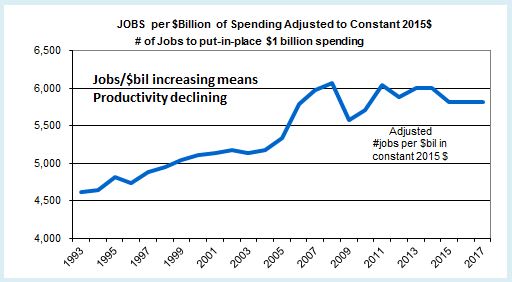

This is a pretty straight forward analysis. If productivity is to remain the same, then jobs need to grow by the same percentage as volume. If volume grows faster, then productivity increases. If jobs grow faster, then productivity declines. Let’s have a look at the numbers to find out what’s been going on and where we might be headed. Spending forecasts will give the basis for predicting jobs growth.

A few weeks back I commented on a study published by Bureau of Labor Statistics on how many construction jobs would be created by 2024. BLS Says +790,000 Construction Jobs by 2024. Let’s Look Behind The Headlines. Now that I’ve completed updating spending and jobs data and developed a forecast for 2016-2017, I will show what has taken place over the last 4 years and what to expect for the next two years.

Here’s what we know.

Volume is not the same as construction spending. Spending is the number nearly everyone follows. Volume is spending minus inflation. I use composite inflation factors based on tracking numerous construction selling price indices.

In 2015 nonresidential buildings spending grew by 17%, but after inflation, volume grew by only 12%. Overall construction spending in 2015 grew by 11%. Total all construction volume grew by 8%. Annual construction inflation varies for residential, nonresidential buildings and nonresidential infrastructure.

For the four years 2012 through 2015 construction spending grew by 35% but after inflation volume grew by 21%.

Work output grows by number of new jobs added and by any increase in total hours worked. For the four years 2012 through 2015 construction jobs increased from 5.5 million to 6.4 million, or 16%. In addition hours worked by the entire 6 million workforce increased by 2%. So effectively, total workforce output increased by 18%.

The last four years volume grew 21% and the effective number of jobs grew 18%. There was an increase in productivity over this four year period of 3%. An increase in productivity occurred because we put-in-place more volume than the (effective) number of jobs added.

Now we can ask the question, “How many construction jobs will be added in the next two years if we achieve the spending forecast?”

Let’s use what we know and apply it to the forecast.

I’m forecasting 10% spending growth in 2016 and 12% in 2017. I anticipate higher inflation than we have experienced in the last few years. After inflation, volume should grow 4% and 6%. So, total volume growth for the next two years is forecast 10%.

With rapid growth, I would expect productivity to decline slightly, but the last 4 years of growth showed a slight productivity gain, so let’s go with that. That means we will lower our estimate of jobs needed because some of the increased volume over the next 2 years will be supported with increased productivity.

Total volume growth for the next two years is forecast at 10%. If we follow the same pattern as the last 4 years, we may see an increase in productivity of 2%. So we need only an 8% increase in workforce output to put-in-place the forecast volume. The average number of jobs for 2015 is 6.4 million. An 8% increase in 2 years on the 6.4 million means we need to add 512,000 jobs in 2016-2017.

If we do not see gains or losses in productivity we need to add 10% to jobs, the same percentage jobs as we have volume growth. That would be 640,000 new jobs in 2016-2017.

As a result, based on this analysis expect a need of about 500,000 to 600,000 new construction jobs in the next two years.

For comparison, in 2014-2015, 601,000 new jobs were added. Then, spending grew 20% but volume after inflation was 12%. Jobs grew by 10%.

Jobs have increased more than 600,000 in two adjacent years only a few times. Any two years within 1996-1998 were over 600,000, also 83-84 and 93-94. The highest ever was 1998-99 when we added 770,000 new jobs, and that two year period had the same total jobs as 2014-2015. The only other recent high periods are 2004-05 added 700,000 and 2014-15 added 601,000.

Also, it’s easy to see now, had this been based on total spending increases for the two years rather than volume, the need would be 20+% or 1.0 to 1.2 million jobs, not just the 8% or 10% jobs growth used here. The last time jobs grew by more than 10-12% in two years was 1977-1978 at 18% and the highest growth ever was 770,000 jobs added in 1998-99, the only time over 700,000. So, as expected, 20+% growth and a million jobs in two years has never been reached.

BLS predicted construction will add 790,000 jobs over 10 years, the period from 2015 through 2024. In 2015 we’ve already gained 260,000 jobs so that would leave 530,000 new jobs expected over the remaining 9 years.

The spending forecast and past job growth patterns indicate that we will add far more jobs and much faster than is predicted by BLS.

Of course, another recession would alter this, but this is not based on another recession.

Welcome to the New Year. What’s Up With Construction?

It’s been about two weeks since I wrote a blog post. With good reason. I’ve spent the last few weeks working sometimes 10 or 12 hour days getting all the information for and writing a construction economics report. Coming soon!

Here’s a few tidbits out of the mass.

The nonresidential buildings construction boom that is going on right now could become an historic expansion. I’m predicting 13.7% growth in 2016. Added to 8.8% in 2014 and 17.1% in 2015 that could be 39.6% growth in 3 years 2014-15-16.

Only 3 year periods back to 1993 that are comparable: 2006-07-08 40.1% and 1995-96-97 32%.

Similarly,

Total construction spending growth for the 3 years 2014-15-16 could reach 30%. I forecast 9.7% growth in 2016.

Only 3 year periods back to 1993 that are comparable: 2003-04-05 29% and 1998-99-2000 25%.

Well, there is one more comparable. The last three years of total construction spending growth for 2013-14-15 was up 27%, so this expansion is already ranked 2nd.

What we see here is the 1st or 2nd most active 3 year period of growth in construction on record back to 1993, and it’s already been happening for two or three years.

For perspective, residential spending for 2013-14-15 grew 46%! Similar only to residential spending in 2003-04-05 at 48%.

Welcome to the new year. So let’s go see if we can break some records.