Construction Spending March 2021

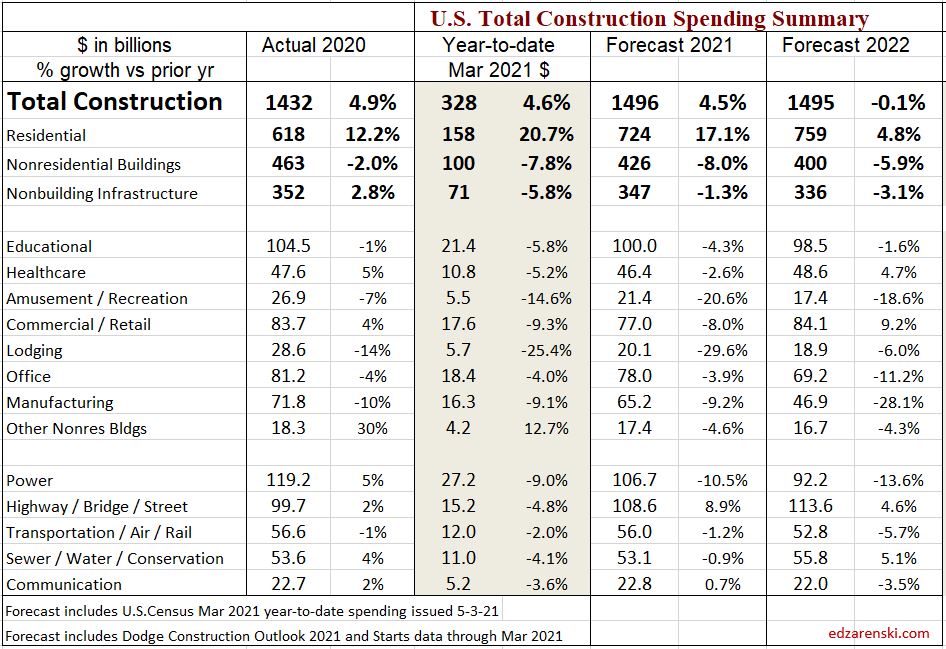

Total ALL construction is up ytd 4.5%. Except for Residential which is UP 21% ytd, and Public Safety, up 14% ytd, every other market is down ytd. In total, Nonres Bldgs is down 8% ytd and Nonbldg Infra is down 6% ytd.

In the 1st 3 months of 2020, spending had reached an all-time high averaging a SAAR of $1,461 billion.

In the 1st 3 months of 2021, spending is at a new all-time high averaging a SAAR of $1,527 billion.

By more than 2:1 margin, nonresidential markets declined in Mar from Feb. Markets that declined make up 80% of the $ value of all nonresidential work. Year-to-date, 14 of 16 nonresidential markets, 95% of total market value, are down.

In current dollars, ytd 2021 spending is $328 billion vs $314 billion in the 1st qtr 2020. Residential gains overcompensate for nonresidential losses.

For the next few months the year-to-date comparison is going to increase due to the fall-off in spending throughout 2020. However, the strong growth in residential will skew results. Residential spending will climb to +27% year-to-date by June and July (due to the steep decline in spending in 2020) before falling back to +17% ytd by year end.

https://census.gov/construction/c30/pdf/release.pdf

This table includes updated forecast for 2021 and 2022. Forecast has increased since January, mostly in residential. Dodge has revised its forecast for construction starts and census reported spending through March is included. Dodge forecast includes increases for infrastructure projects. However, infrastructure will add less than 1% to 2021 spending.

A typical batch of new construction starts within a year gets spent over a cash flow schedule similar to this, 20/50/30, that is 20% of all starts in 2021 gets spent in 2021, the year started, 50% in the next year and 30% in years following. However, if (infrastructure) starts don’t begin until the 2nd half of the year, only 25% to 30% gets spent in the 1st year. Therefore, even if $100 billion in new infrastructure starts begin in the 2nd half 2021, only 25% x 20% or only about 5% would get spent this year. That’s $5 billion, or less than 1% of annual construction spending.

