8-16-22

Construction Spending data updated 8-16-22, actual Year-to-Date through June, Census issued 8-1-22.

Forecast based on starts through July. Residential starts peaked in Feb-May 2022. Residential starts in July are down 15% from the highs reached in the 1st five months of 2022. Nonresidential Bldgs annual rate of starts reached a remarkable new high in July, almost 50% higher than the average of the 1st six months of 2022, and 30% higher than the previous single-month high in 2018. Non-Building starts for July reached 125% higher than the average of the 1st six months of 2022, and 50% higher than the previous high in 2019.

Watch for future revisions in Manufacturing Starts data. Through July, Mnfg starts are up 180% over the same seven months in 2021. It won’t be up 180% at year end. This may not yet be fully reflected here. This will add to spending mostly in 2023 and 2024. Also watch Power/Utilities which posted a 60% gain in the 1st seven months over same period in 2021.

Keep in mind, only time will tell how much of those huge gains in Mnfg and Power starts are a real increase in the amount of new work started or how much of that gain reflects an increase in the share of the market captured in the starts survey. Over the past 10 years, Dodge total starts data captured amounts to only about 40% to 50% of the final spending amount for these two markets.

Construction Starts forecast updated to 8-16-22

Construction Backlog forecast 8-16-22

After a two-year slowdown in backlog growth in 2021 an 2022, growth resumes in 2023 and 2024. Nonresidential Buildings leads in 2023, Nonbuilding leads in 2024.

Watch for this temporary decline in spending over the next few months. Some lower months of residential starts over the past nine months reduces residential spending from May to Sept 2022 before it returns to growth. More moderate declines in Nonres Bldgs and Nonbuilding also contribute to the downturn. Declines generally turn into gains by Q4 2022.

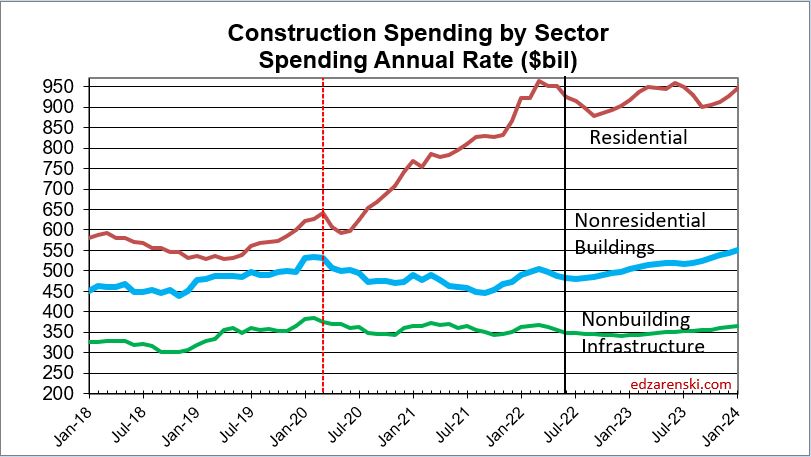

Much of the gains in spending in 2022 and 2023 reflects the very large increases in inflation. Spending after inflation, or volume of work, shown below, declines for all nonresidential in 2022 and declines for Nonbuilding and residential in 2023.

Residential volume peaked in Q1 2022 but will not return to that level until 2025. Both Nonresidential Buildings and Nonbuilding Infrastructure volume peaked in Q1 2020. Neither returns to that level before 2026.

Volume of work (spending minus inflation, or Constant $) has been dropping for several months and will continue to drop for several more months. But jobs have been increasing. Over the long term these two data sets should move in tandem, not in opposition. As greater separation between these two occurs, with jobs over volume, the productivity factor for the amount of work put-in-place per job worsens. That is a hidden factor adding to inflation.

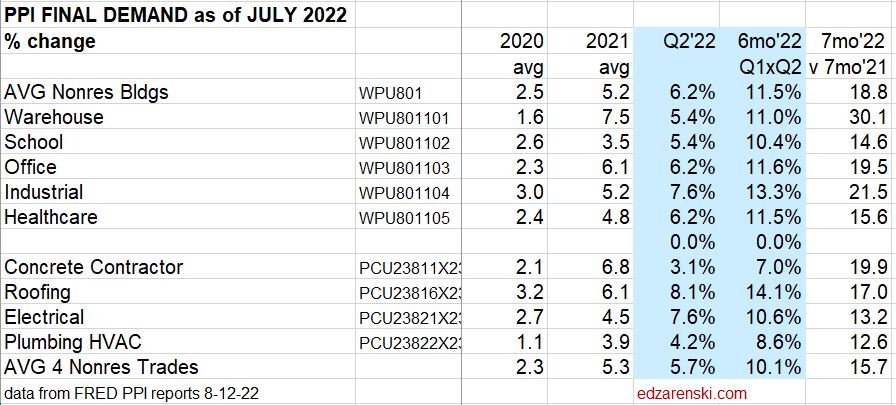

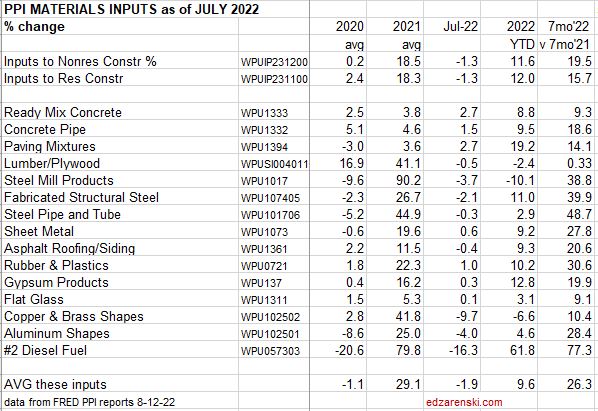

See the PPI post for details on 2022 PPI data.

This month the July update to the Final Demand indices reflects that this index barely moves for two months, then in the third month, when Census performs a contractor survey to update the index, it moves 80% to 90% of the index value for the three months. The same has been true looking back over all recent quarters. Takeaway: the Final Demand indices cannot be used monthly. Essentially, these should be considered a quarterly index. Here I’ve calculated Q2 and Q1xQ2. You can 4x or 2x those results to get an annual rate, but I suspect most of the increase is already in this year, so Q3 and Q4 I’d expect to be lower than Q1 and Q2.