5-8-20 The jobs report today shows construction lost 975,000 jobs last month.

AGC forecasts “virtually no new private starts except pandemic-related and emergency repair work.” This is probably the most pessimistic of forecasts but let’s look closer. Private construction comprises 75% of all construction work, but residential is 40% out of the 75%. In some cases residential work was allowed to continue, perhaps leading to a continuation of residential starts. Healthcare, Office, Warehouse (in Commercial/Retail), Data Center (in Office), Transportation and Manufacturing (Industrial) all have a large share of private work and all may include some critical projects for which starts may proceed. So, a large portion of new private starts might proceed.

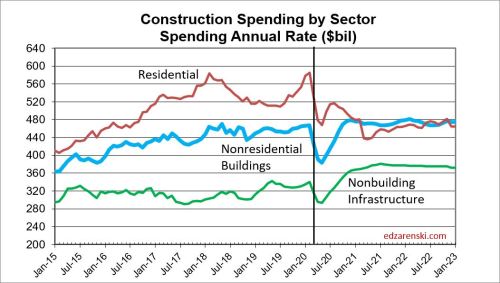

Dodge forecasts new residential construction starts in 2020 will end down -12%, commercial (90% private) down -16%, institutional (50% private) down -7%, Manufacturing/Industrial (100% private) down 22% and Non-building (40% private) down -16%.

ConstructConnect forecast for 2020 construction starts; Residential -29%, Nonresidential Buildings -32%, Non-building Infrastructure -17%. Total Construction starts for 2020 down 27%.

AIA Consensus of eight construction firms 2020 construction spending forecast for nonresidential buildings : Commercial -14%, Institutional -7%, Total Nonresidential Buildings -11%.

CBRE Research reported 70% of total under-construction industrial space nationally remained active. Most of these projects were deemed essential.

Here’s a sampling of Dodge construction starts through March for ten areas: Houston-Baytown-Sugarland, Phoenix-Mesa-Scottsdale, Ohio, Atlanta-Sandy Springs-Marietta, Boston-Cambridge-Quincy, California, Florida, New York-Northern New Jersey-Long Island, Pennsylvania, Seattle-Tacoma-Bellevue. These ten areas represent about one third of all U.S. construction starts. Compared to the same period 2019; Total construction starts are down 3.5%; Nonresidential Buildings down 2.5%; Non-building down 3.5%. Residential starts are up 10%. Only Seattle posted a decline in residential starts.

From March 15th to April 12th, construction lost 975,000 jobs, 13% of the workforce. Not shown in the jobs plot below is that hours worked dropped 3%, so the total work output dropped 16%. Construction Unemployment, which was recently below 5%, as low as 3.2% in summer 2019, is now at 16.6%. The next jobs report covers the period from April 13th through May 17th. Expect more downward movement in the jobs numbers.

The U. S. Census March construction spending forecast was UP. It should not be up. I’ve stated this could potentially be due to insufficient real data input and more dependent on typical spending curves to fill in the blanks due to lack of response with real hard data input. I expect downward spending revisions to the March data. Here’s two examples to support my expectations:

- In any given month about 15% of Residential construction spending comes from new starts that month. March Not Seasonally Adjusted (NSA) spending is historically 15% higher than Feb. But March backlog (without any project delays) was level, new starts in $ increased only 8% and new starts # of units fell 22%, yet March reported residential spending still increased 15%. With a level backlog (which assumes no shut downs) and a new starts below par, residential spending for March should not have increased by the normal historical amount.

- Total NSA construction spending in March increased 9.6% from Feb, historically it would increase 10.5%, so that seems normal. However, in the last two weeks of March it is estimated workforce declined by 300,000+, 4%. It is unlikely construction recorded a 4% boost in productivity in Mar.

There still is little hard data to go on, but based on what I’ve gathered to date, here is my Construction Analytics latest forecast.

Work in backlog that has been delayed, minimum 2 month delay, restart build up over a period of 8 months; Residential -30%, Nonresidential Buildings -28%, Non-building Infrastructure -22%, Total Construction delays -25%.

Work in backlog that has been canceled, Residential -3%, Nonresidential Buildings -3.4%, Non-building Infrastructure -2.2%, Total Construction backlog canceled -2.8%.

New Construction Starts in 2020 canceled, Residential -15%, Nonresidential Buildings -8%, Non-building Infrastructure -11%, Total Construction starts canceled -11%.

Construction Spending Forecast 2020 – Residential -2%, Nonresidential Buildings -4%, Non-building Infrastructure <-1%, Total Construction Spending 2020 -2.3%.

The loss of 975,000 jobs in a single month (if all jobs were lost for a full 30 days), at a rate of 60,000 jobs needed to put-in-place $1 billion in construction in one month (5000 jobs per $1bil pip/yr), equates to a loss of $16 billion in spending between March 15th to April 12th. Normally in this period spending would be $100 to $105 billion. We won’t see the hard spending data for this period until June 1st with first revision July 1st. A $16 billion drop would equate to a 1.25% decline in annual construction spending.

A recent AGC survey of contractors indicates:

- 50% of respondents said an owner halted current work

- 67% are experiencing project delays/disruptions

- 49% said suppliers had notified them deliveries would be delayed or canceled

- 28% reported that an owner canceled an upcoming project

- 35% laid of workers

Just keep in mind, this is a survey of companies responding they have experienced these issues. It IS NOT an indication that 50% or 67% of all construction projects are halted or delayed. If a contractor has 10 ongoing projects and experiences a delay on three of them, or even one of them, he would have answered affirmative in the above survey. As an example, 35% of respondents reported they laid off workers and today’s jobs report shows the workforce dropped by 13%.

ConstructConnect has compiled a list, by state, of construction projects that have been delayed or canceled. From this list you can get an idea of the number of projects that have been delayed or canceled, but you cannot determine the amount or $ value of work that has been delayed or canceled. To get that level of detail, you would need to know the schedule for each job, the start date/end date and the amount of work already put-in-place.

There are no standard means of capturing the duration of delays or the $ value of delays or cancellations from backlog. We may never know the total value of work delayed/work canceled. This is what makes current forecasting so difficult.

See also these articles for all the analysis to date on the Impact of the Pandemic.

Pandemic Impact on Construction – Recession in 2020?

Pandemic Impact on Construction – Part 2

Pandemic Impacts – Part 3 – Jobs Lost, Inflationary Cost

Pandemic Impact #4 – Construction Jobs Recovery

Ed, what a great blog. One of the most analytical outlook on the severity of AEC sector in the next coming months. Time to brace up to weather through the downturn.

LikeLike