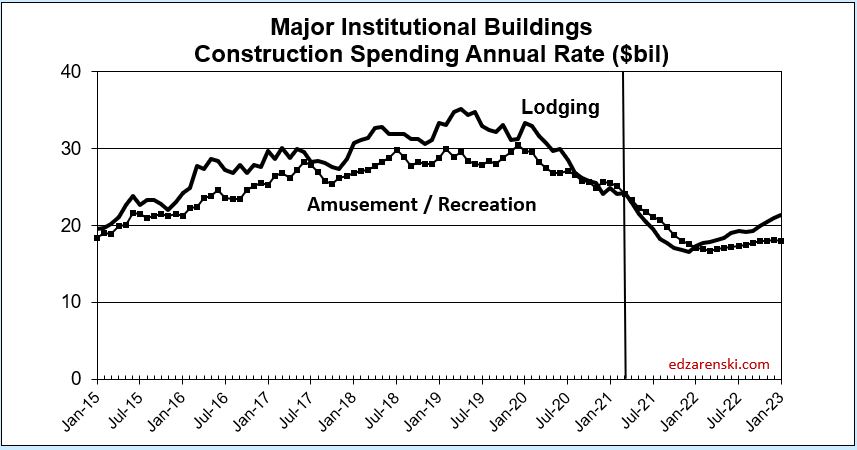

The impact of reduced starts in 2020 is starting to show up in the 2021 year-to-date results. Total Nonres Bldgs starts were down 22% in 2020, Nonbldg Infrastructure down 13%. Some of these markets will be affected by a downward trend in spending for two to three years. 2020 starts for select markets:

- Amusement -38%

- Commercial/Retail -14%

- Office -20%

- Lodging -50%

- Manufacturing -57%

- Power -38%

The greatest downward impact on spending will be felt in mid-2021. Over the next 9 months, every sector will post more down months than up months, although the declines will be most noticeable in nonresidential buildings.

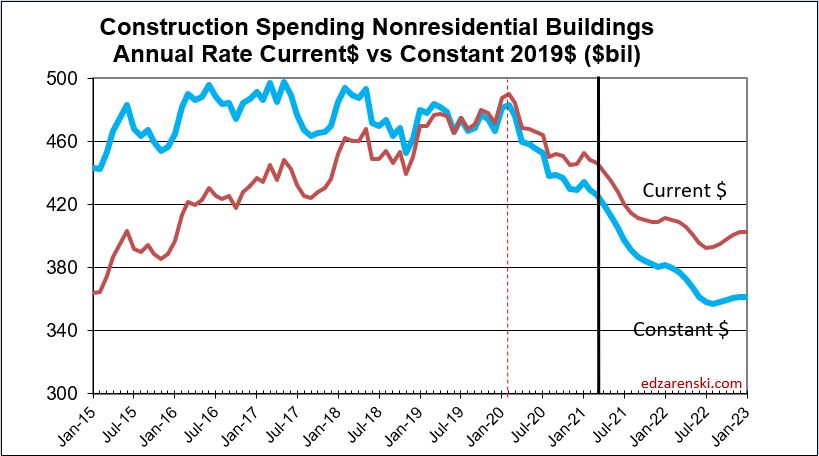

Nonresidential Buildings construction is going to take a lot longer to recover than you might think. The deficit from lost starts in 2020 has not yet hit full impact. After adjusting for inflation, volume is down much more than spending. Nonres Bldgs volume will decline 11% in 2021, the 5th consecutive year of volume declines. Jobs are driven by changes in volume.

5-7-21 Jobs report > Construction Jobs for April posted no change. Although residential spending and volume gains have been helping create jobs, nonresidential volume declines are holding gains in check. Jobs are now 200,000 lower than February 2020.

A more accurate window into jobs compares jobs x hours worked for total labor hours input. YTD through March, jobs x hours was down 3% from same period last year. But in April, even though there was no gain in jobs in Apr 2021, the YTD performance changed from -3% to +1%, entirely due to April 2020 when jobs dropped off a cliff. The real picture in jobs is much closer to the -3% through March than the +1% through April. The spending/volume forecast is projecting total jobs for 2021 will end the year down less than 1% from total jobs in 2020, but by Dec 2021, year/year jobs will be down 6% from Dec 2020.

See Measuring Forecasting Methodology & Accuracy for a comparison of firms’ initial 2021 forecast vs year-to-date spending.